by: Boris Mikanikrezai

.

- Speculators remain extremely bullish after the Brexit shock. ETF investors bought gold in June at the strongest pace since February.

- The fall in US real interest rates is the reason #1 behind the gold’s rally YTD.

- But be careful, the Fed will soon recalibrate market’s rates expectations as soon as its July meeting.

- Under this scenario, a bottoming-out process in US real interest rates will trigger strong selling pressure in gold.

- We are currently not positioned on GLD but are looking for short opportunities. We present our historical trade ideas in GLD (long, short) in the year to date.

Fed Chair Janet Yellen.

Introduction

Every week, we closely monitor net speculative positions on the COMEX as well as ETF holdings in so far as the historical economic behavior of gold prices suggests that over a short-term horizon (<3 months), gold prices are largely influenced by changes in the forward fundamentals, reflected in changes in net spec length, ETF holdings, and central bank reserves.

Speculative positioning

Source: CFTC.

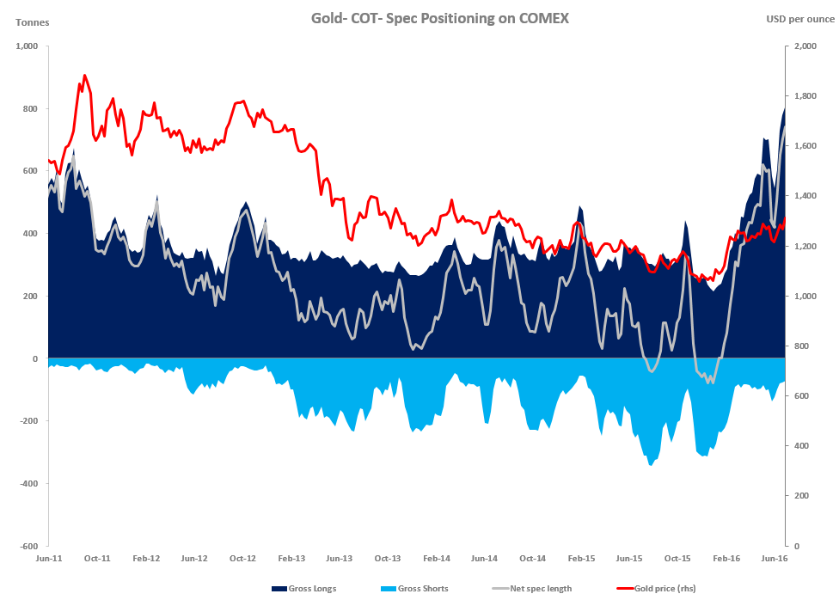

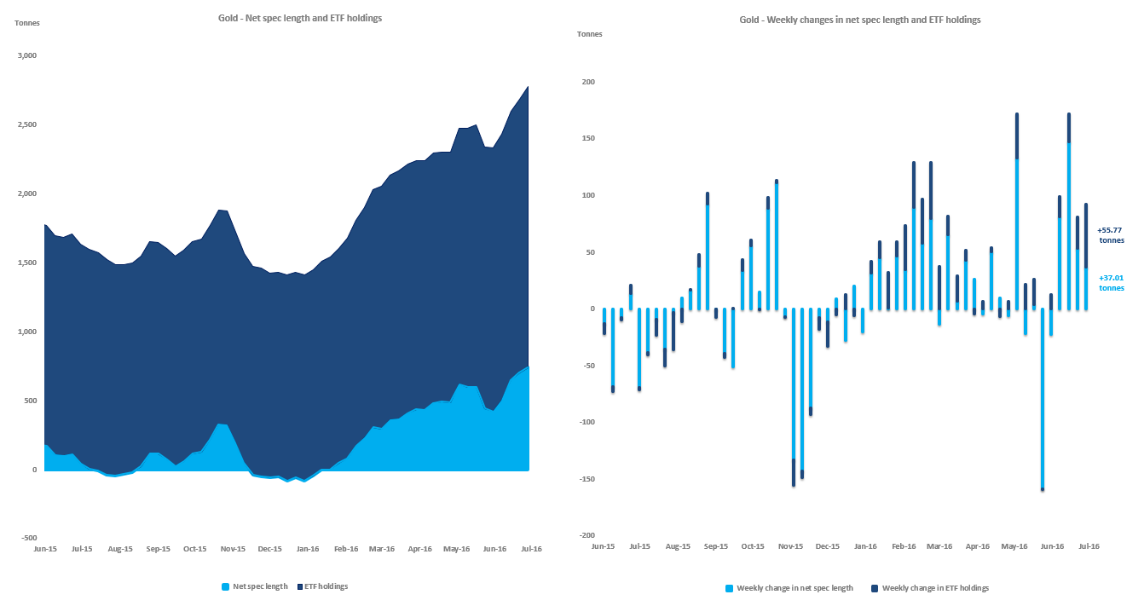

Gold. According to the latest Commitment of Traders (COT) report provided by the CFTC, money managers, viewed as a relevant proxy to gauge speculative activity, raised their net long position for a fourth straight week as of June 28 to a fresh all-time high. Over the period covered by the data (i.e. June 21-28), the gold price surged 3.48 percent.

The net long fund position increased by 37.01 tonnes or 5.0 percent week-on-week (w/w) to 740.06 tonnes, marking its highest level since the CFTC started to publish its statistics in 2006.

The weekly improvement in the speculative positioning was mainly driven by long accumulation and slightly reinforced by short-covering.

