Flawed Assumptions and Grand Experiments

John Mauldin

Over the last few years, I have from time to time had the real pleasure of being in the presence of Lakshman Achuthan, Chief Operations Officer for the Economic Cycle Research Institute, a rather serious team of economists who spend their time researching economic cycles, especially those around recessions. They are known for having forward-looking models rather than always looking in the rearview mirror.

Every time I get around Lakshman I walk away impressed. And I always make a mental note to myself that I need to invite him to speak at my conference – but then manage to file that note somewhere where it doesn’t come up when I’m putting the speakers together. If I post this note in front of 1 million of my closest friends, maybe I’ll remember it for 2017.

Lakshman sent me the speech he presented at the 25th Annual Hyman Minsky Conference, and he has graciously allowed me to share it with you as this week’s Outside the Box.

One point he makes strongly in the initial part of his presentation is the readily observable fact that each recovery since World War II has been a little bit weaker.

And that gives me pause, because that means that after the next recession the recovery will be even more anemic than the current one has been. Thus, absent any significant policy change – and by that I most definitely do not mean the Fed’s giving us more of the same; I mean a clear-cut change in the philosophical drivers of the policy – the US economy is going to look more and more like the Japanese economy.

And that gives me pause, because that means that after the next recession the recovery will be even more anemic than the current one has been. Thus, absent any significant policy change – and by that I most definitely do not mean the Fed’s giving us more of the same; I mean a clear-cut change in the philosophical drivers of the policy – the US economy is going to look more and more like the Japanese economy.

Not that Japan is a bad place to live. Most Japanese have a relatively high standard of living, and life goes on – there’s just not a great deal of growth and all the wonderful things that happen along with that growth. So instead of actually growing its economy, Japan has piled up a huge mountain of debt, prone to unpredictable “landslides.”

I have been saying for years that the Federal Reserve is using the US economy as a big test lab for their monetary theories. This is unlike going to the doctor, where there is generally a prescribed treatment for the problem you have. The Fed is experimenting without understanding the full consequences, let alone the unintended consequences, of their policies. In the piece that follows, Lakshman very effectively criticizes not only the Fed but central banks in general for their false assumptions and grand experiments. This is a growing theme. Even Nobel laureate Joseph Stiglitz, with whose policy recommendations I frequently disagree, jumped on the bandwagon this week at Project Syndicate with a serious smackdown of the Fed, suggesting they have no idea how to create a model for the economy, and that to pretend they can create one and then prescribe policies based on it is folly.

I feel like I’m being mentally and psychologically whipsawed as I swing back and forth from looking at today’s economy to working on a book about what the world will look like in 20 years. There are many aspects of our lives that will get so much brighter – well, except for the economic part. But I think we’ll manage to work through the worst of the crisis in the middle of the next decade and can then get back to the serious business of growing our economy in a more or less normal fashion – in a world that will be anything but.

I went to the eye doctor yesterday, simply wanting to a new prescription for my reading glasses. I hadn’t been in, oh, maybe a decade. They did the usual full range of tests on me; and then when the doctor finally walked in and found that I just needed glasses and was thinking about having another round of Lasik surgery, he stopped me. “You don’t want just reading glasses,” he pronounced. “The prescription I’ve given you can be used just for reading glasses, but you probably want to get a pair of glasses you can wear all the time. And I don’t think you should get LASIK today, because your eyes are still pretty much within range; and in five years we’ll have a new technique that’s been developed in Europe that will allow us to put a lens in your eyes and then do the LASIK directly on the [I assume plastic] lens; and then if you ever need to have further work done, you can come in and we can work on that lens again.”

Wow, I just have to wait for the FDA to get around to approving something that is already available in Europe, and then I can have 20/20 vision for the rest of my life! Sounds like a major improvement to me. And there are literally hundreds of similar things in the works that will arrive in just the next 5 to 10 years. When you go out past 10 or 15 years, it truly gets amazing.

