Gavyn Davies

The influence of the global economy on the decisions of the US Federal Reserve has become a topic of frontline importance in recent months.

Since the start of 2016, events in foreign economies have conspired to delay the FOMC’s intended “normalisation” of domestic interest rates, which had apparently been set on a firmly determined path last December.

This delay has taken the heat out of the dollar. But the key question now is whether weak foreign activity will continue to trump domestic strength in the US.

To judge from last week’s surprisingly hawkish FOMC minutes, which I had not expected, the Fed seems to be reverting to type (see Tim Duy). Many committee members have downplayed foreign risks and have returned to their earlier focus on the strength of the domestic US labour market, which in their view is already at full employment.

The Fed is a conservative institution, greatly influenced by its own history. It has always objected to being portrayed as “the world’s central banker”. The dual mandate set by Congress in 1977 for US monetary policy refers to domestic inflation and employment, which fuels suspicions that the Fed ignores other economies altogether.

The US central bank certainly has no responsibility to take direct account of the welfare of foreigners.

But it (reluctantly) takes note of spillovers in the other direction. The impact of events overseas on the dollar and the domestic US economy are too important to be entirely ignored.

Early history under the gold standard

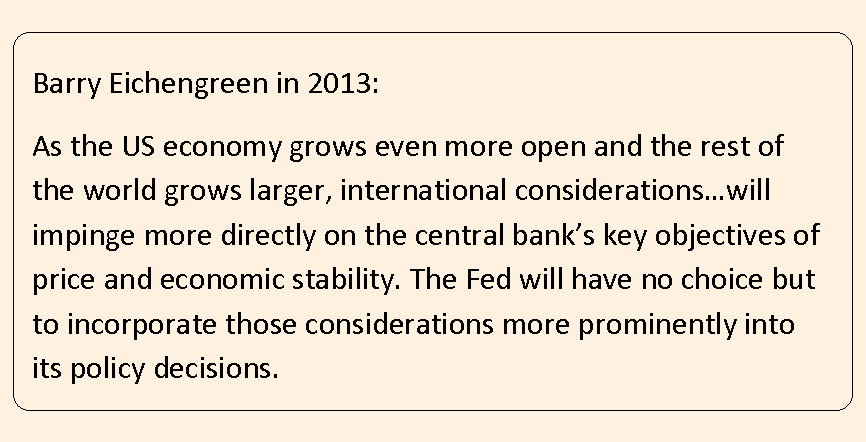

The weight given to foreign influences has waxed and waned through the decades. The redoubtable Barry Eichengreen objects to the prevailing view, which is that the Fed has always been cut off from the global economy. He points out that the foundation of the Fed in 1913 was in part due to a desire to establish a dollar market in trade credits, thus ending the global monopoly of the sterling acceptance market in the financing of international trade.

In the 1920s, the Fed was determined to re-establish the international Gold Standard, which had broken apart during the First World War. Lower domestic interest rates in the US were deemed essential for this objective, because this encouraged gold flows into the UK, helping Britain to resume its role as the centrepiece of the Gold Standard in 1925.

When excessively easy domestic monetary policy caused the boom and bust in US equities in 1929, the dollar’s membership of the Gold Standard assumed the opposite role, preventing the Fed from easing domestic monetary conditions sufficiently to combat the Great Depression from 1931-33.

The decades of isolation

After these debacles, foreign objectives were only rarely in centre stage. In the early 1960s, the FOMC became sufficiently concerned about the US balance of payments to raise domestic interest rates, and in the late 1990s it was forced to reduce rates by the Asian economic crisis.

Nonetheless, after Paul Volcker’s programme of disinflation in the early 1980s, the Fed focused primarily on its own back yard. Eichengreen says that the Fed “could afford to act to a first approximation like the central bank of a closed economy”.

Later, under Alan Greenspan and Ben Bernanke, the doctrine was that each country should look after its own affairs, since that was the best way of maximising the common good. The case for international co-operation fell completely out of favour.

In fact, I have been told by senior central bankers that Mr Bernanke was sometimes a rather bored bystander at major international conferences, perking up only when asked to give his views about the US economy.

Since the crisis in 2008

This changed for only a short while in the 2008 financial crisis, when Mr Bernanke’s Fed crucially provided dollar swap lines with other major central banks in order to prevent the world from running short of dollar liquidity. After the crisis subsided, the Fed returned to its domestic focus, even when many emerging markets complained about the capital inflows into their economies during the Fed’s quantitative easing from 2010-13. They were told, rather bluntly, to take responsibility for their own affairs.

