Italian Banks: The Phantom Menace

by: And Value for All

- A recount of what happened and is happening to the Italian financial system.

- EU regulatory framework in place can regulate the banking crisis, yet Italy is trying to avoid compliance.

- Despite recent happenings, the system will hold, thus enterprising investors might consider bargain opportunities on the market.

- EU regulatory framework in place can regulate the banking crisis, yet Italy is trying to avoid compliance.

- Despite recent happenings, the system will hold, thus enterprising investors might consider bargain opportunities on the market.

Sometimes I forget that, even if I am a business graduate and an investor for quite some time now, my first love has been actually economics. When I do remember though, I still amuse myself spending time trying to understand broad economic issues and their impacts on people, businesses and countries. These days, I am reading with interest about the recent "Italian banking crisis". As I read more and more comments and some article referring to the issue here on SA during the last days, I gradually convinced myself that it might have been a good idea, as an investor, an Italian and a SA contributor, to share a couple of thoughts with the community about it. Here is a brief account of how it went so far and a few takeaways for investors.

Is this really a new crisis?

The failing status of Italian banks is nothing new. It has been an ongoing domestic problem for at least six years now: a never solved vicious issue that has recurrently appeared on the news in a big yet fragile economy that has never really recovered from the 2008-2009 crisis.

These days, because of the international scrutiny raised by some media outlets and IMF reports, the government's "decree to save banks" made its way back to headlines and everyone's mouth. The amazing fact is that, if you make a Google search (in Italian) on the issue, the first headline about a "decree to save banks" is dated December 2011. In fact, it was 2011 when the Italian government of PM Mario Monti passed a decree aimed at supporting troubled banks through state aids. The legislation, approved as a part of a broader financial maneuver for the next year, assigned the role of guarantor of subordinate bank bonds to the already debt-plagued Italian state. It also gave the possibility to intervene in covering banks debts with the issuing of new equity financed by the state.

In 2012, Monte dei Paschi di Siena (OTCPK:BMDPY) - from now referred as Montepaschi in the article - became the first large bank to effectively take advantage of the government decree. The bank was not new to state aids though, having recently benefited from similar measures already under the Berlusconi government. The ECB, guided by Governor Mario Draghi, reluctantly granted permission to the Italian government to give away an already approved help package of 4 billion euros.

At the end of 2013, UBS already estimated that the amount of non-performing loans (NPLs) of Italian banks topped 243 billion of euros, with one of the worst risk covering indexes in Europe.

Two months before, IMF had already warned that Italian banks were facing a potential loss of 125 billion euros on corporate loans alone, but the "financial sector was still solid". At the time, international scrutiny was all on Spain, so Italy somehow managed to get away with it.

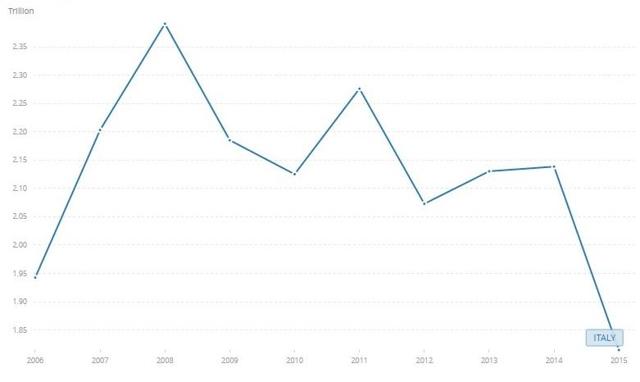

The 2010 Basel III agreement, which included strict rules on NPL coverage ratios and bank's capital adequacy was also supposed to come into effect starting this year and be fully deployed by 2015, but subsequent changes deferred implementation until 2018 and then again to 2019. It was a strong call to action, but delays helped the new Italian PM Enrico Letta to keep avoiding structural reforms in financial sector and to concentrate in selling the fairy tale that economy was recovering to investors abroad and voters in Italy. Readers are left with the hard task to find growth and economic recovery looking at this Italy GDP graph.