All that being said, I wonder what a slow-growth world, with the continuing technological overtake of many jobs that can be automated, will mean to the younger generation. And then I read this week about the disparity between the lifespans of the rich and poor, with the oddity thrown in that the poor in inner cities like Los Angeles live almost as long as the rich in those cities, which tells me that longevity is about more than just access to healthcare. The researchers are just scratching their heads; they can’t figure it out either. Life is just one puzzle after another. You have a great week.

Your trying to solve a 10,000-piece puzzle analyst,

John Mauldin, Editor

Outside the Box

Flawed Assumptions and Grand Experiments

By Lakshman Achuthan

Presented to the 25th Annual Hyman P. Minsky Conference, April 2016

Presented to the 25th Annual Hyman P. Minsky Conference, April 2016

This year began with recession fears throwing a

spotlight on the elephant in the room. As the cover of The Economist put it a few

weeks back – central banks may be out of ammo to fight recession.

How and why did we get here?

As students of the business cycle we have a

perspective that is different from that of most mainstream economists. Because

of our focus on cycles, we have a good handle on what is cyclical and, by

elimination, what is not.

This is why, back in the summer of 2008,

pre-Lehman, we were able to first identify the long-term pattern of weaker and

weaker growth during successive expansions, stretching back to the 1970s. In

fact, Eduardo, your New York

Times colleague Floyd Norris wrote about our findings at the time.

In April 2009, in the depths of the Great

Recession, the talk at the London G20 conference was all about Depression, but

that same month ECRI predicted that the U.S. recession would end by the summer

of 2009. And so it did.

By early 2010, the reality of the new expansion

had engendered expectations of a V-shaped recovery, given the depth of the

downturn. As I recall, there was much talk of the so-called “Zarnowitz Rule”

invoked by the IMF’s late Michael Mussa, to the effect that the deeper the

recession, the stronger the initial stage of the revival.

Wouldn’t you know it, that quickly got simplified

to: “the deeper the recession, the stronger the revival,” dropping the key

qualifier “initial stage.”

Perhaps this simplified version gained so much

traction because it fit well with Milton Friedman’s plucking model, where he

envisioned output as a string attached to an upwardly sloping ceiling, being

occasionally plucked down by recessionary shocks; following which the string

snaps back to the upwardly sloping ceiling, again in line with the simplified

Zarnowitz rule.

The gap between these flawed expectations of

revival and the reality of growth slumping in the so-called “recovery summer”

of 2010 supported the case for what became a Grand Experiment, starting with

QE2 that fall, intended to boost the economy to “escape velocity;” in other

words, to boost the economy to a self-sustaining course, back to “business as

usual,” with long-term trend growth around 3%.

But instead of questioning those assumptions, after

years of zero interest rate policy (ZIRP) and quantitative easing (QE) failing

to achieve that objective, the Fed and other central banks kept doubling down.

So, let’s examine the assumption, is there any

relationship between the severity of a recession and the strength of the

subsequent revival?

At last year’s Minsky conference, I showed that

the conclusion we had first reached in the spring of 2009 had been vindicated.

Meaning that the first year of recovery from the Great Recession was pretty

much in line with historical experience, while, as for the rest of the

expansion, the business cycle owed us nothing more.

Let’s look at the evidence.

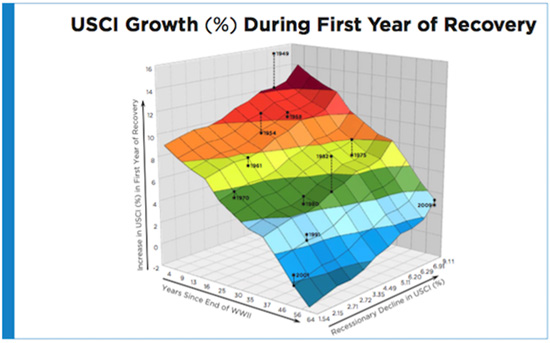

This is a regression surface that supports the

idea that the strength of the first

year of revival depends on the depth of the recession, which is

what Zarnowitz and Mussa meant, before their words were taken out of context.

