Too Big to Fail? So What, Say Bank Depositors

The biggest U.S. banks continued to gain deposits in the first quarter

By Aaron Back

Plenty of people say they don’t like too-big-to-fail banks. Yet plenty of people are still happy to give those same banks their money—even when it earns them next to nothing.

While big banks suffered during the tumultuous first quarter, deposits continued to roll in the door. That was one of several silver linings in what was an otherwise dispiriting first quarter.

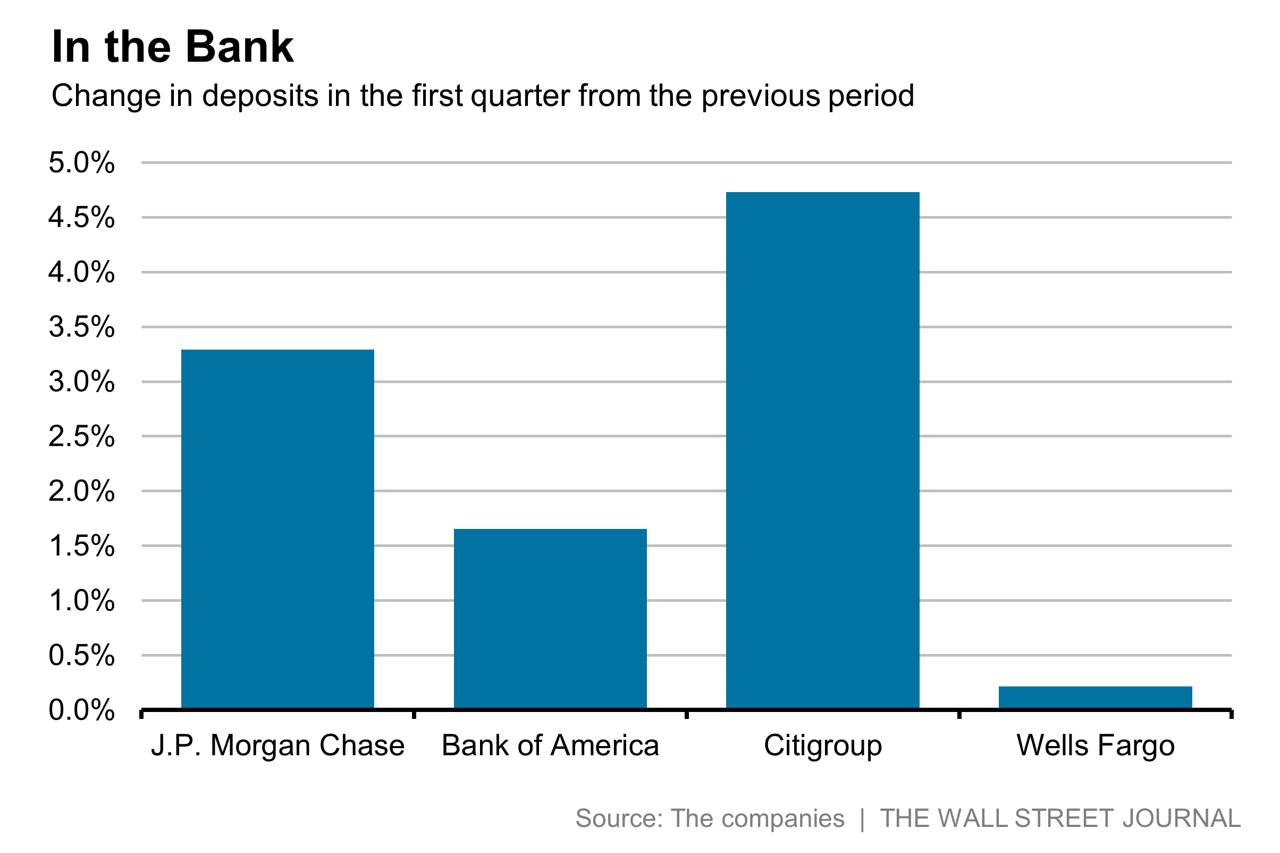

Combined, the big four commercial banks— J.P. Morgan Chase, Bank of America, Wells Fargo and Citigroup —held $4.2 trillion in deposits at the end of the first quarter. That was up 2.1% from the previous quarter, outpacing the overall growth of deposits at U.S. banks, according to Federal Reserve data.

Granted, big banks’ deposits were down slightly versus the first quarter of 2015. But this likely reflects efforts by J.P. Morgan last year to shed so-called nonoperating deposits, or idle corporate deposits not linked to daily cash management, to shrink its balance sheet and cut excess capital it must hold.

For banks, this counts as good news. In recent years, the flood of deposits into big banks was a burden; they couldn’t use all of it due to weak loan demand. That led to a buildup of securities portfolios.

But in the first quarter, total loans at BofA, Citi and Well Fargo were up 5.8%. So the banks are able to put more of the deposit money to work. Indeed, at J.P. Morgan, where total loans rose 11% from a year earlier, the bank’s loan-to-deposit ratio of 64% in the first quarter was up sharply from 56% a year earlier.

Here is why that is good: In the first quarter, BofA paid an average yield of just 0.08 percentage points on U.S. interest-bearing deposits of about $707 billion. Meanwhile, its loans and leases of about $893 billion earned an average yield of 3.74%. That was better than the 2.45% its nearly $400 billion in securities earned, excluding some market-related adjustments. So loan growth allows the banks to at least hold the line on their flagging net-interest margins.

Of course, this wasn’t enough to offset some other big negatives during the quarter, such as market tumult, reduced trading activity and falling long-term yields. But without it, things could have been even worse. And, if nothing else, it shows big-bank depositors aren’t walking the angry too-big-to-fail talk.

0 comments:

Publicar un comentario