GLD And The Structure Of Global Gold Markets

by: Matt R O'Connor

Summary

- A look at the not often discussed structure and mechanics of the global gold markets.

- How SPDR Gold Trust's creation/redemption process works in theory to close gaps between the Trust's value and physical gold prices and evidence this is occurring.

- SPDR Gold Trust's relative (in)significance to global gold markets.

- The future of global gold markets, London remains the global capital, but China is growing.

- How SPDR Gold Trust's creation/redemption process works in theory to close gaps between the Trust's value and physical gold prices and evidence this is occurring.

- SPDR Gold Trust's relative (in)significance to global gold markets.

- The future of global gold markets, London remains the global capital, but China is growing.

If you've been following my recent articles, you already know I've been diving into gold and gold related investments namely to examine what the data tell us about various potential plays on gold. In my last article I looked at the historical relationship between the popular gold miner ETF, the Market Vectors Gold Miners ETF (NYSEARCA:GDX), and the largest ETF tracking physical bullion, the SPDR Gold Trust ETF (NYSEARCA:GLD), and discussed some expected behaviors supported by hard data which investors in either of these ETFs should be aware of.

For this article I continued my investigation to take a look at the liquidity and fundamental structure of global gold markets. In doing so I hope to shed some light on topics related to gold and gold related investments that often are taken for granted and not likely to be well understood.

The Structure of Gold Markets

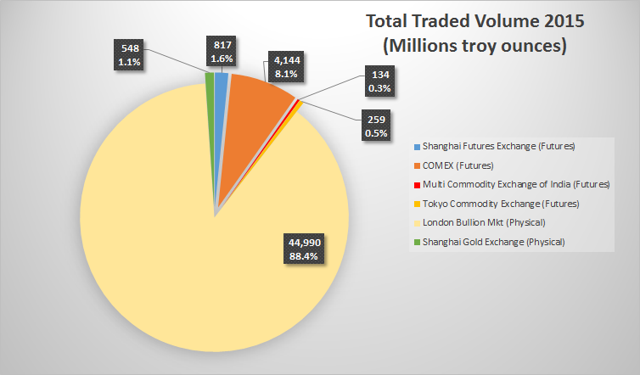

There are a number of marketplaces for gold for both futures and physical gold. The most significant either for their current size or rate of growth are:

Sources: COMEX, TOCOM, MCX, SHFE, SGE, LBMA. For those surprised by the relatively small size of Shanghai markets here is a Bloomberg article to triangulate the data (article is from a year ago but serves as a ballpark verification)

The LBMA is an OTC market where gold trades twenty-four hours a day in the same basic manner as the Forex markets: trades occur between two parties and are not standardized nor cleared through an exchange. Because of this- again comparable to the Forex markets- what would be considered even the most basic information for equity markets can be difficult to find for the gold bullion market. Luckily however, there are a few direct sources.

One can think of the LBMA as a network of affiliated and participating global bullion dealers.

While they do not operate on an exchange, there are well established market conventions, including the globally recognized settlement method for gold bullion trades through "LOCO London" accounts which settle in gold holdings held on deposit with LBMA bullion dealers.

The LBMA also has a market standard for the bars of gold themselves- London Good Delivery bars- which are only sourced through a limited number of suppliers associated with the LBMA.

Besides providing liquidity, the LBMA is also known for publishing the gold fix, the widest used benchmark for spot gold prices (when people talk about the price of gold in general, even if they don't realize it, they are referring to the LBMA gold fix). The fix essentially functions as a twice daily auction, with a clearing price being set where the balance of orders clears. Today there are eight member banks which participate in the fixing price process, including recently for the first time a Chinese bank: the Bank of China.

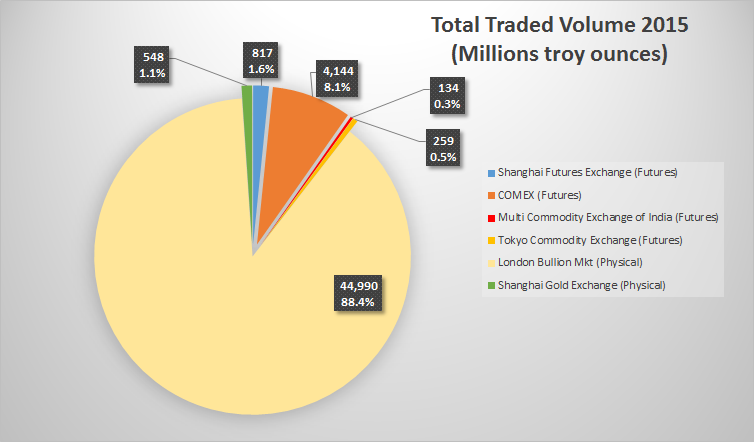

Some but not all OTC transactions clear through the LBMA clearing member banks. Trading parties might choose to go out of their way and clear through these banks if one (or both) are concerned about counter party risk, but otherwise might avoid doing so to save costs and/or to keep their flows hidden. The LBMA reports their clearing statistics on a monthly basis, though the cited figures represent not month totals but the average daily values over the month. For example in January 2016, 18.7 million ounces were cleared daily, but that's not to be confused as the total traded, that's just the subset of activity that was cleared. For data about the total traded amount we have to look to a 2011 liquidity survey published by the LBMA itself. There are various reasons the report may over or under estimate the true figure, but if the report is to be believed, in Q1 2011 the amount of traded gold was 10x the amount actually cleared. To derive the LBMA 2015 volume estimate in the above pie chart that same 10x multiple has been applied to the clearing numbers.

