Some boutique bank stocks are positioned better than others for a downturn in M&A, so investors should take note

By Aaron Back

.

On Wall Street, bankers know that merger booms come and go. Investors need to be aware of the risks when the music stops.

When activity dies down, a handful of boutique investment banks that specialize in M&A will be most exposed. But even among these firms, there are big differences that will matter.

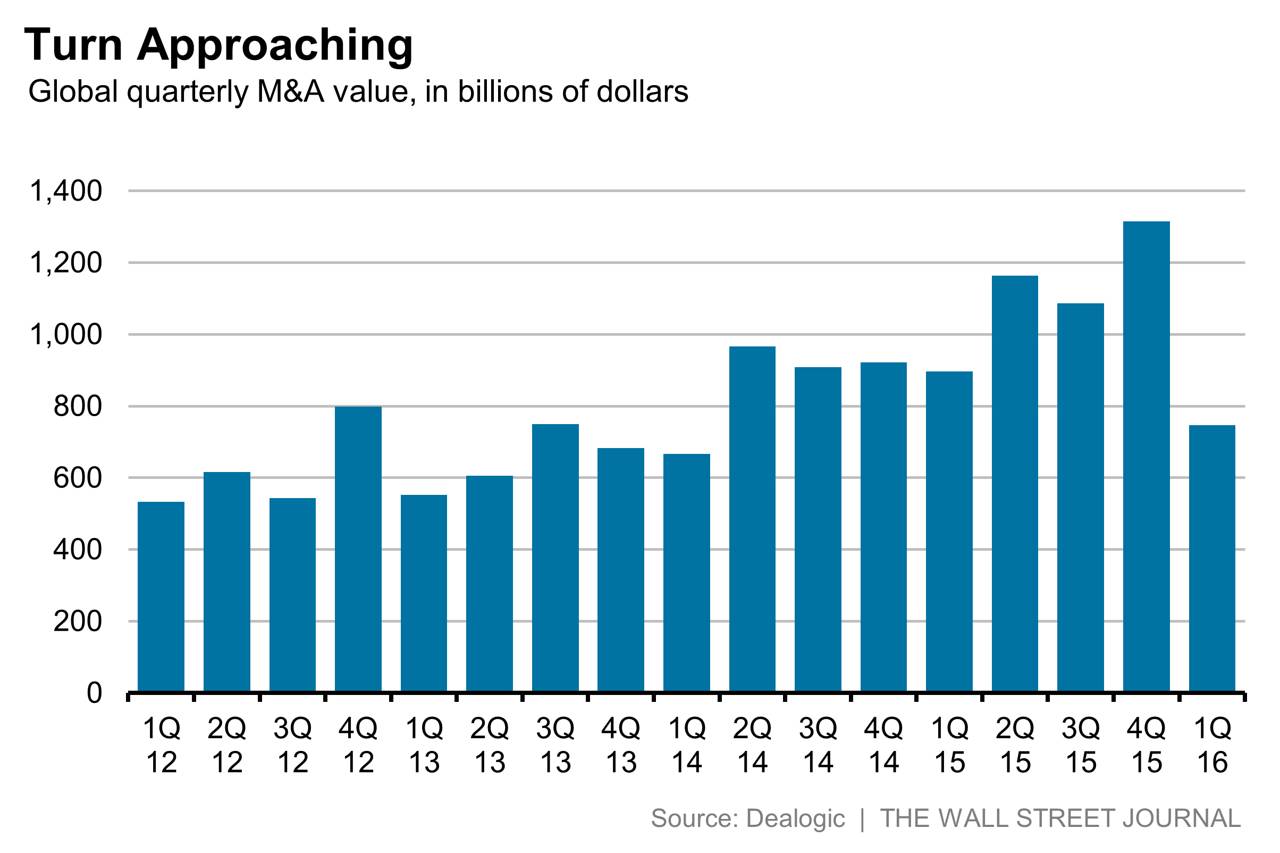

In the first quarter, total global M&A deal value fell 17% from a year earlier, according to Dealogic. The question is whether this was a blip or the start of a downtrend. Early signs aren’t encouraging. So far in the second quarter, M&A value is down 19% from a year earlier, notes Dealogic.

Publicly at least, bankers continue to insist there is a strong pipeline of deals. But the cycle will turn eventually, and investors are starting to prepare. Over the past six months, five listed boutiques— Lazard, Evercore Partners, Greenhill, Moelis and Houlihan Lokey —are down an average 12%.

In the three months to March, Houlihan’s restructuring revenue rose 10% from a year earlier, accounting for 39% of total revenue.

Weakness in the oil, metals and mining industries accounts for the rise, and it should continue.

Debt restructurings can take a long time to complete, meaning revenue for the bankers tends to lag behind by several months or even years, the company said on a conference call with analysts. This helps explain why Houlihan is the only one in the group whose stock has risen, by about 3% over the past six months.

For the rest, though, there is reason to expect more pain. High dividend yields are one prop, but payouts may not be sustainable. Greenhill, for one, has a 9.4% yield. But its regular quarterly payouts are consuming most of the company’s cash flow, notes UBS analyst Brennan Hawken.

So the dividend is in danger of being cut should deal flow dry up.

Bankers who make fat bonuses when the sun shines can ride out weaker periods. Investors in their firms’ shares aren’t always so lucky.

0 comments:

Publicar un comentario