GLD: The Fed Meeting Will Provide A Breakout Catalyst

by: SomaBull

- If gold surpasses those early March highs with a vengeance, then it's game over for those that are still positioned for a bear market in precious metals.

- If GLD can hold these levels this week and start to move up again, the HUI will ultimately reach the 225-250 region before we see the first real consolidation.

- Silver has really exploded since that April 4th date, and has now clearly started to participate in this sector rally.

- Gold and silver should continue to rally hard in the face of rising interest rates and increasing inflation pressures.

- If GLD can hold these levels this week and start to move up again, the HUI will ultimately reach the 225-250 region before we see the first real consolidation.

- Silver has really exploded since that April 4th date, and has now clearly started to participate in this sector rally.

- Gold and silver should continue to rally hard in the face of rising interest rates and increasing inflation pressures.

The SPDR Gold Trust ETF (NYSEARCA:GLD) continues to trade in the 116-121 range, which it has been stuck in during the last 2 1/2 months. It's no surprise though that the physical metal hasn't made any progress to the upside during this time, as we still have many investors focused on general equities. That is where hope and faith reside at the moment, and the latest rebound in the major U.S. indices since the February lows keeps that hope alive. But what is clear, especially given the volume we are seeing in GLD, is that a major repositioning is occurring. The volume in GLD is double to triple what it was at this time last year on a daily basis, and that is consistent volume as well over the last several months. It's that consistency day after day since January/February that implies that this move has tremendous "staying power."

In my previous article earlier this month on GLD, I talked about the possibility of 114 being tested if the 50 day didn't hold. As you can see in the chart below, the 50 day has been a strong level of support over the last few weeks. But I will say that the action on Friday perked up my ears a bit. It's not worrisome at this juncture, just more fascinating to watch than anything as it's clear that both bulls and bears are digging in their heals. You have to keep in mind that this is really the line in the sand for all of those still bearish on the sector. If gold surpasses those early March highs with a vengeance, then it's game over for those that are still positioned for a bear market in precious metals.

(Source: StockCharts.com)

The gold stocks themselves have been completely ignoring what GLD has been doing, as the HUI has gone from strength to strength while gold has consolidated. I have been warning in my articles since February that we simply might not see that big of a correction in the HUI, as new bull markets are very powerful and you really don't get those large sell-offs in the early stages.

However, I wouldn't completely rule out the possibility of one still happening. If GLD sells down to 114 over the next week, then we could see a swift plunge in the HUI back to the 170-180 region. But the correct strategy since the beginning of the year, and the one I have been emphatically recommending, is to keep buying weakness and not try to time this unfolding bull market by jumping in and out of positions. That will most likely result in repurchasing shares at higher prices.

If GLD can hold these levels this week and start to move up again, then I feel that the HUI will ultimately reach the 225-250 region before we see the first real consolidation in the gold and silver stocks. That's been my initial target (before a pause would occur) since the breakout in February.

Should it play out that way, then that 225-250 level could be reached next 1-2 months, and then I believe the HUI would spend several months consolidating in the 200-250 range. The summer months are usually tough for the gold sector anyway, particularly July, so this fits in with that time-frame nicely. But things don't always play out as expected, that's just what looks most likely at this juncture. We will have to see how the HUI ultimately progresses from this point. I will just say that any breakout of GLD from its current level would most definitely put this scenario in play. And I also wanted to mention that while the HUI has been ignoring GLD's flattish trading pattern, and is instead moving to the beat of its own drum, from this point forward it will be the price of gold that ultimately dictates the HUI's short-term direction. I just don't believe that the two (GLD and the HUI) can continue down different paths over the next several weeks, they will move in lockstep.

(Source: StockCharts.com)

I also want to point out that I'm seeing a couple of red flags in the gold and silver stock space.

Not in terms of this turning back into a bear market, but in terms of this becoming more of a stock pickers market should the HUI reach that 225-250 level over the next month or two.