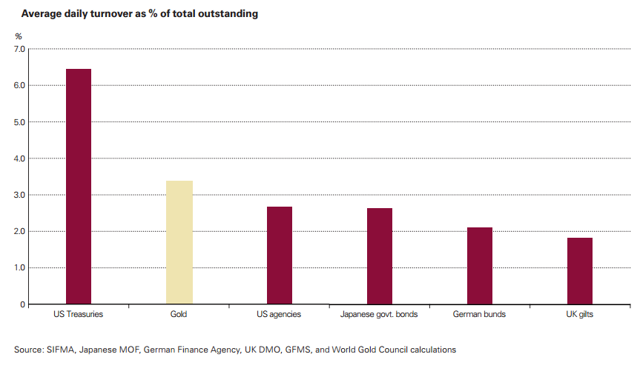

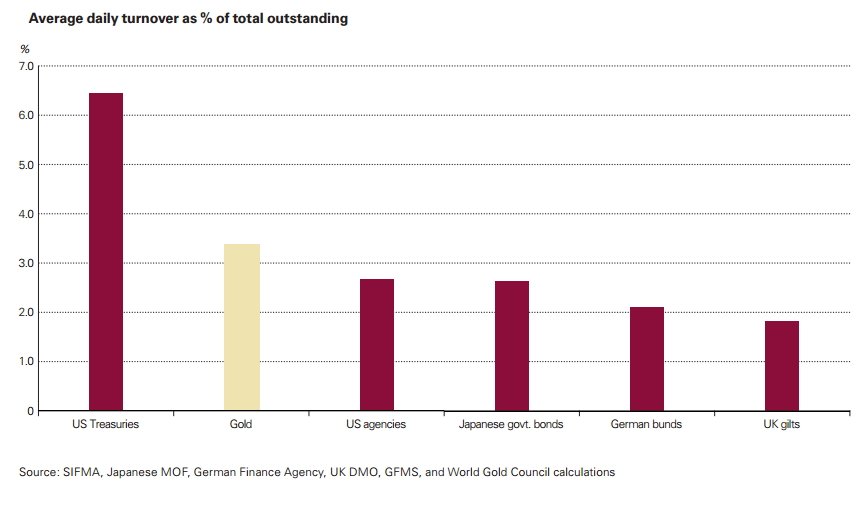

While daily turnover in gold as a percentage of total stocks may sound high, its levels are comparable to that of sovereign debt

You might be wondering how its possible for 45 billion ounces of gold to trade in London yearly, when estimates put the total gold ever mined at about 6 billion ounces. Remember these are volume numbers, with a trade being counted each time ownership of gold changes ones party to another but with no regard to how these changes net against each other. For example, if I sell you a troy ounce and then buy it back from you a week later, that's 2 troy ounces of volume even though there has been no net change in holdings (this is not unique to the LBMA and is equally true of volume traded on all marketplaces so the above pie chart is still an apples-to-apples comparison). The LBMA clearing number itself remains a more indicative figure for the actual net exchange of gold being moved between accounts: a number which typically fluctuates around 20 million ounces/day.

Physical Markets vs Futures Markets

There are in essence two major types of market places, the futures markets (COMEX, SHFE, MCX, TOCOM- and a handful of others that are a very small portion of global liquidity) and physical markets (SGE and LBMA).

In the futures markets contracts trade with fixed specifications for delivery size, date, quality and location. For example 1 COMEX contract is always 100 troy ounces and can be "delivered" or "physically settled" only at the COMEX warehouse itself.

Only a small portion of traded futures contracts are physically settled at the exchange. You can infer this directly yourself simply by looking at the level of trading activity and open interest in the futures contract about to expire directly on the CME's volume page.

For parties who want to take physical delivery, much more common than holding the future contract to expiration is to use something called an 'Exchange for Physical' trade to do so. You can see this activity indicated in the column marked 'EFP' on the CME volume page linked above. An EFP is actually an OTC trade that is cleared through the exchange in which two parties can come to an agreement to swap positions in the futures for physical gold. In essence it works no differently than an OTC trade cleared through the LBMA only at least one party begins with an initial futures position. Here's an example of how it might look:

The important take away though is that via EFP trades, futures positions can be converted to equivalent physical trades. Which brings us to the LBMA and SGE markets. Some, perhaps even most, of these EFP trades on the COMEX futures may actually be conducted with LBMA clearing members. Like the futures EFP trades, all trading on the LBMA is OTC, this means there are no standardized contracts and there is no central exchange to absorb counter party risk and facilitate settlement (unless parties clear through the LBMA clearing banks). There are however some market conventions, including that standard dealing amounts in the spot market are 5,000-10,000 ounces in gold.

From the LBMA's 2011 report we know that roughly 90% of trading activity in OTC takes place in the spot market, with the rest being composed of forwards (agreeing to exchange gold at a fixed price at a fixed date in the future) or other transactions including swaps and EFPs.

