The Latest COT Report And How The Turkish Coup Attempt Will Affect Gold

by: Hebba Investments

.

- Gold jumped Friday afternoon when the Turkish coup hit the news wires.

- While this short-term boost was good for gold longs, it looks like Erdogan regained control of Turkey.

- We expect Turkish political stability to be maintained moving forward and the Turkish Lira and stock market to recover its losses.

- Any risk premium for gold due to these events should be lost, and we worry about gold's short-term fundamentals as physical demand is really poor.

The late Friday Turkish coup attempt (which was conveniently after US markets closed) is probably the foremost thing on gold investors' minds so we will have to cover it in this analysis.

But first we will go over the latest Commitment of Traders report (COT), where we saw record-breaking gold positions drop for the first week in a month. Silver actually diverged a little from gold as speculators increased their own positions, which also probably was reflected in the prices as silver was much stronger for the week than gold.

We will get a little more into some of these details but before that let us give investors a quick overview into the COT report for those who are not familiar with it.

About the COT Report

The COT report is issued by the CFTC every Friday, to provide market participants a breakdown of each Tuesday's open interest for markets in which 20 or more traders hold positions equal to or above the reporting levels established by the CFTC. In plain English, this is a report that shows what positions major traders are taking in a number of financial and commodity markets.

Though there is never one report or tool that can give you certainty about where prices are headed in the future, the COT report does allow the small investors a way to see what larger traders are doing and to possibly position their positions accordingly. For example, if there is a large managed money short interest in gold, that is often an indicator that a rally may be coming because the market is overly pessimistic and saturated with shorts - so you may want to take a long position.

The big disadvantage to the COT report is that it is issued on Friday but only contains Tuesday's data - so there is a three day lag between the report and the actual positioning of traders. This is an eternity by short-term investing standards, and by the time the new report is issued it has already missed a large amount of trading activity.

There are many different ways to read the COT report, and there are many analysts that focus specifically on this report (we are not one of them) so we won't claim to be the exports on it.

What we focus on in this report is the "Managed Money" positions and total open interest as it gives us an idea of how much interest there is in the gold market and how the short-term players are positioned.

This Week's Gold COT Report

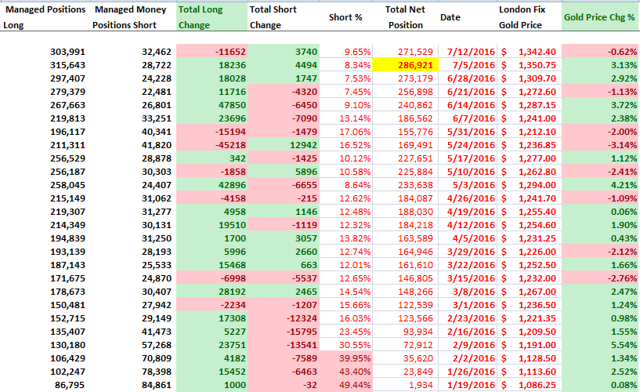

This week's report showed speculative gold longs decreased their positions for the first time in more than a month, while shorts increased their own positions for the third week in a row.

As investors can see, after five weeks of speculative long position increases, we finally saw these longs take some profits their positions. That might have also encouraged shorts to increase their own positions by a mediocre 3,740 contracts.

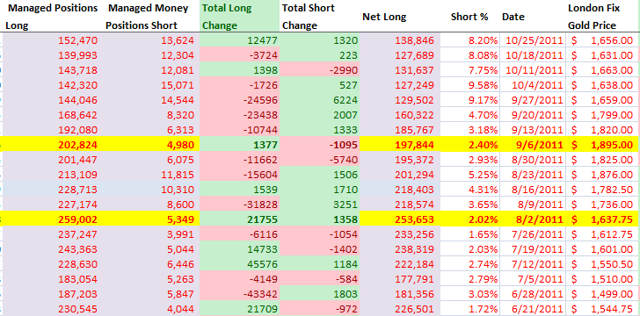

Looking back at the last major gold peak in 2011, the actual peak in gold occurred around a month after the net speculative long peak occurred.

As shown in the table above, gold's previous cyclical speculative net long peak was hit on the week of 8/2/2011, when the net long position reached around 253,000 contracts and the gold price was $1637.75 per ounce. If you had used that data to wait for a pullback (or worse get short), you would have seen gold rise for another month to a high of $1895 per ounce - not a very fun position to be in.

