As Long As The Music Is Playing, Should You Keep Dancing?

by: William Koldus, CFA, CAIA

- Stocks and bonds have been moving up together, and they have been positively correlated, particularly since 2011.

- Commodities, commodity stocks, and emerging market equities were out of favor from 2011 to 2015, but they have joined the party.

- Who will stop dancing first?

- Commodities, commodity stocks, and emerging market equities were out of favor from 2011 to 2015, but they have joined the party.

- Who will stop dancing first?

"When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you've got to get up and dance. We're still dancing."

Chuck Prince, July 10th, 2007 (Former Citigroup CEO)

"There's a trick to the 'graceful exit.' It begins with the vision to recognize when a job, a life stage, (an investment cycle) or a relationship is over - and let it go. It means leaving what's over without denying its validity or its past importance to our lives. It involves a sense of future, a belief that every exit line is an entry, that we are moving up, rather than out."

- Ellen Goodman

Introduction

Chuck Prince had a valid, ill-timed point with his infamous quote in July of 2007 (which is requoted above the Jack Vettriano "Waltzers" painting above). It easy now, with the benefit of hindsight, to go back and critique his statement, which ultimately proved to be one of the indelible markers, that signaled the top was in for asset prices.

Mr. Prince clearly did not have his handle on the situation, and he badly shirked his responsibility to his shareholders to be a steward of their capital. But in his defense, it was his job to have Citigroup (NYSE:C) compete against Bank of America (NYSE:BAC), Barclays (NYSE:BCS), Fannie Mae (OTCQB:FNMA), Freddie Mac (OTCQB:FMCC), Goldman Sachs (NYSE:GS), JP Morgan Chase (NYSE:JPM), Morgan Stanley (NYSE:MS), Wells Fargo (NYSE:WFC), and countless other competitors and peers. These firms were all jockeying for market share in the robust housing and investment banking end markets.

Once the music stopped in 2007, however, there were few places to hide, as almost all asset prices, from homes to commodities to stocks, had been bid far higher than their underlying intrinsic values.

Overvaluation is an almost universal theme at the end of most bull markets, and its symptoms are especially dangerous when a bubble has developed, as crowd psychology takes hold to drive prices to unstable extremes.

The purpose of modern central banking should be to serve as a check and balance in theory, but that is rarely the case in practice, as human emotions often override the correct policy decision. Building on this, the asymmetric approach to busts and bubbles by the current generation of central bankers, who stand aside while excesses build and then rush in when there is a panic, was fully on display in 2007.

Looking back at Mr. Prince in 2007, the crux of the problem was that he, and many others, did not know that the party was already ending. With the benefit of hindsight, we know one of the few safe-havens was sovereign bonds, particularly U.S. Treasuries. They protected portfolios and increased in value during the climatic bear market that roared throughout 2008 and into 2009.

With the music blaring today, and the party even bigger than its predecessor, the dance floor is once again full with investors who feel invincible. Good news is good, and bad news is sometimes better, as it provides cover to increase global liquidity levels by eager central bankers. In this environment, with stocks and bonds at historical highs, what happens when the music stops?

Thesis

Both bonds and stocks are historically overpriced, and projected returns for a traditional 60/40 or 70/30 portfolio are among the worst in modern financial market history.

Bonds & Stocks Are Both Overvalued

Rarely in history have both stocks and bonds been as overpriced as they are presently. I have articulated this observation throughout much of my writing over the past year and a quarter.

Yet the excessive valuations have improbably grown after most of the world, with the notable exception of U.S. large-cap stocks, experienced a verifiable bear market that culminated in a sizeable decline in February of 2016.

The subsequent rally after this important market low, in both stocks and bonds, has reduced long-term real return expectations, from already abysmal levels. This is illustrated by a table that I have put together using underlying data from GMO, which I have been periodically updating for the last 16 years.

.

Expected real returns over the next seven years for U.S. stocks, according to GMO, are -2.7% annually for U.S. large capitalization equities, and -1.1% annually for U.S. small capitalization equities. Adding credence to GMO's forecast is the near universal conclusion by a variety of different broad valuation metrics, which similarly forecast future returns for the next decade to be near zero, or below zero on an annual basis.

While the return expectations for equities are historically low, the expected real returns for U.S. Treasuries and International Government Bonds are even worse, projected at -2.2% annually, and -4% annually, for the next seven years. In summary, as bad as it looks for stock investors, bond investors are likely to have a more treacherous path over the next decade from the current valuation starting point.

