Deflation: The New Normal?

by: Matt R O'Connor

- Inflation remains a short- to mid-term possibility, but longer term trends suggest deflation may be the real threat to the global economy.

- In developed economies, growth is primarily driven by spending, which in turn is driven by credit growth and to a lesser extent, productivity.

- Demographics suggest slower rates of credit growth in the long term, resulting in deflationary pressures.

- Technology has reached or is nearing an inflection point that will act as a major source of deflation.

- What a multi-decade period of global deflation would mean for investors.

- In developed economies, growth is primarily driven by spending, which in turn is driven by credit growth and to a lesser extent, productivity.

- Demographics suggest slower rates of credit growth in the long term, resulting in deflationary pressures.

- Technology has reached or is nearing an inflection point that will act as a major source of deflation.

- What a multi-decade period of global deflation would mean for investors.

In a previous article, 'Inflation: The Beast in the Cage', we discussed how central banks around the world are actively manufacturing inflation in the hopes of countering prevailing deflationary global economic headwinds. Based on the comments from readers, it appears many investors were surprised that the normal state of affairs in the last few years has been too much deflation rather than too much inflation, and that the motives the Fed and central banks have for purposefully trying to create inflation are not well understood. While some investors focus on central bankers' actions and policies in a vacuum - taken on their own QE and low interest rate policies are of course inflationary - global markets do not operate in such an environment. A singular focus on monetary policy has been a large reason those investors calling for runaway inflation and skyrocketing gold prices have been surprised for the last several years. In this article, we'll look at the broader and longer-term global picture specifically with regards to the implications for interest rates and inflation. As we'll see, it may continue to pay to remain in longer duration U.S. treasuries and the widely popular iShares 20+ Year Treasury Bond ETF (NYSEARCA:TLT).

To be clear, as outlined in my previous article, higher than desired inflation for the immediate future remains a possibility, in no small part thanks to the actions of central banks, but those actions must be considered in their broader contexts. What many investors do not realize - or do not actively think about - is that for the last several years the 'natural state' of the global economy has been one of deflation. The main reason for this is simple: economic recessions and debt deleveragings are - all else equal - naturally deflationary. Why? Well, in both an economic recession and a time of overall debt levels coming down (a deleveraging), borrowing and credit growth decline as lenders become more wary about borrowers' ability to repay debts and borrowers lose jobs and income and become less qualified to take on debts. This shrinking of the ease and availability of credit in turn leads to decreased spending. Decreased spending leads to lower revenues and earnings, and as companies struggle to stay competitive and afloat in these conditions they repeatedly slash prices, i.e. deflation.

Thus, the natural deflationary tendency of global markets in recent years has 'absorbed' much of the effect of central banks' inflationary policies, which was their goal all along - counter the prevailing deflationary economic conditions. Central bankers are so terrified about deflation because - as you may already have inferred - a deflationary cycle quickly becomes self reinforcing as less credit means less spending, which leads to falling company revenues and earnings, inducing wage cuts and layoffs, which in turn means even less credit and even less spending... and so on. Not pretty.

While I still stand by what I concluded in my previous article: that in the short to medium term, we may either see a crisis of faith in central banks, and/or an unintended but rapid rise in inflation, the longer-term market dynamics point towards something quite different and perhaps all the more menacing: a growing prevalence of deflation.

Credit and The Economy

In a consumer economy - such as those of the U.S. and most developed or first world countries, and what China is currently trying to transition into - spending is arguably the single most important driver of economic growth.

That's because rising spending creates a self reinforcing effect of growth, in the same way falling spending in a deleveraging leads to a self reinforcing contraction. All else equal - increased spending leads to higher revenues and higher profits for companies, meaning higher wages and/or increased employment, meaning higher aggregate income levels, which means higher disposable income and increased spending... and so on.

Thus, roughly speaking, the trend in spending itself steers the overall direction of the economy. Spending money can come from two possible sources:

Thus, the rate of credit growth or contraction directly impacts spending, which in turn directly impacts the rate of economic growth. It follows then to examine the prospects for long-term credit growth to get an idea for economic growth in the future.

