Why the European Bond Market Is on the Brink

Until the U.K. vote on EU membership is over caution looks advisable

By Richard Barley

.

Two German national flags blowing in the wind. Returns on German bonds of 5.3% this year are all about gains in prices, not interest payments that bond investors usually rely on, index data from Barclays show. Photo: Zuma Press

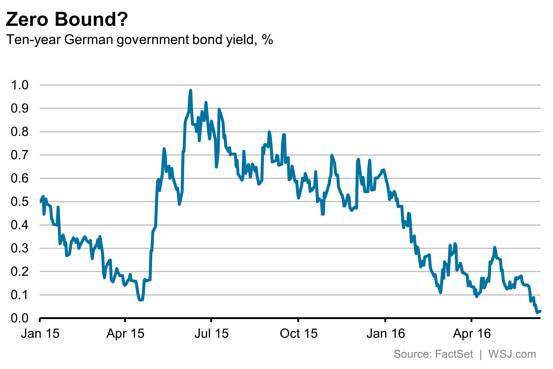

Two German national flags blowing in the wind. Returns on German bonds of 5.3% this year are all about gains in prices, not interest payments that bond investors usually rely on, index data from Barclays show. Photo: Zuma Press The European government bond market is setting more records. German 10-year yields have broken below the low of last April and are hovering just above zero. A move into negative territory would mark a new chapter in the extraordinary bull market for bonds.

The current level of 10-year yields, at around 0.03%, looks absurd for an instrument that is supposed to generate income. Indeed, returns on German bonds so far this year of 5.3% are all about gains in prices, not the steady flow of interest payments that bond investors usually rely on, index data from Barclays show. A move higher in yields would generate steep losses; at such low yields bonds are a high-risk affair.

But the reality is one of several forces that are combining. First, similar to last year, there is a feedback effect related to the European Central Bank’s bond purchase program. The ECB won’t buy bonds that yield less than its deposit rate, currently minus 0.4%. In Germany’s case, that rules out a whole swath of securities; only bonds maturing from January 2022 onward carry higher yields. Thus purchases have to fall more heavily on long-dated bonds. Were the ECB to remove this restriction, it would remove a significant distortion from the market—and increase the amount of German paper eligible for purchase by 65%, strategists at ING calculate.

On top of that, the repricing of U.S. interest-rate risk has piled more downward pressure on yields. The 10-year German yield had found it hard to break sustainably below 0.1% until May’s poor U.S. jobs figures slammed Treasury yields lower.

Meanwhile, risk aversion in Europe is clearly high ahead of next week’s U.K. referendum on membership of the European Union. A vote to leave would have serious consequences for Europe as well as for the U.K.; at the very best markets would face an extended period of uncertainty.

These short-term forces are powerful. A further shock to confidence probably would push yields below zero. But in the longer term, such yields are hard to explain except as the result of a market massively distorted by quantitative easing. That is particularly the case in the face of a continuing, albeit sluggish, recovery in the eurozone economy, and the likelihood that headline inflation will rebound higher as the drag from low oil prices fades.

Investors, however, have been burned time after time if they have bet seriously on rising yields.

At least until the U.K. vote is past, caution looks advisable—even if negative yields on 10-year bonds look like nonsense.

0 comments:

Publicar un comentario