Because of the large minimums and non-transparent market structure one must realize this is not a market in which small/retail players easily participate. The physical gold markets in the West have long been- and continue to be- markets in which retail flows are laughably small and it is not in the market makers' economic interests to cater to or clear/redeem/manage retail trades in physical gold- they are happy to leave that to the 3rd party dealers who charge investors massive premiums to invest in physical gold. For instance, for market participants on the LBMA typical bid offer spreads are about .04-.07%, or about $.70 if gold is trading at $1,200 per ounce. By comparison, spreads for popular retail gold dealers even when dealing in 10 ounce increments (quite large increments for most retail investors) are around 1.3%- or even significantly higher. In other words retail investors trading physical gold are paying a premium of at best nearly 25x that in spot gold markets, and likely in many cases far worse.

We will discuss GLD much more in a moment- but one can immediately see why instruments like GLD are potentially of value to the retail investor. By allowing authorized participants to redeem shares for gold or create shares by depositing gold for a small fee (rather than GLD being the party which has to go out on the market and pay fees to transact), GLD is- in theory- able to pass on a great deal of savings in the costs incurred in investing in physical gold to its holders while charging a small fee in return.

The SGE is an interesting exception to the non-individual investor market structure model though. Partly because of its much smaller size and much shorter existence, and partly because of China's encouragement of its public's direct investment into gold as a kind of quasi-government reserve, the SGE caters much more to the individual investor.

Individual Chinese citizens can register at a member institution with the SGE and are assigned a ten digit identification code that is permanent and unique to them. They can then deposit gold or cash, transact via the SGE, and withdraw funds or withdraw gold via an authorized vault.

Outside of central bank purchases (another issue entirely) China gold volumes are often overestimated as a portion of the market. Even with tremendous growth in recent years SGE activity is only about 1% of the total gold market activity. Though there are several million individual participants in the SGE, the real money remains with the large institutions which transact on the LBMA.

GLD's Role in the Gold Markets

In late 2004 GLD was created as an option to provide investors with access to hold a paper instrument tied to the value of physical gold, thus in theory allowing for exposure to gold prices with the ease of trading an ETF and without the costs in time and money of holding physical gold itself. GLD aims to do this by owning gold bullion which is held in their name in a vault by a custodian. From GLD's own prospectus:

While there are some common concerns about GLD- some more valid than others- it is also a unique aspect of the gold markets that is frequently misunderstood and deserves a further examination.

Other than previously amassing the 260,000 ounces of gold held at the time it first began trading, GLD does not buy or sell gold. As of the latest numbers, for each issued share of GLD the Custodian holds about .095586 ounces of gold. The method by which additional shares are created or destroyed is the same method by which additional gold is acquired or disposed of, and it is the same mechanic by which GLD's price remains tied to the spot price of gold.

Once again, as per the GLD prospectus,

Because of this creation/redemption process and the fact that GLD shares have a gold ounce equivalent, it is no accident or coincidence that GLD's per share price is tied to spot gold prices.

There is a fundamental and often misunderstood mechanic which governs this that relies not on any parties watching out for investor's best interests, but only on the selfish profit-motive interests of a few rich and powerful private parties. Therefore, it is relatively unlikely this relationship should break down outside the most extreme of circumstances. It functions as such:

Historically premiums and discounts have not existed for prolonged periods and have been generally within +/- .25% even during times of financial crisis. Over the entire life of the fund the 99th percentile of daily discount/premiums is a .37% premium and the 1st percentile is a -.45% discount

Thus GLD allows investors- both retail and institutional alike- unprecedented ease and access to transact in shares with exposure to gold, without going directly through the LBMA and dealing in massive quantities. In essence, these LBMA transactions are still occurring, but are done so by large "Authorized Participants" whose activity of buy/selling gold in the OTC market to create/redeem GLD shares generates themselves a profit and keeps GLD and gold prices in line.

Of course there remain some legitimate concerns about GLD, such as concerns should the custodian go bankrupt. In such case ownership of the physical gold is still legally the Trust's- not the custodian's- but complicated legal battles could cause fees and delays which could at least temporarily disconnect GLD from the value of spot gold. Additionally, destruction/theft of the holdings could occur, but once again there is nothing about this unique to GLD. These are always risks associated with holding physical gold, and a major institution will have more means of readily available security than many investors considering personally holding physical gold. There are tradeoffs to be made either way. When it comes to destruction/theft for GLD, at least the parties with deep pockets are incentivized and responsible to be made whole, another advantage over the independent everyday investor holding physicals. This is particularly true with a number of very wealthy and insitutional investors having no qualms with GLD and who would be on the side of investors to be made whole. So while GLD is absolutely not without its potential faults, based on market structure fundamentals and historical behaviors even during financial crises, these faults may often be overblown.

GLD as a Portion of Gold Market Liquidity

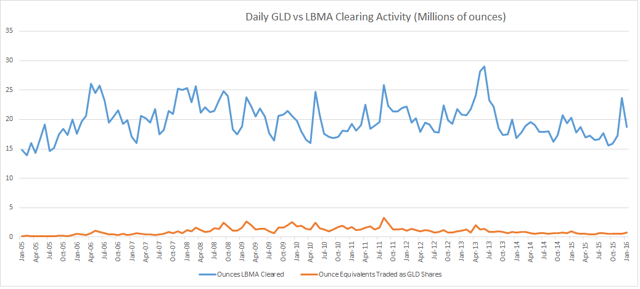

So how does GLD stack up in liquidity terms against the market as a whole? In short, it hardly makes a dent. The chart below is based on actual traded volumes of GLD shares converted to ounce equivalents and LBMA clearing statistics.