Long-term Credit Outlook

A sustained growth in credit levels whilst maintaining the ability to repay and service those growing debt levels is a difficult balance to strike: it requires income and asset prices consistently rising in line with or faster than debt.

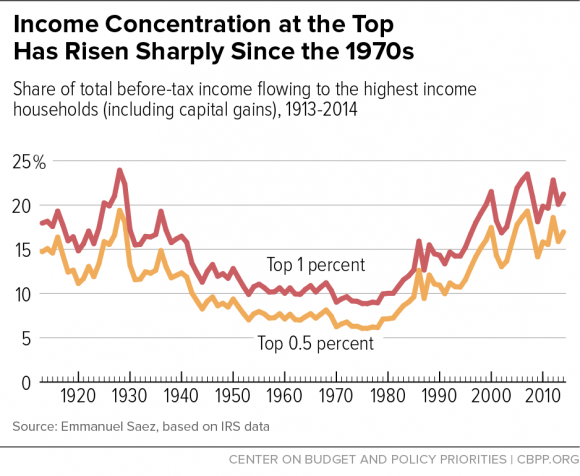

Maintaining this constant growth of spending and credit growth is not easy, even a small contraction in spending can halt the cycle and/or cause the cycle to reverse. Unfortunately, while interest rates play a large part in credit growth, it also depends on large social demographic issues that are not easily controlled by anyone and often entirely outside the scope of central bankers' powers. For example, I recently examined how through QE the Fed has been trying to induce further spending with mixed results. A large part of QE's shortfall can be attributed to America's extreme level of wealth inequality, which is inversely related to economic growth and - all else equal - leads to lower levels of overall spending.

Consistent credit growth requires some mixture of: 1) a growing number of income earners who can spend and borrow more and 2) a more even distribution of capital to a larger number of potential borrowers/spenders, thus maximizing the marginal spending utility of capital rather than concentrating it in the hands of people to whom it has less utility to spend or use as collateral in borrowing.

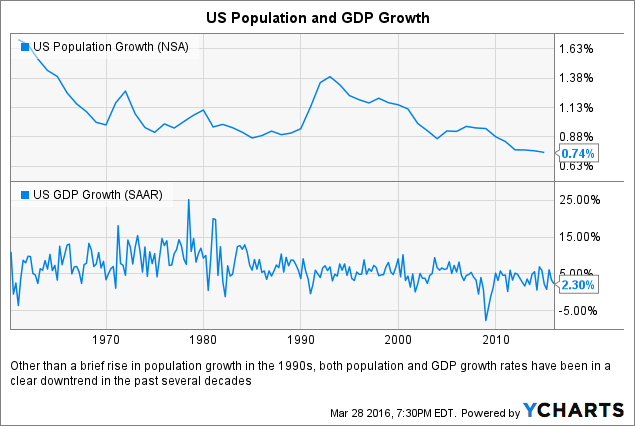

Thus, aggregate credit and spending growth in no small part depend broadly on population growth and (inversely) wealth inequality. Unfortunately, the long-term picture for both point to less credit growth, not more. For the U.S. and many developed nations, population growth rates are on the decline, meaning less income earners and spenders. Combined with a generational effect of Millennials (the largest generation) being "the first in the modern era to have higher levels of student loan debt, poverty and unemployment, and lower levels of wealth and personal income than their two immediate predecessor generations" and their lower rates of home ownership, marriage and general aversion or distrust of financial institutions, the picture for continued credit growth looks even bleaker: Millennials have less means and less desire to borrow in order to finance spending. Things get even worse when you consider that Millennials will hit their stride as peak income earners/spenders (35-45), replacing peak earners currently more open to taking on debt, just as a generation of Baby Boomers that are chronically unprepared for retirement take the place of the 'net spender' retiree demographic.

Taken together, these demographics point to slower credit and spending growth in the future.

This is further exacerbated by the fact that during the same time period population and GDP growth rates have contracted (roughly since the 1970s), wealth inequality has also grown such that is is now at is highest levels since the 1920s.

