The Next Bear Market Will Be Ruthless

by: Eric Parnell, CFA

Summary

- It has been almost nine years since the outbreak of the financial crisis. And it has been more than seven years since the start of the most recent bull market.

- The Fed has created a bubble not only in asset prices but also in the investor belief that the value of their investments will be protected no matter what.

- Unfortunately, the next bear market will eventually come, and it is likely to be ruthless once it finally arrives.

- Investors who recognize such an eventual reality can stand at the ready to capitalize once the time finally arrives.

- The Fed has created a bubble not only in asset prices but also in the investor belief that the value of their investments will be protected no matter what.

- Unfortunately, the next bear market will eventually come, and it is likely to be ruthless once it finally arrives.

- Investors who recognize such an eventual reality can stand at the ready to capitalize once the time finally arrives.

It has been almost nine years since the outbreak of the financial crisis. And it has been more than seven years since the start of the most recent bull market. Stocks have been impressively resilient in the face of every test during the post-crisis period thanks in large part to the seemingly endless support from monetary policymakers including the U.S. Federal Reserve.

This has helped foster an environment where many investors are not only comfortable but have swagger about owning stocks at historically high valuations despite chronically slow growth. As a result, the Fed has helped create bubbles not only in asset prices but investor expectations that the principal value of their investments will be upheld no matter what challenges befall the economy. Unfortunately, just like the bursting of the tech bubble and the onset of the financial crisis, the next recession will finally come. And when it does, it has the potential to be absolutely ruthless for investors.

Let's Get This Out Of The Way

I can already hear the bulls sharpening their knives for the comment section of this article, and I very much look forward to reading and responding to all points of view including those that strongly disagree with my article, but let me get out in front with a few observations.

Indeed, I have been bearish for some time, but this does not mean that I'm predicting that everything is going to go up in smoke tomorrow. Just as the tech bubble went about four years longer than it probably should have, the same could definitely be said for today's market.

Moreover, we could see the S&P 500 Index (NYSEARCA:SPY) continue to rally for the next several months or couple of years. Then again, we could already be one year into a new bear market. Only time will tell. But what's important to note is that the higher and longer today's market continues to rise, the longer and harder it is likely to fall on the backside. In the meantime and until we start to definitely roll down the other side of the mountain, I have and will continue to hold a meaningful allocation to stocks.

But isn't my holding stocks a contradiction to my bearish view? Absolutely not. For just as being bullish does not mean that one should be all in and 100% allocated to equities, being bearish does not imply that one should be completely out of stocks and hide away in a bunker waiting for the world to end. Bear markets slowly evolve over long-term periods of time, and selected segments of the stock market have historically demonstrated the ability to perform well during different stages of bear market cycles. For example, consumer staples (NYSEARCA:XLP), utilities (NYSEARCA:XLU) and healthcare (NYSEARCA:XLV) stocks all typically perform well during the early stages of a bear market, and selected specific stocks of various styles and sizes such as Wal-Mart (NYSE:WMT), Village Super Market (NASDAQ:VLGEA), Community Bank System (NYSE:CBU) and Southern Company (NYSE:SO) have demonstrated the ability to perform well throughout the entirety of two of the worst bear markets in history in the bursting of the tech bubble and the financial crisis. So while I may not be loaded up on the SPY, the market offers a solid menu of stocks that one can hold through the worst of a market storm. I also own a lot of other things outside of stocks that are performing well today and I expect will perform even better during any future bear market in stocks.

Also, isn't my making a statement that the next bear market could be "absolutely ruthless" for investors nothing more than fear mongering? No, it is not. Instead, it is trying to increase investor awareness of a view that they may not otherwise be hearing. After all, one only has to tune into one of the major financial news networks to hear a cornucopia of bullish views on the market, many from analysts that have a direct vested interest in promoting such bullish views and reassuring the audience that despite any short-term rough patch that "stocks will be trading higher by the end of the year."

Conversely, those expressing a bearish view are often met with heavy pushback and scowling derision. As a result, this leaves many that may be less experienced with investment markets exposed to the risk of wondering "why didn't I see this coming" when they eventually find themselves locked in the jaws of the next bear market.

In the end, it is up to individual investors to decide how they wish to proceed with their own portfolio allocation. But by sharing this more bearish perspective on today's markets - it at a minimum provides investors with a viewpoint to consider that they may not be hearing elsewhere.

Now that we've got that out of the way, let's get down to it.

The Economic/Market Disconnect

The next bear market is setting up to be ruthless for investors. But this does not mean that it will be ruthless for the U.S. economy. In fact, it would not be surprising at all to see a prolonged and significant decline in stocks accompanied by what amounts to a somewhat longer than normal but otherwise relatively mild economic recession. How can this be the case? Simple.

Since Main Street (NYSE:MAIN) hardly participated in the glorious ascent that has been Wall Street via the stock market over the past seven plus years, Main Street is not likely to suffer nearly as much when stock prices come falling back to earth. In fact, many parts of Main Street might actually find themselves benefiting in many ways including even lower interest rates on loans, lower gasoline prices at the pump and the execution of more effective fiscal programs by policymakers that finally have had a long overdue fire lit under them.

