Liquidity Traps, Secular Stagnation, Deflation, And The Legacy Of Keynes

by: Ben Comston

- For some good reasons from the past, some have become irrevocably opposed to anything with the label "Keynesian" attached to it.

- Despite limitations, Keynesian models, including liquidity traps and secular stagnation, are the best explanations available for the economy today.

- If the current gap between savings and investment is not closed, the chance for future deflation is far higher than zero.

- Despite limitations, Keynesian models, including liquidity traps and secular stagnation, are the best explanations available for the economy today.

- If the current gap between savings and investment is not closed, the chance for future deflation is far higher than zero.

Quick... What do a radio talk show host, an historian, an internet commentator, and a blogger have in common? They all have visceral reactions to the term "Keynesian".

"The Keynesians are pretending they have everything under control, but we know that's a fantasy. An even greater opportunity than 2008 awaits us, and we want to help guide public opinion and train a cadre of bright young scholars for that day. With your help, we can, at last, awaken from the Keynesian nightmare.

As the Korean translator of an Austrian text put it, "Keynes must die so the economy may live." With your help, we can hasten that glorious day.

- "Keynes Must Die" by Tyler Durden, ZeroHedge, 2016

"Interesting how a haughty snob is supposed to be celebrated. One explanation may be that this economic phantasy became government econ which per handouts to profs becomes university econ, is miraculously accepted by unions, much easier accepted with the poe (than the poverty-alleviating real economics), is miraculously cherished by the elite and military-industrial complex benefiting from gov't spending, and most definitely is a constant boon to banks required for the monetary expansion, not to forget bail-outs of the most irresponsible banks and companies. Nice move learned from the Nazis."

- Comment on The Guardian's website, 2016

"You want more people to know who John Maynard Keynes was. Okay, attention, class. John Maynard Keynes. If you want to know what Keynesian economics is, you're living it: Barack Obama, massive government spending, massive debt, massive redistribution of wealth, the lie that government spending, deficit spending can propel economic growth. She is dead right that they tricked everybody into thinking this is the way we're going to save capitalism! They had no intention of saving capitalism. Just like Obama, they wanted to destroy it and replace it with socialism or Marxism or fascism or whatever you want to call it. And they got pretty close."

- Rush Limbaugh, 2010

"True, not all those who intended to vote Tory showed their hand to the opinion pollsters, who have almost as much egg on their faces as the Keynesians. Next time, however, the pollsters can simply adjust their projections by using a simple economic model. Just so long as they make sure it's not a Keynesian one. Shame where shame is due."

- Niall Ferguson, Financial Times, 2014

Wow... who knew that in reality, Keynes was a snobbish Nazi that returned from the grave to destroy both the British and American economies.

In reality, Keynes was many things. For one, he was an extremely successful investor. The money he managed for Cambridge University grew from £30,000 to £380,000 during the Depression. He was also incredibly astute at political economy - playing the role of prophet, while writing The Economic Consequences of the Peace in 1919, which accurately predicted the damage to be brought by The Treaty of Versailles - as well as a delegate to the Bretton Woods Conference following WWII.

The anger directed towards Keynes today, though, stems from his influence in macroeconomics. Specifically, the excuse that he gave to policymakers to intervene in the economy rubs many the wrong way. The pity is that ideological aversion to Keynes has kept many intelligent people from having a useful paradigm for understanding the state of the economy today, both in the United States and globally.

Before going on to discuss the economy today, it's worth mentioning that there are good reasons why many grew skeptical of the total umbrella of Keynesianism. There was a time when it was believed by some that any desired outcome could be engineered in some way. That arrogance had some consequences.

