Deutsche Bank: Why 2016 Could Still Hold a Nasty Surprise

The German lender’s capital still looks thin, despite efforts to boost it

By Paul J. Davies

January and February witnessed a storm of fear and loathing around European banks and Deutsche Bank was most exposed.

In that light, it is surprising that the bank’s first quarter revenues weren’t worse than reported on Thursday, especially in its investment banking and markets business.

This was always going to be a lost year for Deutsche Bank investors as it pursues a floor-to-ceiling remodelling job. The good news is that the apparent crisis of internal morale that saw a collapse in markets revenues in the final quarter of 2015 at least looks to have abated. The bad news is that there could still be a sting in the tail from legal settlements.

The first quarter has been punishing for all investment banks. But, more than any other, Deutsche Bank also suffered a huge leap in its own perceived riskiness, as shown by the near tripling of the cost of protecting its debt against default.

That led clients and counterparties to question whether they should be doing business with the German lender, costing it work during the panic of mid-February.

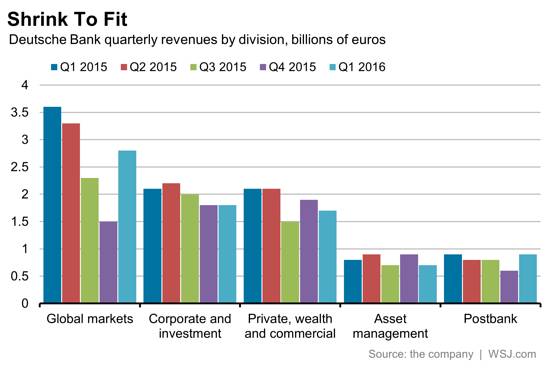

In this light, a fall in revenues in global markets of 23% to €2.77 billion ($3.14 billion) isn’t bad, especially as roughly one-quarter of that decline was business deliberately cut as part of the restructuring. When set against the woeful €1.46 billion revenues of the final quarter last year, it seems positively respectable.

But if that offers some comfort, the overall story is still one of weaker revenues, year-over-year, in all divisions, aside from a marginal improvement at Postbank. Profits were all but completely eaten away by restructuring and litigation charges, which is likely to be true for the rest of the year.

The headline says it all: A bank that made net revenues of more than €8 billion reported bottom line net income of just €200 million.

John Cryan, chief executive, repeated his guidance that the bank will probably make no money this year as it tries to get all its hard work—and the associated costs—through the business. He also said the bank expects to finish 2016 with a common equity capital ratio roughly the same as where it ended 2015, which was 11.1%.

Deutsche Bank lost some capital in the first quarter, but has also agreed the sale of its stake in Chinese lender Hua Xia, which will provide a boost. Taking account of planned balance sheet cuts, it actually looks on course to finish the year with a ratio of 11.7-11.8%. That suggests about €2.5 billion more in capital than it has today, implying substantial losses to come.

The big moving part in this equation is litigation, with settlements still due for U.S. mortgage issues and bad business practices in Russia, for which there is no other benchmark case.

Deutsche Bank’s capital still looks thin. Until it has solid numbers on these settlements there is no way to tell whether it will get through without raising more.

0 comments:

Publicar un comentario