This Is What Will Cause The Next Financial Crisis

by: Martin Vlcek

- I think the next financial crash will be boringly similar to the last one in many basic aspects.

- Real estate will be one of the asset classes being overvalued and imploding.

- Some global real estate markets may already be rolling over, and yet others are already much more relatively overvalued than the U.S.

- But in the U.S., I think the best part of the real estate party is just getting started.

- It is way too soon to leave the party. The bubble pop is probably at least 18 months away, if not much more.

- Real estate will be one of the asset classes being overvalued and imploding.

- Some global real estate markets may already be rolling over, and yet others are already much more relatively overvalued than the U.S.

- But in the U.S., I think the best part of the real estate party is just getting started.

- It is way too soon to leave the party. The bubble pop is probably at least 18 months away, if not much more.

I strongly believe the next financial crisis will happen for generally the same reasons as the last one: thanks to the ultra-low interest rate policy of many major central banks and thanks to high wealth inequality due to which the financial system is flooded with too much money chasing too few quality investments. To make matters worse, central banks are slowly but surely moving from ultra-low rates to outright negative rates.

What will be the troubled asset class?

There are many possible candidates but most of them are too small in relative size to destabilize the global financial system. Some such examples are the current mining and oil & gas junk debt or the auto loans. Even the student loans are arguably too small - unless these debt bubbles pop at the same time - which central banks should and will surely try very hard to avoid. They seem to have been doing just that for years, given what were possibly attempts at limiting the commodity (mining) bubble since 2011 and the oil & gas bubble that popped in mid-2014. Most recently, there are attempts at alleviating the student debt problem and make ~400,000 voters very happy several months before the presidential elections.

And most recently, one might guess the central banks tried to contain the panic buying in gold - perceived as the ultimate safe haven - by convincing the markets the FED is more likely to hike next month that the markets were previously expecting. The timing of the next step-up in the ECB asset purchases next month also helped as the bank will slowly start buying corporate debt and separately Greek government debt - which is tiny relative to global financial system but huge and impossible to repay in terms of Greece - is once again good for ECB purchases. If this is not a debt bubble, I don't know what is. But all these issues seem to be contained for some time, and the cans continue to be kicked down the road.

However, what has the size to potentially shake the financial system confidence again are China's debt bubble, the global real estate bubble, and the overall financial leverage in the global financial system. In order to remain focused, I want to cover only the real estate in this article. Unfortunately, we already know from 2008/2009 that this asset class is big enough to cause some real pain.

Real estate prices are high again

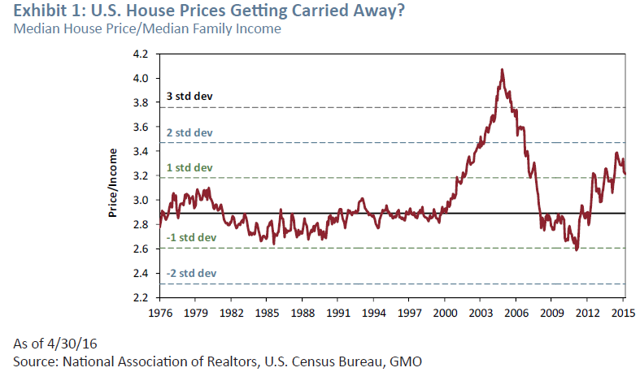

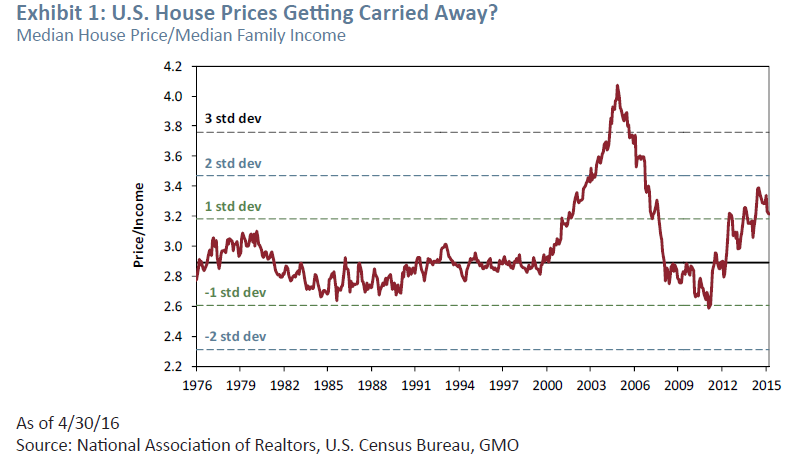

Using several sources, including Jeremy Grantham's GMO quarterly letter, it is clear global real estate prices are heating up again. In the U.S. alone (NYSEARCA:XHB), relative to historical averages, the median price/income ratio is now 1.5 sigma higher than the average figure for the past 40 years. In terms of the standard deviation from the median, we are already more than half way to the previous peak that ended very infamously in 2008/2009. Arguably, this echo-bubble should reach a lower peak as some investors will remain more careful than last time due to the relatively recent vivid memories of the previous bubble. If we believe this scenario, the U.S. housing prices will probably peak in a year or so.