The Excesses of Keynesianism

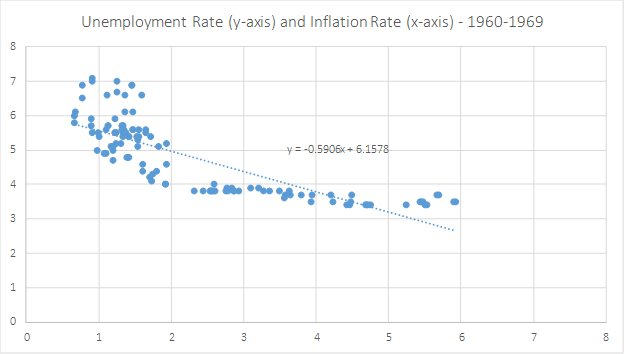

A good way to illustrate the "overdosing" of Keynesianism is found in the Phillips Curve. This is an incredibly simple tool that plots the inflation rate against the unemployment rate. It originated in the observation of a New Zealand economist that there was a trade-off between the two measurements - in other words, a lower rate of unemployment could be "engineered" if you were willing to accept a higher rate of inflation.

Here is what a Phillips curve looked like for the 1960s in the United States:

The results make intuitive sense as well as empirical. If the economy weakens and workers are laid off, they demand less goods and services, which will cause their price to decline and lower inflation; conversely, full employment implies higher demand for goods and services and higher prices.

There's a very obvious flaw in this logic. It completely ignores the supply part of the supply/demand equation. Politicians generally prefer full employment to low inflation. Of course, both are ideal, but voters tend to prefer a job with a little higher prices than no job and lower prices. Ultimately, supply shocks (mostly from oil embargoes) coincided with a Federal Reserve that was excessively political and believed it could "engineer" a lower unemployment rate through excess money creation. The fact that the Fed chairman at the time, Arthur Burns, was trying his hardest to get a Republican, Richard Nixon, re-elected does not alter the value of the lesson in excessive interventions.

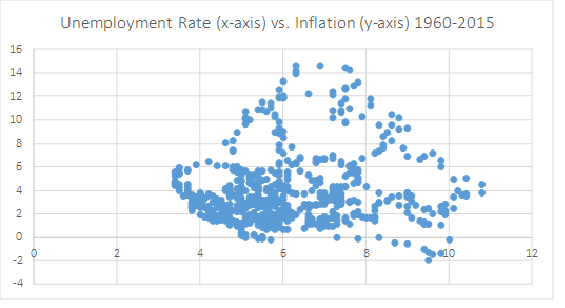

As it turned out, while there is a short-run relationship between prices and unemployment, there is no long-term one.

What causes the short-term relationship to hold but not the long-term one? Milton Friedman was among the first to suggest that there should be no long-term relationship between the two measurements. The explanation can be given through the concept of "rational expectations".

Consciously or unconsciously, everyone operates with expectations about the future, including expectations on the level of prices. If inflation has been mild and a Central Bank has the confidence from others that it will set policy to maintain low inflation, actors in the economy will make decisions with the expectation that prices will continue to be stable. So, if excess money creation causes prices for a particular product to rise, then the decision makers of a business would wrongly assume that the increase in prices is coming from increased demand for their products and supply more; thus lowering unemployment and raising economic growth. Eventually, though, the relationship breaks down, because while the rational expectations of firms are "sticky", they will reset in the long run. In other words, at some point people realize what's going on and stop responding to the price signals.

The stagflation of the 1970s was the first economic malaise that economists had experienced since the Great Depression, but the causes and appropriate policy tools to confront it were not the same as those needed during the Depression. The key difference is that the Great Depression was a shock to demand accompanied with too little money creation, while Stagflation resulted from a shock to supply accompanied by too much money creation.

The work of Keynes was no longer en vogue, as many pundits, policymakers, and economists dismissed his work. Again, some of that came about because, while Keynes did not directly suggest the policies that contributed to stagflation, many saw the permission he gave for market intervention as the real sin.

The perpetuation of that ideological rigidity has caused many to completely misunderstand the post Great Recession economic landscape. In essence, they have continued trying to fight the economic problems of the 1970s, while the economic problems of today are not the result of supply shocks - they have been a result of the shock to demand from excessive leverage, a situation much better paralleled by the Great Depression of the 1930s than the Stagflation of the 1970s.

Liquidity Traps and Secular Stagnation

A liquidity trap and secular stagnation are potentially overlapping, yet distinct, phenomena.