Longs raised their positions by 31.07 tonnes w/w to an all-time high. Although the increase in longs for a fourth straight week looks unsustainable in the medium-term, we recognize the strong willingness from market participants to boost their bullish bets. And we cannot predict accurately when this trend will reverse.

Shorts covered 5.94 tonnes of positions w/w, marking a fourth weekly decline in the gross short position. It is worth noticing that short-covering has steadily slowed over the past few weeks, leading us to believe that the wave of short-covering may soon become exhausted. A renewed build-up of shorts could undermine gold prices.

The latest increase in the net speculative length was largely triggered by the "mini" market panic following the Brexit shock. Because most investors did not expect such an outcome (the probabilities estimated by the political bookmakers were skewed in favor of Bremain), market participants had to recalibrate their portfolios by reducing their exposure to risky assets and building risk-unfriendly positions like gold.

Source: Deutsche Bank.

Source: Deutsche Bank.

Interestingly, we believe that gold was the leader behind last week's precious metals rally, mainly because long accumulation was the driving force behind the gold's rally whereas in other precious metals such as silver, platinum, or palladium, short-covering was the main driver, according to the CFTC.

While we recognize the current bullish sentiment in gold, we think that it is largely attributable to over-pessimistic assumptions about the US economy.

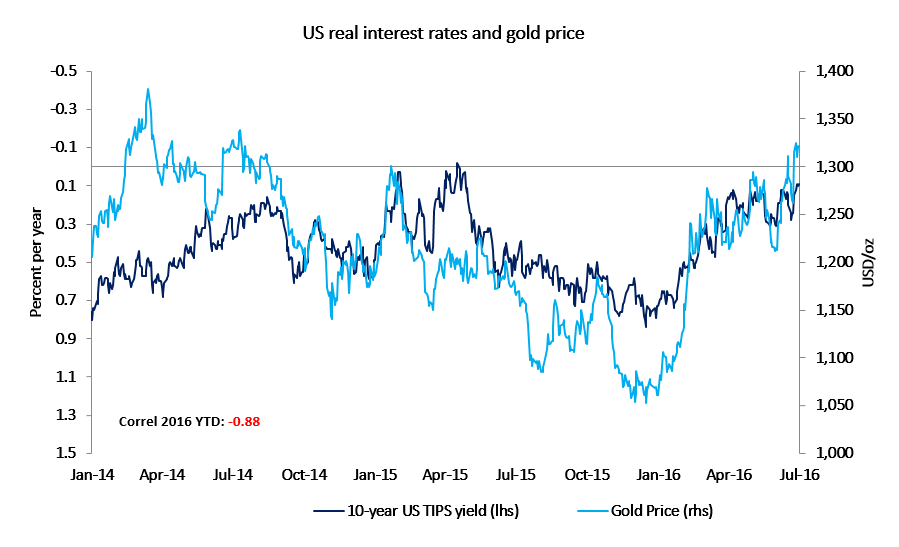

From a historical perspective, gold's speculative positioning has been largely driven by US real interest rates. As can be seen below in the chart, gold prices and the yield on the 10-year US TIPS are highly negatively correlated - we compute a correlation of minus 0.88 in the year to date.

Source: FRED.

Source: FRED.