The Stock Market Has Upside Momentum

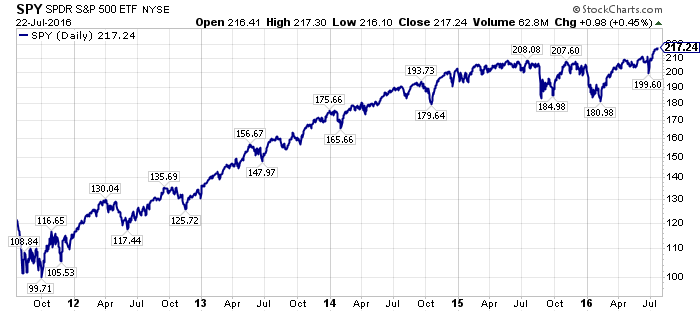

Momentum is currently with the stock market bulls, and I can envision a higher probability scenario, where the S&P 500, as measured by SPDR S&P 500 ETF (NYSEARCA:SPY) rises roughly 20%, from its previous all-time, which had occurred in the summer of 2015. As of this writing, SPY is already nearly 5% above this previous high, as the chart below illustrates.

The S&P 500 Index is rallying in the face of four consecutive quarterly declines in earnings.

This shows that either the market is in a blow-off speculative mania, or that future earnings will rise more than most analysts expect and the stock market is working as a discounting mechanism.

The Sovereign Bond Market Has Upside Momentum Too

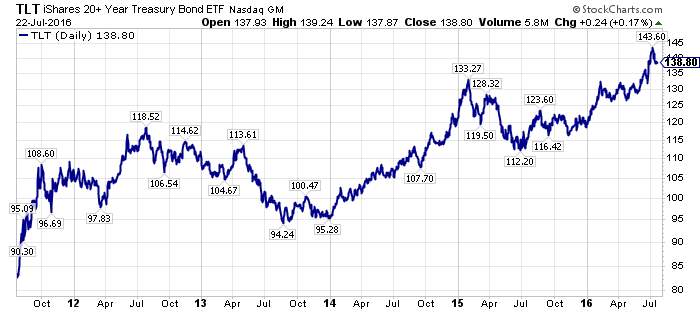

Compared to equities, where a credible case can be made on relative valuations versus bonds, it is hard to envision a scenario where long-term U.S. Treasury Bonds continue rising alongside increasing equity prices.

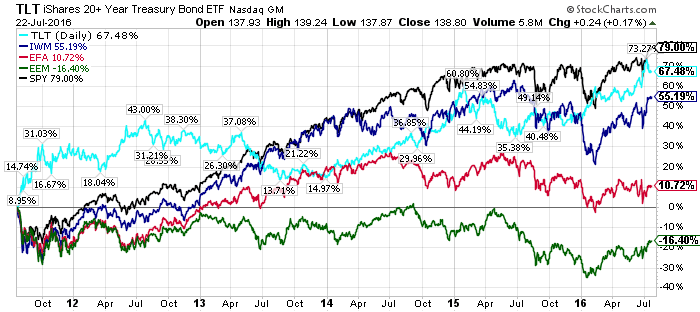

As capital from the rest of the world has flowed to both U.S. equities and bonds, due to their higher relative yields, long-term Treasury prices have surged. This is shown by the chart of the iShares 20+ Year Treasury Bond ETF (NYSEARCA:TLT) in the following chart.

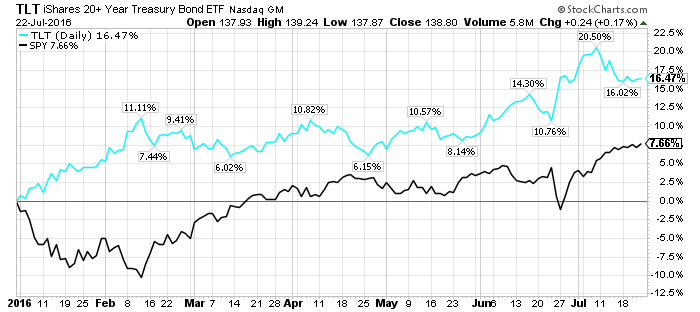

The increase in long-term Treasury bonds has actually outpaced the resilient large-cap U.S. equity market on a percentage basis, leading the SPY in total return, 16.5% to 7.7%.