Italy GDP 2006-2015 (current USD trillions)

(Source: World Bank database)

(Source: World Bank database)

In the meantime, Italian banks were becoming very efficient covering NPL and various inadequacies with false accounting practices. This was the first "Italian Job" that international media outlets could have cared about. In fact, by beginning of 2014, prosecutors were taking judicial actions for false accounting and other malpractices against Banca Etruria (March 2014) and Banca Marche (April 2014). Hearing about the competitors' disgrace, Italian mid-sized lender Banca Popolare di Vicenza started to plan the acquisition of Banca Etruria. A not-so-smart move by the management to put itself on the spotlight since it was later prosecuted for similar malpractices as well. Later the same year, government was starting to plan the salvage of troubled Banca Marche while Montepaschi and Banca Carige (OTC:BCIGY), another medium sized player, failed to pass the ECB stress tests evidencing more weaknesses in the system as a whole. Despite adequate domestic media coverage, many financially illiterate household savers kept subscribing subordinate bonds of the aforementioned lenders.

The situation was domestically downplayed, but it just kept getting worse, and by mid-2015, roughly one year later, four banks went bust. These were the already cited Banca Etruria and Banca Marche and other two small lenders, CaRiFe and CariChieti, which were also already under judiciary compulsory administration for irregularities emerged in 2013 and 2014.

However, the cases of Banca Marche and Banca Etruria ended up to be particularly problematic to handle because the forceful clean-up had to start after January 1st, 2015. What happened in the meantime? The new EU Bank Recovery and Resolution Directive (BRRD, or "bail-in" directive) came into effect.

To make a long story short, the directive forces shareholders and bondholders to step in and effectively "bail-in" banks in the event the institution becomes insolvent. Not only shareholders, but also bondholders of Banca Etruria and Banca Marche became among the first investors in Europe to experience the effects of the new European regulation. In theory, there's nothing bad if bondholders take the risks of their investments. The problem was that, in a country where households' main financial advisors are the bank clerks, Banca Etruria and Banca Marche employees were selling their banks' subordinate notes to small savers, including pensioners with no financial knowledge whatsoever, well over the portion that should be allowed in any diversified portfolio. Small savers "Mario the plumber and his friends" lost their lifetime savings, thanks to the BRRD in order to save the banking system. You can imagine the degree of social mess that followed.

The current situation

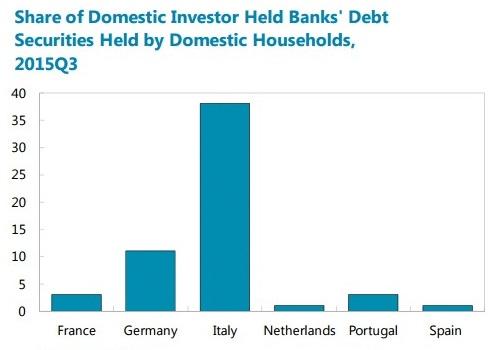

Despite the scars of Banca Etruria and Banca Marche bondholders, brave Mario the plumber and friends are still heavy buyers of other Italian banks' securities.

(Source: IMF publication)

In the meantime, non-performing loans have reached a record high 360 billion of euros, 18% of the total lending. Although the figures have been suddenly showcased with great emphasis and worry, Moody's was looking with cautious optimism at the same figures six months ago, well before the media spotlight. At the time, the rating agency was giving a hopeful outlook on the issue by informing investors that something was moving at the political level (article here).

We can therefore trust Bank of Italy governor's recent declaration that "they (non-performing loans) are not an emergency". Even if the NPL ratio is a problem for Italy, the issue has been known all along by the institutions and professional investors. Increased international scrutiny may turn to be the driving force to push forward a solution. However, reminders from EU officials to act within the BRRD framework obstruct the efforts of the heavily indebted country to find alternative solutions.

The main issue with Montepaschi and the lenders in real trouble which are however only a portion of the whole sector is actually of political nature. Italy's PM, Matteo Renzi, who has been even more active than his predecessors selling the tale of the recovering Italy to international investors and Italian voters, is saddened by the issue as he faces an important ballot in fall. He is domestically pressed to find alternatives and might somehow manage to sell the necessity of state aids to the Italian population as a new "financial stabilization measure," but he has hard time to sell it to the EU. The Union has already indicated that it would not tolerate further state aids, and EU officials know well that the BRRD mechanism could solve the Italian issue again if such necessity arises.

Still, Renzi is battling to avoid to comply with the bail-in directive following Banca Etruria's mess of last year. More money-stripped Mario the plumber and friends means more angry voters, and this could pose a serious threat to the Renzi's popularity and career, especially since Montepaschi is a regional bank of Tuscany, a vote powerhouse of the PM.

The last government-backed initiative has been the backing of a PE fund (the Atlante Fund) whose primary function is to recapitalize troubled banks and buy NPL. However, the small size of the fund (5 billion euros) has only allowed to focus on the recapitalization issues.