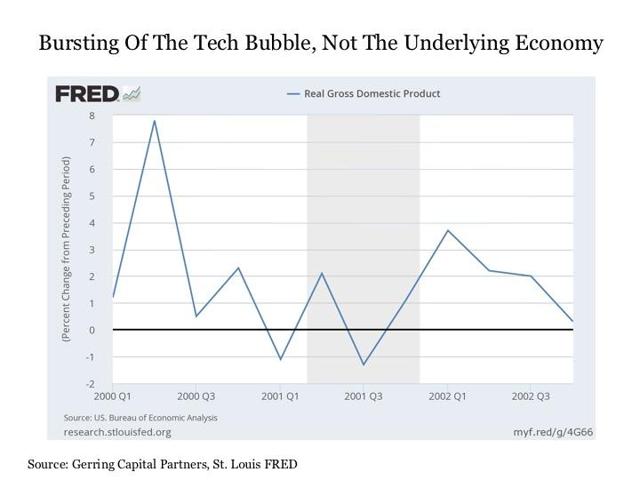

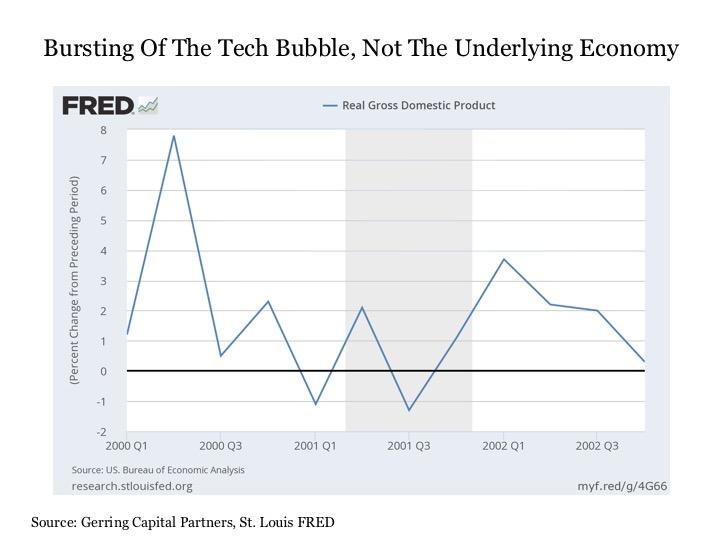

Impossible, you might say. How can we have a major stock market decline with a relatively milder impact on the broader economy? One has to look no further than the bursting of the technology bubble from 2000 to 2002. During this time period, stocks declined by more than -50%, but the economy hardly even declined. Although we officially had a recession from March 2001 to November 2001 according to the National Bureau of Economic Research (NBER), the overall decline in U.S. real GDP was -0.3% and we didn't even have two consecutive quarters of negative growth during this stretch. This recent example highlights the fact that it is certainly possible to have a stock market more than cut in half without any measurable contraction in economic activity. For if stock valuations get too far ahead of the economy, as they were then and are arguably today, they then have a huge air pocket through which to descend by simply falling back to the underlying economic reality.

What About Not Fighting The Fed? Lest We Forget - Lest We Forget!

What about fighting the Fed? Haven't we learned by now during the post-crisis period that the U.S. Federal Reserve and their global central bank counterparts are going to do whatever it takes to protect stock prices at every turn? This has been definitely true in recent times as any attempts to try and short the market over the past seven years when it looked like stocks were going to break sharply to the downside have been absolutely steamrolled along the way. But in order to avoid falling victim to recency bias, just because this has been true in recent years does not mean that it is universally true.

In fact, the history of the Fed is filled with examples of them winning so many of the battles but ultimately losing the wars.

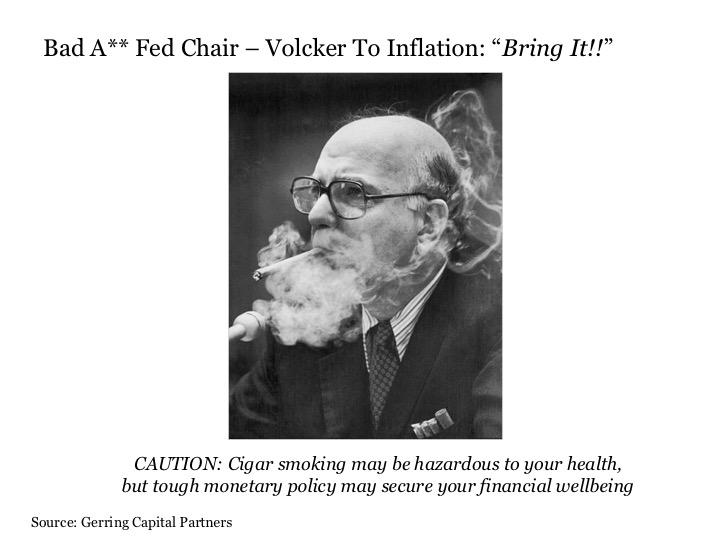

To set the stage for this point, let's go back to the last great Fed victory, which was winning the war over inflation back in the early 1980s. How did the Fed win this war? Because it was willing to endure the hardship, lose the battles, and suffer the sacrifice to prevail with overall victory in the end.

Then Fed Chair Paul Volcker did not coddle and cajole the economy and financial markets at the time in working to solve the problem. Instead, he dialed up interest rates to nearly 20% and ripped the heart out of the inflation problem. During this time, the economy endured two back-to-back recessions and a solid bear market, but it set the stage for the years of prosperity that followed in the 1980s and 1990s. In short, the Fed was willing to lose some battles to win the war. And until former Fed Board Governor Kevin Warsh is appointed to the position, Mr. Volcker will remain my favorite all-time Fed Chair.

