Fed Running Out Of Excuses On Interest Rates

by: Chris Ciovacco

Summary

The "data dependent" Fed is going to have to deal with new economic data.

How do things look relative to the Fed's stated targets on unemployment and inflation?

Can the Fed wait indefinitely on rates?

Fed Has A Difficult Job

How do things look relative to the Fed's stated targets on unemployment and inflation?

Can the Fed wait indefinitely on rates?

Fed Has A Difficult Job

In terms of government policy, the economy has two primary types of stimulus, fiscal and monetary. The Fed controls monetary policy. Congress is the primary driver of fiscal policy.

In recent years, Congress has left all the heavy lifting to the Fed. Having stated the Fed is in a difficult position, their focus in recent years appears to have shifted almost solely to keeping asset prices (NYSEARCA:VOO) propped up, a concept that has not gone unnoticed by the financial markets (NYSEARCA:VTI).

2012 Plan Was To Raise Rates When Unemployment Hit 6.5%

In December 2012, the Federal Reserve provided a 6.5% unemployment target with respect to allowing rates to remain near zero. From USA Today:

The Federal Reserve on Wednesday agreed to keep a key short-term rate near zero until the 7.7% unemployment rate is 6.5% or lower.

Goalpost Taken Down In 2014

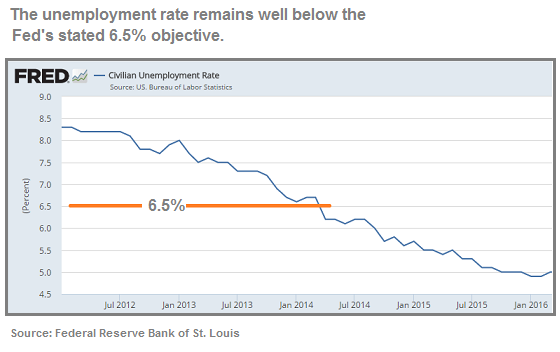

The chart below shows the unemployment rate between 2012 and 2016. As you can see, unemployment has been below the Fed's 6.5% target for some time.

Since it would be a constant source of "why are you still waiting to raise rates" questions, the Fed decided in April 2014 to remove the unemployment goalpost. From CNBC:

The members of the Federal Open Market Committee agreed unanimously in March that a 6.5 percent unemployment target for raising interest rates was "outdated" and should be removed, according to meeting minutes.

The Fed Originally Choose An "Outdated" Target

Rather than face the difficult decision to begin raising interest rates, the Fed kicked the can down the road after calling their own stated unemployment target "outdated", which begs the question if the target is outdated, then why did the Fed use it in the first place? Did the 6.5% target somehow become outdated between 2012 and 2014?

We Can Afford To Be Patient

In a move that surprised the markets, the Fed stated in March 2015 that it still needed to see more. From the Chicago Tribune:

The Federal Reserve signaled Wednesday that it needs to see further improvement in the job market and higher inflation before it raises interest rates from record lows.

In February 2016, Janet Yellen once again played the "we can be patient" card. From NewsMax:

Federal Reserve Chair Janet Yellen said Tuesday that the U.S. economy is making steady progress, but that for now the Fed is will remain patient about raising interest rates because the job market is still healing and inflation is too low.

Inflation Data Has Been Picking Up

Recent reports have shown inflation (NYSEARCA:TIP) is beginning to pick up. In fact, a report released on May 17 said wage growth was the highest in seven years. From Bloomberg:

The median U.S. worker is enjoying their highest wage growth since 2009, according to the Federal Reserve Bank of Atlanta's wage growth tracker. This metric showed that the median employee saw pay rise 3.4 percent year-over-year as of April, setting a new record for this expansion.

The markets (NYSEARCA:IEF) are starting to question the Fed's stated objectives on unemployment and inflation. From an April 7, 2016 CNBC article:

Inflation in the U.S. has picked up in recent months, toward the top end of Federal Reserve forecasts. While several Fed officials remain focused on building inflationary pressures, Fed Chair Janet Yellen has recently struck a dovish tone, stressing her concerns about global growth and financial conditions as reasons to proceed cautiously with interest-rate hikes.

Trading Volume Has Dropped By 70%

Can markets see the difference between the Fed's stated/mandated objectives and their actions?

If we look at trading volume for the SPDR S&P 500 Trust ETF (NYSEARCA:SPY), the answer seems to be a definitive yes. Three-month average daily volume for SPY for May-July 2010 was 283,000,000 shares. Average daily SPY volume for August-October 2011 was 322,000,000.

Current average daily volume for SPY going back three months is just 99,000,000, based on data from Yahoo Finance.

