by: Tiago André

- There are always two valid opposing views of each data set; the pessimistic and the optimistic.

- As important as the (bullish or bearish) argument is the person making the claim.

- What are the odds that some of the best investors of our time are all plain wrong at the same time?

- Is it worthwhile to chase risk at these levels?

- As important as the (bullish or bearish) argument is the person making the claim.

- What are the odds that some of the best investors of our time are all plain wrong at the same time?

- Is it worthwhile to chase risk at these levels?

A Brief Story

There was once this shoe entrepreneur who was interested in selling his products in Africa. So, he sent his two sale executives to the continent in order to do the necessary market analysis.

The first one came back and said: "Very bad market, nobody has shoes".

The second one came back and said: "Very good market, nobody has shoes".

In fact, very different (even opposite) conclusions can be taken from the exact same data.

The Bull & Bear Debate In Financial Markets

Financial markets are not different from the previous story, and at any point in time, there are always valid reasons to be bearish or bullish over any asset. Listening to the arguments from both sides is important before making your own mind. But the person who makes those arguments is also determinant.

Taking the initial story as an example, what if I told you that the first executive had a proven long track record in identifying new prosperous markets for the company while the second one was just starting his career? Should the shoe entrepreneur favor the first executive's view on Africa?

This brings me to my point in this article: What are some of the best investors of our time saying and doing?

What Are The Industry Experts Saying And Doing?

Don't worry, I won't be covering Goldman Sachs's (NYSE:GS) claim of a 10% drop in equity markets in the coming months.

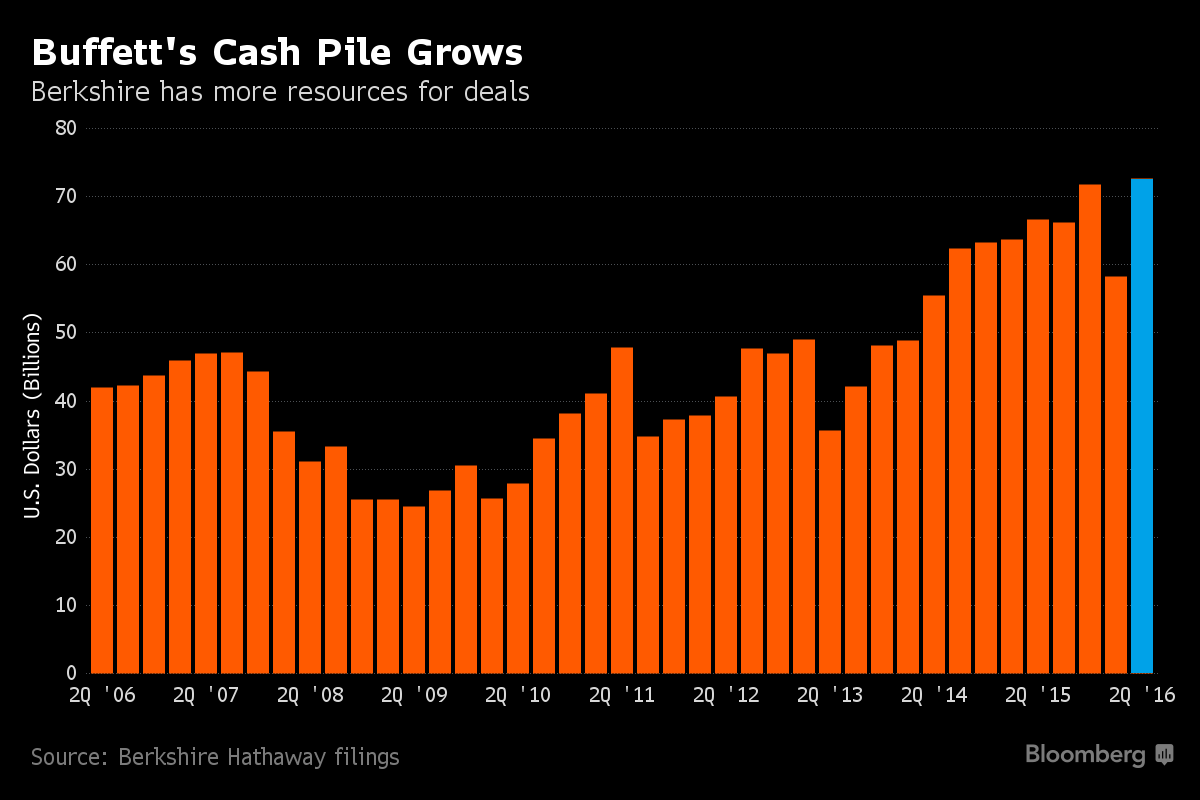

I will start with Warren Buffett. Berkshire Hathaway's (NYSE:BRK.A) (NYSE:BRK.B) cash pile jumped to a record high of $72.7 billion in June 30. Not less impressive is the $14.4 billion increase from March 30.

Source: Bloomberg

Source: Bloomberg

Could this mean that the Oracle of Omaha is finding it hard to spot good deals at current market valuations? Maybe he's just being coherent with one of his lessons: "Be Fearful When Others Are Greedy and Greedy When Others Are Fearful".

Bill Gross, the Bond King, doesn't like bonds (who does anyway?). On his August letter to investors, he says, "I don't like bonds; I don't like most stocks; I don't like private equity. Real assets such as land, gold, and tangible plant and equipment at a discount rate are favored." He recommends investors to "reduce risk and accept lower than historical returns." At the same time, he warns that "negative returns and principal losses are increasingly possible".

