ZIRP & NIRP: Killing Retirement As We

Know It

By John Mauldin

“Baby boomers who are counting on the stock market are in trouble.”

– Robert Kiyosaki

“Pension and health care costs for our employees are going to bankrupt this city.”

– Michael Bloomberg

Over the last 150 years or so, numerous innovations have radically changed the way people live. You can tick off the list: electricity, the automobile, refrigeration, television, the Internet. Yet one innovation rarely makes those lists, even though it is just as significant if not more so: retirement.

The idea that people can stop working in their fifties or sixties and then enjoy 20+ years of relative leisure is actually quite new. For most of human history, the vast majority of people worked as long as they were physically able to – and died soon after. Retirement is possible now only because those other 20th-century innovations accelerated the division of labor and lifted us out of subsistence farming and living.

Our inventions often have a dark side that can come to haunt us. They may be applied to wage war… or to create reality TV. Are we going over to the dark side with retirement? Maybe not, but we’re certainly heading in that direction. And there’s nothing wrong with the idea of retirement, of course – the concept is a fabulous invention, helping to extend life and happiness. But retirement is made possible by a prior life of hard work and careful saving and investment. And the very funds that make retirement possible are dependent on growth of the economy. Without growth, retirement as we have come to know and love it will not work. Retirement will still be possible, of course – just not under the same conditions.

The zero interest rate and now negative interest rate policies of our central banks are gumming up the global retirement machinery. The Federal Reserve and other central banks have spent so many years subsidizing debt and punishing savings that it is now extremely difficult to guarantee future income streams at a reasonable present cost. And future income streams are the very heart and soul of retirement. Without adequate future income streams, retirement as we know it today is off the table.

Whether this sad fact is what the central bankers intended or not, it is indeed a fact, whether you are an individual saver or a trillion-dollar pension fund. Today we’ll examine how we have come to this unhappy point.

But first, let me mention that although my Strategic Investment Conference (May 24–27 in Dallas) is sold out, we’re trying hard to find a way to accommodate a few more people without compromising the experience for those who have already registered. We have created a waiting list, and you can click on this link and pay a small fee (which is refundable) to get on it. Seriously, we expanded the room this year and thought we were fine – then we sold out in less than a month! I have friends calling me up and asking to get in, as they have attended for many years. Not an unreasonable expectation. Believe me when I say we are trying, but there is a space issue. So even if we are BFF’s, get on that list! THEN call. The only way to be fair and to save my sanity is to do this on a first-come, first-served basis. The line is growing, so even though the conference is three months away, sign up NOW!

Saving money for retirement has never been easy for the average worker, but at least it was feasible if you started early and earned a middle-class living, especially if you had automatic deposits or a business or government guaranteeing you a pension. Plus, the bond market was on your side. Until the year 2000 or so, anyone could lock in risk-free 5% or higher yields in bank certificates of deposit.

Suppose you saved all through your career and accumulated a million dollars. It was a simple matter to put it all in CDs, Treasury bonds, or tax-free muni bonds and generate $50,000 a year in current income. Living costs were lower last century, too. Presumably, you also paid off your mortgage in the course of living the American Dream. Add in Social Security and you could enjoy a comfortable if not extravagant retirement. Your million-dollar principal would remain intact and could go to your children upon your death.

Again, this was relatively easy to do. It didn’t require any financial sophistication or even a brokerage account. The hardest part was saving the million dollars in the first place, but you could get by with much less if you drew down the principal over a 20- or 30-year period (and didn’t outlive the drawdown).

Better yet, you could do this with no risk, just by keeping your money in FDIC-insured banks. You might have to split it between a few different banks to stay within the limits. Some extra paperwork, but easily done. There were plenty of services that would help you distribute your assets over multiple FDIC-insured banks.

It was even simpler if you had an employer or union pension plan to do the work for you. Pension plans pooled people’s money, calculated how much cash they would need to pay benefits in future years, and built portfolios (mainly bonds) to match the liability projections. Government and corporate bonds yielded enough to make the process feasible.

Younger readers may think I just described a fantasy world. I assure you, it was very much a reality not so long ago. Ask your grandparents if you don’t believe me. However, you may find them in a state of shock today because they thought the fantasy would last forever. Indeed, their financial planner probably told them they could count on drawing down 5% of their portfolio per year to live on, because the income from the investments in their portfolio would more than make up for the drawdown.

None of this is possible today. Neither you nor a massive pension plan acting on your behalf can generate enough risk-free income to assure you a comfortable retirement.

Why not? Because our monetary overlords decreed that it should be so. Retirees and their pensions are being sacrificed for what now passes as “the greater good.” Because these very compassionate overlords understand that the most important prerequisite for successful future retirements is economic growth. And they think that an easy monetary environment is the necessary fertilizer for that growth. So, when they dropped rates to zero some years ago, they believed they would soon be able to raise them again – and get people’s retirements back on track – without risking future economic growth. The engine of growth would fire back up, and everything would return to normal.

So much for the brilliant plan. You and I, the expendable foot soldiers in the war to reignite growth, now gaze about, shell-shocked, as the economic battlefield morphs from the Plains of ZIRP to the Valley of NIRP.

In fairness to our central banks, they must balance competing priorities. The Fed’s statutory mandate is to promote “maximum employment and stable prices.” Their primary tools to execute this mandate are the manipulation of the money supply and interest rates. Since 2008 they relied on near-zero interest rates to stimulate economic growth. As I wrote last week, the Fed (and much of the economics profession) sincerely believes that low interest rates will do the job they’re supposed to.