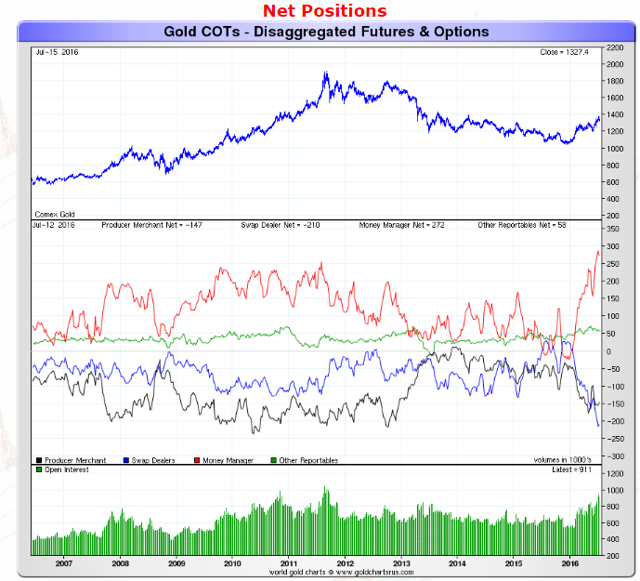

Moving on, the net position of all gold traders can be seen below:

Source: Sharelynx Gold Charts

Source: Sharelynx Gold ChartsThe red-line represents the net speculative gold positions of money managers (the biggest category of speculative trader), and as investors can see, speculative traders have taken a break from their parabolic rise and sit at a net long position of 272,000 contracts.

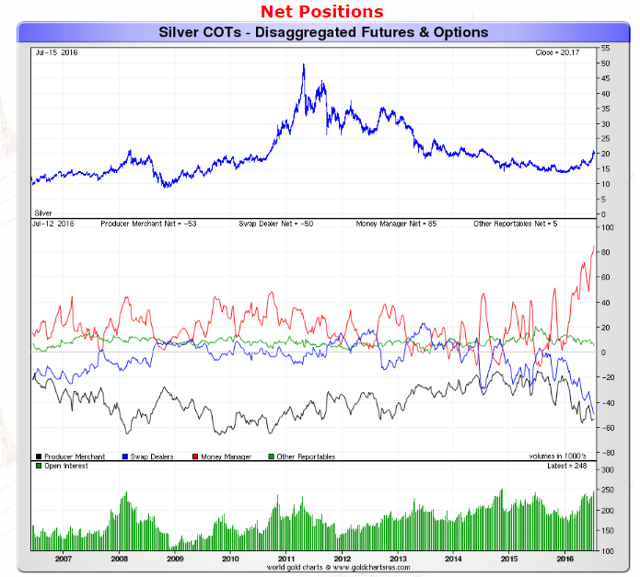

As for silver, the action week's action looked like the following:

Source: Sharelynx Gold Charts

Source: Sharelynx Gold ChartsThe red line which represents the net speculative positions of money managers, increased by a little more than 2,000 contracts while shorts decreased by a similar 2,000 contracts. This is a bit of a divergence from gold as speculative silver positions increased compared to a decent decrease in gold speculators. This may tell us that investors are expecting the silver-gold ratio to decrease further and it certainly explains why silver outperformed gold on the week.

The Implications of the Failed Turkish Coup Attempt on Gold

It is time to deal with the biggest event of the week, the failed Turkish coup attempt. While this news is obviously live and could change in the next few days, it looks like for now the situation has calmed down a bit as Turkish President Erdogan returned to the country and declared the coup over.

Additionally, it looks like he has commenced the hunt for sympathetic elements of the military and judiciary - these folks probably will not be receiving much in the way of mercy from Mr. Erdogan.

While Erdogan has accused Fethullah Gullen, a US-based Turkish dissident cleric, of being involved in the coup (which he has denied), we haven't seen a lot of evidence of who was really involved. Regardless, we think as long as it is an internal Turkish dispute between these two parties and does not involve any other outside nations (which seems a bit clearer now), this dispute itself will not have much in the way of gold implications.