Investors Losing Interest In Centrally-Planned Markets

Trading volume helps us better understand investor interest in a particular market. Using SPY volume, investor interest in the stock market has dropped by almost 70% since 2011.

Obviously, there are countless factors impacting investor interest/trading volume, including fundamentals.

Valuations A Concern To Many

When we examine valuations, it is most likely a combination of markets that seemingly get talked up by the Fed every time they begin to fall and extended valuations that have resulted in a sharp decline in investor interest at current S&P 500 levels. According to FactSet, the forward P/E ratio for the S&P 500 is higher today than at the 2007 Financial Crisis peak in the stock market.

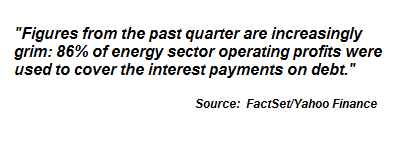

Low Rates Mean More Debt

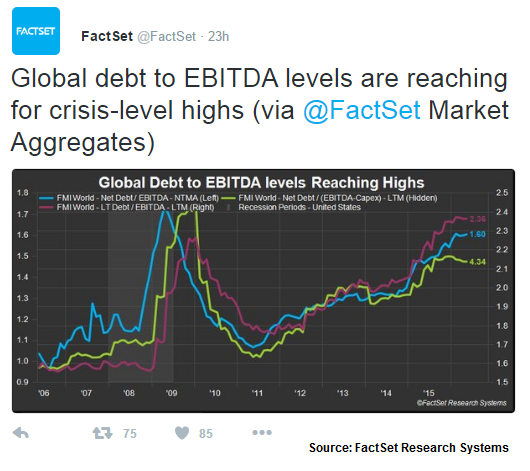

The Fed's seemingly never-ending period of near-zero interest rates has also led to an alarming amount of debt relative to earnings. The tweet below is from FactSet (EBITDA stands for earnings before interest, tax, depreciation and amortization).

Rates Are Too Low

It is not just Fed critics that are waving yellow flags about keeping rates near zero for an extended period. In a recent speech, a voting member of the Fed's Open Market Committee outlined numerous concerns tied to low rates. From MarketWatch:

Interest rates are too low for today's economic conditions, creating risks for the outlook, said Kansas City Fed President Esther George on Thursday."Because monetary policy has a powerful effect on financial conditions, it can give rise to imbalances or capital misallocation that negatively affects longer-run growth," George said in a speech to business leaders in Albuquerque, New Mexico. Low rates can cause interest-sensitive sectors to take on too much debt and grow quickly, only to unwind in ways that are disruptive, George said, citing the housing crisis and the "current adjustment in the energy sector." George is a voting member of the Fed's policy committee. She has dissented at the last two policy meetings in favor of hiking rates.

Data Dependent?

The Fed has been telling the markets over and over again that the path of interest rates is "data dependent". The fact that the "data" has been improving relative to the Fed's own stated objectives and Janet Yellen continues to read from the dovish playbook has not gone unnoticed by seasoned market professionals. From CNBC:

Legendary billionaire investor Stanley Druckenmiller told Sohn Investment Conference attendees to sell their equity holdings Wednesday. The billionaire investor expressed skepticism about the current investment environment due to Federal Reserve's easy monetary policy and a slowing Chinese economy. "The Fed has borrowed from future consumption more than ever before. It is the least data dependent Fed in history. This is the longest deviation from historical norms in terms of Fed dovishness than I have ever seen in my career," Druckenmiller said. "This kind of myopia causes reckless behavior."

Global Central Banks In Radical Waters

A recent article outlined numerous "are they really doing that" policies being implemented by other central banks around the globe. As noted in a May 2016 video, the Fed's dual mandate, and more importantly basic economic principles, tell us central banks will try to inflate as long as they possibly can. When inflation starts to become a problem on the high end of the price stability spectrum, it will be much harder for central banks to keep things propped up.

Therefore, until the Fed starts to acknowledge inflation, investors must be open to:

- A continuation of extremely dovish and radical policies from global central banks (see article regarding possible expansion of stock purchases).

- The possibility of asset prices remaining artificially elevated, including the scenario of U.S. markets pushing to new all-time highs.

Interest Rate Policy Works With A Lag

Even the Fed has acknowledged in the past that it is dangerous to wait until inflation targets are hit before starting to lay the groundwork for keeping longer-term inflation in check. From the Fed's 2015 Jackson Hole keynote address by Stanley Fischer:

"Because monetary policy influences real activity with a substantial lag, we should not wait until inflation is back to 2% to begin tightening."

The latest read on inflation was a wage figure that represented the highest wage growth since 2009. Meanwhile, the Fed continues to wait.

0 comments:

Publicar un comentario