Remember, these are the just the clearing figures, about 10% of the probable true level of gold traded in London daily. There is so much gold and money in gold in the physical market that activity in GLD peaked in 2011 at 10% of daily clearing figures, making it roughly the same proportional size as the Shanghai Gold Exchange is today. These days, trading volumes in GLD are back down to around 3-5% that of LBMA clearing figures.

Even GLD's entire gold holdings, currently around 26 million ounces, is hardly more than a single days worth of cleared gold trades on the LBMA, and not much more than 10% of a day's total trading volume. For all the focus directed to GLD and Chinese private investment in gold, it remains pittance to the real markets, something that may come as a surprise to many investors.

Looking Ahead

The developing market trend to watch in global gold markets is how much activity Chinese marketplaces can wrest from London, and how quickly. In the past, premiums on physical gold in Shanghai have led to observed outflows of gold from the West to Shanghai- even from GLD itself as it served as a readily available source of physical gold- as market makers redeemed shares to withdraw gold and sell it at premiums in Shanghai. A degree of perspective matters though, these flows were only a portion of GLD which in turn is only a fraction the liquidity in London. They have not represented a structural shift in marketplace liquidity... yet.

London's grasp goes beyond mere liquidity though as, by means of the LBMA fixing London remains the major source of price discovery liquidity, something China is only beginning to be a part of through Bank of China's inclusion as a member to set the fixing.

Whether you choose to invest in gold markets and how you choose to do it is obviously a subjective decision. Not only are there risks to gold prices, and high transaction costs to trading physical gold for the retail investor, there are risks that gold related instruments like GLD may not behave like the price of gold. No one can deny that these risks exist. But once the facts of how GLD operates, the historical trends, and the fundamental structure of gold markets are examined, some may find the risks associated with GLD are often overblown and easily justified for the ease, cost and convenience it offers. Others will not. As with all investing the important thing is to remain focused on actual data, logic and evidence and stay within your personal risk tolerance and objectives rather than be swayed by fear, greed or any other emotion.

I hope you found this deeper dive into the gold markets and global liquidity insightful. Thanks for reading, and please share your informed thoughts in the comments.

For this article I continued my investigation to take a look at the liquidity and fundamental structure of global gold markets. In doing so I hope to shed some light on topics related to gold and gold related investments that often are taken for granted and not likely to be well understood.

The Structure of Gold Markets

There are a number of marketplaces for gold for both futures and physical gold. The most significant either for their current size or rate of growth are:

- Shanghai Gold Exchange (SGE)

- Shanghai Futures Exchange (SHFE)

- Multi Commodity Exchange of India (MCX)

- Tokyo Commodity Exchange (TOCOM)

- COMEX- Part of the NYMEX and CME Group

- London Bullion Market Association (LBMA)

Sources: COMEX, TOCOM, MCX, SHFE, SGE, LBMA. For those surprised by the relatively small size of Shanghai markets here is a Bloomberg article to triangulate the data (article is from a year ago but serves as a ballpark verification)

The LBMA is an OTC market where gold trades twenty-four hours a day in the same basic manner as the Forex markets: trades occur between two parties and are not standardized nor cleared through an exchange. Because of this- again comparable to the Forex markets- what would be considered even the most basic information for equity markets can be difficult to find for the gold bullion market. Luckily however, there are a few direct sources.

One can think of the LBMA as a network of affiliated and participating global bullion dealers.

While they do not operate on an exchange, there are well established market conventions, including the globally recognized settlement method for gold bullion trades through "LOCO London" accounts which settle in gold holdings held on deposit with LBMA bullion dealers.

The LBMA also has a market standard for the bars of gold themselves- London Good Delivery bars- which are only sourced through a limited number of suppliers associated with the LBMA.

Besides providing liquidity, the LBMA is also known for publishing the gold fix, the widest used benchmark for spot gold prices (when people talk about the price of gold in general, even if they don't realize it, they are referring to the LBMA gold fix). The fix essentially functions as a twice daily auction, with a clearing price being set where the balance of orders clears. Today there are eight member banks which participate in the fixing price process, including recently for the first time a Chinese bank: the Bank of China.

Some but not all OTC transactions clear through the LBMA clearing member banks. Trading parties might choose to go out of their way and clear through these banks if one (or both) are concerned about counter party risk, but otherwise might avoid doing so to save costs and/or to keep their flows hidden. The LBMA reports their clearing statistics on a monthly basis, though the cited figures represent not month totals but the average daily values over the month. For example in January 2016, 18.7 million ounces were cleared daily, but that's not to be confused as the total traded, that's just the subset of activity that was cleared. For data about the total traded amount we have to look to a 2011 liquidity survey published by the LBMA itself. There are various reasons the report may over or under estimate the true figure, but if the report is to be believed, in Q1 2011 the amount of traded gold was 10x the amount actually cleared. To derive the LBMA 2015 volume estimate in the above pie chart that same 10x multiple has been applied to the clearing numbers.