So what have we seen since? Under Fed Chair Alan Greenspan, we saw the Fed win battle after battle. This included the stock market crash of 1987, the recession of 1990, the should-have-been recession of 1994, the Asian Flu in the late 1990s, and the collapse of Long-Term Capital Management in 1998. And the Fed did so by helping investors avoid any pain along the way.

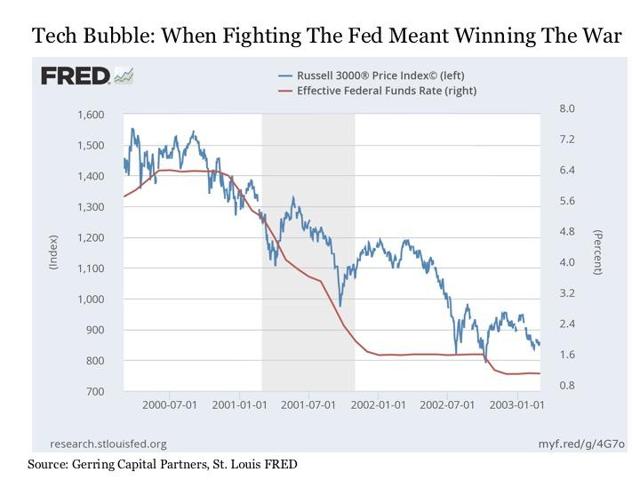

Yet, in the end, they lost the war, as the tech bubble finally burst with roughly four years of investor gains during the late 1990s evaporating in the process.

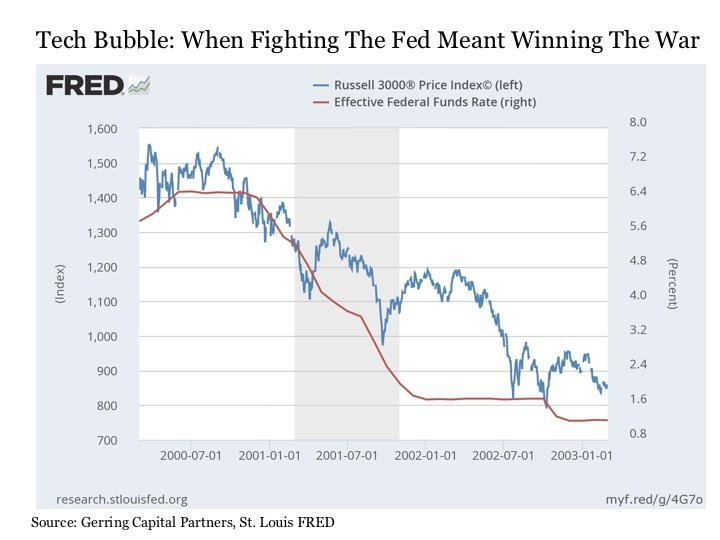

About that Fed put. While it is easy to forget, particularly when it has lifted markets for so many years, but the Fed does not always get what it wants from stocks with accommodative monetary policy. Lest we forget! During the bursting of the tech bubble, the Fed was aggressively lowering interest rates for three years starting in early 2000, yet stock prices lost more than half of their value before finally bottoming in late 2002 and early 2003.

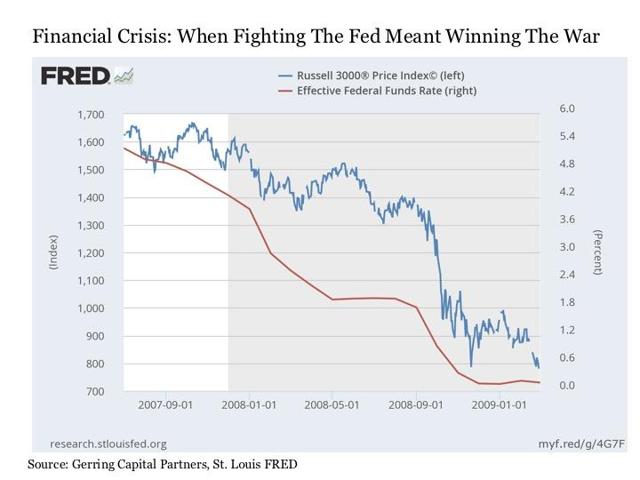

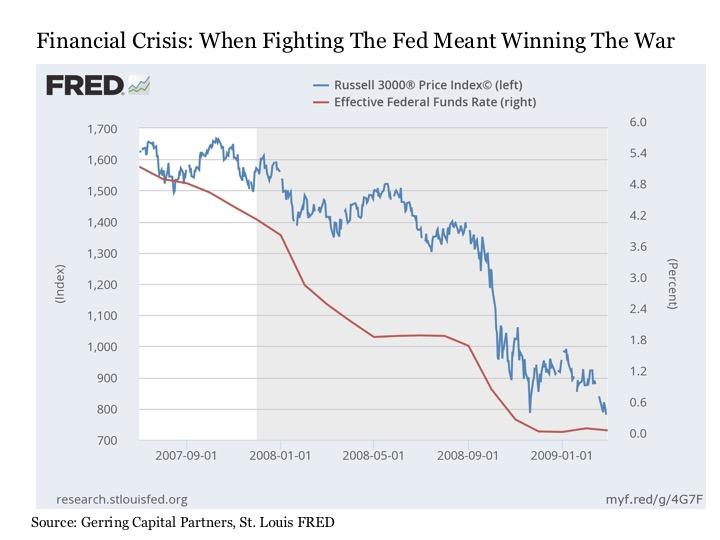

But then came the post-tech bubble period. Under Fed Chairs Alan Greenspan and Ben Bernanke, the Fed once again was winning all of the wars thanks to low interest rates and a booming housing market. And once again, investors were able to bask in the warmth of an accommodating market filled with gains and free of pain. In the process, they managed to bring the stock market all the way back to its tech bubble highs. But in the end, the Fed once again lost the war, as the housing bubble burst with nearly catastrophic consequences. By the time the financial crisis was brought under control in March 2009 (not fixed, but brought under control), the market had exceeded the losses of the tech bubble to the downside and was back to the same level it had first reached more than a decade earlier.

