Hoisington Quarterly Review and Outlook – 1Q2016

John Mauldin

You often hear me harping on the dangers of too much debt, and I keep my eyes peeled for significant work that backs up my concerns. In today’s Outside the Box good friend Dr. Lacy Hunt of Hoisington Investment Management gives us more ammunition to take on those who just don’t seem to get that the endless piling up of debt is not a sustainable way to run an economy.

The most striking feature of the US economy’s performance in 2015, according to Lacy, was a massive advance in nonfinancial debt that kept the economy stuck in the doldrums of subpar growth. US nonfinancial debt rose 3.5 times faster than GDP last year. (Nonfinancial debt is the sum of household debt, business debt, federal debt, and state and local government debt.)

Lacy points out unfavorable trends in each component of nonfinancial debt:

Household debt:

Delinquencies in household debt moved higher even as financial institutions continued to offer aggressive terms to consumers, implying falling credit standards. Furthermore, the New York Fed said subprime auto loans reached the greatest percentage of total auto loans in ten years. Moreover, they indicated that the delinquency rate rose significantly.

Business debt:

Last year business debt, excluding off balance sheet liabilities, rose $793 billion, while total gross private domestic investment (which includes fixed and inventory investment) rose only $93 billion. Thus, by inference this debt increase went into share buybacks, dividend increases and other financial endeavors…. When business debt is allocated to financial operations, it does not generate an income stream to meet interest and repayment requirements. Such a usage of debt does not support economic growth, employment, higher paying jobs or productivity growth. Thus, the economy is likely to be weakened by the increase of business debt over the past five years.

Federal debt:

U.S. government gross debt, excluding off balance sheet items, gained $780.7 billion in 2015 or about $230 billion more than the rise in GDP….

The divergence between the budget deficit and debt in 2015 is a portent of things to come. This subject is directly addressed in the 2012 book The Clash of Generations, published by MIT Press, authored by Laurence Kotlikoff and Scott Burns. They calculate that on a net present value basis the U.S. government faces liabilities for Social Security and other entitlement programs that exceed the funds in the various trust funds by $60 trillion. This sum is more than three times greater than the current level of GDP.

State and local government debt:

State and local governments … face adverse demographics that will drain underfunded pension plans…. The state and local governments do not have the borrowing capacity of the federal government. Hence, pension obligations will need to be covered at least partially by increased taxes, cuts in pension benefits or reductions in other expenditures.

Lacy adds this note on total debt, which includes nonfinancial, financial, and foreign debt:

Total debt … increased by $1.968 trillion last year. This is $1.4 trillion more than the gain in nominal GDP. The ratio of total debt-to-GDP closed the year at 370%, well above the 250-300% level at which academic studies suggest debt begins to slow economic activity.

Lacy makes the key point that overindebtedness impairs monetary policy, not just in the US but globally:

The Federal Reserve, the European Central Bank, the Bank of Japan and the People’s Bank of China have been unable to gain traction with their monetary policies…. Excluding off balance sheet liabilities, at year-end the ratio of total public and private debt relative to GDP stood at 350%, 370%, 457% and 615%, for China, the United States, the Eurocurrency zone, and Japan, respectively…. The debt ratios of all four countries exceed the level of debt that harms economic growth. As an indication of this over-indebtedness, composite nominal GDP growth for these four countries remains subdued. The slowdown occurred in spite of numerous unprecedented monetary policy actions – quantitative easing, negative or near zero overnight rates, forward guidance and other untested techniques.

Read it and think about this, gentle reader. We’re digging a great big hole that is likely to cave in on us before we manage to claw our way back out of it. We need to “wargame” how we respond in our personal lives. That is going to be a big focus of my letters in the coming months.

Lacy’s firm, Hoisington Investment Management Company (www.Hoisingtonmgt.com), is a registered investment advisor specializing in fixed-income portfolios for large institutional clients. Located in Austin, Texas, the firm has over $5 billion under management and is the sub-advisor of the Wasatch-Hoisington US Treasury Fund (WHOSX).

My days continue to be full of information downloads, phone calls, decisions. Probably not unlike yours. Am I the only one that feels that in a world where we have ever more tools that are supposed to simplify our lives, our lives are becoming more complex? Time seems to be a dwindling resource.