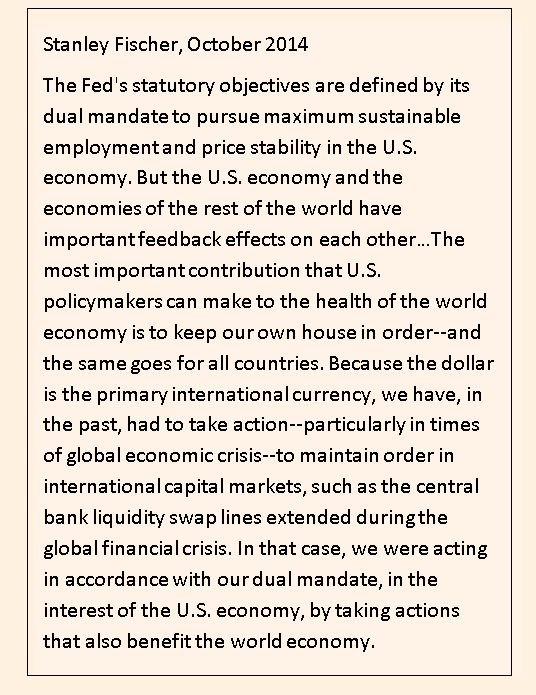

Surprisingly, this isolationist approach was still apparent in a landmark speech by Stanley Fischer in October, 2014. Generally regarded as the most internationally aware member of the Fed Board, Fischer argued strongly that there were indeed global spillovers that the FOMC needed to consider, but nevertheless concluded that the Fed should basically focus on its own domestic objectives.

There was little recognition – even after the taper tantrum of 2013 – that the Fed could trigger such a convulsion overseas that it would be dislodged from its own domestic objectives. Instead, Fischer argued that the FOMC’s main responsibility was to ensure that it spelled out its intentions clearly in advance, thus avoiding disruptive policy shocks.

Theory vs practice

As Jim Bullard has recently pointed out, this scepticism about the gains from cooperation between the major central banks was strongly supported by the established international macro-economic theory at the time. Recently, however, the consensus has been changing.

Bullard himself wrote an important paper with Aarti Singh in 2008, showing that there could be gains from co-operation if any of the major central banks were departing from “optimal” monetary policy, as defined by a standard Taylor Rule. He speculates that this could now be the case, because both the Bank of Japan and the ECB have hit the zero lower bound on interest rates, and cannot therefore follow optimal monetary policy. This causes instability in the global economy, which the Fed cannot eliminate by focusing only on its domestic objectives.

Similar results have been reported in other recent papers [1]. But it seems that the FOMC is still not convinced.

Most members of the FOMC have accepted that foreign influences have reduced the equilibrium real rate of interest in the world as a whole, and probably also in the US. But several important FOMC members argue that the current level of US rates is still far below equilibrium, and they conclude that there should be further gradual steps to close the gap, starting fairly soon.

These members argue that foreign influences should not be used (as they were in the late 1920s) as a reason to delay the rate increases needed to control domestic inflation and prevent asset price bubbles.

Next steps

Until now, the markets have strongly believed that foreign weakness would severely temper the Fed’s reaction to the tightening in the US labour market. Janet Yellen and William Dudley certainly adopted a dovish line on these issues when the global market convulsions happened in February, but other influential voices (including Stanley Fischer and John Williams) have fought back hard.

A hike at the June FOMC meeting still seems somewhat improbable, but July is certainly in play. We will hear more about this in a decisive speech from Janet Yellen on 6 June.

Since the start of 2016, events in foreign economies have conspired to delay the FOMC’s intended “normalisation” of domestic interest rates, which had apparently been set on a firmly determined path last December.

This delay has taken the heat out of the dollar. But the key question now is whether weak foreign activity will continue to trump domestic strength in the US.

To judge from last week’s surprisingly hawkish FOMC minutes, which I had not expected, the Fed seems to be reverting to type (see Tim Duy). Many committee members have downplayed foreign risks and have returned to their earlier focus on the strength of the domestic US labour market, which in their view is already at full employment.

The Fed is a conservative institution, greatly influenced by its own history. It has always objected to being portrayed as “the world’s central banker”. The dual mandate set by Congress in 1977 for US monetary policy refers to domestic inflation and employment, which fuels suspicions that the Fed ignores other economies altogether.

The US central bank certainly has no responsibility to take direct account of the welfare of foreigners.

