China’s Economy Faces Recovery Without Legs

Old tricks to reflate the economy could cause problems down the road

By Alex Frangos

Laborers at a construction site in Beijing. China's economy grew 6.7% in the first three months of 2016, its slowest quarterly expansion in years. Photo: Agence France-Presse/Getty Images

China’s economy may have stabilized for now, thanks to gobs of new debt and a reflating property bubble. Dipping into that old bag of tricks, however, seems likely to dredge up the same old problems.

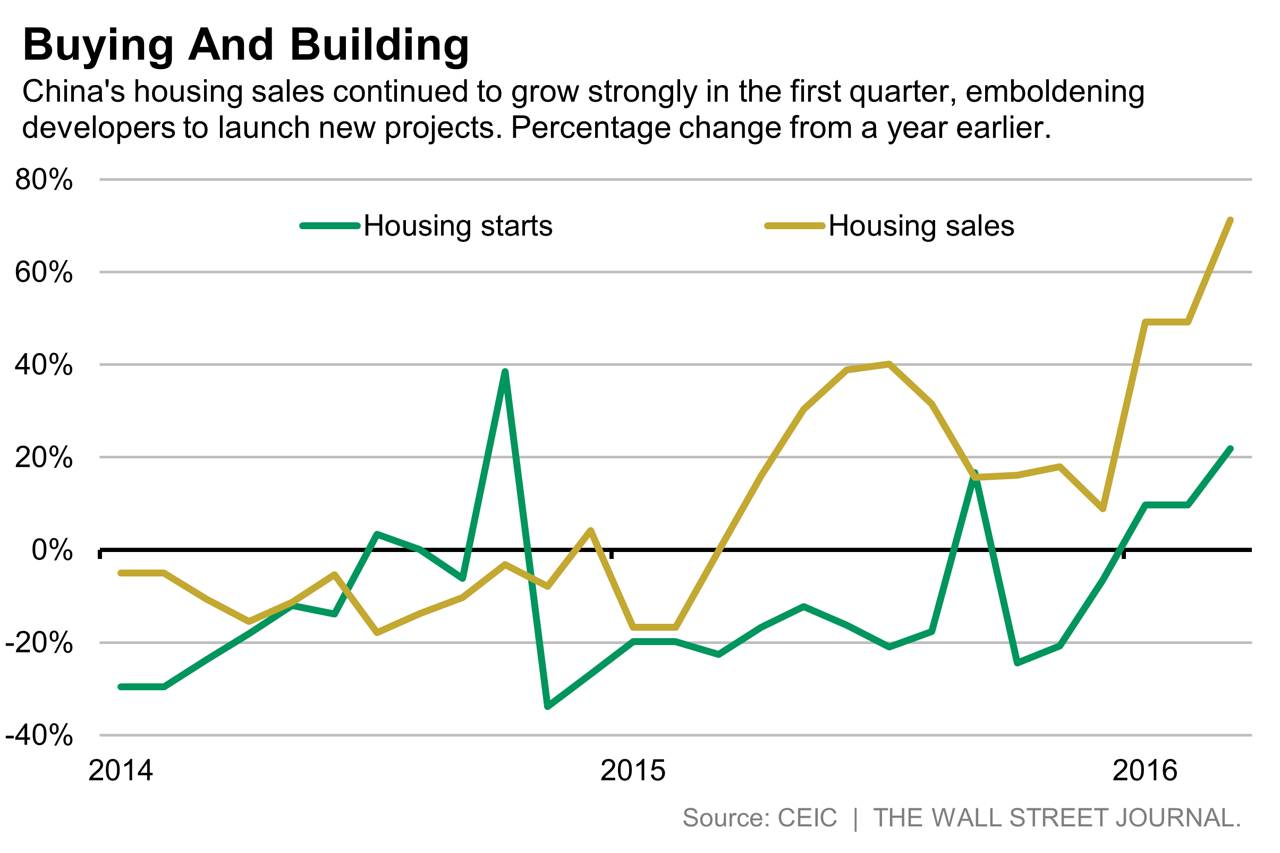

Official data showed China’s gross domestic product slowed to 6.7% in the first quarter from a year earlier. As expected, that is the slowest in years, but underlying data showed activity picked up toward the end of the quarter.

Home buyers, for instance, continued to splash out for new property, with residential sales rising 54% in the first quarter from a year earlier. That has emboldened developers to start to build again, with housing starts rising 16% in the first quarter, after falling 15% last year.

That augurs well for employment and demand for raw materials.

But it is hard to see China’s property market—which in past years generated directly and indirectly up to a third of all economic activity—returning to its past glory. Much of the recovery in prices and activity has been in China’s so-called tier one cities—the four largest cities—and regulators there are already clamping down to prevent things from getting out of hand.

In the rest of China, the property recovery is far more subdued, and inventories of unsold apartments remain substantial. Around 95% of real estate sales occur outside of those top four cities, notes Louis Kuijs of Oxford Economics, so unless the boom spreads, the impact on the broader economy will remain muted.

China’s old economy sectors also seem to have awoken somewhat from their slumber.

Industrial production grew 6.8% in March, the fastest in nine months. Fixed asset investment, spending on things like factories and infrastructure, grew 11.2%, much faster than the 6.8% low it hit in December.

Driving all this activity: easy money. Real interest rates have fallen. And nominal GDP grew faster than real GDP for the first time in five quarters, which in theory makes servicing debt easier.

What should trouble investors is that while China’s economic activity is ticking up, debt is piling up faster. The stock of total financing in the economy, including bond issuance as part of a local government bailout program, rose 15.8% in March from a year ago, the fastest rate since mid-2014.

With nominal GDP growing 7.2%, Beijing’s plans to deleverage the economy continue to be overwhelmed by the need to support growth.

China bulls will be pleased by the data, hoping that a proper recovery is at hand. Those hopes may prove short lived. The more the recovery is fueled by debt and property, the more concerned Beijing will be that it is pushing the gas too hard and will have to ease off sooner than people think.

0 comments:

Publicar un comentario