The chart also shows something further. The

strength of the first year of revivals has been declining over the decades. We

use the analogy of a rubber ball that gradually loses its elasticity over the

decades. Like that rubber ball, the economy still bounces back stronger in the

initial period following deeper recessions, but with its elasticity gradually

declining, the strength of the first year rebound is diminishing over time.

The chart shows two independent variables – the

time elapsed since World War II (left horizontal axis) and the depth of

recession (right horizontal axis). Here we use a broad measure of U.S. economic

activity, which is ECRI’s U.S. Coincident Index, subsuming the aggregate

measures of output, employment income and sales.

The dependent variable is USCI growth in the first

year of economic recovery (vertical axis). The relationship among these

variables is statistically significant and explains three-quarters of the

variance in the strength of the recovery in the first year of recovery.

The regression surface slopes downward on the left

side, showing that, as years pass, the rate of growth in the first year of

expansion declines. The ball becomes less bouncy, so to speak.

The upward slope on the right side shows that,

when recessions are deeper, you then see a stronger rebound in the first year

of expansion.

The stars mark the actual strength of revival in

the first year of recovery, and the dots on the regression surface mark the

corresponding regression estimates.

I would encourage everybody to look at this chart

more closely later on, but let’s highlight the first year of recovery following

the recession that ended in 2009... where you can see that if we’d had that

severe a recession in the late 1940s, we would have expected a rebound on the

order of 14%, up here.

Also, it’s only because the recession was so

severe – all the way back here – that we managed a rebound over 3%. In other

words, if the recession had been half as deep, the expected rebound would be

less than 1% in the first year in terms of USCI growth.

At the end of the day, this chart tells us that

the size of the V-shaped recovery in the first year of revival is linked to

both the depth of the recession and the passage of time, a proxy for structural

change, which we will soon touch on.

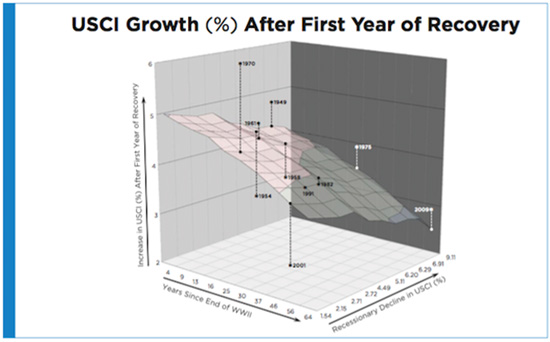

However, following the first year of recovery,

it’s a different picture.

This chart is very similar to the previous one,

with the same independent variables: the passage of time and the depth of

recession.

The crucial difference is that the dependent

variable on the vertical axis is the average pace of growth during the

expansion following the first

year of recovery.

Notably, in sharp contrast to the results shown in

the previous chart, this relationship is not statistically significant, which

is why we faded out the colors.

If anything, to the extent that there is any loose

relationship, it is the opposite of what one might expect.

While the slope of the regression surface along

the left horizontal axis is still downward-sloping, the one along the right

horizontal axis is now also downward-sloping. This suggests that deeper

recessions may actually be associated with more sluggish economic growth

following the first year of revival.

That observation flies in the face of how most

people believe the economy “should” perform, but deeper recessions are

sometimes followed by weaker growth after the first year of expansion.

Basically, there is no real relationship here.

After the first year of recovery the pace of growth has little to do with the

depth of the earlier recession.

To be clear, we are not suggesting that this is a

model anybody should use to design policy.

The point is that the evidence raises considerable

doubt that, beyond the first year of revival, V-shaped recoveries repair the

damage done by deep recessions.

Furthermore, the real issue remains the long-term

decline in trend growth, which even extraordinary monetary policy efforts

cannot change.

