China Is Now Driving Drunk - And You're The Passenger

by: The Heisenberg

- The party: global growth. The liquor: debt.

- The life of the party: China.

- Why did you agree to go along on a beer run?

- The life of the party: China.

- Why did you agree to go along on a beer run?

- It's Thursday afternoon.

- Your phone rings.

You hesitate, but you pick up.

"Hello?" (as if you don't know who it is).

"It's me. I'm having another party tomorrow. You're coming right?"

You try to hide your trepidation. You feign enthusiasm. "Yeah man, what time is everyone showing up?"

"Eight." Click.

Now you've RSVP'd. You have to show up. Crap.

It's not so much that you didn't have a great time at the last party, it's just that there towards the end, the host looked like he might have had one too many tequila shots and you, like most of the other partygoers, were scared of what might happen next.

("Once it hits your lips...")

Fortunately, he stumbled to his room and passed out. He didn't drive anywhere. Or fight anyone. But he could have. Who knows what's going to happen this Friday.

For those unfamiliar with the analogy, China is the drunk party host. The tequila is debt.

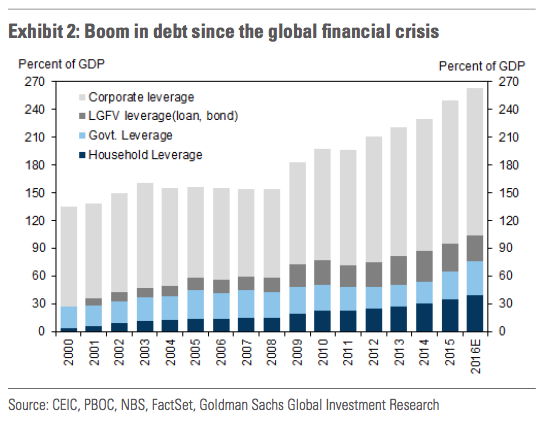

In all kinds of ways, China is the host of the global economic party. They're all at once the engine of growth and the barometer for demand. They're "behind the wheel," as it were. And make no mistake, they're drunk. Drunk on debt.

(Chart: Goldman)

Now the thing is, we don't know for sure where all the debt is. We don't know the extent to which 260% of GDP even captures it all. We don't know which sectors owe what to who. We don't know how much is obscured via banks' exposure to channel loans. We don't know what the real non-performing loans numbers are. Basically, we don't know anything. We're in the passenger seat, China is driving, China is clearly drunk, but we have no way to assess how drunk.

I'm not going to run through the mechanics behind China's sprawling shadow banking complex here.

If you want to know the details, it's covered here and here, among other places. Rehashing it takes forever, but I will say that in order to fully understand what follows, you need to read those linked pieces. Sorry. It's a pain, but diverting new readers to those is preferable to subjecting veterans to repetition and redundancy.

So China's mid-tier local banks are in deep. Like, waist deep. Recall the following from Reuters:

At China's mid-tier lender Industrial Bank Co, for example, the volume of investment receivables doubled over the first nine months of 2015 to 1.76 trillion yuan ($267 billion).

This is equivalent to its entire loan book - and to the total assets in the Philippine banking system, filings showed.

Remember, "investment receivables" is a line item Chinese banks have created to obscure the extent to which they're taking credit risk that doesn't show up as tradition loans. Here's what UBS financial analyst Jason Bedford, a former bank auditor in China told Reuters back in January:

These are now the fastest growing assets on the balance sheets of most listed banks, excluding the Big Five, not just in percentage terms but absolute terms. The concern is that the lack of transparency and mis-categorization of credit assets potentially hide considerable non-performing loans.

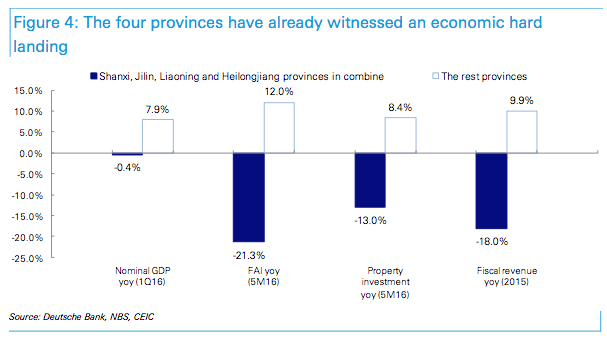

Precisely. Well, Deutsche Bank (whose work on China banking risk is unparalleled on the sellside) went looking for systemic risk at local banks in struggling provinces and guess what they found? Nothing good. Here are some excerpts from their latest:

An economic hard landing has already happened in north-eastern China and Shanxi province, with combined nominal GDP growth slowing to 1% yoy in 2015 and further to -0.4% in 1Q16.