Perhaps even worse than the demographics, current global debt levels stand at what look like unsustainable levels, having outpaced GDP growth since the Great Recession. At some point, debt levels will have to fall, and contrary to what some investors may believe, a deleveraging event is uniquely deflationary rather than inflationary. This is because falling debt levels usually see periods where lenders are unwilling to create new debt, while at the same time money that could be used on spending is instead used to pay down debts, both of which lead to less spending and in turn lower prices (deflation).

With all this in mind, it's no surprise some major players such as Ray Dalio also see the world at the possible inflection point of a 'long-term debt cycle.' The weight of the evidence seems to

suggest that global economies will face slower credit growth and less spending in the future, which will directly contribute to lower economic growth and prices, i.e. deflationary headwinds.

But credit growth - while arguably the more significant driver of the economy (at least in the shorter term) - is just one piece of the puzzle, we must also consider the impact of productivity trends on the outlook for the global economy. Unfortunately, there is not much better news these for investors looking to avoid deflation.

Long-term Productivity Outlook

Traditionally, the more efficiently or longer an employee works, the more he earns. In the past, technological advancement has mainly served to augment employees and enable workers to achieve ever greater levels of efficiency and aggregate production.

But with technology reaching or nearing a major inflection point of not enabling human workers, but beginning to replace them, a new productivity dynamic may be emerging, and a new economic theory about technology and deflation is gaining ground.

Technology serves to be a major driver of deflation in the future in two ways:

Investors should be wary to make the classic blunder allegedly committed by Charles Holland Duell, Commissioner of the U.S. Patent Office in 1899, when he said "everything that can be invented has been invented."

Implications for Investors

The outlook of 1) lower rates of credit growth due to demographics, 2) a likelihood that current debt levels are at or near a peak and will soon contract in a deleveraging, and 3) technology will increasingly contribute itself to wealth inequality and lower prices, all means that in the long term, investors can expect an increasing frequency and severity of deflationary headwinds. This is both due to prices directly falling due to technology, and due to decreased incomes and spending which in turn induce falling prices.

Likely, this prevalence of deflation will lead to stagnant economic growth, low interest rates, and higher levels of intervention by central banks and monetary policy makers.

In my opinion, the most obvious beneficiary of slow global growth and low (but still for the time being positive) rates are U.S. treasuries and funds like TLT. While in the near to mid term U.S. rate hikes could mean treasury prices fall, this could pose a significant buying opportunity.

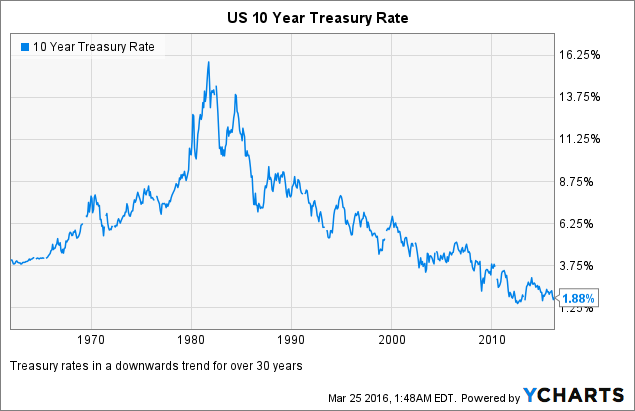

Interest rates are in a nearly four-decade established downtrend that has lasted through previous periods of inflation. Looking forward, signs pointing to a growing prevalence of deflation will likely only serve to strengthen this trend as global interest rates continue to fall and investors seek the positive yield and relative safety of U.S. treasuries.

A perhaps less obvious beneficiary, however, is gold and funds like the SPDR Gold Trust ETF (NYSEARCA:GLD). Although gold is perhaps most frequently talked about as a hedge for inflation, gold is also unique in its role as a 'non-paper' currency and an alternative as a 'storage of value' to currencies backed by central banks. Since threats of prolonged and increasingly severe deflation are likely to be met with proportionally increasing intervention by policy makers, and that intervention is expected to only get less efficient at stimulating growth, a very likely outcome is a general loss of faith in those policy makers and a commensurate devaluing in the currencies they issue and back.