Once again, the Fed put does not always work. Lest we forget! During the financial crisis, the Fed was once again aggressively lowering interest rates for nearly two years starting in mid-2007, eventually lowering interest rates to zero and launching into quantitative easing along the way, yet stock prices once again lost more than half of their value before finally bottoming in early 2009.

All of this leads us to today. Under Fed Chair Ben Bernanke, the Fed has won all of the battles by giving investors everything they could ever imagine and more. Stocks have skyrocketed virtually without interruption and investor pain has been virtually non-existent. In the process, the Fed managed to catapult the stock market more than one-third higher above its tech bubble and pre-financial crisis peaks. And they did so with a global economy that has been sluggish, uneven and lackluster at best.

Why The Next Recession Will Be Ruthless For Stocks

Maybe the outcome this time around will be different. But given the historical pattern over the past two decades, my bet remains that the Fed will end up losing this war once again.

Why? Let's begin with the qualitative, which is that war is not won by bypassing the pain and sacrifice necessary to prevail. And until policymakers finally decide that they are ready to win the war and replace the monetary cotton candy with a steady diet of spinach, we are likely to continue in these monetary induced boom and bust cycles.

Now let's get to the quantitative. What enabled the Fed to rescue the stock market after the last two lost wars? Because they entered financial markets firing all monetary guns for an extended period of time lasting two to three years in order to get the markets stabilized and moving higher again. But let's assume whatever bubble of the many that exist today finally bursts and sends stocks sustainably lower despite all of the best efforts and jawboning by the U.S. Federal Reserve and their global cohorts. From exactly what arsenal are they going to fire from to turn the stock market around so quickly this next time around?

Will it be lowering interest rates by several percentage points? No, because interest rates are already effectively still at zero in the U.S. and negative in much of the developed world outside of the U.S. And the temptation to go further into negative interest rate territory is unlikely, for not only has it not lifted stock price in any measurable way, evidence is growing by the day that it simply does not work and is causing more harm than good.

Will it be launching into yet another round of aggressive quantitative easing? Perhaps, but what is the justification for putting our global fiat currency system that is still a baby at only less than half of a century old at even greater peril than it already is for returning to a program that simply has not worked in generating sustained economic growth over the past seven years?

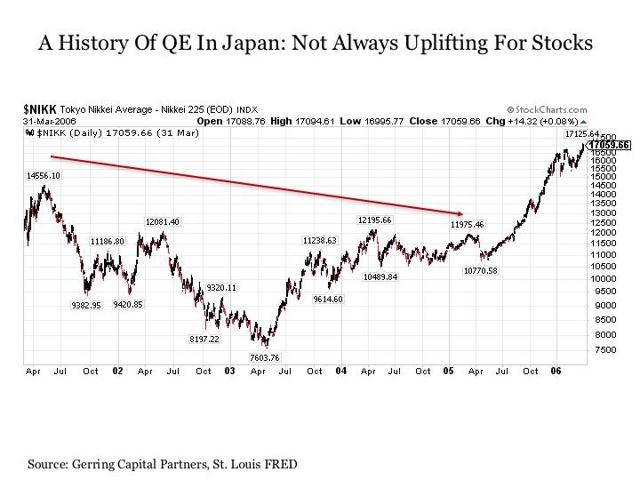

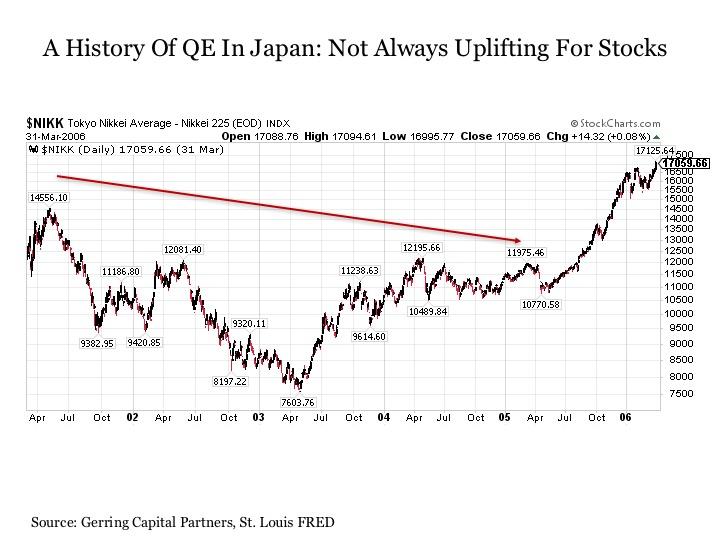

With that said, I still wouldn't put it past the Fed to go back to this well, but it stands to question what the marginal benefit to stock prices would be at the end of the day. Lest we forget the experience that Japan (NYSEARCA:EWJ) had with quantitative easing from March 2001 to March 2006 when the Bank of Japan increased its balance sheet by more than seven-fold, with the lion share of the increases taking place during the first three years of the program.