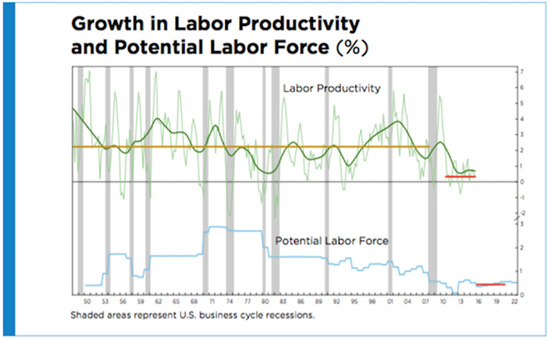

Last June, we underscored the simple math

underlying the decline in trend growth.

As you know, labor productivity growth and

potential labor force growth add up to potential GDP growth.

The Congressional Budget Office now pegs potential

labor force growth at 0.4% a year for the next five years, and that’s pretty

much set in stone. You see it here as the horizontal red line in the bottom

panel of the chart.

Meanwhile, productivity growth has averaged 0.4% a

year for the last five years, shown by the horizontal red line in the upper

panel. In the words of Fed Vice Chairman Stanley Fischer, it “has stayed way,

way down.”

As to where it’s going from here, Cleveland Fed

President Loretta Mester thinks it will revert to its post-WWII average of

around 2¼ percent, shown by the horizontal gold line.

Yet Mr. Fischer noted that “productivity is

extremely difficult to predict,” and only went as far as to say that it “will perhaps eventually return” to

its earlier pace (italics ours).

But if things stay around where there are, we’re

looking at 0.4% productivity growth plus 0.4% potential labor force growth,

adding up to 0.8% longer-term real GDP growth.

Potential labor force growth is just about

demographics. But if you dig into what’s driving this drop in productivity

growth, you find something interesting.

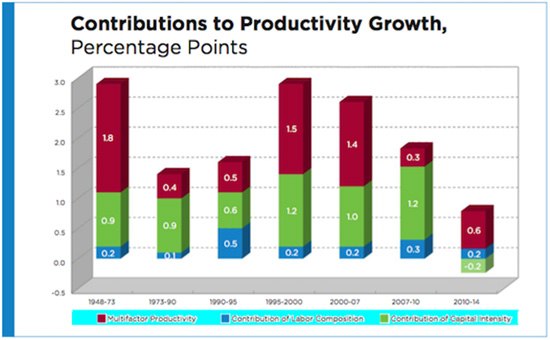

This chart shows that there has been a steady fall

in labor productivity growth and a noticeable shift in its sources of growth

over the years.

But, eyeballing the previous chart, it looks like

the post-World War II history of productivity growth has unfolded over several

phases. So it’s instructive to break up the period judgmentally, starting with the

initial 1948-73 period of relatively strong productivity growth, followed by a

slump that lasted until the early 1990s, and so on, and ending with the period

following the Great Recession and its immediate aftermath.

It is instructive to break out labor productivity

growth into growth in labor composition (the quality of labor); capital

intensity (the ratio of capital to hours worked); and multifactor productivity,

a measure of the combined influences of technological change, higher

efficiency, returns to scale, reallocation of resources, and other factors

affecting economic growth, over and above the individual effects of capital and

labor.

From 1948 to 1973, a period that saw labor

productivity growth average almost 3% per year (first bar), multifactor

productivity (red portion of bar) was the overwhelming driver of labor

productivity growth, followed by capital intensity (green portion of bar).

The contribution of multifactor productivity then

collapsed, causing labor productivity growth to fall by about half to 1½% per

year between 1973 and 1995 (second and third bars), but then rebound between

1995 and 2007 (fourth and fifth bars), basically remaining robust until the eve

of the Great Recession.

What jumps out is the period following the initial

recovery from the Great Recession (rightmost bar), where the contribution of

capital intensity went negative, after being in the ballpark of 1%, give or

take, in the entire post-war period.

So while multifactor productivity and labor

composition have been making modestly positive contributions in recent years,

that of capital intensity has turned negative despite cheap money and the

average age of private nonresidential fixed assets being near a half-century

high.

