The Perfect Storm

by: Lawrence Fuller

- Fed Chair Yellen contends that there are no extreme threats to financial stability at this time.

- To the contrary, a confluence of threats have been developing for months in what looks to be taking shape as a perfect storm.

- Investors are being led into the eye of this storm as they take on more risk in search of higher rates of return.

- To the contrary, a confluence of threats have been developing for months in what looks to be taking shape as a perfect storm.

- Investors are being led into the eye of this storm as they take on more risk in search of higher rates of return.

There was stunning commentary from the Federal Reserve this week. In its Monetary Policy Report submitted to Congress, Fed officials conceded that "forward price-to-earnings ratios have increased to levels well above their median of the past three decades. Although equity valuations do not appear to be rich relative to Treasury yields, equity prices are vulnerable to rises in term premiums to more normal levels."

In other words, the Fed is acknowledging that the stock market is extremely overvalued on a historical basis, which are due in large part to its monetary policy stimulus. At the same time, the Fed suggests that the stock market doesn't have to be considered overvalued if we compare it to artificially depressed Treasury yields, which is also due in large part to its monetary policy stimulus.

Therefore, it sees no need to be concerned so long as bond yields remain near all-time lows.

Consequently, if Treasury yields rise to more normal levels, which the Fed has no idea how to define, then stock and bond prices could decline substantially, which would lead to significant financial instability. Herein lies a dilemma of epic proportions for investors-stocks and bonds are overvalued, while cash yields nothing at all.

During her testimony to members of Congress this week, Fed Chair Janet Yellen said "I don't see signs of extreme threats to financial stability at this time. This is something we monitor very closely, but it is something that can happen in a low interest-rate environment."

In other words, Yellen is telling us that the current interest-rate environment, which was by the Fed's design, is ripe for extreme threats to financial stability. Yet there is no need to be concerned, because she and her cohorts at the Fed watch closely for these threats, and they see no evidence that there is anything to be concerned about at this time.

The reality is that there are several significant threats to financial stability at this time. These threats are blatantly obvious, but the Fed isn't acknowledging them for two important reasons.

The first is that the Fed does not want investors to sell stocks or bonds, because that could undermine the wealth effect that it instigated with its policies, slowing what is already a tepid rate of economic growth. The second is that the Fed has never forewarned of pending threats to financial stability until those threats ultimately result in financial instability, at which point it is too late.

Janet Yellen reminds me of the captain of the commercial fishing boat Andrea Gail in the biographical disaster film called The Perfect Storm. In the film Captain Billy Tyne, played by George Clooney, leads his crew well beyond their typical fishing grounds to the Flemish Cap in hopes of a big catch, despite a developing storm behind them. After great success, they must hurry home before their catch spoils, but now they face a confluence of two stormy weather fronts and a hurricane in what would become the perfect storm. Regardless, and after repeated warnings, the captain convinces his crew to take this storm head on in what would ultimately lead to their demise.

If Janet is the captain, then investors are her crew, and she has led them to push financial market valuations well beyond what has been the historical norm. We are in uncharted waters.

She has done this despite the steady deterioration in market fundamentals. Yellen's success in achieving her objectives has been modest at best. Regardless, she continues to forecast nothing but calm waters ahead for investors, even as they face a confluence of foreboding factors that is taking shape as a perfect storm of a different sort.

Weather Front #1 - Valuations

One of the tenets of the bullish narrative is that the S&P 500 index (NYSEARCA:SPY) yields a whopping 2.1% right now, which when compared to the yield on the 10-year Treasury at 1.69% gives investors the impression that stocks are reasonably valued. However, if we compare the yield on the S&P 500 to the negative yields on sovereign debt in many parts of the developed world, the S&P 500 could be construed as undervalued.

Historically, when the yield on this benchmark index has moved above that of long-term Treasuries, it has been a buy signal. Yet this has been because equity prices have fallen in the past, while today the S&P 500 flirts with all-time highs. Instead, it is bond yields that have fallen, leaving the broad equity market significantly overvalued. While an overvalued market doesn't necessitate a significant near-term decline in stock prices, it does tell us a lot about what to expect in terms of future long-term returns.

In keeping with the Fed's discussion of median price-to-earnings ratios, let us look at the median P/E for the S&P 500 index, defined as the one for which half of all the constituents of the index have P/E ratios that are higher and half have ratios that are lower. The median P/E ratio for the S&P 500 index is currently over 22. You can see the median P/E ratios of historical significance over the past three decades in the chart below.

What is notable is that today's median P/E is higher than that at any point in time over the past 30 years with the exception of the period during the tech bubble in 2000-2001. It is also notable that the forward 10-year returns have been exceedingly poor when the median P/E has been over 20, as it is today. While this weather front does not have any immediate consequences on a stand-alone basis, it is clearly a threat to financial stability at some point over the longer term.