But I really can’t complain because it’s a fascinating complexity to explore. I have roughly 120 people, sorted into various sized groups, doing research on nearly two dozen topics dealing with the future that we will cover in the new book. The groups are beginning to get their research and outlines for the chapters back to me, and overall I’m quite impressed with what I’m reading. We’re talking about 1000+ pages of dense research and links to other articles. As I was thinking about the design of particular chapters and assigning groups to research them, I had a general idea of the direction in which things would go. More often than not, though, I had little idea of the complexity (there is that word again) and the scope of information that the research on each topic would reveal.

It is truly a mind-expanding experience to try to get your head around how the world will change in the next 20 years. I glibly say in speeches that the world is going to change more and faster in the next 20 years than it did in the last 100 years; but when you begin to contemplate the dozens of different areas in which change is going to happen – and not just the technological but the sociological and geopolitical implications of the change – and then, on top of all that, try to think about how all that will impact our investments, it becomes a bit daunting.

Don Quixote comes to mind as I face this task. But I’m going full tilt at the windmill anyway. I hope you’re having a great week, too.

Your trying to solve a very complex puzzle analyst,

John Mauldin, Editor

Outside the Box

Hoisington Quarterly Review and Outlook – 1Q2016

2015’s Surging Debt

The striking aspect of the U.S. economy’s 2015

performance was weaker economic growth coinciding with a massive advance in

nonfinancial debt. Nominal GDP, the broadest and most reliable indicator of

economic performance, rose $549 billion in 2015 while U.S. nonfinancial debt

surged $1.912 trillion. Accordingly, nonfinancial debt rose 3.5 times faster

than GDP last year. This means that we can expect continued subpar growth for

the U.S. economy.

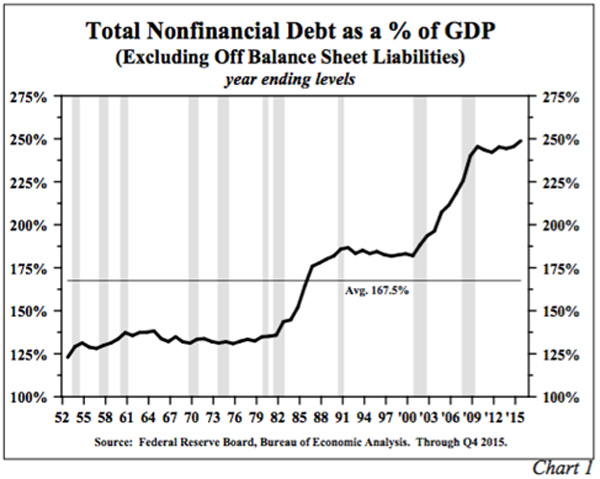

The ratio of nonfinancial debt-to-GDP rose to a

record year-end level of 248.6%, up from the previous record set in 2009 of

245.5%, and well above the average of 167.5% since the series’ origination in

1952 (Chart 1). During the four and a half decades prior to 2000, it took about

$1.70 of debt to generate $1.00 of GDP. Since 2000, however, when the

nonfinancial debt-to-GDP ratio reached deleterious levels, it has taken on

average, $3.30 of debt to generate $1.00 of GDP. This suggests that the type

and efficiency of the new debt is increasingly non-productive.

Most significant for future growth, however, is

that the additional layer of debt in 2015 is a liability going forward since

debt is always a shift from future spending to the present. The negative

impact, historically, has occurred more swiftly and more seriously as economies

became extremely over-indebted. Thus, while the debt helped to prop up economic

growth in 2015, this small plus will be turned into a longer-lasting negative

that will diminish any benefit from last year’s debt bulge.

Unfavorable Trends

in Nonfinancial Debt

Nonfinancial debt consists of the following: a)

household debt, b) business debt, c) federal debt and d) state and local

government debt.

Households

Household debt, excluding

off balance sheet liabilities, was 78.3% of GDP at year-end 2015, more than 20

percentage points above the average since 1952.

However, this ratio has

declined each year since the 2008-09 recession.