While daily turnover in gold as a percentage of total stocks may sound high, its levels are comparable to that of sovereign debt

You might be wondering how its possible for 45 billion ounces of gold to trade in London yearly, when estimates put the total gold ever mined at about 6 billion ounces. Remember these are volume numbers, with a trade being counted each time ownership of gold changes ones party to another but with no regard to how these changes net against each other. For example, if I sell you a troy ounce and then buy it back from you a week later, that's 2 troy ounces of volume even though there has been no net change in holdings (this is not unique to the LBMA and is equally true of volume traded on all marketplaces so the above pie chart is still an apples-to-apples comparison). The LBMA clearing number itself remains a more indicative figure for the actual net exchange of gold being moved between accounts: a number which typically fluctuates around 20 million ounces/day.

Physical Markets vs Futures Markets

There are in essence two major types of market places, the futures markets (COMEX, SHFE, MCX, TOCOM- and a handful of others that are a very small portion of global liquidity) and physical markets (SGE and LBMA).

In the futures markets contracts trade with fixed specifications for delivery size, date, quality and location. For example 1 COMEX contract is always 100 troy ounces and can be "delivered" or "physically settled" only at the COMEX warehouse itself.

Only a small portion of traded futures contracts are physically settled at the exchange. You can infer this directly yourself simply by looking at the level of trading activity and open interest in the futures contract about to expire directly on the CME's volume page.

For parties who want to take physical delivery, much more common than holding the future contract to expiration is to use something called an 'Exchange for Physical' trade to do so. You can see this activity indicated in the column marked 'EFP' on the CME volume page linked above. An EFP is actually an OTC trade that is cleared through the exchange in which two parties can come to an agreement to swap positions in the futures for physical gold. In essence it works no differently than an OTC trade cleared through the LBMA only at least one party begins with an initial futures position. Here's an example of how it might look:

- I buy 1 COMEX futures gold contract (100 troy ounces).

- I desire to take physical delivery, but don't want my gold at the COMEX warehouse. Let's say I want it in Zurich instead.

- I call you up, and as the top gold dealer in Zurich you quote me an 'EFP' price: the price at which you are willing to sell me 100 troy ounces of physical gold in Zurich and buy 1 COMEX future from me.

- We transact: in one single EFP transaction I both sell my future and buy physical gold, and you both sell physical gold and buy the futures contract from me.

The important take away though is that via EFP trades, futures positions can be converted to equivalent physical trades. Which brings us to the LBMA and SGE markets. Some, perhaps even most, of these EFP trades on the COMEX futures may actually be conducted with LBMA clearing members. Like the futures EFP trades, all trading on the LBMA is OTC, this means there are no standardized contracts and there is no central exchange to absorb counter party risk and facilitate settlement (unless parties clear through the LBMA clearing banks). There are however some market conventions, including that standard dealing amounts in the spot market are 5,000-10,000 ounces in gold.

From the LBMA's 2011 report we know that roughly 90% of trading activity in OTC takes place in the spot market, with the rest being composed of forwards (agreeing to exchange gold at a fixed price at a fixed date in the future) or other transactions including swaps and EFPs.

Because of the large minimums and non-transparent market structure one must realize this is not a market in which small/retail players easily participate. The physical gold markets in the West have long been- and continue to be- markets in which retail flows are laughably small and it is not in the market makers' economic interests to cater to or clear/redeem/manage retail trades in physical gold- they are happy to leave that to the 3rd party dealers who charge investors massive premiums to invest in physical gold. For instance, for market participants on the LBMA typical bid offer spreads are about .04-.07%, or about $.70 if gold is trading at $1,200 per ounce. By comparison, spreads for popular retail gold dealers even when dealing in 10 ounce increments (quite large increments for most retail investors) are around 1.3%- or even significantly higher. In other words retail investors trading physical gold are paying a premium of at best nearly 25x that in spot gold markets, and likely in many cases far worse.

We will discuss GLD much more in a moment- but one can immediately see why instruments like GLD are potentially of value to the retail investor. By allowing authorized participants to redeem shares for gold or create shares by depositing gold for a small fee (rather than GLD being the party which has to go out on the market and pay fees to transact), GLD is- in theory- able to pass on a great deal of savings in the costs incurred in investing in physical gold to its holders while charging a small fee in return.

The SGE is an interesting exception to the non-individual investor market structure model though. Partly because of its much smaller size and much shorter existence, and partly because of China's encouragement of its public's direct investment into gold as a kind of quasi-government reserve, the SGE caters much more to the individual investor.

Individual Chinese citizens can register at a member institution with the SGE and are assigned a ten digit identification code that is permanent and unique to them. They can then deposit gold or cash, transact via the SGE, and withdraw funds or withdraw gold via an authorized vault.

Outside of central bank purchases (another issue entirely) China gold volumes are often overestimated as a portion of the market. Even with tremendous growth in recent years SGE activity is only about 1% of the total gold market activity. Though there are several million individual participants in the SGE, the real money remains with the large institutions which transact on the LBMA.

GLD's Role in the Gold Markets

In late 2004 GLD was created as an option to provide investors with access to hold a paper instrument tied to the value of physical gold, thus in theory allowing for exposure to gold prices with the ease of trading an ETF and without the costs in time and money of holding physical gold itself. GLD aims to do this by owning gold bullion which is held in their name in a vault by a custodian. From GLD's own prospectus:

As at December 31, 2015, the Custodian held 20,691,044 ounces of gold on behalf of the Trust in its vault, 100% of which is allocated gold in the form of London Good Delivery gold bars...For a more up to date tracker SPDR lists daily figures here. Though in the past GLD has drawn the suspicions of some investors who for one reason or another doubt the actual amount of gold being held on behalf of the Trust, as a SEC registered entity that is also independently audited, purposefully misrepresenting these reported figures about how much gold is owned and held on the Trust's behalf would not be so easy done and would have serious ramifications.