Companies like First Majestic (NYSE:AG), Endeavour Silver (NYSE:EXK), and Coeur (NYSE:CDE) have been the clear leaders when it comes to silver and gold stocks. They have had enormous runs over the course of the last several months, and are sporting gains in the 200-300% range. While they still have upside should the HUI move to 250, I don't envision them doubling in value during that time. And then you have Harmony Gold (NYSE:HMY), which was really one of the early movers in the sector as it bottomed in December 2015 and has proceeded to shoot up like a rocket since (going from $0.50 to $4.00 during that time). It is now about 25% off its most recent high from earlier this month, and is clearly in consolidation mode. While HMY has been a phenomenal performer over the last several months, I'm not sure that its most recent high will be surpassed in the short-term, should the HUI have further room to run. If it does, then I believe the gains will be more muted compared to other stocks in the sector. A stock such as Gold Fields (NYSE:GFI) - which has doubled in value from the lows - has been consolidating for the last few months already and is in no way overbought like the others below. There are several companies like GFI that are lagging somewhat, and I believe a basket of these will far outperform the recent high-flyers, should the HUI continue to trend to that mid-200 territory over the coming weeks.

(Source: StockCharts.com)

In other words, it's time to be more selective when it comes to gold and silver stocks. Some might double should the HUI increase by 25%, some might stay flat and consolidate further, others might eke out decent gains but not make significant progress.

Again, it's all dependent on what GLD does in the short-term. If it decides to head lower from here then the HUI is going down, possibly by a significant amount (at least I would have to believe given the gains). I still lean towards GLD breaking out to the upside, and we will most definitely have an answer here shortly as the Fed is on tap and will provide a catalyst both in terms of the stock market and the precious metals sector.

Silver Finally Joins The Party

In my article from early April, I talked about the underperformance of physical silver compared to gold and the precious metal stocks. I stated at the time:

I still believe this is simply a waiting game, and silver will eventually break out to the upside very shortly. It's at $15.05 at the moment, with $16.00-$16.25 being the key level to surpass in the near term to get this party started.

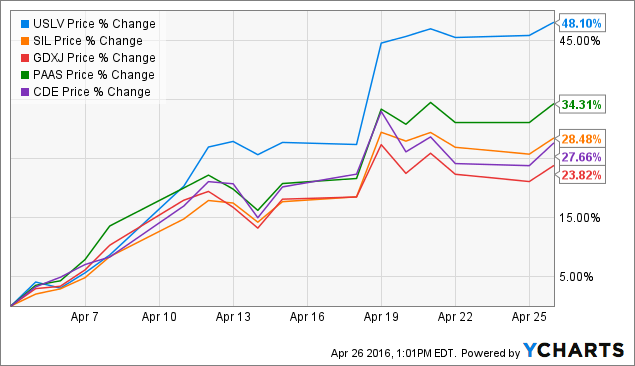

Silver has really exploded since that April 4th date, and has now clearly started to participate in this sector rally.

(Source: StockCharts.com)

I also said at the time that I'm playing this divergence in silver via the VelocityShares 3x Long Silver ETN (NASDAQ:USLV), which is a highly leveraged physical silver fund. I mentioned that:

Everything at this moment is pointing to physical silver reversing the 4+ year downtrend, we just need confirmation by slightly higher prices first. If that occurs, USLV should have a major spike over the next 3-6 months, one which should produce a return in excess of 200%...Any increase in physical to those levels will also result in large short-term gains for the silver companies, just not nearly to the same extent as what USLV will experience.

Over the last few weeks, USLV is up 48%, far surpassing the gains on average for silver companies (as well as junior gold/silver miner ETFs). USLV is 1/4 of the way to my 200% expected gain, but since this is a highly leveraged fund, I already have a well designed exit strategy and I don't plan to try and realize a 200% return. That wouldn't be advisable on a triple levered ETN, which will ultimately give up all of these gains when physical silver starts to consolidate. As a side note, I still own silver stocks, and mentioned at the time that I didn't plan to liquidate any of those holdings or "rotate" into USLV. Rather I had some excess cash on the sidelines and continually built my position in the ETN.

