Buttonwood

A chronic problem

Ideas for reducing the debt burden

.

DEBT levels grew spectacularly in the rich world from 1982 to 2007. When the financial crisis broke, worries about the ability of borrowers to repay or refinance that debt caused the biggest economic downturn since the 1930s.

It could have been worse. The danger was that, as private-sector borrowers scrambled to reduce their debts, the resulting contraction in credit would drive the world into depression.

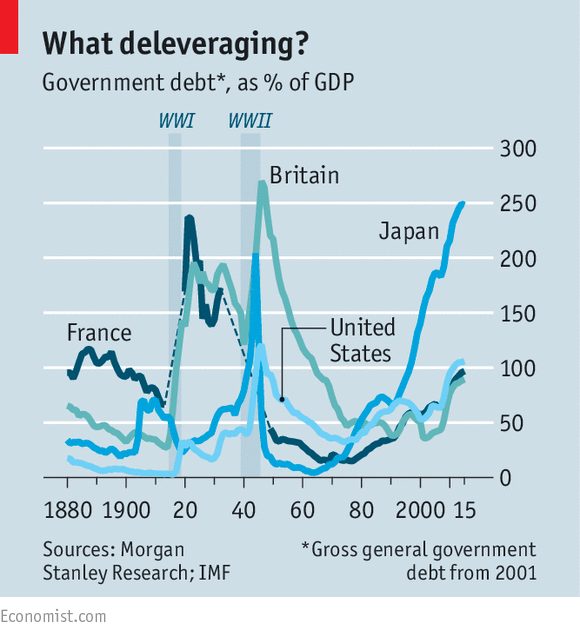

Fortunately, this outcome was averted. First, the governments of rich countries allowed their debts to rise, offsetting the reduction in private debt. In addition, emerging markets (notably China) continued to borrow. So there was no global deleveraging; quite the reverse (see chart).

Central banks also helped, slashing interest rates to zero and below. Although lower policy rates have not always resulted in cheaper borrowing costs (in Greece, for example), debt-servicing costs have fallen in most developed countries.

Although this approach has staved off disaster, it has not got rid of the problem, as a research note from Manoj Pradhan, an economist at Morgan Stanley, makes clear. “High debt forces interest rates to stay low, which encourages yet more debt,” Mr Pradhan writes. Central banks dare not push interest rates up too quickly for fear of causing another crisis; hence the stop-start nature of the Federal Reserve’s statements on monetary policy. The developed world seems stuck with sluggish growth and low rates.

In health terms, the disease is chronic, not acute. A lurch into another global crisis, Mr Pradhan reckons, would require three ingredients. First, the assets financed by the debt build-up would need to fall sharply in price or prove uneconomic. Second, the debtors would have to be concentrated in big, globalised economies. Lastly, global investors would have to be heavily exposed to the debt in question. All this was the case in 2007-08, as debt secured by American housing turned bad, raising doubts about the health of the Western banking system.

This time round the debtors are in different places. Some of them are emerging-market governments and commodity producers. But, except for China, none of these is crucial to the world economy. And China’s debts are mainly in domestic hands, rather than widely dispersed in the portfolios of international banks, pension funds and insurance companies.

Large, rich countries are systemically important, and their government debt is at the heart of most institutional portfolios. If a President Trump were to follow through on his confusing statements about buying back Treasury bonds for less than face value, that would trigger a crisis. In the absence of such a cataclysm, and with the support of central banks, governments that have borrowed in their own currency should not face an imminent problem.

But that doesn’t mean getting rid of the debt will be easy. Debt has been inflated away in the past, but central banks are still struggling to meet their current inflation targets of 2% or so. It is not clear that governments, which set the mandates central banks must follow, would be willing to put up with the high rates of inflation needed to reduce the real value of debt substantially, even if central banks could find a way of generating it. Debt forgiveness (the old idea of a jubilee) sounds good in theory.

But writing off either private-sector or government debt could cripple the financial sector, creating the very crisis the measure was designed to avoid.

Morgan Stanley has some alternative suggestions. One would be to replace debt with equity-like capital. In the public sector, governments could issue GDP-linked bonds, akin to the inflation-linked debt that America, Britain and others already offer. If a bond’s repayment value is linked to real GDP, then governments would be spared the crippling surge in debt-to-GDP ratios that occurs during recessions. Governments could also issue irredeemable debt, or “consols”, which eliminate the risk of a refinancing crisis.

In the private sector, equalising the tax treatment of equity and debt would be a good idea, although tricky to implement. Creating “shared-responsibility mortgages”, in which lenders take an equity stake in the homes they finance, would make borrowers less vulnerable to house-price declines.

All these ideas seem sensible, but they can be applied only to newly issued debt, not to the mass of obligations that has already been accrued. So they will help only over the long term. The next global debt crisis will almost certainly occur before they become widespread.

0 comments:

Publicar un comentario