We Didn't Panic. We Just Sold Everything

by: Shareholders Unite

Summary

- Stocks were fully valued, so upside was limited.

- Brexit in and of itself won't lead to a market crash, let alone an immediate one.

- However, there are so many cracks and fissures in the world economy that the risks have increased significantly, and cash is king in this environment.

- Brexit in and of itself won't lead to a market crash, let alone an immediate one.

- However, there are so many cracks and fissures in the world economy that the risks have increased significantly, and cash is king in this environment.

Two weeks ago we expressed our concern about the complacency that the upcoming Brexit vote engendered in the markets. These markets even rallied when the vote approached, apparently discounting an expected win for the Remain camp.

Well, how did that work out? Now, after the vote, many people here (and elsewhere) urge us to remain calm, which is solid advice. One should always try to remain calm in the markets, but that doesn't exclude big decisions, as long as they're taken rationally.

Here is one big decision: we sold everything on Friday. That's what we did in our little example portfolio (which, if you must, you can follow here). Except for two solar stocks and InvenSense, it was actually doing fine, with a few considerable wins.

However, with the Brexit vote, we decided to liquidate everything. At first sight, that might sound a hasty and emotional decision, but hear us out, it isn't.

Basically we see an environment for stocks in which the returns are capped and the risks have significantly increased. While individual stocks might still do well (and we might buy back a few stocks, or buy other ones), we think this environment warrants a much larger cash position.

Here are our reasons.

- Brexit increases the chance of a recession

- The world economy is fragile

- US stocks are expensive

- The biggest risk is political Brexit contagion

Brexit increases the chance of a recession

There are quite a few ways in which Brexit increases the chances of a recession:

It's unchartered territory, which is engendering uncertainty. Markets don't like uncertainty and neither do those that take investment decisions. It's unclear how the UK's trade relations with the EU will be affected (but affected they will be).

Politically, since immigration played such a big part for the Leave camp, immigration into the UK has to be lowered. But this goes against the four freedoms underpinning the single market, so the UK can't be a part of that.

The Norway solution, in which Norway is part of the single market while not being an EU member is therefore not open to the UK, so they're out of the single market.

This will affect trade, and issues of market access play a pretty prominent role in cross-border investment decisions. The uncertainty alone about how these issues will be solved is enough to have a material effect on investment. And the uncertainty will remain for a good while, years.

Here is The Economist:

With 72% of investors citing access to the European single market as important to the UK's attractiveness, the referendum has the potential to change perceptions of the UK dramatically, posing a major risk to FDI. Our survey indicates that 31% of investors will either freeze or reduce investment until the outcome is known.

Car exports are likely to suffer, according to the BBC:

Britain must strike a trade deal with Europe as soon as possible to protect the country's multi-billion pound car industry and avoid high tariffs. David Bailey, professor of industry at Aston University, warned of a "big uncertainty" for the sector following the UK's vote to leave the EU. Without a deal, he fears a return to the days when the industry faced a 10% tariff on exports. The UK exports 77.3% of its car output, 57.5% of which goes to Europe. "What we don't want in two years' time is to go back to [World Trade Organisation] rules which involve 10% tariffs on car exports," he said.

Then there is the impact of UK's trade relations with the rest of the world. At present they don't even have the required number of specialists to negotiate, as this was an EU policy area.

According to the above quoted Economist article, tax revenues will take a much larger hit than the 8 billion pounds which EU membership is supposed to save.

There are myriads of other implications that are not immediately obvious. What to think of funding for British tech start-ups. It turns out that a significant part for that comes from the EIF, the European Investment Fund.

Brexit is also likely to affect the position of the City of London, at least for trading the euro-denominated assets. Some of that is likely to move to the continent.

The one saving grace is the decline of the pound, which provides at least some compensation for the risks in the UK. The UK runs a very large trade deficit, it is therefore dependent on foreign capital to finance that.

Some of that foreign capital will not arrive because of the uncertainty and the questions about the conditions of future access to the single market. This can only mean the pound has further to fall, although a British recession will cut into the trade deficit by reducing imports (and a rising currency will do the same).

