by: The Structure Of Price

- In a new long-term uptrend, the appetite of foreign central banks for bullion is a driver of gold price.

- The strategic value of gold reserves is potentially critical long after the era of the gold standard has passed.

- China, Russia, India and Saudi Arabia are aggressive acquirers of gold.

- The U.S. suffers a decline in strategic advantage regarding gold reserves.

- The strategic value of gold reserves is potentially critical long after the era of the gold standard has passed.

- China, Russia, India and Saudi Arabia are aggressive acquirers of gold.

- The U.S. suffers a decline in strategic advantage regarding gold reserves.

"The suspense is terrible. I hope it will last."

- Oscar Wilde

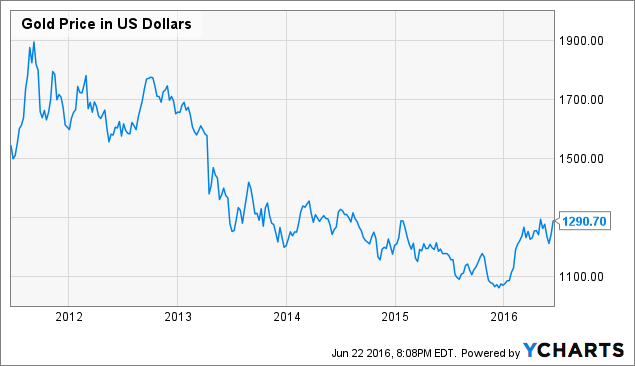

In the first months of 2016, gold established the beginning of a new long-term uptrend (see "The Future of Gold: A Long-Term Direction Upward"). It is important, therefore, to identify macroeconomic factors which may strongly impact the market either positively or negatively and mould its future. One of these factors is certainly the aggressive accumulation of gold bullion by foreign central banks - a positive driver of price.

Gold Price in US Dollars data by YCharts

For reference purposes, some of the most popular derivative instruments for investing in gold are the SPDR Gold Trust ETF (NYSEARCA:GLD), the iShares Gold Trust ETF (NYSEARCA:IAU), the Sprott Physical Gold Trust (NYSEARCA:PHYS), the ETFS Physical Swiss Gold Trust ETF (NYSEARCA:SGOL), the ProShares Ultra Gold ETF (NYSEARCA:UGL), and the DB Gold Double Long ETN (NYSEARCA:DGP).

Under the gold standard which prevailed until 1971, the creditworthiness of the U.S. was determined by the amount of its gold reserves. After Richard Nixon ended its convertibility to gold, the U.S. dollar has enjoyed a privileged position among fiat currencies, not least ironically because the United States is the country with the highest level of declared gold reserves.

An Essential Strategic Value

The primacy of the U.S. regarding gold reserves has not been just a notional association with the bygone era of the gold standard, a mere perception of strength. Gold reserves have an essential strategic value.

The U.S. Defense Department devotes considerable resources to disaster planning regarding future attacks on domestic financial targets. In the event that such attacks cause substantial damage, the downward pressure on the U.S. dollar may lead to the global economy turning increasingly to gold as a measure of value and economic standing. This is all the more likely when one may conclude that the limits of what monetary policy can do redemptively have been reached.

In 2015 alone, the U.S. Office of Personnel Management, an FBI portal, and those of at least nine banks and other financial institutions, including JPMorgan and Dow Jones, were hacked, and the personal details of over 100 million people with bank accounts were stolen in what the authorities called securities fraud on cyber steroids. The potential for broader, systemic attacks on a scale that would move generic markets is clear.

Other Strategic Considerations

Cyber attacks on financial arteries are far from the only strategic context in which the level of U.S. gold reserves may be called into play. Whether in the event of a significant stock market downturn, the economic collapse of other nations in an interconnected global economy, the fragmenting of nations, the dissolution of economic blocs, or debt default by the U.S., the amount of America's gold reserves would become of greatly increased importance in determining its future economic and geopolitical standing.

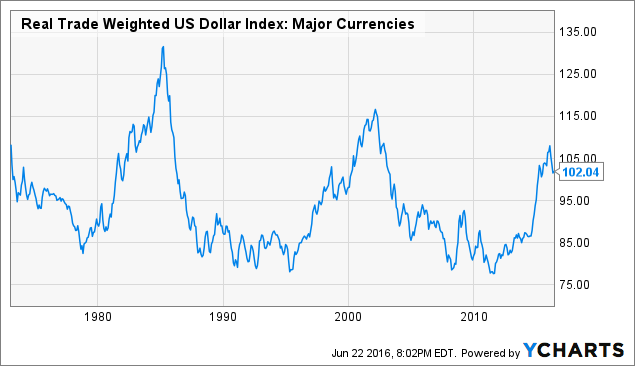

There has already been a long-term ranging downtrend in the value of the U.S. dollar as measured against other major currencies.

An examination of America's creditworthiness, or the creditworthiness of any nation, in a scenario where the value of the U.S. dollar is substantially lowered would bring scrutiny on the level of its gold reserves. This reference to national gold reserves will be all the more likely if the extent of the devaluation of the dollar approaches levels where creditors are less inclined to accept dollars in debt service payment.