Yet during the first several years of the program, stock prices were cut in half before finally finding their footing. And they didn't begin bursting to the upside until more than four years after the launch of the program, and this was thanks in part to a global tailwind where the rest of the global economy was already well into its post tech bubble recovery at that point.

If and when stocks began falling in earnest the next time around, be it because of the onset of the next recession or the bursting of a bubble in capital markets, it is very likely that global central banks will lack sufficient monetary firepower and policy flexibility to stem the decline lower in stocks. In short, markets may finally be allowed to wash themselves out and cleanse themselves despite what monetary policymakers wish to allow. It's the return of Volcker-style monetary policy whether global central banks want it or not.

It should be noted that such a decline is likely to cut deeper and last longer than the two major bear markets that preceded it since the start of the new millennium. It will likely lead to a larger overall decline in the end due to the fact that central bankers will lack the resources to reverse the overall market decline the next time around. And it will likely last longer because central bankers are likely to try and fight the decline in global stock markets at every turn, as there will almost certainly be no Lehman Brothers style bandage ripping off next time around.

The good news is that it will provide investors with several opportunities to evacuate the market before the lights fully go out. One could even argue that the market is providing investors with such opportunities as we speak today.

Moreover, such a longer, more gradual bear market would provide abundant short-term trading opportunities for the nimbler investors among us. The bad news is that the next bear market is likely to feel as agonizingly long as the bull market has seemed endless today.

The Silver Lining

Such an outcome would certainly be difficult to endure and is unfortunately likely to leave a good number of investors smarting from the inevitable loss in portfolio value sustained by many along the way. But the silver lining to such an outcome is an American-style happy ending.

We don't reflect back with regret on the challenges that we had to endure during the late 1970s and early 1980s when the inflation rate was pushing toward 15% and the Fed had to crank up its restrictive monetary policy deals to fix the economy. Instead, many reflect on that time with tales of courage like how they had to walk into a bank and get a mortgage with sky-high interest rates in order to provide their family with a place to live after relocating to a new city.

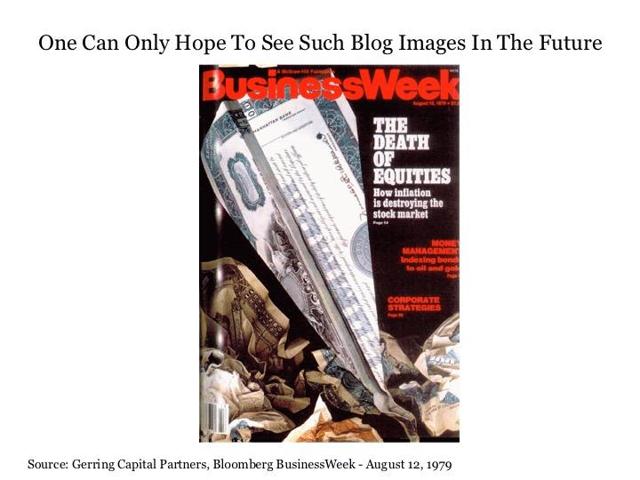

And almost nobody regrets the years of sustained economic prosperity that followed during the 1980s and 1990s, and that includes struggling through the markets at the time that inspired the now much ridiculed "Death of Equities" magazine cover that came along the way. In short, suffering through this inevitable market pain ahead will bring us to the dawn of the next great phase of sustained economic growth in the United States and around the world.

Just as importantly, the fact that stocks are set up for a fall due in part to monetary policymakers being just about out of firepower will likely finally induce frustratingly complacent and bungling political leaders to get off their collective duffs and finally start working together in enacting effective fiscal policy to fix the chronic problems that have existed around the globe for far too long.

The general voting population around the world are really angry, and for good reason. It is because their political systems and leaders from the major established parties have failed them badly. This is a big part of the reason why we have seen the rise of outsider candidates such as Donald Trump and Bernie Sanders here in the United States and scores of outsider candidates in countries around the developed and emerging world rise to the forefront of political influence. It is also part of the reason why a candidate like Gary Johnson that effectively finished tenth out of nine candidates in the 2012 Republican primaries and could not even consistently make the debate stage that year has recently been registering in the double-digits in the general election polls as the Libertarian candidate for president in 2016. It's because the masses want big time change to happen that includes much more effective fiscal policy and they are willing to go to whatever lengths necessary to endure whatever pain required and to elect whatever candidate is needed to make it happen. And if the markets go through such a corrective cycle in the coming years, the people are likely to get this outcome regardless of who takes office both in the U.S. and in countries around the world.

The Bottom Line

Whether it starts tomorrow, next month, three years now, or already started more than a year ago, the next bear market is likely to be ruthless both in depth and duration. And the higher stocks continue to climb today, the more ruthless the next bear market is likely to be in the end.

Investors can ignore the likelihood for such an outcome, but they do so at their own peril.

Instead, investors can be well served by embracing or at least recognizing such a potential outcome and preparing their portfolio accordingly. This does not mean moving to cash right now, running for the hills and stockpiling your emergency food rations. Instead, it means crafting a game plan that includes stocks as well as components from various other asset classes that are not stocks so that you are ready to capitalize on the various ebbs and flows of the market as it travels through such an extended corrective process. After all, some of the greatest and most legendary investment gains have been made during extended bear markets, and the next time around is likely to be no exception in this regard. For those who are interested, this is an area among others that we explore in much great detail on my premium service The Universal.

