Emerging Markets in the Sweet Spot: Can It Last?

Emerging markets are back in vogue, but investors’ newfound enthusiasm has some weak spots

By Richard Barley

Emerging-market investors have finally caught a break. Currencies, bonds and stocks have rallied; money has been flowing in. But some of the foundations for optimism are fragile.

The sighs of relief from fund managers are justifiable. Pessimism on the asset class had been overdone, and emerging markets have got some of their mojo back. Year to date, the MSCI Emerging Market index is up 2.4%, outpacing the developed-market World index, down 2.7%.

Exchange rates have rebounded, with the Brazilian real up 7.6% against the dollar, the Russian ruble up 6.4% and the Turkish lira up 2.4%. Local-currency and dollar-denominated emerging-market bonds have gained.

In March, portfolio flows into emerging markets hit a 21-month high at $36.8 billion, the Institute of International Finance estimates. J.P. Morgan says investors added the most to positions in local-currency bonds and emerging-market foreign exchange since it started surveying them in 2001.

But a chunk of this welcome relief has come about because of central-bank actions in developed markets, and in particular the apparent unwillingness of the U.S. Federal Reserve to raise interest rates by as much as feared. A weaker dollar has generated breathing space. Looser U.S. monetary policy relative to expectations gives emerging-market central bankers additional room for maneuver as the downward pressure on their currencies eases.

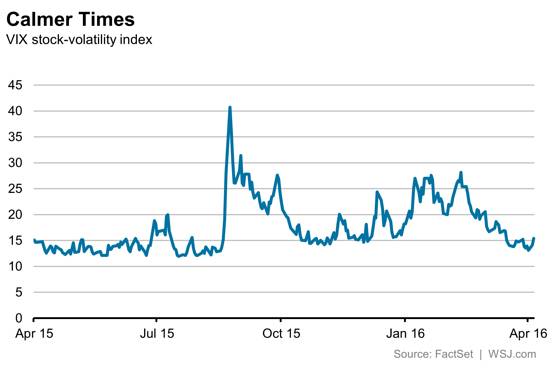

The monetary-policy detente has also smoothed the path of markets, encouraging risk appetite. The VIX stock-volatility index last week reached a low not seen since mid-2015, before China’s botched currency shift sparked panic among investors. But to the extent monetary policy is once again suppressing volatility, it is simply delaying the day of reckoning.

Emerging markets aren’t relying entirely on the kindness of strangers. Fears of a Chinese devaluation have eased, with some clearer communication from policy makers. Investors are hoping for political change in Brazil as President Dilma Rousseff’s government teeters. Russia, although damaged by generating geopolitical instability, has won confidence from investors for its handling of the oil-price shock. And in the coming months, the focus of worries for global investors may move back to Europe. Greece is edging back onto the agenda, and the U.K.’s European Union vote is also causing jitters. Emerging markets might benefit from not topping the list of investor concerns.

But for a true recovery in emerging markets, investors will need to see greater evidence of sustainable growth and reform. To the extent that this latest shift is as a result of adjustments in global exchange rates and U.S. interest-rate expectations, it is vulnerable to a reversal. Even an acceleration in U.S. growth can become a problem: it will probably lead markets to tighten global financial conditions in anticipation of a less accommodative tone from the Fed.

A world in which a stronger U.S. recovery is a worry is one that doesn’t inspire lasting confidence that emerging markets are fully out of the woods. The sweet spot can’t last forever.

0 comments:

Publicar un comentario