Source: GMO investor letter

Source: GMO investor letter

But interest rates are even lower than last time

On the other hand, interest rates globally and in the U.S. are much lower today than during the previous bubble, so the current real estate prices look relatively more attractive due to the higher return differential over government bonds. In other words, the even bigger bubble in bonds (NYSEARCA:TLT) is making real estate (and other asset classes) relatively cheap. So it is very hard this time to estimate at what level the U.S. real estate prices will stall this time.

My educated guess is the peak will reach above 2 sigma but below last peak's ~3 sigma above the mean, and this could take about 18 months to two years. The timing will greatly depend on many factors and the central banks and governments will have one of the largest impacts on the magnitude and timing of both expansion and contraction of the asset class bubbles. Of course, there is no average house and some housing markets will peak sooner than others, within the U.S. and internationally.

And the prices are rising faaast in some global markets

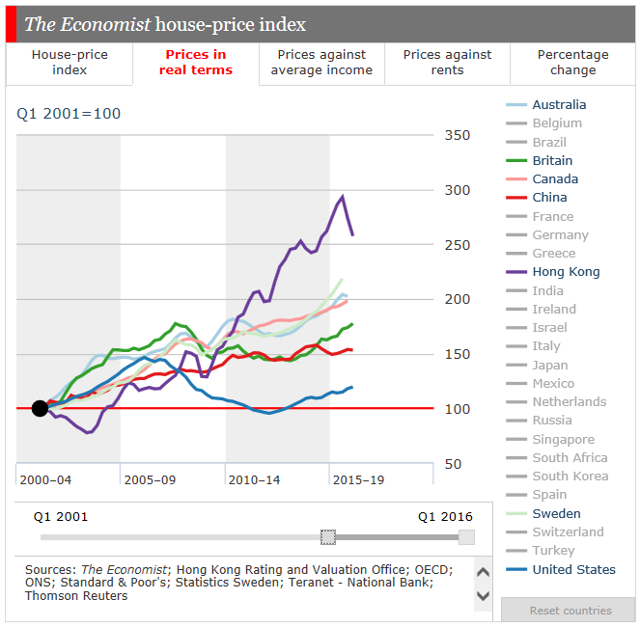

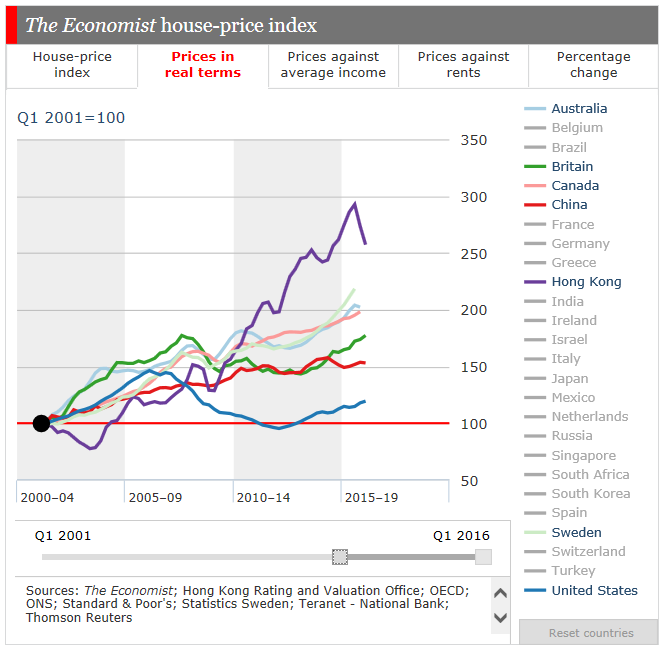

In fact, many real estate markets around the world have been on fire much more than the U.S. market, partly due to the local currency devaluation effects caused by the sharp dollar rise relative to the local currencies. While housing prices in real terms are much lower today in the U.S. than during the previous peak, they are already significantly above 2008/2009 in Canada, Australia, and the UK, among other countries. And Hong Kong is the champion where the bubble already seems to be bursting or at least correcting and being volatile both ways.