Perhaps the most positive outcome of all is the following. By enduring such a cleansing process in the global economy and financial markets, as painful as it might be along the way, it will finally bring us all to that 1921, 1946, and 1982 moment where we stand at the dawn to watch the sunrise on the next great sustained global economic expansion. Nobody said the journey through the 1910s into the early 1920s, the 1930s into the 1940s, and the 1970s into the early 1980s was easy, but they were required to bring us to the periods of great prosperity that followed.

The good news is that we have already endured the challenges of the 2000s and the early 2010s.

Now we just need to finish it off with one final cleansing phase, if only monetary policymakers would finally get out of the way and fiscal policymakers would finally get on with it. Perhaps we will find out sooner rather than later one way or another.

This has helped foster an environment where many investors are not only comfortable but have swagger about owning stocks at historically high valuations despite chronically slow growth. As a result, the Fed has helped create bubbles not only in asset prices but investor expectations that the principal value of their investments will be upheld no matter what challenges befall the economy. Unfortunately, just like the bursting of the tech bubble and the onset of the financial crisis, the next recession will finally come. And when it does, it has the potential to be absolutely ruthless for investors.

Let's Get This Out Of The Way

I can already hear the bulls sharpening their knives for the comment section of this article, and I very much look forward to reading and responding to all points of view including those that strongly disagree with my article, but let me get out in front with a few observations.

Indeed, I have been bearish for some time, but this does not mean that I'm predicting that everything is going to go up in smoke tomorrow. Just as the tech bubble went about four years longer than it probably should have, the same could definitely be said for today's market.

Moreover, we could see the S&P 500 Index (NYSEARCA:SPY) continue to rally for the next several months or couple of years. Then again, we could already be one year into a new bear market. Only time will tell. But what's important to note is that the higher and longer today's market continues to rise, the longer and harder it is likely to fall on the backside. In the meantime and until we start to definitely roll down the other side of the mountain, I have and will continue to hold a meaningful allocation to stocks.

But isn't my holding stocks a contradiction to my bearish view? Absolutely not. For just as being bullish does not mean that one should be all in and 100% allocated to equities, being bearish does not imply that one should be completely out of stocks and hide away in a bunker waiting for the world to end. Bear markets slowly evolve over long-term periods of time, and selected segments of the stock market have historically demonstrated the ability to perform well during different stages of bear market cycles. For example, consumer staples (NYSEARCA:XLP), utilities (NYSEARCA:XLU) and healthcare (NYSEARCA:XLV) stocks all typically perform well during the early stages of a bear market, and selected specific stocks of various styles and sizes such as Wal-Mart (NYSE:WMT), Village Super Market (NASDAQ:VLGEA), Community Bank System (NYSE:CBU) and Southern Company (NYSE:SO) have demonstrated the ability to perform well throughout the entirety of two of the worst bear markets in history in the bursting of the tech bubble and the financial crisis. So while I may not be loaded up on the SPY, the market offers a solid menu of stocks that one can hold through the worst of a market storm. I also own a lot of other things outside of stocks that are performing well today and I expect will perform even better during any future bear market in stocks.

Also, isn't my making a statement that the next bear market could be "absolutely ruthless" for investors nothing more than fear mongering? No, it is not. Instead, it is trying to increase investor awareness of a view that they may not otherwise be hearing. After all, one only has to tune into one of the major financial news networks to hear a cornucopia of bullish views on the market, many from analysts that have a direct vested interest in promoting such bullish views and reassuring the audience that despite any short-term rough patch that "stocks will be trading higher by the end of the year."

Conversely, those expressing a bearish view are often met with heavy pushback and scowling derision. As a result, this leaves many that may be less experienced with investment markets exposed to the risk of wondering "why didn't I see this coming" when they eventually find themselves locked in the jaws of the next bear market.

In the end, it is up to individual investors to decide how they wish to proceed with their own portfolio allocation. But by sharing this more bearish perspective on today's markets - it at a minimum provides investors with a viewpoint to consider that they may not be hearing elsewhere.

Now that we've got that out of the way, let's get down to it.

The Economic/Market Disconnect

The next bear market is setting up to be ruthless for investors. But this does not mean that it will be ruthless for the U.S. economy. In fact, it would not be surprising at all to see a prolonged and significant decline in stocks accompanied by what amounts to a somewhat longer than normal but otherwise relatively mild economic recession. How can this be the case? Simple.

Since Main Street (NYSE:MAIN) hardly participated in the glorious ascent that has been Wall Street via the stock market over the past seven plus years, Main Street is not likely to suffer nearly as much when stock prices come falling back to earth. In fact, many parts of Main Street might actually find themselves benefiting in many ways including even lower interest rates on loans, lower gasoline prices at the pump and the execution of more effective fiscal programs by policymakers that finally have had a long overdue fire lit under them.

Impossible, you might say. How can we have a major stock market decline with a relatively milder impact on the broader economy? One has to look no further than the bursting of the technology bubble from 2000 to 2002. During this time period, stocks declined by more than -50%, but the economy hardly even declined. Although we officially had a recession from March 2001 to November 2001 according to the National Bureau of Economic Research (NBER), the overall decline in U.S. real GDP was -0.3% and we didn't even have two consecutive quarters of negative growth during this stretch. This recent example highlights the fact that it is certainly possible to have a stock market more than cut in half without any measurable contraction in economic activity. For if stock valuations get too far ahead of the economy, as they were then and are arguably today, they then have a huge air pocket through which to descend by simply falling back to the underlying economic reality.