So silver has been performing exactly as I expected over the last few weeks, but gold still hasn't broken out yet since my last article. I continue to believe that GLD will start a new move higher soon, but I just don't know if it will hold support here at the 50 day and then take off or retest that 114 region first before it begins higher again. We are still in wait and see mode.

Say Goodbye To Ultra-Low Rates, and Hello To Rising Inflation Pressure

Many investors aren't prepared for what's coming down the pipe, at least here in the U.S. Even to this day, we have individuals still firmly in the deflation camp and expecting further decreases in U.S. Treasury yields as well as a declining gold price. That herd mentality mindset will soon reverse if the precious metal sector increases even further.

The conundrum that faces investors with those expectations is that the Fed, more specifically Janet Yellen, is only going to hold back on raising rates if the stock market panics (which she has clearly implied in past speeches and commentary). You have the labor market where the Fed wants and you have the PCE getting close to its preferred target, which is why the Fed has already begun to normalize interest rates. But the stock market is very jumpy and is deathly afraid of any sort of bump up in rates, as the assumption is the economy just can't handle a Fed Funds rate of 1% or higher. Which is a silly notion and has no basis in economic reality, but nonetheless, is firmly embedded into the cerebral cortex of the majority of investors and economists at the moment.

If you went back 10-20 years ago and told a group of high valued investors that the market in 2016 was panicking at the prospects of the Federal Reserve lifting rates to 1% or more, the reaction in the room would have probably been an extreme concern about the state of the U.S. Economy. Was there a Depression occurring, a World War, double digit unemployment, significant negative GDP growth, a stock market crash, massive deflation, or some other extreme event? That would be the only logical reason to assume that our financial system couldn't withstand a measly 1% Fed Funds rate, or needed this ultra-low rate environment to continue. Especially when a decade or two ago it was normal for the Fed Funds rate to be in the 5% range.

But we are far from any of those scenarios. We have basically full employment at the moment, GDP isn't gangbusters right now but it's still in positive territory, the stock market is sitting close to all-time highs, housing has recovered, global conditions (both political and economical) are not at extremely elevated or worrisome levels.

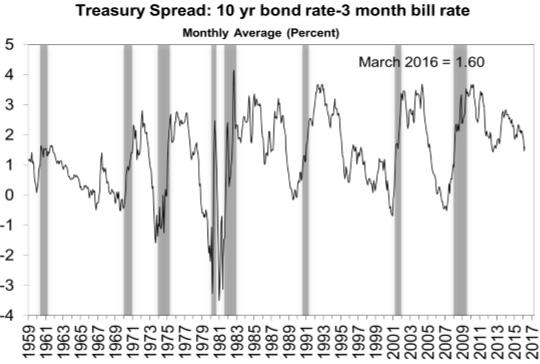

In no way are Treasury spreads indicating that a recession is on the horizon. The difference between the 3-month bill rate and 10 year last month was 1.6%, it's now 1.7% at today's rates.

Past recessions have always occurred after the spread was at or around zero, with the yield curve flat or inverted.

(Source: Federal Reserve Bank Of New York)

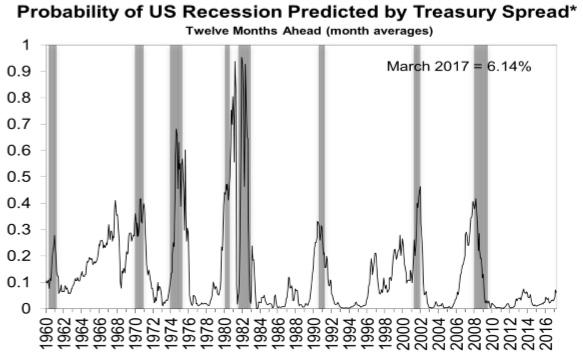

The Federal Reserve Bank of New York currently puts the probability of a recession over the next year at just 6.14%. Granted the U.S. economy is due for one soon (given past historical data), but we could still be a few years out in terms of time-frame as we have had numerous 10-year gaps between recessions before.