It also indicates that forward returns are likely to be well below historical averages.

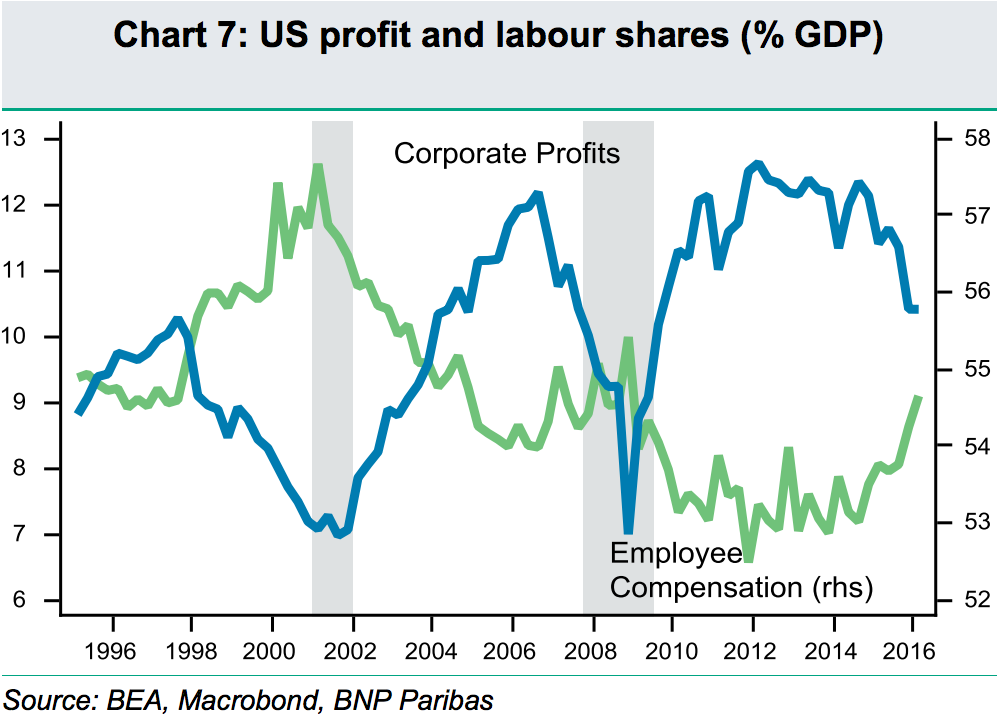

Weather Front #2 - The Business Cycle

It doesn't take any expertise to look at the chart below and recognize that there is another foreboding weather front taking shape on the horizon. In the late stages of every business cycle, labor costs begin to rise and corporate profits fall as a percentage of overall GDP. This typically presages a recession.

Companies are currently unable to raise prices in today's low-inflation environment in order to offset rising labor costs, so profits suffer. This leads to further reductions in capital spending and investment in their businesses. Ultimately, companies hire fewer employees, which we saw a glimpse of in last months' employment report.

Instead of investing in their businesses, which creates jobs and leads to economic growth, companies have focused on financial engineering by buying back shares of stock. The Fed has incentivized this practice with cheap borrowing costs. Corporate buybacks rose to a near-record high of $161.4 billion in the first quarter of this year, and the trailing 12-month total of $589.4 billion has now eclipsed the previous record of $589.1 billion set in 2007. That was not money well spent in 2007. It will not have been money well spent in 2015 either. It has been a key factor in inflating stock valuations, and when this source of demand for stock fades, it poses a significant threat to financial market stability.

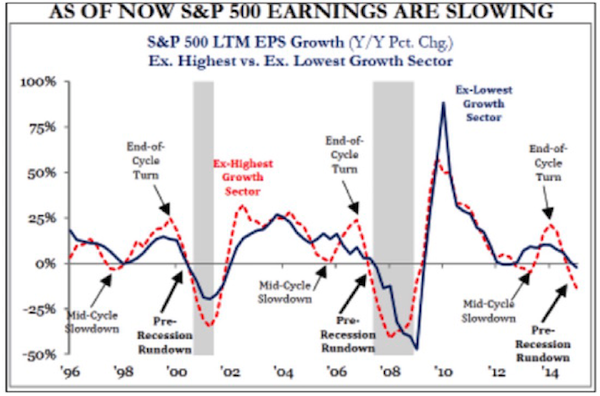

The Hurricane - An Earnings Recession

The recession in corporate profits for S&P 500 companies is in its fifth consecutive quarter. It presents the greatest and most obvious risk to near-term financial stability, but it has been going on for so long that the consensus believes it has been fully discounted in stock prices. I strongly disagree. The bulls continue to blame this profits recession on the energy sector, which is why I find the chart below to be particularly enlightening, because it reflects earnings growth for the S&P 500 excluding both the highest and the lowest growth sectors.