What About Not Fighting The Fed? Lest We Forget - Lest We Forget!

What about fighting the Fed? Haven't we learned by now during the post-crisis period that the U.S. Federal Reserve and their global central bank counterparts are going to do whatever it takes to protect stock prices at every turn? This has been definitely true in recent times as any attempts to try and short the market over the past seven years when it looked like stocks were going to break sharply to the downside have been absolutely steamrolled along the way. But in order to avoid falling victim to recency bias, just because this has been true in recent years does not mean that it is universally true.

In fact, the history of the Fed is filled with examples of them winning so many of the battles but ultimately losing the wars.

To set the stage for this point, let's go back to the last great Fed victory, which was winning the war over inflation back in the early 1980s. How did the Fed win this war? Because it was willing to endure the hardship, lose the battles, and suffer the sacrifice to prevail with overall victory in the end.

Then Fed Chair Paul Volcker did not coddle and cajole the economy and financial markets at the time in working to solve the problem. Instead, he dialed up interest rates to nearly 20% and ripped the heart out of the inflation problem. During this time, the economy endured two back-to-back recessions and a solid bear market, but it set the stage for the years of prosperity that followed in the 1980s and 1990s. In short, the Fed was willing to lose some battles to win the war. And until former Fed Board Governor Kevin Warsh is appointed to the position, Mr. Volcker will remain my favorite all-time Fed Chair.

So what have we seen since? Under Fed Chair Alan Greenspan, we saw the Fed win battle after battle. This included the stock market crash of 1987, the recession of 1990, the should-have-been recession of 1994, the Asian Flu in the late 1990s, and the collapse of Long-Term Capital Management in 1998. And the Fed did so by helping investors avoid any pain along the way.

Yet, in the end, they lost the war, as the tech bubble finally burst with roughly four years of investor gains during the late 1990s evaporating in the process.

About that Fed put. While it is easy to forget, particularly when it has lifted markets for so many years, but the Fed does not always get what it wants from stocks with accommodative monetary policy. Lest we forget! During the bursting of the tech bubble, the Fed was aggressively lowering interest rates for three years starting in early 2000, yet stock prices lost more than half of their value before finally bottoming in late 2002 and early 2003.

But then came the post-tech bubble period. Under Fed Chairs Alan Greenspan and Ben Bernanke, the Fed once again was winning all of the wars thanks to low interest rates and a booming housing market. And once again, investors were able to bask in the warmth of an accommodating market filled with gains and free of pain. In the process, they managed to bring the stock market all the way back to its tech bubble highs. But in the end, the Fed once again lost the war, as the housing bubble burst with nearly catastrophic consequences. By the time the financial crisis was brought under control in March 2009 (not fixed, but brought under control), the market had exceeded the losses of the tech bubble to the downside and was back to the same level it had first reached more than a decade earlier.

Once again, the Fed put does not always work. Lest we forget! During the financial crisis, the Fed was once again aggressively lowering interest rates for nearly two years starting in mid-2007, eventually lowering interest rates to zero and launching into quantitative easing along the way, yet stock prices once again lost more than half of their value before finally bottoming in early 2009.

All of this leads us to today. Under Fed Chair Ben Bernanke, the Fed has won all of the battles by giving investors everything they could ever imagine and more. Stocks have skyrocketed virtually without interruption and investor pain has been virtually non-existent. In the process, the Fed managed to catapult the stock market more than one-third higher above its tech bubble and pre-financial crisis peaks. And they did so with a global economy that has been sluggish, uneven and lackluster at best.

Why The Next Recession Will Be Ruthless For Stocks

Maybe the outcome this time around will be different. But given the historical pattern over the past two decades, my bet remains that the Fed will end up losing this war once again.

Why? Let's begin with the qualitative, which is that war is not won by bypassing the pain and sacrifice necessary to prevail. And until policymakers finally decide that they are ready to win the war and replace the monetary cotton candy with a steady diet of spinach, we are likely to continue in these monetary induced boom and bust cycles.

Now let's get to the quantitative. What enabled the Fed to rescue the stock market after the last two lost wars? Because they entered financial markets firing all monetary guns for an extended period of time lasting two to three years in order to get the markets stabilized and moving higher again. But let's assume whatever bubble of the many that exist today finally bursts and sends stocks sustainably lower despite all of the best efforts and jawboning by the U.S. Federal Reserve and their global cohorts. From exactly what arsenal are they going to fire from to turn the stock market around so quickly this next time around?

Will it be lowering interest rates by several percentage points? No, because interest rates are already effectively still at zero in the U.S. and negative in much of the developed world outside of the U.S. And the temptation to go further into negative interest rate territory is unlikely, for not only has it not lifted stock price in any measurable way, evidence is growing by the day that it simply does not work and is causing more harm than good.

Will it be launching into yet another round of aggressive quantitative easing? Perhaps, but what is the justification for putting our global fiat currency system that is still a baby at only less than half of a century old at even greater peril than it already is for returning to a program that simply has not worked in generating sustained economic growth over the past seven years?