Please recall that the ratio of capital to hours

worked defines capital intensity. What’s happened is that economic growth, such

as it is, has been skewed toward growth in the number of hours worked, largely

in lower-wage service sector jobs, while capital investment has taken a huge

hit.

Basically, without a revival in capital

investment, we are unlikely to see much of a recovery in labor productivity

growth.

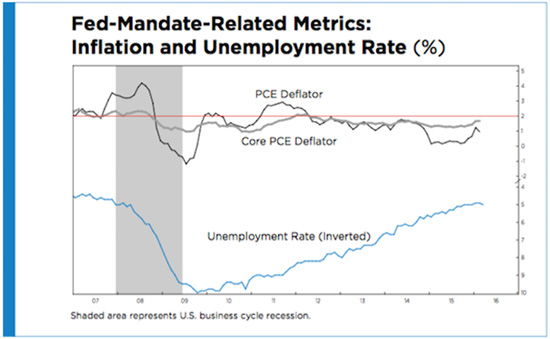

But notwithstanding this long-term structural

problem, the Fed is pretty close to meeting its dual mandate, right?

As we know, the unemployment rate has been falling

steadily for years, and is now practically at the Fed’s shrinking estimate of

the non-accelerating inflation rate of unemployment (NAIRU).

And inflation, including, in particular, the core

PCE deflator, is pretty close to the Fed’s 2% target. And yet the Fed seems

pretty “dovish.”

So what’s the problem?

One could argue that it’s what has effectively

become the Fed’s third mandate…

I don’t think it’s news to anyone that every time

the market has faltered following the financial crisis, the Fed has turned

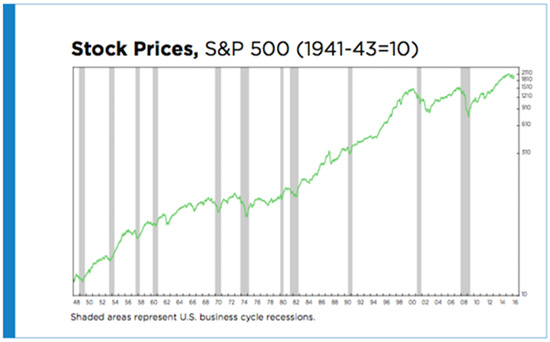

“dovish” in some way, shape or form. This chart suggests why that may be.

Perhaps it’s because the recessionary bear markets

in the 21st century, around the 2001 and 2007-09 recessions, are

bigger than any other post-World War II bear market.

If the Fed really does consider avoiding a major

bear market to be part of its informal mandate, you can understand why a

recession must now be avoided at any cost.

Or perhaps it’s not about “us,” but rather about

“them,” meaning it’s all about global growth, given that the word “global” was

mentioned 22 times in the latest Fed minutes.

If it’s global growth that’s the problem, ECRI’s

view has been for a while that we are in a global slowdown that will continue

for the foreseeable future, so it’s hard to see those concerns receding in

short order.

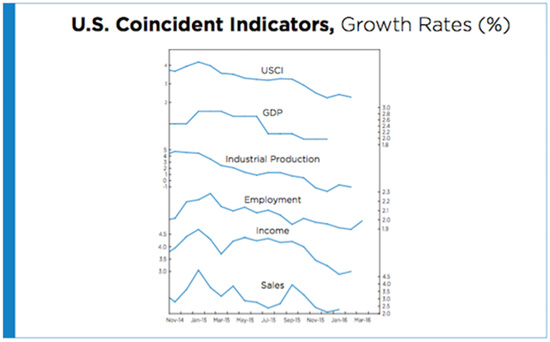

But for over a year, ECRI has argued that this is

about the U.S. economic cycle.

Sure we’ve seen relatively decent job growth. But

year-over-year (yoy) growth in nonfarm payroll jobs has been trending down

since early 2015.