More impressively, over the past five years TLT has only marginally trailed SPY in total performance, 79% to 67.5% respectively. It has handily outpaced the iShares Russell 2000 ETF (NYSEARCA:IWM), a measure of small-cap U.S. stocks, which is up 55.2%; the iShares MSCI EAFE ETF (NYSEARCA:EFA), a measure of developed international stocks, which is up 10.7%; and the iShares MSCI Emerging Markets ETF (NYSEARCA:EEM), a benchmark of emerging market stocks, which has actually declined 16.4%. Meanwhile, the U.S. markets have been going gangbusters.

With the relative underperformance of EFA and EEM, and their higher prospective future returns based on the GMO expected return table shown earlier, it is a good time, in my opinion, for investors to overweight international stocks as part of their overall asset allocation.

No Place To Hide For U.S. Centric Investors

The bull market in U.S. stocks and bonds, particularly Treasury Bonds, has benefited investors since 2009, but it has brought valuations to nosebleed levels today. This has made it unlikely that future returns can meet the expectations of most investors, especially if they have a traditional 60/40 or 70/30 portfolio centered in U.S. securities.

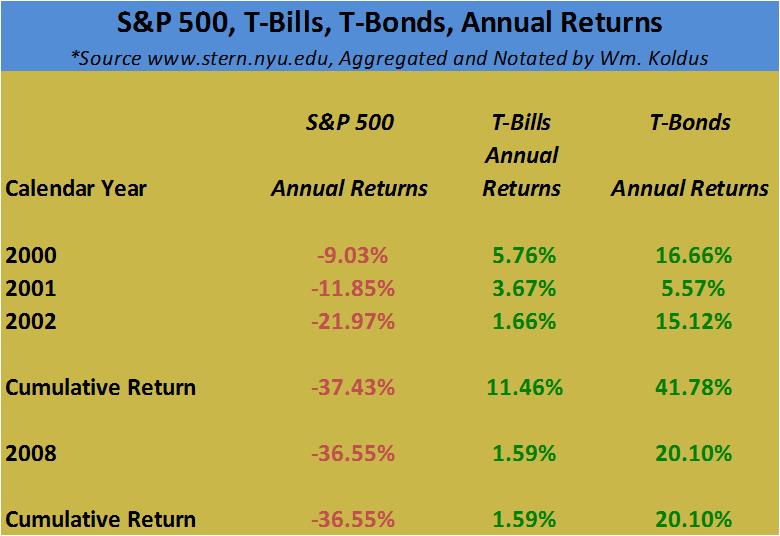

Additionally, in the event of a significant market correction, it is unlikely that U.S. Treasuries can offer the same non-correlated return potential that they have in the past bear markets, simply because of their current absolute valuations.

.

.

Put simply, since U.S. Treasuries have soared during the current bull market, there is not much upside to their prices, or downside in yields. In the event of a bear market, it is unlikely that Treasuries deliver the returns they did in 2000-2002, and in 2008 as shown in the table above.

Additionally, U.S. economic data is coming in stronger than expected, almost across the board, and U.S. home prices rising for the 52nd consecutive month to a new record. So there is a real risk that interest rates could rise, causing stock and bond prices to retreat together, unwinding a portion of their dual rise together.

Conclusion - Consider A Non-Traditional Portfolio If You Want To Keep Dancing

With so many people worried about "Brexit", and deflation, the party is probably not over yet, as the markets usually do not go down when everyone is expecting a decline. Having said this, similar to 2007, the top may be in, or near, for some asset classes. If equities and bonds keep rising from this juncture, particularly U.S. stocks and bonds, it will simply reduce future expected returns further.

This is a non-trivial probability, especially in the buoyant equity market, from my perspective.

This is a non-trivial probability, especially in the buoyant equity market, from my perspective.

Building on this narrative, due to their underperformance over the past five years combined with their future real return forecasts, it makes sense to at least consider an overweight position in international equities. That's particularly true for emerging market stocks, which have been negatively correlated with the U.S. large-cap equity market over the past five years.

Brazil, with all of their negative news, including political corruption, the Zika virus, and the low expectations for the upcoming 2016 Olympics, perfectly encapsulates the historic reversal rally in out-of-favor assets in 2016. The iShares MSCI Brazil Capped ETF (NYSEARCA:EWZ) has delivered a total return in excess of 60%, defying all expectations.