But it (reluctantly) takes note of spillovers in the other direction. The impact of events overseas on the dollar and the domestic US economy are too important to be entirely ignored.

Early history under the gold standard

The weight given to foreign influences has waxed and waned through the decades. The redoubtable Barry Eichengreen objects to the prevailing view, which is that the Fed has always been cut off from the global economy. He points out that the foundation of the Fed in 1913 was in part due to a desire to establish a dollar market in trade credits, thus ending the global monopoly of the sterling acceptance market in the financing of international trade.

In the 1920s, the Fed was determined to re-establish the international Gold Standard, which had broken apart during the First World War. Lower domestic interest rates in the US were deemed essential for this objective, because this encouraged gold flows into the UK, helping Britain to resume its role as the centrepiece of the Gold Standard in 1925.

When excessively easy domestic monetary policy caused the boom and bust in US equities in 1929, the dollar’s membership of the Gold Standard assumed the opposite role, preventing the Fed from easing domestic monetary conditions sufficiently to combat the Great Depression from 1931-33.

The decades of isolation

After these debacles, foreign objectives were only rarely in centre stage. In the early 1960s, the FOMC became sufficiently concerned about the US balance of payments to raise domestic interest rates, and in the late 1990s it was forced to reduce rates by the Asian economic crisis.

Nonetheless, after Paul Volcker’s programme of disinflation in the early 1980s, the Fed focused primarily on its own back yard. Eichengreen says that the Fed “could afford to act to a first approximation like the central bank of a closed economy”.

Later, under Alan Greenspan and Ben Bernanke, the doctrine was that each country should look after its own affairs, since that was the best way of maximising the common good. The case for international co-operation fell completely out of favour.

In fact, I have been told by senior central bankers that Mr Bernanke was sometimes a rather bored bystander at major international conferences, perking up only when asked to give his views about the US economy.

Since the crisis in 2008

This changed for only a short while in the 2008 financial crisis, when Mr Bernanke’s Fed crucially provided dollar swap lines with other major central banks in order to prevent the world from running short of dollar liquidity. After the crisis subsided, the Fed returned to its domestic focus, even when many emerging markets complained about the capital inflows into their economies during the Fed’s quantitative easing from 2010-13. They were told, rather bluntly, to take responsibility for their own affairs.

Surprisingly, this isolationist approach was still apparent in a landmark speech by Stanley Fischer in October, 2014. Generally regarded as the most internationally aware member of the Fed Board, Fischer argued strongly that there were indeed global spillovers that the FOMC needed to consider, but nevertheless concluded that the Fed should basically focus on its own domestic objectives.

There was little recognition – even after the taper tantrum of 2013 – that the Fed could trigger such a convulsion overseas that it would be dislodged from its own domestic objectives. Instead, Fischer argued that the FOMC’s main responsibility was to ensure that it spelled out its intentions clearly in advance, thus avoiding disruptive policy shocks.

Theory vs practice

As Jim Bullard has recently pointed out, this scepticism about the gains from cooperation between the major central banks was strongly supported by the established international macro-economic theory at the time. Recently, however, the consensus has been changing.

Bullard himself wrote an important paper with Aarti Singh in 2008, showing that there could be gains from co-operation if any of the major central banks were departing from “optimal” monetary policy, as defined by a standard Taylor Rule. He speculates that this could now be the case, because both the Bank of Japan and the ECB have hit the zero lower bound on interest rates, and cannot therefore follow optimal monetary policy. This causes instability in the global economy, which the Fed cannot eliminate by focusing only on its domestic objectives.

Similar results have been reported in other recent papers [1]. But it seems that the FOMC is still not convinced.

Most members of the FOMC have accepted that foreign influences have reduced the equilibrium real rate of interest in the world as a whole, and probably also in the US. But several important FOMC members argue that the current level of US rates is still far below equilibrium, and they conclude that there should be further gradual steps to close the gap, starting fairly soon.

These members argue that foreign influences should not be used (as they were in the late 1920s) as a reason to delay the rate increases needed to control domestic inflation and prevent asset price bubbles.

Next steps

Until now, the markets have strongly believed that foreign weakness would severely temper the Fed’s reaction to the tightening in the US labour market. Janet Yellen and William Dudley certainly adopted a dovish line on these issues when the global market convulsions happened in February, but other influential voices (including Stanley Fischer and John Williams) have fought back hard.

A hike at the June FOMC meeting still seems somewhat improbable, but July is certainly in play. We will hear more about this in a decisive speech from Janet Yellen on 6 June.

0 comments:

Publicar un comentario