Fragile world economy

The most immediate recession risks are in the UK, but the rest of the world can catch some contagion as well. This is what happens when a shock to the system hits a world economy where fault lines are already plentiful. Here are just the main ones:

- Much of the eurozone was just emerging from the longest slump in modern times, but the recovery can hardly be called vigorous and economic conditions (unemployment, debt levels) are mostly far worse than before the crisis. If growth is snuffed out again, this could have dire consequences.

- Italian public debt has ratcheted up through the denominator effect (low or negative nominal GDP growth increasing debt/GDP ratios), they lost a quarter of their industry, GDP is still way below pre-crisis levels and youth unemployment is dramatically high. On top of that, Italian banks sit on the highest levels of bad loans.

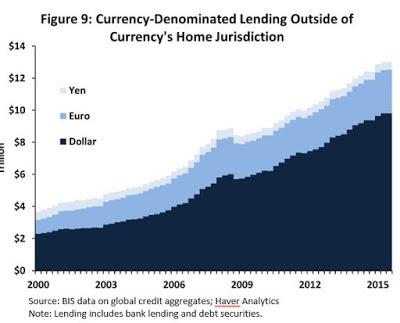

- Many emerging markets have huge amounts of dollar debt outstanding (see figure below), any rise in the dollar is hurting them and a sufficient rise can set off a chain reaction.

- Japan has thrown everything and the kitchen sink to get out of deflation and get the yen lower, but Brexit shaves 8% off the Nikkei and the yen tumbles to 100 to the dollar. They need 4-5% nominal GDP growth to stabilize the public debt/GDP ratio. With 100 yen to the dollar, they can forget about that.

Here is how Morgan Stanley assessed the situation:

While the size of the economic impact depends on the political steps taken from here, our economists estimate that it could knock 1.5pp off UK GDP over the next 18 months. This impact is not limited to the UK. After considering the impacts to trade, confidence and investment, they see a potential cost of 0.8pp to euro area GDP. For the global economy, there could be a cumulative hit of ~0.5pp from our baseline between now and the end of 2017. This weakening of the global environment would likely weigh on the Fed's thinking. Our US economists no longer expect the Federal Reserve to raise rates this year, keeping G4 yields lower for longer."

Politics is already in disarray. We have a leadership contest in the ruling Conservative party that will last until October. Brexit campaign leaders seem to have been unprepared for their campaign to actually win, given their silence in the days following the outcome. Do they actually have a plan? It doesn't seem so, here is former Tory Chairman Liam Fox:

I think that it doesn't make any sense to trigger Article 50 without having a period of reflection first, for the Cabinet to determine exactly what it is that we're going to be seeking and in what timescale. And then you have to also consider what is happening with the French elections and the German elections next year and the implications that this might have for them. So a period of calm, a period of reflection, to let it all sink in and to work through what the actual technicalities are.

Funny enough, nobody can really force the UK to trigger invoking Article 50 and there might yet be ways to avoid this (for instance if a general election was called which could function as a sort of second referendum on Brexit).

If the Brexit camp can converge on a plan to keep access to the single market (for instance, through membership of the EEA), things could stabilize. But we're not there yet, British politics is in disarray and has to sort itself out first. That can take quite some time.

The future of the EU

Here is where the biggest fall-out can happen. While Britain wasn't a member of the euro, the impact could be greatest in the eurozone.

The large cracks in the eurozone have been papered over by a mild upturn in the business cycle after the longest slump in history. This has been driven by the ECB, lower energy cost, and a lower euro.

But this recovery is weak, and the cracks and fissures brought about by the euro are still very much present. What's more, the long slump brought about mostly by the deflationary bias of the euro itself, has left many countries in a terrible shape.

Usually a recovery restores metrics like unemployment and debt levels to before the recession, but in many eurozone countries this hasn't happened at all. Economically the likes of Italy, Portugal, Greece, Spain, and even Finland and France are very ill prepared to handle another downturn while they haven't really recovered from the previous one.

But it's the politics of this where the greatest danger lies. Populations in many of the eurozone countries are adrift. While many wrongly blame the EU, they are right to blame the most ambitious part of it, the euro.

Conclusión

Stocks were fully valued, even under better circumstances we saw limited upside. We're not saying that Brexit will crash the markets, but what we are saying is that Brexit could be the trigger that cracks some of the fissures festering in the world economy, of which there are quite a few. We think cash is king under these circumstances.

0 comments:

Publicar un comentario