A Matter Of National Security

The concomitant unloading of Treasuries by creditors would further exacerbate the dollar's fall and sharpen the focus on gold. In this way, a country's gold bullion reserves can still be said, even now, long after the days of the official gold standard have passed, to be a matter of national security.

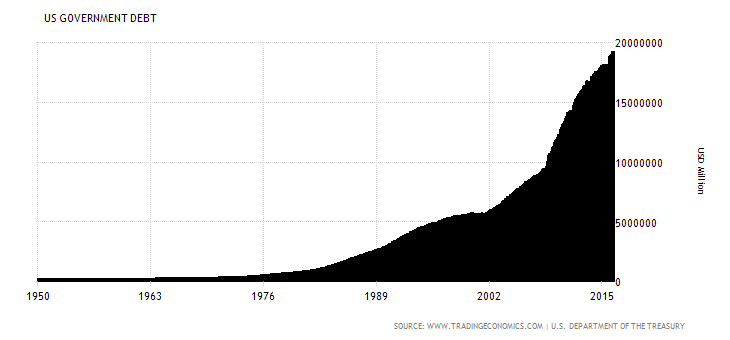

Central banks of other nations have reason enough, then, to anticipate in a post-easing world that the U.S. dollar may lose something of its relative value and pre-eminence as the world's reserve currency. Of particular concern would be a case where the U.S. defaults on its exponentially increasing national debt. Government debt in the U.S. reached an all-time high of USD 19265452 million in May 2016.

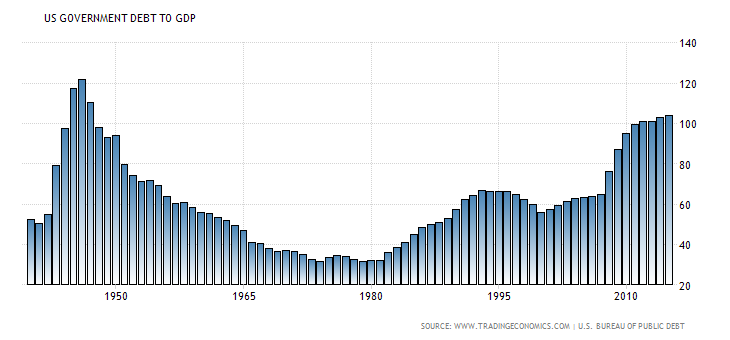

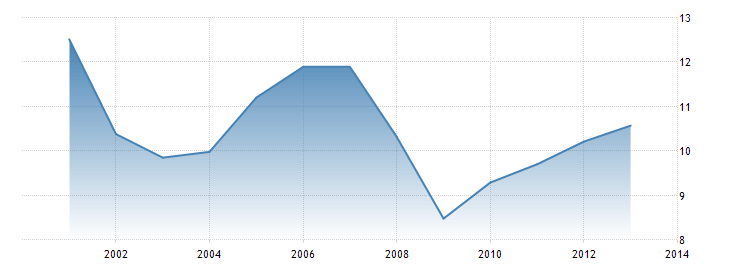

While the ratio of government debt to GDP is now lower than in the 1940s, implying a greater ability on the part of the government to repay, tax revenue as a percentage of GDP - indicating resources available to the government to make such repayments - has been falling.

U.S. tax revenue as a percentage of GDP:

(Source: TradingEconomics.com)

(Source: TradingEconomics.com)

This is the context in which other nations are formulating their policies on the level of their gold reserves. The IMF compiles statistics of national assets as reported by various countries. This data is used by the World Gold Council to periodically rank and report the gold holdings of countries and international financial organizations.

Gold Reserves By Country

The following table ranks nations and institutions by the size of their self-reported gold reserves in metric tonnes as of April 2016, and shows the percentage of that holding as a part of the country's total foreign exchange reserves.