Liquidity traps exist when monetary policy reaches a lower bound such that it becomes ineffective in stimulating demand. Interest rates are what equilibrate the choices that are made between current and future consumption. Within a normal monetary policy framework, lowering real interest rates should stimulate aggregate demand because it makes it cheaper for firms and individuals to prefer current to future consumption. Once a lower bound is reached, for instance zero percent interest rates, then monetary policy becomes ineffective at encouraging current versus future consumption because the price of the trade-off is no longer affected. More money can be injected to the economy, but in this scenario, it will be "trapped" rather than lent, and stimulative to aggregate demand.

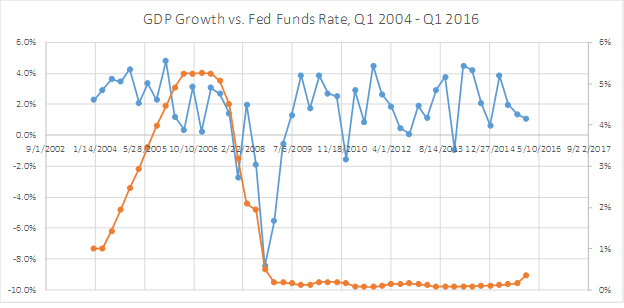

While not dispositive, the liquidity trap we're currently in can be seen in the relationship (or lack of one) between short-term interest rates and economic growth.

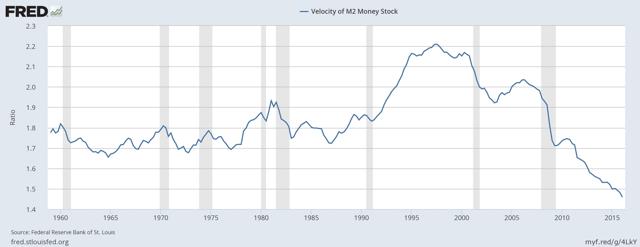

Another obvious clue to the reality of a liquidity trap is the steep decline that's been experienced in the velocity of money, or how often money changes hands. Consistent with money creation being trapped and not spent or invested, the velocity of money has never been lower than it is currently.

Unsurprisingly, a steep fall in the velocity of money also occurred during the Great Depression - another period of economic weakness caused by a shock to demand.

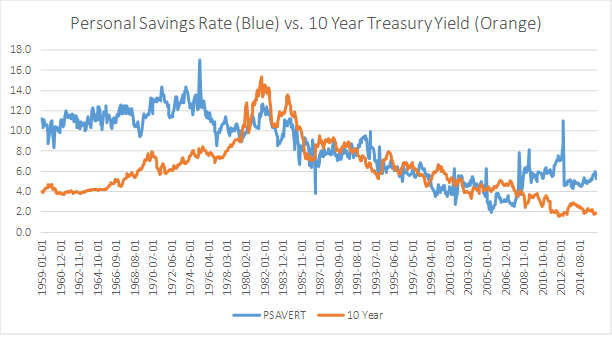

What is the underlying cause of a liquidity trap? One potential cause is a very high preference for savings, such that taking interest rates down to zero will not cause increased demand because of deleveraging or a dearth of good credit risks banks are willing to lend to. And indeed, we have seen a pretty dramatic increase in savings rates for several years now, despite a continual fall in long-term interest rates that should, ostensibly, discourage savings.

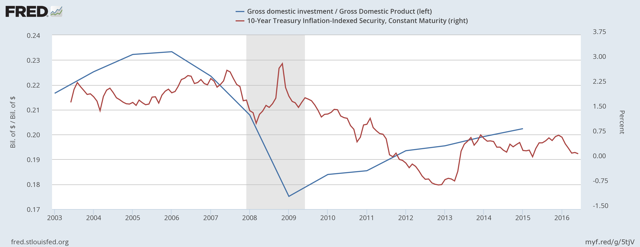

Secular stagnation describes a similar phenomenon, but takes as its focus a gap between investment and savings rather than consumption and time. There is some interest rate that will balance investment and savings in an economy, i.e., if there is too much savings and not enough investment, market interest rates should fall to discourage saving and encourage investment.