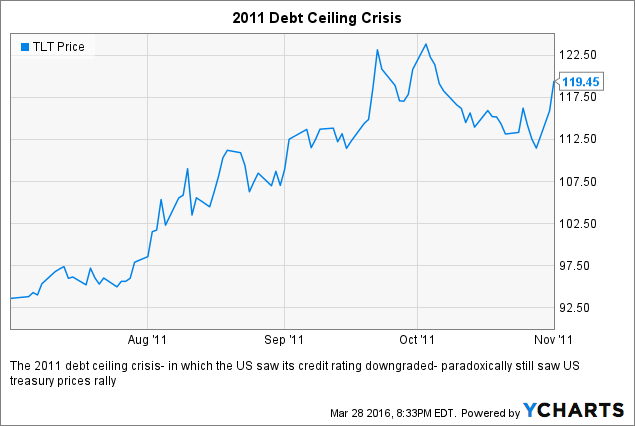

I should note that these two things are NOT mutually exclusive as some investors might initially believe. Both treasuries and gold could benefit in a period of deflation and a loss of faith in policy makers. Paradoxically, a crisis in the faith of the Fed or U.S. government debt has been known to lead to rallying U.S. treasury prices as investors are more concerned about the alternatives, which are still seen as relatively more risky.

For all investors' talk of inflation and the Fed's loose monetary policy, the broader context of the global economy and the long-term dynamics often go unexamined, and many investors seem unaware about the causes or existence of the deflationary global economic pressures seen in recent years.

While inflation remains a possible concern in the U.S. in the short to mid term, investors would be wise to remember to consider the broader context in which the Fed is acting and in which investors are ultimately investing their hard earned money.

For many reasons, it is deflation, rather than inflation, that may prove to be the larger concern for investors looking to build their wealth into the mid-2000s. As a topic that seems to often go unmentioned amongst retail investors more directly concerned with the U.S.'s debt levels and the Fed's low rate policies, I hope you have found this article insightful. Thank you for reading, and please share your outlooks for rates, inflation/deflation and related assets such as treasuries and gold in the comments.

To be clear, as outlined in my previous article, higher than desired inflation for the immediate future remains a possibility, in no small part thanks to the actions of central banks, but those actions must be considered in their broader contexts. What many investors do not realize - or do not actively think about - is that for the last several years the 'natural state' of the global economy has been one of deflation. The main reason for this is simple: economic recessions and debt deleveragings are - all else equal - naturally deflationary. Why? Well, in both an economic recession and a time of overall debt levels coming down (a deleveraging), borrowing and credit growth decline as lenders become more wary about borrowers' ability to repay debts and borrowers lose jobs and income and become less qualified to take on debts. This shrinking of the ease and availability of credit in turn leads to decreased spending. Decreased spending leads to lower revenues and earnings, and as companies struggle to stay competitive and afloat in these conditions they repeatedly slash prices, i.e. deflation.

Thus, the natural deflationary tendency of global markets in recent years has 'absorbed' much of the effect of central banks' inflationary policies, which was their goal all along - counter the prevailing deflationary economic conditions. Central bankers are so terrified about deflation because - as you may already have inferred - a deflationary cycle quickly becomes self reinforcing as less credit means less spending, which leads to falling company revenues and earnings, inducing wage cuts and layoffs, which in turn means even less credit and even less spending... and so on. Not pretty.

While I still stand by what I concluded in my previous article: that in the short to medium term, we may either see a crisis of faith in central banks, and/or an unintended but rapid rise in inflation, the longer-term market dynamics point towards something quite different and perhaps all the more menacing: a growing prevalence of deflation.

Credit and The Economy

In a consumer economy - such as those of the U.S. and most developed or first world countries, and what China is currently trying to transition into - spending is arguably the single most important driver of economic growth.

That's because rising spending creates a self reinforcing effect of growth, in the same way falling spending in a deleveraging leads to a self reinforcing contraction. All else equal - increased spending leads to higher revenues and higher profits for companies, meaning higher wages and/or increased employment, meaning higher aggregate income levels, which means higher disposable income and increased spending... and so on.