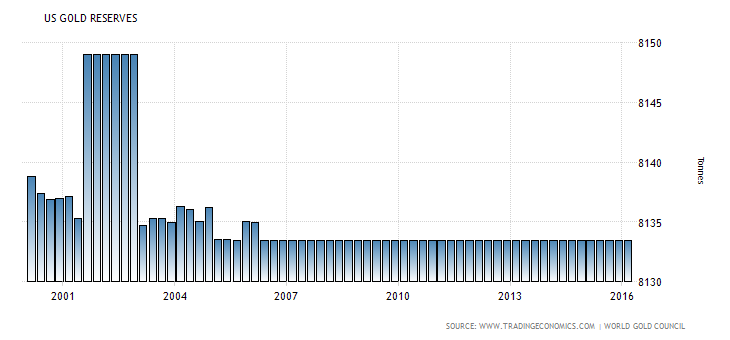

| 1 |  United States United States | 8,133.46 | 75.35% |

| 2 |  Germany Germany | 3,380.98 | 69.35% |

| 3 | International Monetary Fund | 2,814.04 | N.A. |

| 4 |  Italy Italy | 2,451.84 | 68.61% |

| 5 |  France France | 2,435.66 | 64.54% |

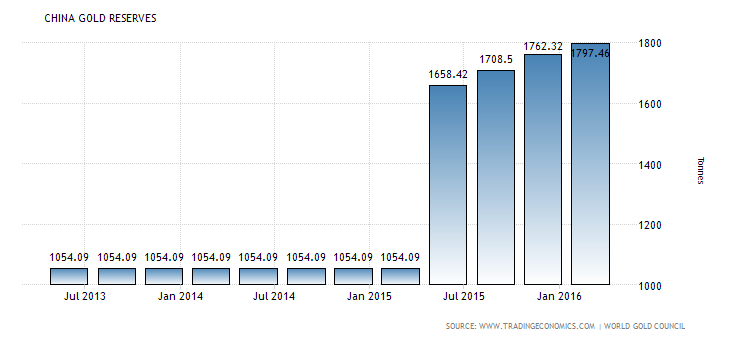

| 6 |  China China | 1,808.34 | 2.25% |

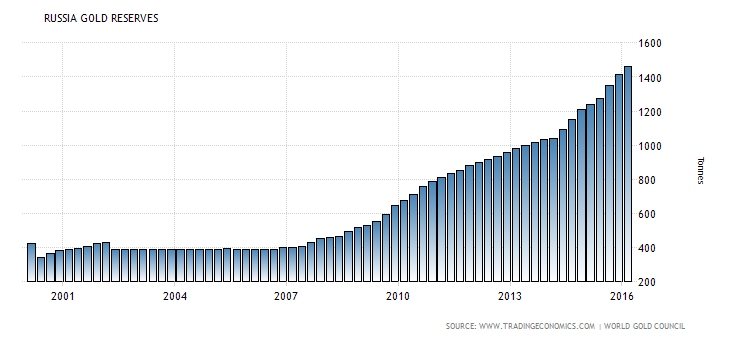

| 7 |  Russia Russia | 1,476.63 | 15.57% |

| 8 |  Switzerland Switzerland | 1,039.99 | 6.60% |

| 9 |  Japan Japan | 765.22 | 2.51% |

| 10 |  Netherlands Netherlands | 612.45 | 62.34% |

| 11 |  India India | 557.77 | 6.33% |

| 12 |  European Central Bank European Central Bank | 504.77 | 27.19% |

| 13 |  Turkey[14] Turkey[14] | 481.91 | 17.15% |

| 14 |  Republic of China (Taiwan) Republic of China (Taiwan) | 422.69 | 3.88% |

| 15 |  Portugal Portugal | 382.51 | 71.39% |

| 16 |  Saudi Arabia Saudi Arabia | 322.90 | 2.22% |

| 17 |  United Kingdom United Kingdom | 310.29 | 8.98% |

| 18 |  Lebanon Lebanon | 286.83 | 23.49% |

| 19 |  Spain Spain | 281.58 | 20.47% |

| 20 |  Austria Austria | 279.99 | 44.21% |

Russia has exponentially increased the level of its gold reserves since 2007, and now holds 15.57% of its total foreign exchange reserves in gold. Other aggressive acquirers of gold proportionate to their previous holdings are India and Saudi Arabia.

The level of gold reserves declared by the U.S. has, however, remained largely static since 2004, and raises questions as to U.S. policy on the strategic importance of gold. The global economic reality has, after all, changed greatly since 2004.

The matter of accurately assessing gold reserves held by nations is complicated by a lack of transparency. In addition to the IMF relying on self-declarations, the gold declared by each country may not be physically stored in that country. Central banks have not usually permitted independent audits of their reserves. It should also be borne in mind that gold leasing or rehypothecation by central banks could place in doubt the level of gold holdings they lay claim to.

Declining Strategic Advantage

If the IMF statistics on the level of U.S. gold reserves are accurate, then the U.S. has, over recent years, experienced a decline in strategic advantage relative to the acquisitive nations: China, Russia, India and Saudi Arabia. While the gulf in absolute levels of gold reserves is still great, the proportionate strategic advantage the U.S. holds is reducing.

There is little to indicate to date that any foreign nation is pursuing an increase in its gold reserves to an extent that would be a direct challenge to the global economic primacy of the U.S. The gap is presently too great. In fact, it is can be argued that none of the countries now aggressively acquiring gold wishes to see the U.S. dollar replaced as the world's reserve currency, in large part because they hold sizable foreign exchange reserves that are denominated in dollars. Also, there is no viable alternative candidate to the dollar among the fiat currencies.

Instead, their aggressive acquisition of gold may well be a fortress strategy rather than an attack strategy, with its progenitor being a negative assessment of the prospects for the U.S. dollar in a dystopian global economic future.

Conclusions

The sizable increases in the purchase of gold bullion by foreign central banks as a macroeconomic strategy may be expected to continue into the foreseeable future, and will be an upward driver of the price of gold.

The forward policy the U.S. implements regarding the presently diminishing relative advantage it holds over other nations in the amount of its gold reserves may well have global strategic implications for its future.

0 comments:

Publicar un comentario