Credit standards were lowered considerably for

households in 2015 making it easier to obtain funds. Delinquencies in household

debt moved higher even as financial institutions continued to offer aggressive

terms to consumers, implying falling credit standards. Furthermore, the New

York Fed said subprime auto loans reached the greatest percentage of total auto

loans in ten years. Moreover, they indicated that the delinquency rate rose

significantly. Fitch Ratings reported that the 60+ day delinquencies for

subprime auto asset-backed securities jumped to over 5%, the highest level

since 1996. Prime and subprime auto delinquencies are likely to move even

higher. According to the Fed, 34% of auto sales last year were funded by

72-month loans. With used car prices falling on an annual basis, J.D. Power

indicates that the negative equity on auto loans will hit a ten-year high of

31.4% this year.

Despite the lowering of credit standards, the

ratio of household debt-to-GDP did decline in 2015, primarily due to mortgage

repayments. However, the apparent decline in household debt is somewhat

misleading because it excludes leases.

The Fed website acknowledges the deficiency of

excluding leases by pointing out that personal consumption expenditures (PCE),

compiled by the Bureau of Economic Analysis (BEA), do include leases. With

leases included, the change in consumer obligations can be inferred by using

the personal saving rate (PSR), which is household disposable income minus

total spending (PCE). If the PSR rises (i.e. spending is growing more slowly

than income) debt is repaid or not incurred. Indeed from 2008 to 2012 the PSR rose

from 4.9% to 7.6%. However, since 2012, the saving rate has declined to 5.0%

(at year-end 2015), implying a significant increase in debt obligations. The

consumer did, in fact, increase borrowing last year by $342 billion even though

the household debt as a percent of GDP declined. The household debt-to-GDP

ratio dropped from 82.0% in 2012 to 78.3% in 2015; however, excluding mortgages

consumers have actually become more leveraged over the past three years with

non-mortgage debt rising from 17.9% to 19.5% of GDP.

Businesses

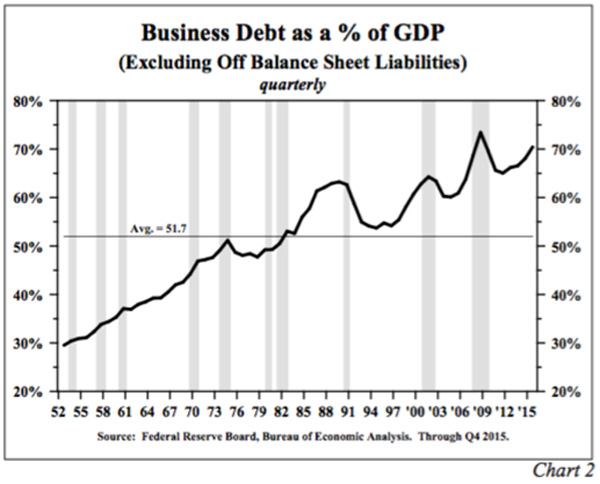

Last year business debt,

excluding off balance sheet liabilities, rose $793 billion, while total gross

private domestic investment (which includes fixed and inventory investment)

rose only $93 billion. Thus, by inference this debt increase went into share

buybacks, dividend increases and other financial endeavors, albeit corporate

cash flow declined by $224 billion. When business debt is allocated to

financial operations, it does not generate an income stream to meet interest

and repayment requirements. Such a usage of debt does not support economic

growth, employment, higher paying jobs or productivity growth. Thus, the

economy is likely to be weakened by the increase of business debt over the past

five years (Chart 2).

In 2015 the ratio of business debt-to-GDP advanced

two percentage points to 70.4%, far above the historical average of 51.7%. Only

once in the past 63 years has this ratio been higher than in 2015. That year

was 2008, when the denominator of the ratio (GDP) fell sharply during the

recession. Importantly, the ratio advanced over the past five years just as it

did in the years leading up to the start of the 2008-09 recession, and the 2015

ratio was 3% higher than immediately prior to 2008.