Thus, roughly speaking, the trend in spending itself steers the overall direction of the economy. Spending money can come from two possible sources:

- Wages (productivity) - All else equal, the more productive an employee is - the more hours they work or the more they accomplish and produce within those hours - the more income they will earn.

- Credit (borrowing) - The more wealth or income an individual has compared to existing debt, the more they can borrow against that wealth and income.

Thus, the rate of credit growth or contraction directly impacts spending, which in turn directly impacts the rate of economic growth. It follows then to examine the prospects for long-term credit growth to get an idea for economic growth in the future.

Long-term Credit Outlook

A sustained growth in credit levels whilst maintaining the ability to repay and service those growing debt levels is a difficult balance to strike: it requires income and asset prices consistently rising in line with or faster than debt.

Maintaining this constant growth of spending and credit growth is not easy, even a small contraction in spending can halt the cycle and/or cause the cycle to reverse. Unfortunately, while interest rates play a large part in credit growth, it also depends on large social demographic issues that are not easily controlled by anyone and often entirely outside the scope of central bankers' powers. For example, I recently examined how through QE the Fed has been trying to induce further spending with mixed results. A large part of QE's shortfall can be attributed to America's extreme level of wealth inequality, which is inversely related to economic growth and - all else equal - leads to lower levels of overall spending.

Consistent credit growth requires some mixture of: 1) a growing number of income earners who can spend and borrow more and 2) a more even distribution of capital to a larger number of potential borrowers/spenders, thus maximizing the marginal spending utility of capital rather than concentrating it in the hands of people to whom it has less utility to spend or use as collateral in borrowing.

Thus, aggregate credit and spending growth in no small part depend broadly on population growth and (inversely) wealth inequality. Unfortunately, the long-term picture for both point to less credit growth, not more. For the U.S. and many developed nations, population growth rates are on the decline, meaning less income earners and spenders. Combined with a generational effect of Millennials (the largest generation) being "the first in the modern era to have higher levels of student loan debt, poverty and unemployment, and lower levels of wealth and personal income than their two immediate predecessor generations" and their lower rates of home ownership, marriage and general aversion or distrust of financial institutions, the picture for continued credit growth looks even bleaker: Millennials have less means and less desire to borrow in order to finance spending. Things get even worse when you consider that Millennials will hit their stride as peak income earners/spenders (35-45), replacing peak earners currently more open to taking on debt, just as a generation of Baby Boomers that are chronically unprepared for retirement take the place of the 'net spender' retiree demographic.

US Population Growth data by YCharts

Taken together, these demographics point to slower credit and spending growth in the future.

This is further exacerbated by the fact that during the same time period population and GDP growth rates have contracted (roughly since the 1970s), wealth inequality has also grown such that is is now at is highest levels since the 1920s.

Perhaps even worse than the demographics, current global debt levels stand at what look like unsustainable levels, having outpaced GDP growth since the Great Recession. At some point, debt levels will have to fall, and contrary to what some investors may believe, a deleveraging event is uniquely deflationary rather than inflationary. This is because falling debt levels usually see periods where lenders are unwilling to create new debt, while at the same time money that could be used on spending is instead used to pay down debts, both of which lead to less spending and in turn lower prices (deflation).

With all this in mind, it's no surprise some major players such as Ray Dalio also see the world at the possible inflection point of a 'long-term debt cycle.' The weight of the evidence seems to

suggest that global economies will face slower credit growth and less spending in the future, which will directly contribute to lower economic growth and prices, i.e. deflationary headwinds.

But credit growth - while arguably the more significant driver of the economy (at least in the shorter term) - is just one piece of the puzzle, we must also consider the impact of productivity trends on the outlook for the global economy. Unfortunately, there is not much better news these for investors looking to avoid deflation.

Long-term Productivity Outlook

Traditionally, the more efficiently or longer an employee works, the more he earns. In the past, technological advancement has mainly served to augment employees and enable workers to achieve ever greater levels of efficiency and aggregate production.