As the name implies, secular stagnation is a problem that could have long-range consequences due to under-investment in the economy.

There are a variety of reasons for relatively low investment, while real interest rates are still barely positive. In the article "The Age of Secular Stagnation", Larry Summers put forward one possibility that today's corporations - Google (GOOG, GOOGL), Facebook (NASDAQ:FB), Apple (NASDAQ:AAPL), etc. - are not as capital-intensive as past corporations that were more likely to be involved in autos, steel, or oil. This means that, all things being equal, the demand for capital and investment will be lower than would otherwise be the case.

Additional capital required to be held in banks is another contributor to lowered investment. Although it's proper that banks should be required to hold more capital than they were in 2006 and 2007, the decline in lending per dollar of deposits in banks results in lower investment.

Whatever the cause or causes, the result of secular stagnation is that the real interest rate required to balance savings and investment has declined, and without achieving that proper balance, excess savings and diminished investment should be expected to continue.

Deflation

Without a change in course by policymakers, the best-case scenario is that we continue to meander through low growth for some time until structural changes alter the equilibrium real interest rate necessary to spur consumption, and investment is increased. If you look at the example of Japan, that could be a very long time.

The worst-case scenario may be that we see endemic deflation in the United States and Europe (it's already in Japan). That would be an extremely unpleasant experience. But, if conventional monetary policy cannot deliver a real interest rate that the market demands to encourage consumption and investment, then the adjustment that the market demands could well come in the form of deflation, which would lower the real interest rate further from where it is today.

The economic participants in the US and the global economy are signaling that real interest rates today are still too high rather than too low. For whatever reason, a shockingly large number of people have confused themselves into thinking the opposite is the case.

A Way Out?

What can be done in the face of the liquidity trap and secular stagnation we currently find ourselves? Or is there anything at all?

To repeat my argument from above, the central feature of both of these related scenarios is that the real interest rate needs to decline, and cannot through conventional central bank policy.

Quantitative easing is a completely reasonable response to such a situation, but has not been enough to lower the real rate of interest enough.

The obvious Keynesian response is to increase fiscal stimulus, which will increase overall investment in the economy, reduce aggregate savings, and thereby increase the real rate of interest that the market needs to achieve equilibrium.

Larry Summers, in the same article cited above, has advocated this approach through a dramatic increase in infrastructure spending. This approach has the dual benefit of providing hope that the economic situation we find ourselves in could be alleviated, but also achieves the needed infrastructure spending that would increase productivity, and thereby growth, for many years to come.

An unnecessary fixation on deficits has inhibited stimulus on this scale, with many holding to the illusion that lower amounts of gross debt along with an ageing infrastructure is preferable to higher amounts of gross debt along with greater economic output and productivity by enhancing the backbone to the economy.

What comes next?

The greatest danger remains the continual decline in inflation turning into prolonged deflation.

In such an environment, you would probably prefer to own long-term bonds as opposed to other investments, but with yields so low, it would be advisable to keep the duration of the bonds extremely short. (I know, if there is significant deflation then long-term bonds are your best bet, but over a full holding period, you're not going to be compensated enough to hold them.)

No one can say for sure what's on the horizon. For the time being, it's unlikely that there will be any coordinated effort from Washington to increase investment. The election this Fall could change that, or it may not. But, in the meantime, far too many policymakers continue to fight the malaise of the 1970s rather than the malaise of 2007 to today, even though the current situation of inadequate demand is much more akin to the 1930s than the 1970s. The attitude of many is reminiscent of the description of the Great Powers from WWI that Barbara Tuchman describes in The Guns of August, who spent most of the war fighting the enemy according to the rules of the previous wars, which had all changed. Or, as John Bolton put it, "Politicians, like Generals, have a tendency to fight the last war."

Let's hope we start fighting the war in which we find ourselves and stop fighting the war we wish we had.

0 comments:

Publicar un comentario