What we are watching in terms of consequences for the gold price are the following:

- The effect on the Turkish Lira

- Will Turkey's political stability be maintained

As soon as the coup made the news wires on Friday afternoon, the Turkish Lira plummeted into the markets close. Gold as a store of value would obviously benefit if the Lira collapsed further as the Turkish affinity for gold would only increase physical imports. While we expect Turkish gold imports to probably increase over the next few weeks or months, we don't expect a complete Turksih gold rush as the coup did not succeed or turn into a civil war and it looks like Erdogan is going to severely crackdown on dissidents and prevent any further chaos.

In terms of political stability, it looks like there was little in the way of public support for the coup attempt, and in fact, it looks like much of the Turkish public actually supported Erdogan and actively resisted the coup. Unlike the coup in Egypt, Erdogan seems to have much greater support from the public and this should give him reason to crack down further on Turkish dissidents. Ultimately, right or wrong, this will probably lead to a bit more stability in the country moving forward in a dictatorial fashion.

Thus we expect this to result in the Turkish Lira regaining a bit of what it lost on Friday afternoon.

Additionally, short-term traders may want to take a flier on some of the Turkish market ETF's if they show weakness on Monday as we expect things to return to relative normality.

All of this means that any risk premium that was built into the gold price on Friday afternoon (gold surged $10 in a matter of minutes) is probably not justified, at least at this point. If there are no extraordinary events, we expect gold to give back those gains as trading started next week. Of course, that call would completely change if (1) a foreign sovereign nation is found to be involved (think Russia), or (2) if the coup or crackdown results in violent backlash that could possibly suggest a civil war. Ultimately it comes down to Turkish political stability, if that stability is not maintained, then there are significant implications to the region's stability, European stability (think what would happen to immigration if Turkey fell into chaos), and of course, the gold price will reflect that.

Our Take and What This Means For Investors

If the coup had succeeded or thrown the country into civil war, then we would be buying gold hand over fist as these implications would have much greater global consequences than a mere $10 rise in the gold price. But the coup failed rather quickly and it looks like it may result in further crack-downs on dissent in the country, so ultimately it shouldn't have a real effect on the gold price other than causing gold to give back some of its Friday after-hours gains.

In terms of the COT report, while gold speculators decreased their net long position, we are still at historical highs. Of course, highs can always become higher, to justify that we would need to see strong evidence that gold could be propelled further. While there are some major catalysts that can do that (this is why we believe in gold as a long-term investment), there are many short-term catalysts that should cause investors to think long and hard about increasing positions after gold's spectacular 2016 run.

Bron Suchecki of Monetary Metals did an excellent job outlining a few of them in his recent article Yin and Yang:

So how to navigate this new terrain? While one can never avoid subjective interpretation, we feel it helps to take one's bearings from the reality of market prices and in particular, spreads. Therefore it is with interest that I read the following from Reuters:

On the flow front, Platts reported Indian "gold bar imports at only around 215 mt so far this year, just under half the 2015 level, many are expecting a much lower total for full-year 2016" and SCMP noted that Chinese "sales of gold jewellery across the sector have slumped 20-40 per cent".

- Dealers in India were offering a discount of up to $100 per ounce to the global spot benchmark

- Prices in China were seen at a discount of $1-$2 per ounce

- A discount of 50 cents to $1 was being offered in Japan

- Hong Kong prices were at a discount of $1 this week

These are the things that worry us in the short-term as gold seems to be driven simply by Western investor ETF demand. This doesn't even include much of the traditional gold buying population as American Gold Eagle sales are down and bullion dealers seem to be well-stocked.

This is part of the reason why we believe that despite new historical gold speculator position highs, we haven't seen anything close to the highs gold reached in 2011 when it had both paper demand and physical demand working together to propel it higher.

We know we are going to sound like a broken record here, but we think the logical and disciplined thing for gold and silver investors to do here is take profits and wait for a better re-entry point. Thus investors should be lightening up on gold positions in the ETFs and miners such as the SPDR Gold Trust ETF (NYSEARCA:GLD), iShares Silver Trust (NYSEARCA:SLV), ETFS Physical Swiss Gold Trust ETF (NYSEARCA:SGOL), and miners such as Randgold (GOLD) and Barrick Gold (NYSE:ABX).

While we think gold will rise much further in the coming years, now is not the best time to be establishing new positions in gold if you already own a satisfactory core gold portfolio position.

0 comments:

Publicar un comentario