The King of Bonds, Jeffrey Gundlach, shares the same view. Known for his bold calls, he puts it simply: "sell everything". In fact, he is "not interested in treasuries" as "you don't make any money," "the risk-reward is horrific" and "there is no upside." On stocks, he says that "the stock markets should be down massively but investors seem to have been hypnotized that nothing can go wrong."

But as "things are shaky and feeling dangerous," Gundlach says: "I am not selling gold."

George Soros is back to trading with a strong view on where to put his own money. He bought a 1.7% stake in Barrick Gold (NYSE:ABX) and increased his allocation to gold; at the same time, he slashed his holdings of US equities.

His former chief strategist, Stan Druckenmiller, has the same bearish outlook with gold being his largest currency allocation as central banks experiment with the "absurd notion of negative interest rates." On equities, he thinks that "higher valuations, three more years of unproductive corporate behavior, limits to further easing and excessive borrowing from the future suggest that the bull market is exhausting itself."

Carl Icahn discloses that even though he owns a lot of companies, he has a "built in edge" so that he's "net short." On current asset prices, he says, "I don't think you can have near zero interest rates for much longer without having these bubbles explode on you."

Another billionaire investor, Paul Singer, is also "bullish on gold, which is the anti-paper money, of course, and is under owned by investors around the world."

What's The Common Denominator?

All these investors share a bearish view on bonds and equities in general and most of them also have a bullish view on gold - GLD, DGP, GTU, IAU, PHYS, UGL, SGOL.

We all know that the Oracle of Omaha doesn't like gold as "it doesn't do anything but sit there and look at you." Still, Berkshire Hathaway's record cash pile shows his cautious stance towards bond and stock prices at the momento.

Could All These Legendary Investors Be Wrong?

We're all humans, we all had our share of bad investment decisions, and even these legendary investors are no exception. But given their top-tier track records over the past decades, what are the odds that they are all plain wrong at the same time?

As the shoe entrepreneur, you have to make your own mind. As always, both bulls and bears have valid arguments and make it hard to decide. Maybe, knowing the person behind the claim will help you make the right decision.

What If They're Wrong Before They're Right?

We all know timing is important, and markets can be irrational longer than you can remain solvent.

But, as Carl Icahn said, "it's ridiculous to think anyone can always get it right in the short term."

Also, as Paul Singer reminds us, "if you break even in a bear market or crash or financial crisis, you're way ahead of the game."

So, why should anyone be chasing risk for mere single-digit return at these levels? Shouldn't we all be doing the opposite?

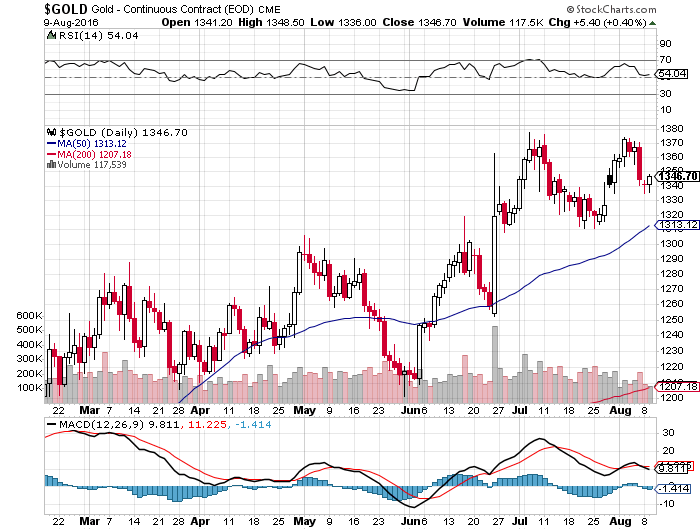

Why Gold And Why Now?

As I mentioned in The Money Printing Drug, Gold Prices and Central Bank Policy and in Gold: Beyond Brexit, gold thrives in this environment of quantitative easing, monetary expansion, negative real (and sometimes even nominal) interest rates and high public and private debt to GDP. In fact, there are plenty of reasons to be bullish on gold in the long run.

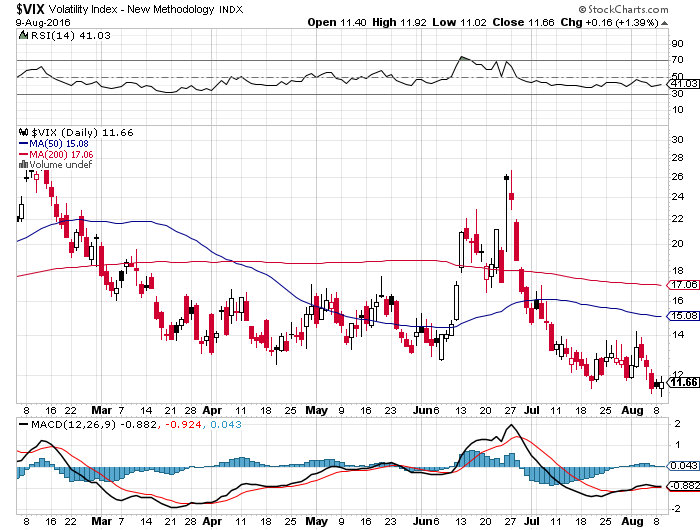

In the short term, gold works as a buffer in your portfolio whenever there's a jump in volatility.

With the VIX at historical low levels, the recent pullback in gold prices is offering a good entry point to investors.

Source: Stock Charts

Source: Stock Charts

0 comments:

Publicar un comentario