With that said, I still wouldn't put it past the Fed to go back to this well, but it stands to question what the marginal benefit to stock prices would be at the end of the day. Lest we forget the experience that Japan (NYSEARCA:EWJ) had with quantitative easing from March 2001 to March 2006 when the Bank of Japan increased its balance sheet by more than seven-fold, with the lion share of the increases taking place during the first three years of the program.

Yet during the first several years of the program, stock prices were cut in half before finally finding their footing. And they didn't begin bursting to the upside until more than four years after the launch of the program, and this was thanks in part to a global tailwind where the rest of the global economy was already well into its post tech bubble recovery at that point.

If and when stocks began falling in earnest the next time around, be it because of the onset of the next recession or the bursting of a bubble in capital markets, it is very likely that global central banks will lack sufficient monetary firepower and policy flexibility to stem the decline lower in stocks. In short, markets may finally be allowed to wash themselves out and cleanse themselves despite what monetary policymakers wish to allow. It's the return of Volcker-style monetary policy whether global central banks want it or not.

It should be noted that such a decline is likely to cut deeper and last longer than the two major bear markets that preceded it since the start of the new millennium. It will likely lead to a larger overall decline in the end due to the fact that central bankers will lack the resources to reverse the overall market decline the next time around. And it will likely last longer because central bankers are likely to try and fight the decline in global stock markets at every turn, as there will almost certainly be no Lehman Brothers style bandage ripping off next time around.

The good news is that it will provide investors with several opportunities to evacuate the market before the lights fully go out. One could even argue that the market is providing investors with such opportunities as we speak today.

Moreover, such a longer, more gradual bear market would provide abundant short-term trading opportunities for the nimbler investors among us. The bad news is that the next bear market is likely to feel as agonizingly long as the bull market has seemed endless today.

The Silver Lining

Such an outcome would certainly be difficult to endure and is unfortunately likely to leave a good number of investors smarting from the inevitable loss in portfolio value sustained by many along the way. But the silver lining to such an outcome is an American-style happy ending.

We don't reflect back with regret on the challenges that we had to endure during the late 1970s and early 1980s when the inflation rate was pushing toward 15% and the Fed had to crank up its restrictive monetary policy deals to fix the economy. Instead, many reflect on that time with tales of courage like how they had to walk into a bank and get a mortgage with sky-high interest rates in order to provide their family with a place to live after relocating to a new city.

And almost nobody regrets the years of sustained economic prosperity that followed during the 1980s and 1990s, and that includes struggling through the markets at the time that inspired the now much ridiculed "Death of Equities" magazine cover that came along the way. In short, suffering through this inevitable market pain ahead will bring us to the dawn of the next great phase of sustained economic growth in the United States and around the world.

Just as importantly, the fact that stocks are set up for a fall due in part to monetary policymakers being just about out of firepower will likely finally induce frustratingly complacent and bungling political leaders to get off their collective duffs and finally start working together in enacting effective fiscal policy to fix the chronic problems that have existed around the globe for far too long.

The general voting population around the world are really angry, and for good reason. It is because their political systems and leaders from the major established parties have failed them badly. This is a big part of the reason why we have seen the rise of outsider candidates such as Donald Trump and Bernie Sanders here in the United States and scores of outsider candidates in countries around the developed and emerging world rise to the forefront of political influence. It is also part of the reason why a candidate like Gary Johnson that effectively finished tenth out of nine candidates in the 2012 Republican primaries and could not even consistently make the debate stage that year has recently been registering in the double-digits in the general election polls as the Libertarian candidate for president in 2016. It's because the masses want big time change to happen that includes much more effective fiscal policy and they are willing to go to whatever lengths necessary to endure whatever pain required and to elect whatever candidate is needed to make it happen. And if the markets go through such a corrective cycle in the coming years, the people are likely to get this outcome regardless of who takes office both in the U.S. and in countries around the world.

The Bottom Line

Whether it starts tomorrow, next month, three years now, or already started more than a year ago, the next bear market is likely to be ruthless both in depth and duration. And the higher stocks continue to climb today, the more ruthless the next bear market is likely to be in the end.

Investors can ignore the likelihood for such an outcome, but they do so at their own peril.

Instead, investors can be well served by embracing or at least recognizing such a potential outcome and preparing their portfolio accordingly. This does not mean moving to cash right now, running for the hills and stockpiling your emergency food rations. Instead, it means crafting a game plan that includes stocks as well as components from various other asset classes that are not stocks so that you are ready to capitalize on the various ebbs and flows of the market as it travels through such an extended corrective process. After all, some of the greatest and most legendary investment gains have been made during extended bear markets, and the next time around is likely to be no exception in this regard. For those who are interested, this is an area among others that we explore in much great detail on my premium service The Universal.

Perhaps the most positive outcome of all is the following. By enduring such a cleansing process in the global economy and financial markets, as painful as it might be along the way, it will finally bring us all to that 1921, 1946, and 1982 moment where we stand at the dawn to watch the sunrise on the next great sustained global economic expansion. Nobody said the journey through the 1910s into the early 1920s, the 1930s into the 1940s, and the 1970s into the early 1980s was easy, but they were required to bring us to the periods of great prosperity that followed.

The good news is that we have already endured the challenges of the 2000s and the early 2010s.

Now we just need to finish it off with one final cleansing phase, if only monetary policymakers would finally get out of the way and fiscal policymakers would finally get on with it. Perhaps we will find out sooner rather than later one way or another.

0 comments:

Publicar un comentario