(Source: Federal Reserve Bank Of New York)

The bottom line, is nothing is flashing a warning that the Fed should hold back raising rates, other than a jumpy stock market. I continue to believe the Fed will increase by 25 basis points several times this year, probably back-end loaded though. Gold and silver should continue to rally hard in the face of rising interest rates and increasing inflation pressures as both the PCE and CPI are now clearly trending higher (I have my eye on the "shelter" component of the CPI in particular as we are seeing a continued steady increase over the last few years).

The only way the Fed is going to hold off raising rates even more is if the stock market buckles from current levels, and I'm not even sure that scenario would ultimately stop the Fed from increasing the Funds rate. Either way, gold is going to be the sector to be invested in over the next few years, and that is becoming clear to more and more investors everyday. Which is why you are seeing the current reaction in the gold sector.

The 10-year Treasury yields have bottomed, as while they have approached their 2012 lows several times over the last few years, yields still remain above that 1.40% level. I see a nice setup taking place for the yield curve to steepen over the next year or so, as long-term rates begin to normalize at a quicker pace that short-term rates.

(Source: Bloomberg)

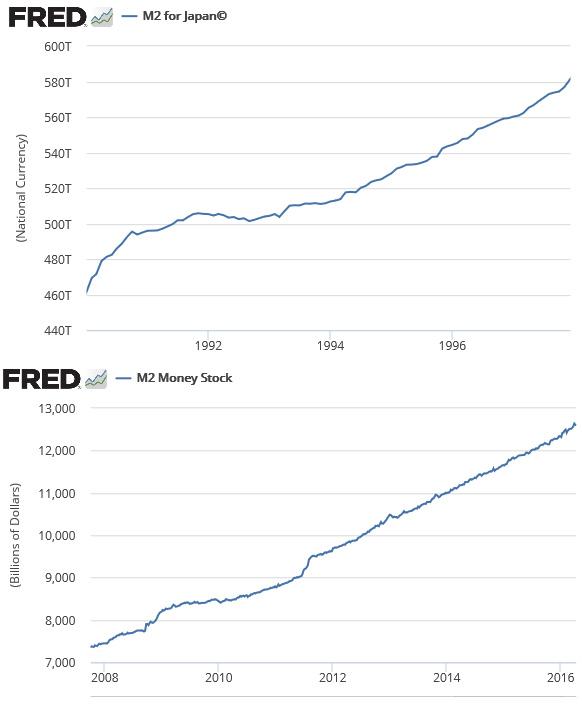

And for anybody saying that the U.S. is like Japan circa 1990, and the we could be faced with deflationary pressures for years to come, I would consider the difference between money supply growth for both economies/situations. From each of their respective stock market peaks (Nikkei in December 1989 and S&P in October 2007), and charting the increase in M2 over the next 8 or so years that followed, we can see that the Japanese money supply only moved higher by about 25% during that time. Conversely, the U.S. money supply has risen by 75%. If M2 here in the U.S would have only grown 25% since the stock market peak of 2007 - and subsequent financial crisis that soon followed - then we would be only looking at a current M2 figure of just over $9 trillion. If that's where U.S. money supply stood I could make the case for an ultra-low interest rate environment for several more years. But that's not the road we are on.

(SOURCE: FRED)

I'm still of the opinion that general equities trend sideways at best over the next few years, but I also don't envision a major crash. A 20%-30% decline could develop over the course of that time frame, along with a mild recession as well. It's during this lull in the market that gold and silver will really rip higher.

It doesn't matter what the U.S. Dollar does during that time either. The continued thinking seems to be that gold needs a declining USD to make further headway, but that is simply not the case - as I have pointed out many times in the past that there is no long-term correlation between the two.

Investors needs to keep in mind the U.S. dollar index was flat during 1979 to early 1980, and stayed in a relatively tight range during that time. Gold went from $200 to over $800 per ounce during that period, and interest rates were skyrocketing during that time as well.

0 comments:

Publicar un comentario