Source: The Economist, author selection of countries

Source: The Economist, author selection of countries

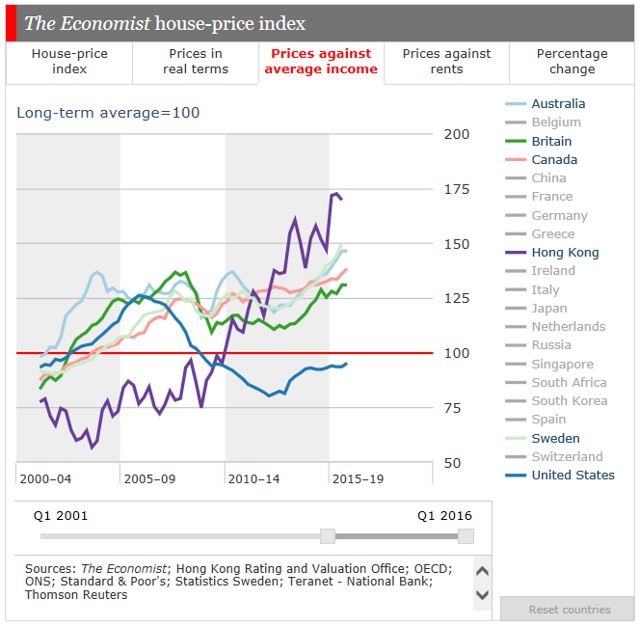

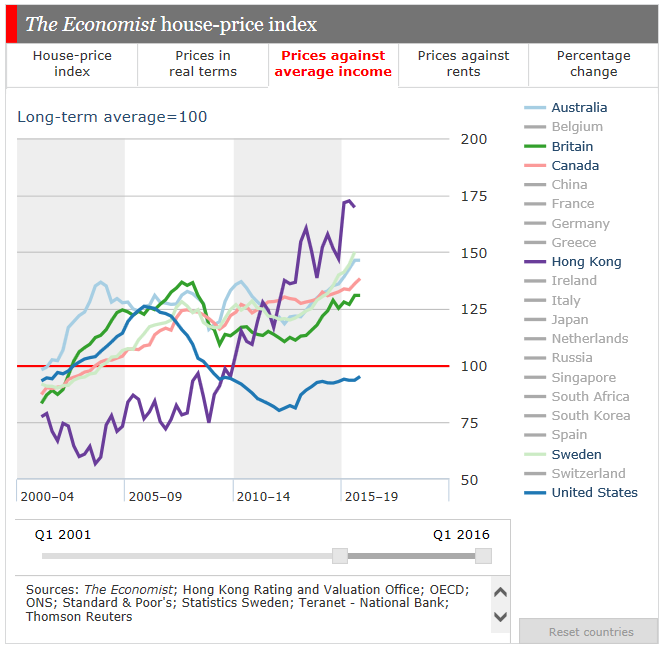

In terms of how expensive houses are for an average person, housing in many countries is already well above the previous peak.

In most of these countries, even the price-to-income ratios for real estate have already surpassed the previous peak levels. This is certainly the case for Hong Kong, Australia, Sweden, Canada and soon will be for the UK.