And, as you see, so has GDP growth, even without

Q1 data.

Meanwhile, yoy industrial production growth is

also trending down, and remains near a six-year low.

You can see similar downtrends in yoy income and

sales growth, which are around 1½- and 2-year lows, respectively.

That’s why growth in the U.S. Coincident Index

(USCI) has been falling rather steadily since the start of 2015, and is now

hovering near a 2-year low. By the way, this is the same measure of economic

growth used in the earlier regressions.

These concerted declines in output, employment,

income and sales growth, resulting in a USCI growth downturn, constitute the

hallmark of a growth rate cycle downturn, meaning a full-blown cyclical

slowdown, on top of the long-term structural decline in trend growth.

Understanding this, we warned last summer that the

Fed’s rate hike plans were on a collision course with the economic cycle.

So the Fed started its rate hike cycle a year

inside a growth rate cycle downturn, something it has never done before. This

may be why the Fed is having trouble following through on its rate hike plans,

even though its dual mandates have essentially been met.

Under these circumstances, can the Fed hike rates

much further?

In fact, will they actually have to backtrack and

cut rates the way the European Central Bank (ECB) did in 2011?

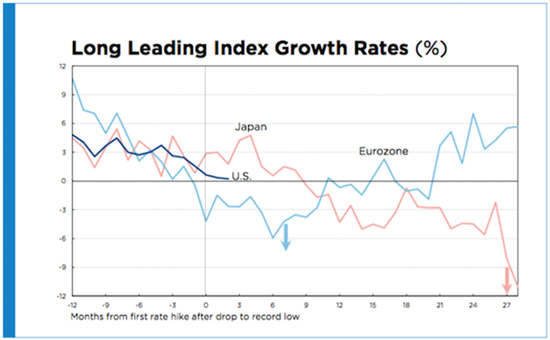

Let’s look at the circumstances under which the

ECB and the Bank of Japan (BoJ) reversed their last rate hike cycles, in terms

of ECRI’s Eurozone and Japanese Long Leading Index growth rates.

The light blue line is the growth rate of ECRI’s

Eurozone Long Leading Index, and the vertical black line shows where the ECB

started hiking rates in 2011.

The blue down arrow shows where they had to

reverse course and cut rates just seven months later, after Eurozone Long

Leading Index growth had plunged deep into negative territory.

The red line shows Japanese Long Leading Index

growth, beginning in the mid-2000s, and the vertical black line once again

shows where the BoJ started hiking rates in 2006.

Japanese Long Leading Index growth actually

improved for a bit, before starting to sink, and it was not until 27 months

after the first rate hike that the BoJ reversed course and cut, as shown by the

red arrow, following a plunge in Japanese Long Leading Index growth.

Now, the shorter, dark blue line shows current

U.S. Long Leading Index growth, with the black vertical line marking off the

timing of the Fed’s December 2015 rate hike.

It’s interesting to see that it’s right in-between

the other two, and while we’ll have to wait and see how it evolves, the chart

suggests a reasonable chance that the Fed will find itself backtracking. But

what does that look like if you’re out of ammo?

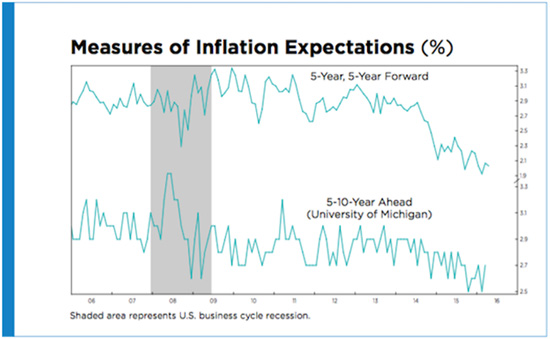

The point is that, for central banks in general,

credibility is the most important asset, and even for the Fed, this next chart

raises questions.

Here we have both the market-based and

survey-based five-to-ten-year-ahead inflation expectations hovering around

record lows.