While there are some common concerns about GLD- some more valid than others- it is also a unique aspect of the gold markets that is frequently misunderstood and deserves a further examination.

Other than previously amassing the 260,000 ounces of gold held at the time it first began trading, GLD does not buy or sell gold. As of the latest numbers, for each issued share of GLD the Custodian holds about .095586 ounces of gold. The method by which additional shares are created or destroyed is the same method by which additional gold is acquired or disposed of, and it is the same mechanic by which GLD's price remains tied to the spot price of gold.

Once again, as per the GLD prospectus,

The Trust creates and redeems the Shares from time to time, but only in one or more Baskets (a Basket equals a block of 100,000 Shares).At .095586 ounces of gold per share, this represent increments of 9,559 ounces, far too large for the vast majority of retail investors but right in line with sizes LBMA market participants are very comfortable dealing with.

Creations of Baskets may only be made after the requisite gold is deposited in the allocated account of the Trust.In other words, when additional GLD shares are created this is done directly in proportion with additional gold being deposited by the recipient of these new shares. GLD is not buying or selling gold on the open market, and the factor which changes the ounce/share ratio is not the price of GLD per share, the price of gold per ounce, or the amount of creations or redemptions (since each creation and redemption keeps the existing ratio constant), but the fact that GLD sells a small amount of gold to pay for its fees:

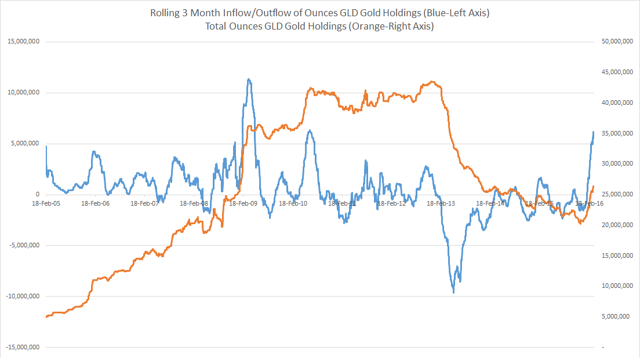

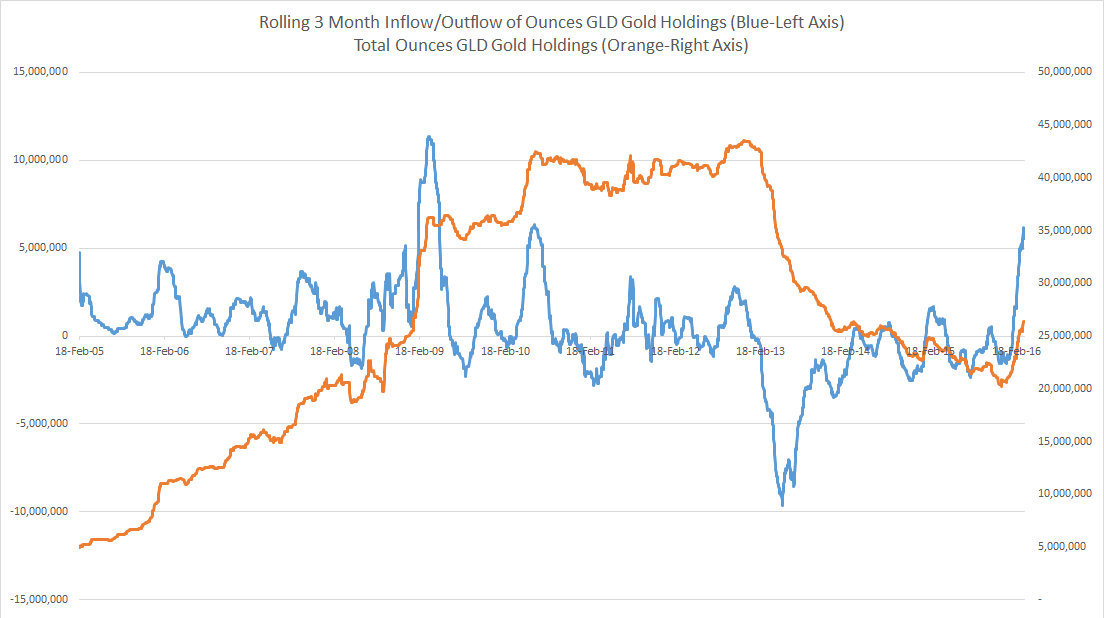

The number of ounces of gold required to create a Basket or to be delivered upon the redemption of a Basket gradually decreases over time, due to the accrual of the Trust's expenses and the sale of the Trust's gold to pay the Trust's expenses.One way to see the creation/redemption process in action is to look at the net flows of gold holdings into/out of the trust. The below chart displays the rolling 3 month change in the level of ounces of physical gold owned by the Trust and held by the custodian. We can see the actual creation/redemption process leading either to the number of shares outstanding falling and gold holdings being withdrawn (outflows), or the number of shares outstanding rise and gold holdings increasing (inflows).