Source: The Economist, author selection of countries

Source: The Economist, author selection of countries

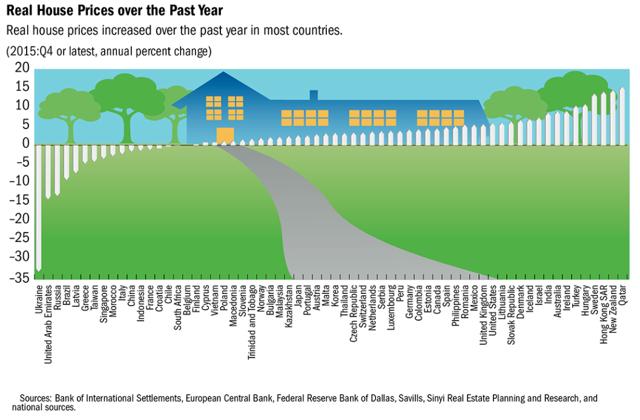

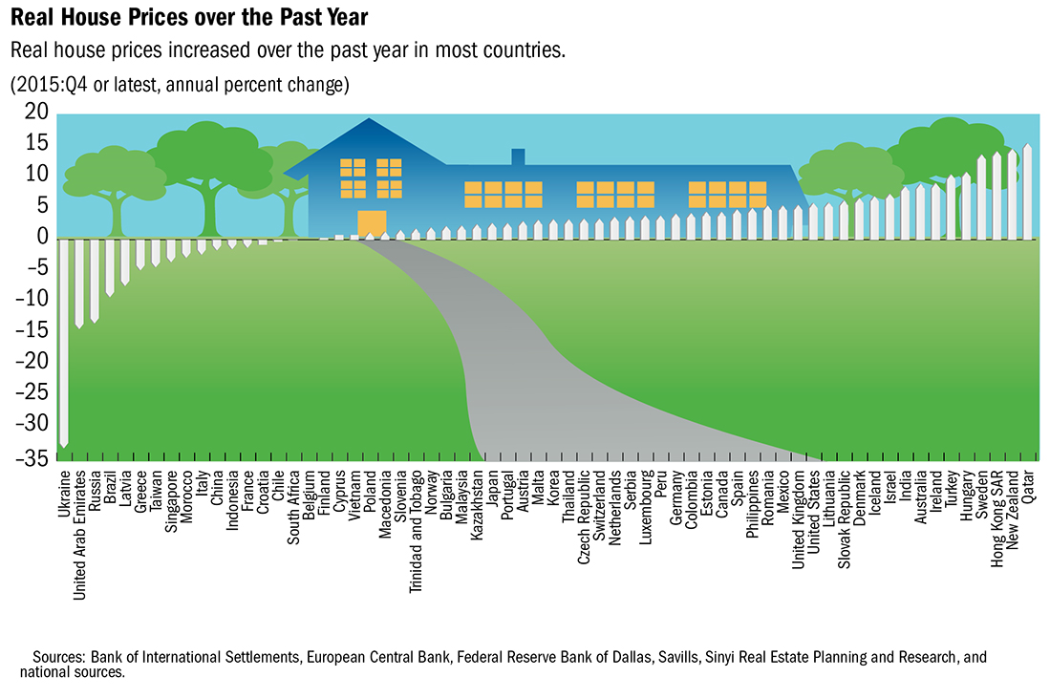

The most recent YoY growth in many markets has been brisk, to say the least, with prices in Qatar rising ~15% while New Zealand, Hong Kong, and Sweden all jumped more than 10%.

Source: IMF Global Housing Watch

Source: IMF Global Housing Watch

Conclusión

To conclude, the ultra-cheap money continues to chase various assets around the world, and real estate prices in many countries today are higher than they were in 2008 both in real price terms as well as in relation to average household income. Hong Kong, Australia, Sweden, Canada and the UK are some of the markets where investors should make sure they are buying good value before making the move. But I am not calling an immediate bubble pop even in these markets. It is too soon in my opinion.

The U.S. seems to be in a relatively solid spot relative to many other countries as the post-2009 price correction was very deep. However, even the U.S. already shows elevated levels of median income/price ratios above the historical average. But the real elephant in the room may be the relative overvaluation of global government bonds vs. almost any asset class. An industry veteran Bill Gross shorting credit now after being 4 decades in this business makes you pause for a moment.

Due to interest rates being lower now than in the previous cycle, real estate prices in the U.S. and globally may actually surprise us with several more years of growth before they peak this time. The bubble may grow bigger and more dangerous (fall even further) this time. U.S. real estate prices may even accelerate to the upside in the near term as global liquidity searches for the few relatively safe assets in the least dirty shirt fashion as a way to protect against reflation and devaluation in non-U.S. countries.

The strong April new home sales may be telling us something. And the large U.S. banks, such as Wells Fargo (NYSE:WFC) Bank of America (NYSE:BAC) and JPMorgan Chase (NYSE:JPM) have only just started really targeting the low-income and first-time home buyers with non-FHA mortgages and 3% down payments. So this clearly is a déjà vu but it is way too soon to leave the party yet.

What will be the troubled asset class?

There are many possible candidates but most of them are too small in relative size to destabilize the global financial system. Some such examples are the current mining and oil & gas junk debt or the auto loans. Even the student loans are arguably too small - unless these debt bubbles pop at the same time - which central banks should and will surely try very hard to avoid. They seem to have been doing just that for years, given what were possibly attempts at limiting the commodity (mining) bubble since 2011 and the oil & gas bubble that popped in mid-2014. Most recently, there are attempts at alleviating the student debt problem and make ~400,000 voters very happy several months before the presidential elections.

And most recently, one might guess the central banks tried to contain the panic buying in gold - perceived as the ultimate safe haven - by convincing the markets the FED is more likely to hike next month that the markets were previously expecting. The timing of the next step-up in the ECB asset purchases next month also helped as the bank will slowly start buying corporate debt and separately Greek government debt - which is tiny relative to global financial system but huge and impossible to repay in terms of Greece - is once again good for ECB purchases. If this is not a debt bubble, I don't know what is. But all these issues seem to be contained for some time, and the cans continue to be kicked down the road.