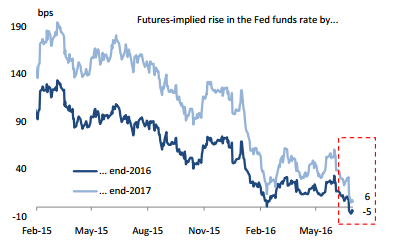

While we are willing to admit that the steep fall in US real interest rates since the start of the year has been partly driven by a losing momentum in the US economic growth reinforced by growing uncertainty, it has also been influenced by overhyped Fed easing expectations. Indeed, while the Fed left unchanged its rate outlook for 2016 (2 rate increases to be expected) at its latest June meeting, we are surprised to see that the market is now pricing a 5 bps decline in the Fed funds rate by the end of 2016 (as seen below in the chart).

Source: Deutsche Bank.

Our analysis of the US economy takes into account the presence of growing signs of inflationary pressure, which should be reinforced by the ongoing rally in oil, the fall in the dollar, and wage growth. Under these circumstances, we think that the Fed may eventually move the market closer to its median view of 2 rate increases in 2016, which should thereby result in a bottoming-out process in US real interest rates higher and move gold accordingly lower due to a noticeable reduction in net speculative positions. We will pay a close attention to the June FOMC meeting minutes, released on July 6, as well as the June employment report, released on July 8, to detect any realignment of perceptions. But this recalibration of expectations is likely to emerge this summer, at the July 26-27 FOMC meeting.

Investment positioning

Source: FastMarkets.

Source: FastMarkets.

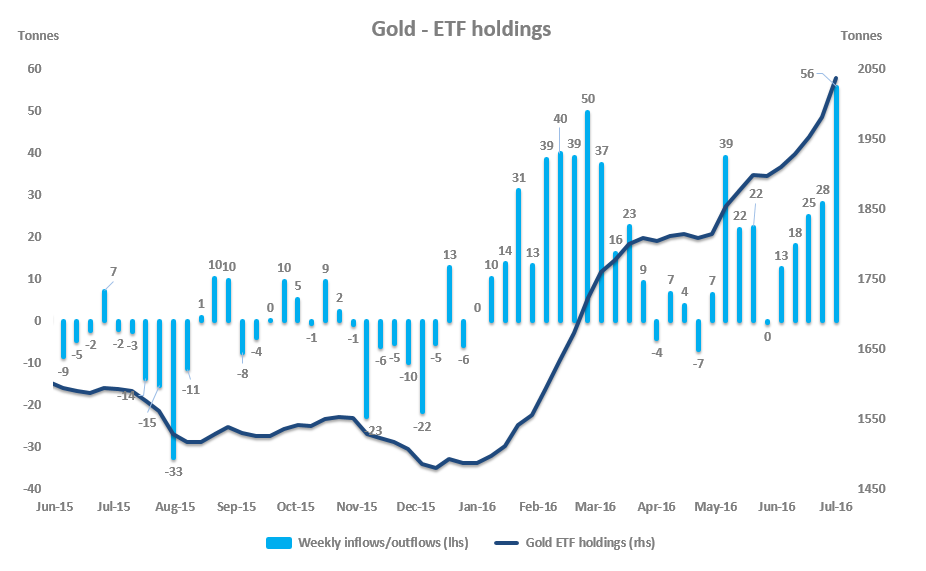

Gold. ETF investors boosted their holdings for a fifth consecutive week as of July 1, pushing total ETF holdings up to a fresh 2016 high of 2,037 tonnes, marking its highest level since July 2013.

ETF investors bought a total of 56 tonnes last week (+2.7 percent). Taking a look at ETF inflows/outflows dynamics in the entire precious metals complex, it is fair to argue that investors considered gold as the only "game in town". Over the same period (June 24 - July 1), ETF investors bought only 105 tonnes of silver (+0.5 percent), only 7,100 ounces of palladium (+0.3 percent), and actually sold 33,600 ounces of platinum (-1.4 percent), according to FastMarkets' estimates.

We recognize that there is currently a strong appetite for safe-haven related trades (long gold, core government bonds, yen, etc.) due to sizeable uncertainty about the global economy.

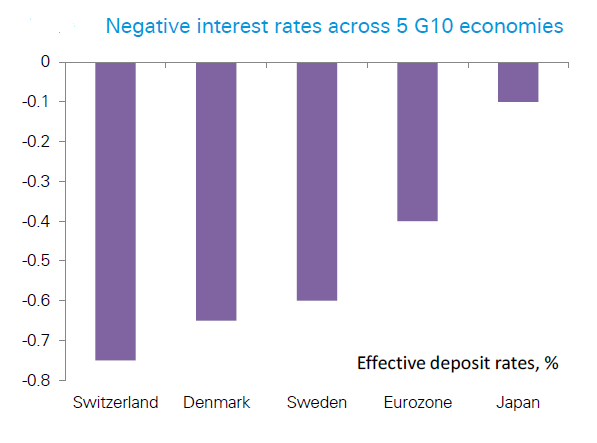

In addition, gold has better comparative advantage compared to most core government bonds defined as "safe-havens". While a few years ago, gold was criticized for being a non-yielding asset, it is now in a better posture than those government bonds in developed countries where interest rates are actually negative.