Source: Mark Yusko, Morgan Creek Capital Management

What is notable is that even when we exclude the energy sector, which is exhibiting the weakest growth, S&P 500 earnings are declining on a year-over-year basis. This type of decline is typical in advance of economic recessions, as we saw in both 2001 and 2008.

The Perfect Storm

So investors are now confronted with extreme overvaluation, what is likely the near-end of the current economic expansion and a recession in corporate profits, which are all combining to form a perfect storm. Yet Janet Yellen sees no signs of threats to financial stability. Instead, she is leading investors directly into the eye of the storm. The Fed's policies have forced investors to take greater and greater risks to seek what are lower and lower returns.

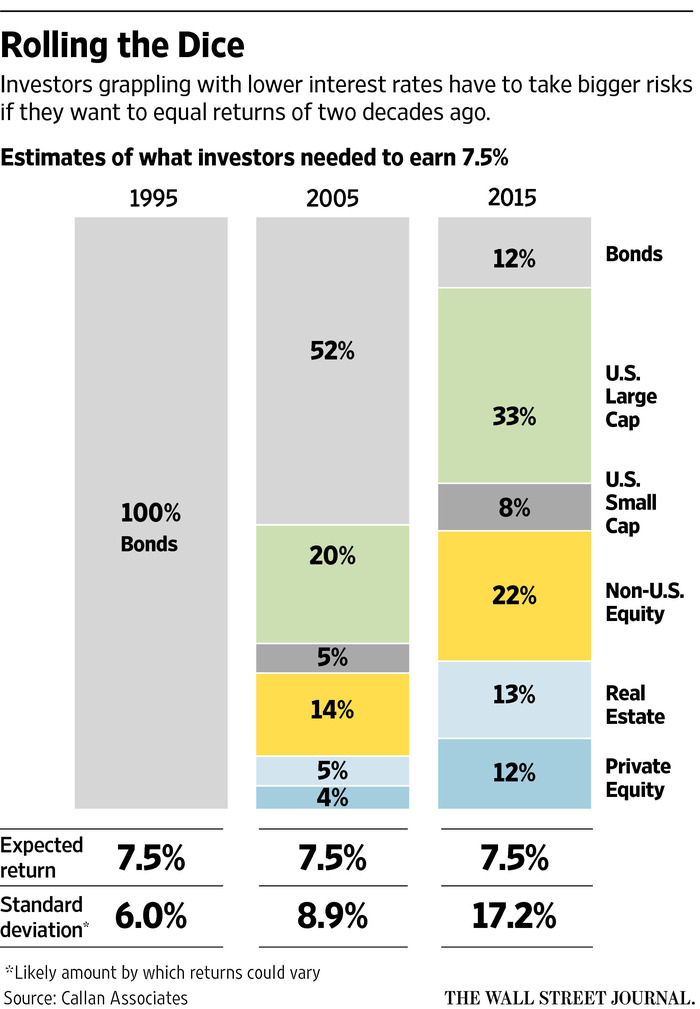

This includes what have historically been the most conservative investors, and they manage a tremendous amount of financial assets. Pension funds used to be able to earn 7.5% with a relatively conservative fixed-income portfolio, but the Fed's monetary policies have forced managers to continually increase the amount of risk they take in hopes of achieving the same return. The 2015 portfolio allocation seen below looks as ill-advised today as the record level of corporate stock buybacks executed during the past year.

The Fed has intentionally created a shortage of safe investments with sufficient yields, forcing investors of all stripes into far more risky ones to obtain the income and growth they require.

This creates the appearance of both economic progress by inflating financial asset prices, and a wealth effect that primarily benefits those that hold all of the wealth. It is a cheap short-term fix to economic issues that require long-term solutions, and in the end it will be very costly.

As the S&P 500 has meandered sideways since reaching its all-time high in May 2015, this perfect storm has been gathering strength. Today, the stock market is plunging in what most perceive to be a reaction to the news that Britain is leaving the EU. This is clearly important, but I see the unexpected results from the Brexit vote as more of an excuse rather than the primary reason to sell financial assets .

It is simply a trigger to reduce risk as the greater threats to financial stability are becoming increasingly more apparent. My recommendation continues to be to stay on shore with a very conservative asset allocation and not to follow Janet Yellen into the eye of this perfect storm. I believe that those who accept lower returns today with less risk will be better positioned to capitalize on the potential for much greater returns in the future.

0 comments:

Publicar un comentario