In contrast, local banking asset growth remained strong at 16% yoy, with city/rural commercial banks and policy banks the key funding providers (assets up 26% for each type), while the big- five banks in the local market only grew their asset base by 6%. The 17 unlisted local banks, which made up 12% of local banking assets, recorded asset expansion of 22% yoy, mainly driven by fast-growing, higher-risk shadow credit (up 78% yoy). We think that these banks are likely providing "evergreen" lending to weaker corporates and hence are associated with higher credit risks.

When Deutsche talks about "evergreening", they're talking about companies that borrow just to service their existing obligations. In other words: these companies have reached their "Minsky moment."

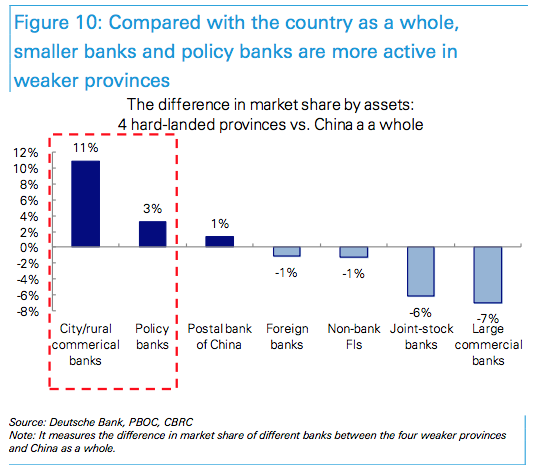

And don't think this is just local banks. The policy banks are there too:

(Chart: Deutsche Bank)

Not to put too fine a point on it, but Deutsche's takedown is devastating. Here's more:

The 17 local banks grew their asset balance by 22% yoy in 2015. If including the three listed banks in these four provinces, their asset growth registered at 28% yoy in 2015. This compares to the Chinese banking system as a whole at 15.7% yoy, nearly twice as fast. Furthermore, it is also stunning when compared with only 1% nominal growth in regional GDP. In our view, one explanation would be that these banks were extending "evergreen" credit to weaker corporates, in order to prevent unemployment and corporate bankruptcy.

The strong asset growth was mainly driven by shadow credit (58% of new assets), which was packaged in the form of receivable investments and available-for-sale (AFS) investments. Their receivable investments were up 85% yoy and accounted for 13% of total assets.

And finally, this:

With a relatively small loan book of c.Rmb50bn per bank, these 17 banks are more exposed to riskier sectors and also have a higher concentration of large customers.

As shown in Figure 18, they have notably higher exposure than listed banks to the manufacturing, wholesale & retail trade and mining sectors, which include the major overcapacity sectors (e.g. steel, cement, coal and non- ferrous etc.).

In short, one (or more) of these local banks is going to collapse. It's just a matter of time. And when it does, the question becomes whether that sends shockwaves through the rest of the system.

Remember, Kyle Bass's entire short thesis on the yuan (NYSEARCA:CYB) rests on the idea that Beijing will need to embark on a massive recap of the banking sector. Will a local bank be the first domino? Here's what I said last month:

If just one of these banks (even one of the country's 130+ city commercial lenders) goes under, it could send shock waves through the whole system and cause a crisis of confidence. It only takes one domino to trigger a collapse. That's when Bass's thesis comes into play. When it comes time to plug the holes, there's really no where to go but down for the yuan for the four reasons outlined at the outset.

If the Chinese banking system collapses (which it will), there's no alternative for the PBoC.

They'll have to deploy their balance sheet. And you know what that means, right? A sharply lower renminbi. You might as well take risk assets - including US equities (NYSEARCA:SPY) - into the back alley and execute them now. Show some mercy for God's sake.

And on that note, I'll close with an updated version of a chart I've shown many times previous:

0 comments:

Publicar un comentario