Source: Deutsche Bank.

Having said that, we remain of the view that gold ETF buying has mainly been the result of lower US interest rates, which has been exacerbated by momentum-based traders like George Soros or Stanley Druckenmiller.

Yes, ETF inflows could continue in the near-term because US interest rates continue to decline.

But our macro analysis suggests that the Fed may continue to remove gradually its monetary accommodation rather than to expand it as the market is currently pricing. A recalibration of market's rate expectations may put an end to the fall in US interest rates and induce some outflows in gold ETFs.

Another possible trigger of gold ETF outflows would be a prolonged recovery in risk-appetite. It seems so far that the Brexit shock had a muted negative impact on risky assets. Taking a look at the SPDR S&P 500 Trust ETF (NYSEARCA:SPY), it has recovered roughly 80 percent of its Brexit-losses. This could therefore suggest that investors are currently seeing US equities as an alternative safe-haven. Should the recovery in US equities be sustained, we would not be surprised to see some investors increasing their exposure toward SPY at the expense of gold.

However, we are currently of the view that risks to US equities are skewed to the downside.

Source: Trading View.

To sum up, we think that current ETF inflows, essentially driven by the fall in US real interest rates, may prove unsustainable once the Fed moves the market closer to its median view. This could probably happen this summer, during the July 26-27 FOMC meeting. The poor seasonality of gold in the summer months could reinforce ETF outflows, we think.

Spec positioning vs. investment positioning

Source: MikzEconomics.

SPDR Gold Trust ETF (NYSEARCA:GLD) positioning

Source: TradingView.

The SPDR Gold Trust ETF surged to a fresh 2016 high of $128.40 (intraday basis) last week, posting a weekly gain of 1.97 percent.

As we explained last week, the current picture remains positive in the near-term, principally because GLD is able to make higher highs, indicative of an upward trend.

But we remain of the view that further upward pressure will be limited in coming weeks, due to strong resistance level at the downtrend line (red).

Our speculative positioning analysis suggests that the speculative positioning in gold is overstretched on the long side and is therefore vulnerable to a reversal once US real interest rates enter a bottoming-out process. This could occur as soon as this summer, perhaps triggered by the upcoming Fed's meeting in July.

Our ETF positioning analysis suggests that investors currently gold as the only game in town, perhaps because most of its competing alternatives are not safe anymore (the risk-free asset has been removed due to the negative interest policy in a number of developed economies). But we also believe that inflows are exacerbated by momentum-based traders who may take the exit door in a rush in case of rising US real interest rates.

To sum up, we see a double selling pressure in gold coming this summer, which could undermine meaningfully prices.

Trading perspective

We are not currently positioned in GLD but we are looking to implement a short GLD position.

Our three trading criteria (fundamentals, technicals, tone) need to be met before jumping on the short side.

At present, it is important to recognize that those criteria are in favour of a further uptrend but we expect a reversal this summer. This is why we prefer to remain patient rather than getting sucked into this rally.

For longer-term investors, we remain of the view that accumulating gold on a regular basis in a well-diversified risky portfolio with a horizon of 5+ years will be a rewarding strategy, especially for non-US investors (the dollar will remain king in the coming years). But shorting gold later this year could provide a decent hedge against a sudden sell-off in gold.

Final note: we try to provide our SA readers with regular updates about the gold market - namely, what are the current drivers of the market and how market participants are positioned. While we express our bias toward gold (bullish, neutral, or bearish) on a weekly basis, we do not actually implement positions on a regular basis. In fact, given our conservative approach, we need to see our three trading criteria being met before initiating trade ideas. Equally important, when we implement trade ideas, we make sure that the reward-to-risk ratio of the hypothetical position is skewed in our favour (generally 3 or 4). This has allowed our GLD portfolio to perform well since the start of the year without taking a significant amount of risk in our individual trades.

For the sake of clarity, please find below the historical of our trade ideas since the start of the year.

We currently do not have active trade ideas.

0 comments:

Publicar un comentario