Because of this creation/redemption process and the fact that GLD shares have a gold ounce equivalent, it is no accident or coincidence that GLD's per share price is tied to spot gold prices.

There is a fundamental and often misunderstood mechanic which governs this that relies not on any parties watching out for investor's best interests, but only on the selfish profit-motive interests of a few rich and powerful private parties. Therefore, it is relatively unlikely this relationship should break down outside the most extreme of circumstances. It functions as such:

- Imagine spot gold is trading at $1200 an ounce, but GLD shares are trading at $95.59 per share, or (at .09559 shares per ounce equivalent) $1,000 per ounce.

- Market makers can make a risk-free profit (arbitrage), by buying 100,000 GLD shares on the open market at $95.59 each, redeeming those shares for 9,559 ounces of physical gold, and then selling that physical gold on the open market at $1,200 an ounce.

- Without any risk, they have paid 100,000 shares * $95.59 per share = $9,559,000 and received 9,559 ounces * $1,200 = 11,470,800 for a profit of the difference: $1,911,800.

- In doing so, market makers are buying GLD shares (driving GLD prices up) and selling physical gold (driving gold prices gold). Because this process can be repeated as many times as one likes, eventually GLD prices will be driven up and spot gold prices down so much, that the gap will be closed, at which point it becomes no longer profitable to conduct the trade.

- Because there are multiple parties able to do this who are all competing for profits, there is essentially a bidding war. Whoever is willing to take the smallest profit to do the above will be the first to act, and thus deviations in price are relatively small.

- If GLD shares are trading expensive to spot gold the process simply reverses: market makers capture a profit by buying spot gold, depositing the gold to create new GLD shares, and then they sell those GLD shares on the open market.

Proceeds received by the Trust from the issuance and sale of Baskets consist of gold and, possibly from time to time, cash. Pursuant to the Trust Indenture, during the life of the Trust the gold and any cash will only be (1) held by the Trust, (2) distributed to Authorized Participants in connection with the redemption of Baskets or (3) sold or disbursed as needed to pay the Trust's ongoing expenses.This qualification of 'Authorized Participants' sometimes worries investors less familiar with the creation/redemption process for ETFs. It is absolutely true that only a few 'Authorized Participants'- or 3rd parties who come to terms with Authorized Participants- can create/redeem shares and complete the arbitrage process outlined above. Yet there are two main reasons that fears about this point, while valid in some small part, are none-the-less often overstated:

- There is absolutely nothing unique to GLD about only 'Authorized Participants' being able to create/redeem shares

- Some investors discuss the 'authorized participants' stipulation as if it is only GLD which has this restriction. Yet in truth it would be far stranger if GLD did not have this in restriction in place. Dealing with a large number of small transactions with unknown counterparties is neither cost nor time effective- nor is it in the best interests of any involved parties including GLD and its holders themselves to do so since in one way or another these costs are passed onto holders of shares in the Trust. Restricting transactions to known counterparties of sufficient monetary resources is standard business practice for ETFs. For instance, the massively popular S&P 500 ETF, SPY, has the exact same requirements listed in its own prospectus: "Investors must accumulate enough Units in the secondary market to constitute a Creation Unit in order to have such Units redeemed by the Trust, and Units may be redeemed only by or through an Authorized Participant."

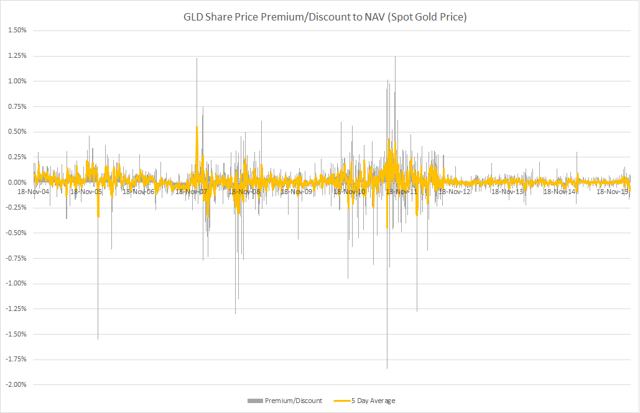

In order to redeem SPY shares for the actual shares of the index member companies, one must be an Authorized Participant for SPY, just as to redeem GLD shares for the actual ounces of gold one must also be an Authorized Participant for GLD. - Authorized participants are more than adequate to keep GLD prices tied to gold- they have the deepest pockets and lowest transaction costs. In addition to avoiding unnecessary higher costs of dealing with smaller and unknown parties for creation/redemption, there is also little benefit to dealing with additional parties. If authorized participants were not sufficient at tying the price of GLD shares to the price of gold, there would be large and regular discrepancies in price which would show up in the shares' premium or discount to NAV, since NAV is based directly on spot price gold. Yet as the below chart indicates, this simply is not the case, and was not even the case during 2008 in the largest financial crisis and meltdown markets have seen for multiple decades. Authorized participants are the most qualified parties to keep prices tied together precisely because they have the deepest pockets to do so, and are incentivized to do so with profits from arbitrage.