It is notable that these numbers are much lower

than during the Great Recession, but what’s remarkable is how much they’ve

dropped since 2014.

This is about the Fed’s credibility in keeping

inflation around its target, not in the next few years, but in the next decade.

To cite St. Louis Fed President Jim Bullard, these inflation expectations are

“a rough measure of Fed credibility with respect to its 2% inflation target.”

Yes, there’s been a good correlation between crude oil prices and 5-year,

5-year forward inflation expectations, but it may have persisted for a reason.

It may be because a plunging oil price could threaten lenders to energy

producers and jeopardize the financial system. Simultaneously, falling oil

prices may be seen as a symptom of rising recession risk, while also increasing

the probability of deflation that naturally boosts real interest rates,

stymieing the Fed and making monetary policy less potent. Of course, anytime

the Fed’s perceived impotence increases, so does the disbelief in its ability

to meet its inflation target, even in the longer run.

And this is not just about the Fed, which

undertook a Grand Experiment of an extended ZIRP and QE. There are actually

three grand experiments that are too big to fail, and yet they are at risk of

failing.

Following the Global Financial Crisis, China

launched not only massive monetary easing, but truly colossal fiscal stimulus

that included pouring nearly one and a half times as much concrete in the three

years ending in 2013 as the U.S. had in the entire 20th century. The

resource bust that followed has sent deflationary shockwaves around the globe,

and the repercussions are not over yet.

Years of robust growth had fostered the belief

that China was led by infallible technocrats who always knew what levers to

pull, and when. But their handling of the stock market crash and exchange rate

volatility since last summer undermined confidence in China’s ability to pull

off a tricky transition to a consumer-driven economy, even though they’ve

calmed market jitters for the moment. Please recall, the latest Fed minutes

mentioned the word “global” 22 times.

We’ve talked about the Fed’s predicament, but the

real issue is the fear that, in the event of another recession, the U.S. will

essentially “become Japan.” Hence the concern about falling long-term inflation

expectations.

But if you do “become Japan,” Abenomics was

supposed to be the way out. Yet after three years, Abenomics is clearly

failing, with GDP falling in five of the 12 quarters since its launch. Two

years ago, Japan had its fourth full-blown recession since 2008, and last year

it had negative GDP growth in two of four quarters. Looking ahead, we’re

monitoring the risk of yet another Japanese recession in 2016, which would be a

deathblow to Abenomics.

This is quite a global predicament to be in after

years of unprecedented stimulus.

In the summer of 2008, before Lehman blew up and

many years before the secular stagnation debate, we showed that the pace of

expansions had been stair-stepping down since the 1970s.

We’ve also shown why the case for a strong

recovery beyond the first year following a deep recession is not supported by

the evidence, as we had originally concluded way back in 2009.

Therefore, the discourse among policymakers,

trying to explain their disappointment and prescribe additional solutions, has

been based largely on flawed assumptions that trend growth was actually higher

than it’s turned out to be, and that we were somehow owed a return to that

long-term trend.

As a result, policy initiatives designed to blast

the economy toward “escape velocity” wound up being not only misguided, but

also futile.

As Sherlock Holmes observed in “A Scandal in

Bohemia,” “It is a capital mistake to theorize before one has data. Insensibly

one begins to twist facts to suit theories, instead of theories to suit

facts.”

We would submit that the first step in correcting

this mistake is to restart the theorizing from a closer look at the evidence.

And we would also heed the advice of another

well-known investigator. Carl Sagan used to say that “extraordinary claims

require extraordinary evidence.”

Similarly, if you’re going to embark on Grand

Experiments, you’d better make sure that your assumptions are rock-solid. But

as we’ve shown, there should have been serious doubts about some key

assumptions underlying central bank policy.

Ultimately, only policies that genuinely address

the challenges of demographics and productivity have a chance to succeed.

Meanwhile, the notion that the Fed can indefinitely forestall the 48th

recession in U.S. history remains wishful thinking.

0 comments:

Publicar un comentario