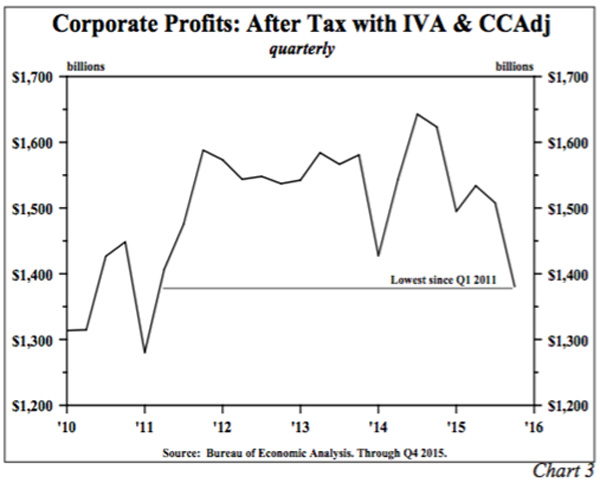

The rise in the debt ratio is even more striking

when compared to after-tax adjusted corporate profits, which slumped $242.8

billion in 2015. The 15% fall in profits pushed the level of profits to the

lowest point since the first quarter of 2011 (Chart 3). In the past eight

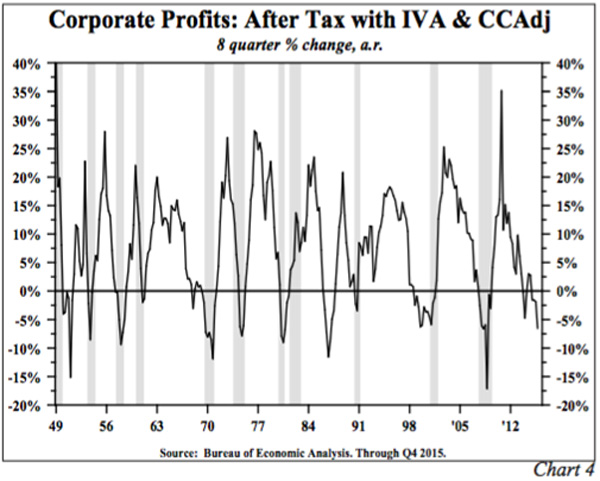

quarters profits fell 6.6%, the steepest drop since the 2008-09 recession. On

only one occasion since 1948 did a significant eight quarter profit contraction

not precede a recession (Chart 4).

The jump in corporate debt, combined with falling

profits and rising difficulties in meeting existing debt obligations, indicates

that capital budgets, hiring plans and inventory investment will be scaled back

in 2016 and possibly even longer. Indeed, various indicators already confirm

that this process is underway. Core orders for capital goods fell sharply over

the first two months of this year. Surveys conducted by both the Business

Roundtable and The Fuqua School of Business at Duke University indicate that

plans for both capital spending and hiring will be reduced in 2016.

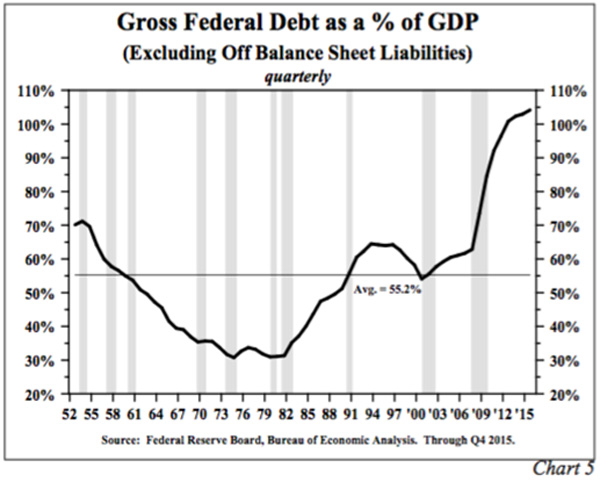

U.S. Government

U.S. government gross

debt, excluding off balance sheet items, reached $18.9 trillion at year-end

2015, an amount equal to 104% of GDP, up from 103% in 2014 and considerably

above the 63-year average of 55.2% (Chart 5).

U.S. government gross debt, excluding off balance

sheet items, gained $780.7 billion in 2015 or about $230 billion more than the

rise in GDP. The jump in gross U.S. debt is bigger than the budget deficit of

$478 billion because a large number of spending items have been shifted off the

federal budget.

The divergence between the budget deficit and debt

in 2015 is a portent of things to come. This subject is directly addressed in

the 2012 book The Clash of

Generations, published by MIT Press, authored by Laurence Kotlikoff

and Scott Burns. They calculate that on a net present value basis the U.S.

government faces liabilities for Social Security and other entitlement programs

that exceed the funds in the various trust funds by $60 trillion. This sum is

more than three times greater than the current level of GDP. The Kotlikoff and

Burns figures are derived from a highly regarded dynamic generational

accounting framework developed by Dr. Kotlikoff. They substantiate that,

although these liabilities are not on the balance sheet, they are very real and

will have a significant impact on future years’ budget deliberations.