But with technology reaching or nearing a major inflection point of not enabling human workers, but beginning to replace them, a new productivity dynamic may be emerging, and a new economic theory about technology and deflation is gaining ground.

Technology serves to be a major driver of deflation in the future in two ways:

- Technology directly decreases costs/prices - Whether it's fracking, assembly line automation, or the induced efficiencies of the 'sharing economy,' technology makes things better, faster and cheaper. And this is an effect that will likely only be increasingly felt, as technology advances at an exponential rate. This not only means that technology will - all else equal - cause lower prices in the future, but for a fixed period of time it will cause increasingly large declines in price as time goes on: an effect that is directly deflationary.

- Technology (under current government/social/economic constructs) induces further wealth inequality - As technology advances and more and more roles traditionally staffed by humans are in full or in part filled by machines, employees can expect layoffs, fewer hours, and smaller aggregate wages. While there are many forces which might slow this effect - labor unions, regulations, etc. - on aggregate, employees will see wage cuts, while the owners and executives will directly benefit from induced cost savings and increased output achievable via automation and layoffs, only serving to further worsen wealth inequality.

Investors should be wary to make the classic blunder allegedly committed by Charles Holland Duell, Commissioner of the U.S. Patent Office in 1899, when he said "everything that can be invented has been invented."

Implications for Investors

The outlook of 1) lower rates of credit growth due to demographics, 2) a likelihood that current debt levels are at or near a peak and will soon contract in a deleveraging, and 3) technology will increasingly contribute itself to wealth inequality and lower prices, all means that in the long term, investors can expect an increasing frequency and severity of deflationary headwinds. This is both due to prices directly falling due to technology, and due to decreased incomes and spending which in turn induce falling prices.

Likely, this prevalence of deflation will lead to stagnant economic growth, low interest rates, and higher levels of intervention by central banks and monetary policy makers.

In my opinion, the most obvious beneficiary of slow global growth and low (but still for the time being positive) rates are U.S. treasuries and funds like TLT. While in the near to mid term U.S. rate hikes could mean treasury prices fall, this could pose a significant buying opportunity.

Interest rates are in a nearly four-decade established downtrend that has lasted through previous periods of inflation. Looking forward, signs pointing to a growing prevalence of deflation will likely only serve to strengthen this trend as global interest rates continue to fall and investors seek the positive yield and relative safety of U.S. treasuries.

10 Year Treasury Rate data by YCharts

A perhaps less obvious beneficiary, however, is gold and funds like the SPDR Gold Trust ETF (NYSEARCA:GLD). Although gold is perhaps most frequently talked about as a hedge for inflation, gold is also unique in its role as a 'non-paper' currency and an alternative as a 'storage of value' to currencies backed by central banks. Since threats of prolonged and increasingly severe deflation are likely to be met with proportionally increasing intervention by policy makers, and that intervention is expected to only get less efficient at stimulating growth, a very likely outcome is a general loss of faith in those policy makers and a commensurate devaluing in the currencies they issue and back.

I should note that these two things are NOT mutually exclusive as some investors might initially believe. Both treasuries and gold could benefit in a period of deflation and a loss of faith in policy makers. Paradoxically, a crisis in the faith of the Fed or U.S. government debt has been known to lead to rallying U.S. treasury prices as investors are more concerned about the alternatives, which are still seen as relatively more risky.

TLT data by YCharts

Conclusión

While inflation remains a possible concern in the U.S. in the short to mid term, investors would be wise to remember to consider the broader context in which the Fed is acting and in which investors are ultimately investing their hard earned money.

For many reasons, it is deflation, rather than inflation, that may prove to be the larger concern for investors looking to build their wealth into the mid-2000s. As a topic that seems to often go unmentioned amongst retail investors more directly concerned with the U.S.'s debt levels and the Fed's low rate policies, I hope you have found this article insightful. Thank you for reading, and please share your outlooks for rates, inflation/deflation and related assets such as treasuries and gold in the comments.

0 comments:

Publicar un comentario