Historically premiums and discounts have not existed for prolonged periods and have been generally within +/- .25% even during times of financial crisis. Over the entire life of the fund the 99th percentile of daily discount/premiums is a .37% premium and the 1st percentile is a -.45% discount

Thus GLD allows investors- both retail and institutional alike- unprecedented ease and access to transact in shares with exposure to gold, without going directly through the LBMA and dealing in massive quantities. In essence, these LBMA transactions are still occurring, but are done so by large "Authorized Participants" whose activity of buy/selling gold in the OTC market to create/redeem GLD shares generates themselves a profit and keeps GLD and gold prices in line.

Of course there remain some legitimate concerns about GLD, such as concerns should the custodian go bankrupt. In such case ownership of the physical gold is still legally the Trust's- not the custodian's- but complicated legal battles could cause fees and delays which could at least temporarily disconnect GLD from the value of spot gold. Additionally, destruction/theft of the holdings could occur, but once again there is nothing about this unique to GLD. These are always risks associated with holding physical gold, and a major institution will have more means of readily available security than many investors considering personally holding physical gold. There are tradeoffs to be made either way. When it comes to destruction/theft for GLD, at least the parties with deep pockets are incentivized and responsible to be made whole, another advantage over the independent everyday investor holding physicals. This is particularly true with a number of very wealthy and insitutional investors having no qualms with GLD and who would be on the side of investors to be made whole. So while GLD is absolutely not without its potential faults, based on market structure fundamentals and historical behaviors even during financial crises, these faults may often be overblown.

GLD as a Portion of Gold Market Liquidity

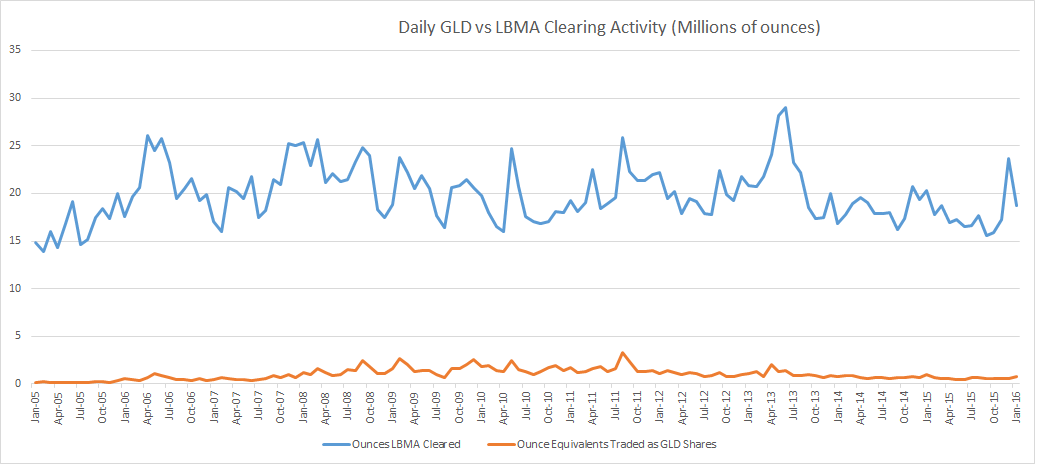

So how does GLD stack up in liquidity terms against the market as a whole? In short, it hardly makes a dent. The chart below is based on actual traded volumes of GLD shares converted to ounce equivalents and LBMA clearing statistics.

Remember, these are the just the clearing figures, about 10% of the probable true level of gold traded in London daily. There is so much gold and money in gold in the physical market that activity in GLD peaked in 2011 at 10% of daily clearing figures, making it roughly the same proportional size as the Shanghai Gold Exchange is today. These days, trading volumes in GLD are back down to around 3-5% that of LBMA clearing figures.

Even GLD's entire gold holdings, currently around 26 million ounces, is hardly more than a single days worth of cleared gold trades on the LBMA, and not much more than 10% of a day's total trading volume. For all the focus directed to GLD and Chinese private investment in gold, it remains pittance to the real markets, something that may come as a surprise to many investors.

Looking Ahead

The developing market trend to watch in global gold markets is how much activity Chinese marketplaces can wrest from London, and how quickly. In the past, premiums on physical gold in Shanghai have led to observed outflows of gold from the West to Shanghai- even from GLD itself as it served as a readily available source of physical gold- as market makers redeemed shares to withdraw gold and sell it at premiums in Shanghai. A degree of perspective matters though, these flows were only a portion of GLD which in turn is only a fraction the liquidity in London. They have not represented a structural shift in marketplace liquidity... yet.

London's grasp goes beyond mere liquidity though as, by means of the LBMA fixing London remains the major source of price discovery liquidity, something China is only beginning to be a part of through Bank of China's inclusion as a member to set the fixing.

Whether you choose to invest in gold markets and how you choose to do it is obviously a subjective decision. Not only are there risks to gold prices, and high transaction costs to trading physical gold for the retail investor, there are risks that gold related instruments like GLD may not behave like the price of gold. No one can deny that these risks exist. But once the facts of how GLD operates, the historical trends, and the fundamental structure of gold markets are examined, some may find the risks associated with GLD are often overblown and easily justified for the ease, cost and convenience it offers. Others will not. As with all investing the important thing is to remain focused on actual data, logic and evidence and stay within your personal risk tolerance and objectives rather than be swayed by fear, greed or any other emotion.

I hope you found this deeper dive into the gold markets and global liquidity insightful. Thanks for reading, and please share your informed thoughts in the comments.

0 comments:

Publicar un comentario