According to the Congressional Budget Office, over

the next 11 years federal debt will rise to $30 trillion, an increase of about

$10 trillion from the January 2016 level, due to long understood commitments

made under Social Security, Medicare and the Affordable Care Act. Any kind of

recession in this time frame will boost federal debt even more. The government

can certainly borrow to meet these needs, but as more than a dozen serious

studies indicate this will drain U.S. economic growth as federal debt moves

increasingly beyond its detrimental impact point of approximately 90% of GDP.

State and Local Governments

The above federal debt

figures do not include $2.98 trillion of state and local debt. State and local

governments also face adverse demographics that will drain underfunded pension

plans.

Already problems have become apparent in the cities of Chicago,

Philadelphia and Houston as well as in the states of Illinois, Pennsylvania and

Connecticut; the rating agencies have downgraded their respective debt rankings

significantly over the past year. More problems will surface over the next

several years. The state and local governments do not have the borrowing

capacity of the federal government. Hence, pension obligations will need to be

covered at least partially by increased taxes, cuts in pension benefits or

reductions in other expenditures.

Total Debt

Total debt, which includes nonfinancial (discussed

above), financial and foreign debt, increased by $1.968 trillion last year.

This is $1.4 trillion more than the gain in nominal GDP. The ratio of total

debt-to-GDP closed the year at 370%, well above the 250-300% level at which

academic studies suggest debt begins to slow economic activity.

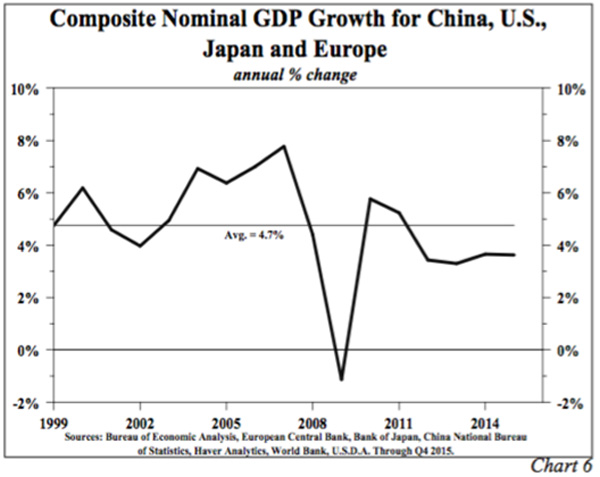

Over-indebtedness Impairs Global Monetary

Policy

The Federal Reserve, the European Central Bank,

the Bank of Japan and the People’s Bank of China have been unable to gain

traction with their monetary policies. This is evident in the growth of nominal

GDP and its two fundamental determinants – money and velocity. The common

element impairing the actions of these four central banks is extreme

over-indebtedness of their respective economies. Excluding off balance sheet

liabilities, at year-end the ratio of total public and private debt relative to

GDP stood at 350%, 370%, 457% and 615%, for China, the United States, the

Eurocurrency zone, and Japan, respectively.

The debt ratios of all four countries exceed the

level of debt that harms economic growth. As an indication of this

over-indebtedness, composite nominal GDP growth for these four countries

remains subdued. The slowdown occurred in spite of numerous unprecedented

monetary policy actions – quantitative easing, negative or near zero overnight

rates, forward guidance and other untested techniques. In 2015 the aggregate

nominal GDP growth rose by 3.6%, sharply lower than the 5.8% growth in 2010

(Chart 6). The only year in which nominal GDP was materially worse than 2015

was the recession year of 2009.