Government and banks are consulting on how to enlarge the size and scope of the fund. It is speculated that the main actor in this new phase would be Cassa Depositi e Prestiti, which is however nothing less than a state-owned bank (80.1% shares controlled by Italian government). Since this is just another badly covered direct public aid, it remains to be seen how the EU will react. IMF is more flexible on the issue of state intervention, but it is also pushing Italy for deeper reforms on the bankruptcies and judicial recovery.

Since current regulations make judicial recoveries a difficult practice, Italian NPLs have been trading at a discount compared to European peers on the specialized market, making them harder to be sold without large write-offs and contributing in penalizing Italy's position within the EU.

Because of the "phantom menace" of the BRRD directive, shareholders and subordinate bondholders of Italian troubled banks are now reasonably worried. Bank's equity and bonds issued exceed NPL by a large amount, so there is limited risk for the economy as a whole in the short term. Nevertheless, the fear of an upcoming bail-in is the main driver behind the stock's free-fall not only of Montepaschi and Carige, but also of UniCredit (OTCPK:UNCFF), Italy's biggest lender, and Intesa (OTCPK:ISNPY). Intesa has however a better coverage ratio and usually performs well on ECB stress tests, so the downside of the stock so far has been somehow limited compared to peers.

A few takeaways for investors

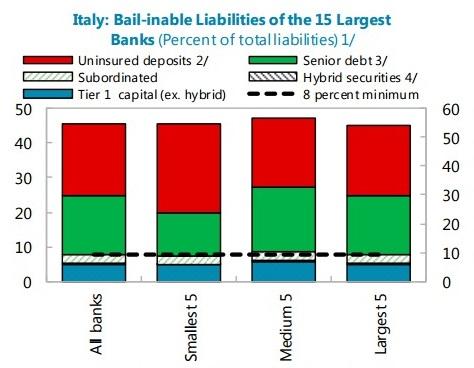

The Italian banking system is not on the verge of collapsing. Should all the worst hypothesis come true (all NPL being written off and bail-in eating household savings again), the system would not collapse. This is hardly a real scenario as at least some impaired loans will be in the end recovered, thus the system would remain solvent if NPLs rise even further than 18%. You can take a look at IMF data and judge by yourself: the bail-in-able capital is well above the NPL level.

(Source: IMF publication)

Corporate bankruptcies in the country peaked in 2012, suggesting the country is still in pain yet somehow better off now than few years ago, or at least more solvent. It is highly unlikely that NPLs will go far higher from the current levels. They have gone so far because bank malpractices were not changed, but this is hardly to continue much further. Taken all these points, it is undeniable that banking problems are an issue today, but Italy is getting more and more pushed by the international community to swiftly address its financial system problems.

In the current situation, substantial risks remain for shareholders and bondholders of the institutions cited in the article. Conservative investors seeking the highest level of safety might be therefore better off avoiding Italian banks at the moment, but more enterprising ones, while avoiding the most troubled issues, might bet on the stabilization of the sector. These investors can seek bargains in representative household names which have been strongly beaten down but maintain a good NPL coverage ratio such as the cited banks, Intesa Sanpaolo, and UBI Banca (OTC:BPPUF), another major player in a relatively better position than competitors.

As Mr. Market, in such situations, always penalizes the sector as a whole, possible bargains are likely to be found also in quality issues such as Banca Mediolanum (OTCPK:MDLAY). The Bank (I would say, this bank which is associated with former PM Berlusconi) has relatively low exposure to the problem and has been suggested as a new possible shareholder in the Atlante Fund. Another institution in good financial shape is Banca IFIS [BIT:IF], which has been actively trading NPL of other banks and has been quite profitable in the activity, thanks to its competent management. Similar considerations apply also to Fineco Bank (OTC:FCBBF).

Banks traditionally related with insurance businesses such as Unipol (BIT:UNI) and Banca Generali (BIT:BGN) are also definitely interesting choices which have experienced huge sell-offs during the last year because of sector fears. They may definitely trade at compelling valuations for investors seeking some safety and an interestingly high dividend yield. In particular, Unipol, after reinstating dividend payments in 2012 (suspended during the worst crisis years 2009-2011), has been raising them each year since, and the yield is currently 7.4%.

As Baron Rothschild's quote goes, "buy when there's blood in the streets". For Italian banks, that time could be now.

0 comments:

Publicar un comentario