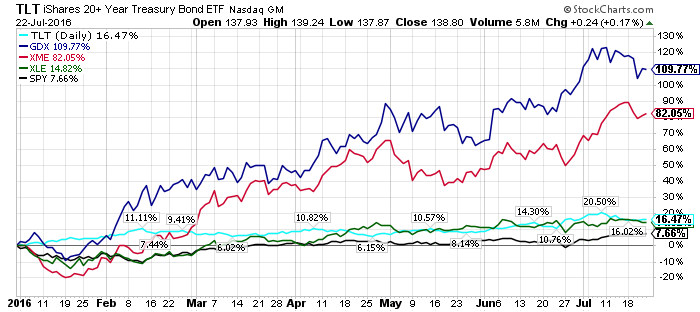

Additionally, out-of-favor inflationary assets, including gold stocks, as measured by the VanEck Vectors Gold Miners ETF (NYSEARCA:GDX); material and mining stocks, as measured by the SPDR S&P Metals and Mining ETF (NYSEARCA:XME); and energy stocks, as measured by the Energy Select Sector SPDR ETF (NYSEARCA:XLE), have all outpaced the S&P 500 Index in 2016.

The GDX and XME are up a remarkable 110% and 82% respectively, and the XLE is up a still healthy 15%.

.

The GDX and XME are up a remarkable 110% and 82% respectively, and the XLE is up a still healthy 15%.

.

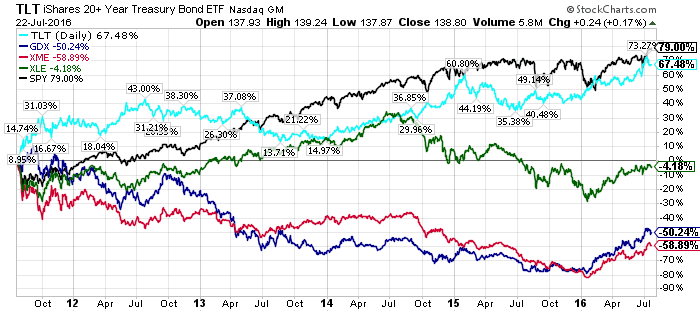

Looking back over the past five years, however, shows a different picture. GDX, XME, and XLE all trail the performance of SPY and TLT by a considerable margin, signaling that there could be more upside potential in these out-of-favor, non-traditional assets.

From my vantage point, the value in these out-of-favor asset classes is not necessarily in the larger capitalization companies like Exxon Mobil (NYSE:XOM), or Chevron (NYSE:CVX), who are trading closer to the high-end of their five-year ranges. Rather, the opportunity is smaller, out-of-favor stocks, like Cliffs Natural Resources (NYSE:CLF), Southwestern Energy (NYSE:SWN), Teck Resources (NYSE:TCK), Unit Corporation (NYSE:UNT), and U.S. Steel (NYSE:X). I wrote public articles on all of these earlier this year, and whom all remain materially below their five-year highs.

There is certainly risk, and I have had my misses, most embarrassingly, and publicly with Peabody Energy (OTCPK:BTUUQ). But having a concentrated basket of out-of-favor equities as a component of your overall asset allocation, with an emphasis on inflationary commodity stocks and emerging market equities, has been unquestionably the best way to deliver alpha in 2016.

In addition to the public content and archive available on Seeking Alpha, I also founded and actively contribute to a highly rated premium research service, called "The Contrarian". There we highlight and go in-depth on a number of out-of-favor companies, including the next wave of opportunities in the commodity sector, an increasing focus on companies in the financial sector, and a new spotlight on the downtrodden biotech and specialty pharma sectors. In "The Contrarian" we have been at the forefront of researching a number of these out-of-favor stocks, and we feel there is much more opportunity in the next 12-36 months.

In conclusion, stock and bond prices are at historical highs, and their expected real returns are deep in negative territory for the next seven years, on an annual basis, according to one of the most preeminent asset class forecasters in the investment business. Could stock and bond prices move higher from here? Yes, of course, and in the near-term, I could actually see that happening in the U.S. equity market, possibly after a short-term correction, but the overwhelming probability is that investors will need to consider alternate investment strategies and out-of-favor asset classes in order to meet their portfolio return objectives in the years ahead.

0 comments:

Publicar un comentario