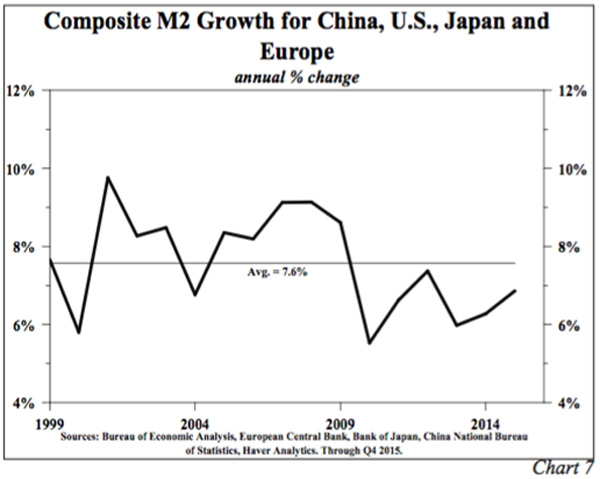

Since nominal GDP is equal to money (M2) times its

turnover, or velocity (V), the present situation becomes even less rosy when

examining the two critical variables M2 and V.

Money Growth

Utilizing M2 as the

measure of money, the growth of M2 for China, the United States, the Eurozone

and Japan combined was 6.9% in 2015, almost a percentage point below the

average since 1999, the first year of available comparable statistics for all

four (Chart 7). Historical experience shows that central banks lose control

over money growth when debt is extremely high.

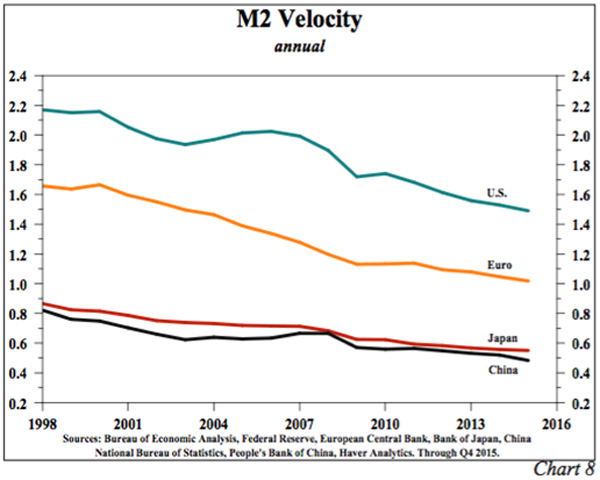

Velocity

Velocity, or the turnover

of money in the economy (V=GDP/M2), constitutes a serious roadblock for central

banks that are trying to implement policy actions to boost economic activity.

Velocity has fallen dramatically for all four countries since 1998 (Chart 8).

Functionally, many factors influence V, but the

productivity of debt is the key.

Money and debt are created simultaneously. If

the debt produces a sustaining income stream to repay principal and interest,

then velocity will rise since GDP will eventually increase by more than the

initial borrowing. If the debt is a mixture of unproductive or

counterproductive debt, then V will fall. Financing consumption does not

generate new funds to meet servicing obligations. Thus, falling money growth

and velocity are both symptoms of extreme over-indebtedness and non-productive

debt.

Velocity is below historical norms in all four

major economic powers. U.S. velocity is higher than European velocity that, in

turn, is higher than Japanese velocity.

This pattern is entirely consistent

since Japan is more highly indebted than Europe, which is more indebted than

the United States. Chinese velocity is slightly below velocity in Japan. This

is not consistent with the debt patterns since, based on the reported figures,

China is less indebted than Japan. This discrepancy suggests that Chinese

figures for economic growth are overstated, an argument made by major scholars

on China’s economy.

Outlook

Our economic view for 2016 remains unchanged. The

composition of last year’s debt gain indicates that velocity will decline more

sharply in 2016 than 2015. The modest Fed tightening is a slight negative for

both M2 growth and velocity. Additionally, velocity appears to have dropped

even faster in the first quarter of 2016 than in the fourth quarter of 2015.

Thus, nominal GDP growth should slow to a 2.3% - 2.8% range for the year. The

slower pace in nominal GDP would continue the 2014-15 pattern, when the rate of

rise in nominal GDP decelerated from 3.9% to 3.1%. Such slow top line growth suggests

that spurts in inflation will simply reduce real GDP growth and thus be

transitory in nature.

Accordingly, the prospects for the Treasury bond

market remain bright for patient investors who operate with a multi-year

investment horizon. As we have written many times, numerous factors can cause

intermittent increases in yields, but the domestic and global economic

environments remain too weak for yields to remain elevated.

Van R. Hoisington

Lacy H. Hunt, Ph.D.

Lacy H. Hunt, Ph.D.

0 comments:

Publicar un comentario