However, what has the size to potentially shake the financial system confidence again are China's debt bubble, the global real estate bubble, and the overall financial leverage in the global financial system. In order to remain focused, I want to cover only the real estate in this article. Unfortunately, we already know from 2008/2009 that this asset class is big enough to cause some real pain.

Real estate prices are high again

Using several sources, including Jeremy Grantham's GMO quarterly letter, it is clear global real estate prices are heating up again. In the U.S. alone (NYSEARCA:XHB), relative to historical averages, the median price/income ratio is now 1.5 sigma higher than the average figure for the past 40 years. In terms of the standard deviation from the median, we are already more than half way to the previous peak that ended very infamously in 2008/2009. Arguably, this echo-bubble should reach a lower peak as some investors will remain more careful than last time due to the relatively recent vivid memories of the previous bubble. If we believe this scenario, the U.S. housing prices will probably peak in a year or so.

Source: GMO investor letter

Source: GMO investor letterBut interest rates are even lower than last time

On the other hand, interest rates globally and in the U.S. are much lower today than during the previous bubble, so the current real estate prices look relatively more attractive due to the higher return differential over government bonds. In other words, the even bigger bubble in bonds (NYSEARCA:TLT) is making real estate (and other asset classes) relatively cheap. So it is very hard this time to estimate at what level the U.S. real estate prices will stall this time.

My educated guess is the peak will reach above 2 sigma but below last peak's ~3 sigma above the mean, and this could take about 18 months to two years. The timing will greatly depend on many factors and the central banks and governments will have one of the largest impacts on the magnitude and timing of both expansion and contraction of the asset class bubbles. Of course, there is no average house and some housing markets will peak sooner than others, within the U.S. and internationally.

And the prices are rising faaast in some global markets

In fact, many real estate markets around the world have been on fire much more than the U.S. market, partly due to the local currency devaluation effects caused by the sharp dollar rise relative to the local currencies. While housing prices in real terms are much lower today in the U.S. than during the previous peak, they are already significantly above 2008/2009 in Canada, Australia, and the UK, among other countries. And Hong Kong is the champion where the bubble already seems to be bursting or at least correcting and being volatile both ways.

Source: The Economist, author selection of countries

Source: The Economist, author selection of countriesIn terms of how expensive houses are for an average person, housing in many countries is already well above the previous peak.

In most of these countries, even the price-to-income ratios for real estate have already surpassed the previous peak levels. This is certainly the case for Hong Kong, Australia, Sweden, Canada and soon will be for the UK.

Source: The Economist, author selection of countries

Source: The Economist, author selection of countriesThe most recent YoY growth in many markets has been brisk, to say the least, with prices in Qatar rising ~15% while New Zealand, Hong Kong, and Sweden all jumped more than 10%.

Source: IMF Global Housing Watch

Source: IMF Global Housing WatchConclusión

To conclude, the ultra-cheap money continues to chase various assets around the world, and real estate prices in many countries today are higher than they were in 2008 both in real price terms as well as in relation to average household income. Hong Kong, Australia, Sweden, Canada and the UK are some of the markets where investors should make sure they are buying good value before making the move. But I am not calling an immediate bubble pop even in these markets. It is too soon in my opinion.

The U.S. seems to be in a relatively solid spot relative to many other countries as the post-2009 price correction was very deep. However, even the U.S. already shows elevated levels of median income/price ratios above the historical average. But the real elephant in the room may be the relative overvaluation of global government bonds vs. almost any asset class. An industry veteran Bill Gross shorting credit now after being 4 decades in this business makes you pause for a moment.

Due to interest rates being lower now than in the previous cycle, real estate prices in the U.S. and globally may actually surprise us with several more years of growth before they peak this time. The bubble may grow bigger and more dangerous (fall even further) this time. U.S. real estate prices may even accelerate to the upside in the near term as global liquidity searches for the few relatively safe assets in the least dirty shirt fashion as a way to protect against reflation and devaluation in non-U.S. countries.

The strong April new home sales may be telling us something. And the large U.S. banks, such as Wells Fargo (NYSE:WFC) Bank of America (NYSE:BAC) and JPMorgan Chase (NYSE:JPM) have only just started really targeting the low-income and first-time home buyers with non-FHA mortgages and 3% down payments. So this clearly is a déjà vu but it is way too soon to leave the party yet.

0 comments:

Publicar un comentario