However, the hard evidence of the past few years is that ultra-low rates, combined with quantitative easing, haven’t stimulated much growth. Unemployment has fallen, which is good – but probably not as good as the numbers suggest, because people have gone back to work for lower pay and are now even deeper in debt. Personal income growth has stagnated, as we will see a little later in this letter. So, are we better off now than we were five years ago? The answer is a qualified yes. But it is not entirely clear, at least to your humble analyst, that the halting economic recovery is the result of low interest rates and not other less manipulable factors such as entrepreneurial initiative and good old muddling through. In fact, an ultra-easy monetary policy may be part of the reason we’ve been stuck with low growth. Witness Japan and Europe. Just saying…

Seriously, no one fully understands how all the moving parts influence each other. Years of ZIRP did help businesses and consumers reduce their debt burdens. ZIRP and multiple rounds of QE have also done wonders for stock prices … but not much for the kind of business expansion that creates jobs and GDP growth.

If year upon year of ultra-low rates were enough to create an economic boom, Japan would be the world’s strongest economy right now. It obviously isn’t – which says something about ZIRP’s efficacy as a stimulus tool.

What isn’t a mystery, however, is that ZIRP has created a massive problem for retirement savers and pension fund managers. NIRP will make their problem worse – and they were already facing other challenges as well.

If we get negative interest rates for a sustained period, similar to Japan and Europe, it will be because the economy is stuck at no-growth or in contraction. Stock prices will head the other direction: down. It will be the mother of all bear markets. We are getting a little taste of it right now in bank stocks. Look for much worse as the growing impact of NIRP and the threat of NIRP reaches other sectors.

Employer-based retirement plans come in two flavors: defined benefit and defined contribution. A defined-benefit plan is what we usually think of as a pension. You work for employer X, who promises to let you retire at age 60 or 65 with a defined monthly pension payment – so many dollars per month, based on your salary, years of service, etc. You and your employer pay for this plan by contributing cash to it during your working years. (Unless you work for a government entity like a police force or fire department and can retire in your early 40s with full benefits after 20 years, then go to work for another government entity and retire with a second and sometimes even a third defined-benefit retirement plan. Yes, there are numerous instances of this. Not a bad gig if you can get it.)

But will the amount you and your employer contributed be enough to pay that defined benefit for all the years you survive after retirement? The answer necessarily involves guesswork and assumptions about events 20 or 30 years in the future. It also means someone has to be on the hook in case the guesswork is wrong. That’s usually the employer … or taxpayers.

Private-sector employers realized decades ago that carrying pension liabilities on their balance sheets left them at a competitive disadvantage. They removed those liabilities by switching newer workers to defined-contribution plans – the now-familiar 401(k) and similar programs. You and (if you’re lucky) your employer both deposit cash into your 401(k) account. You decide how to invest the money and hopefully do well. More to the point, a defined-contribution plan does not require your employer be on the hook for poor investment results. The one on the hook is you.

Defined-benefit plans now exist mainly in state and local governments, where unionized workers have more influence over management and elected leaders come and go. Politicians, by their nature, often think no further ahead than the next election. Their path of least resistance is to promise workers the moon and let their successors figure out how to pay for it.

Guess what? The future is here, and it turns out the guesswork and assumptions about the future were really, really bad. As in, if you are just about to retire or have only been retired a few years and have a pension, you may be seriously screwed.

I get a creepy déjà vu feeling every time I write about public pensions. I’ve been preaching about them for more than a decade now, and the situation keeps getting worse. Obviously the politicians are ignoring me – and not without reason. Clearly, I underestimated their ability to postpone the inevitable. Nevertheless, I firmly believe a train wreck is coming. The math has never worked well, and now ZIRP/NIRP is making it much worse.

Fixed-income markets are tailor-made for funding future liabilities. Suppose you sign a contract in which you agree to pay your supplier $1 million exactly one year from now. How do you make sure you will have the cash on hand when the time comes?

The most conservative way would be to put $1 million in a lockbox right now, with instructions to open the box and disburse payment on the agreed date.

Back when CD and Treasury bill rates were 5%, you could just buy a series of $100,000 CDs for $1 million. When the time came, you handed over the principal and kept the interest accrued. You covered your obligation and still had $50,000 to use however you wanted.

That is roughly how defined-benefit pensions used to work, with longer time spans and much larger numbers. My example also has an advantage they don’t: certainty on how much cash you will need at maturity and the exact amount the investment will make in the meantime.

A pension plan that covers thousands of retirees can make educated guesstimates as to how long those pensioners will live. Professional actuaries are uncannily good at this when the population is large enough.

The far bigger challenge is to determine the expected rate of return on the pension’s assets.

That number is a hot potato, because it determines how much cash the employer must contribute each year to keep the plan “fully funded.” The laws require the sponsor of a pension plan to maintain a fully funded position. However, they allow a great deal of flexibility in how “fully funded” is defined. Assume higher returns in the future and you can get away with spending less money in the present. Furthermore, because we are dealing with large numbers over long time spans, small changes can make a huge difference.

The state and local officials responsible for these plans want to assume higher returns so they don’t have to raise taxes or cut other spending. So, as politicians often do, they shop around for someone who will give them the answer they want – along with plausible deniability should that answer turn out to be wrong. This is why we have a thriving “pension consultant” industry.

Almost without exception, public pension plans still assume very optimistic future returns. They base those projections on long-run past performance and assume the future will be like the past. CALPERS, the California public employee plan that is the nation’s largest pension, is in the process of reducing its base forecast from 7.75% to 7.5%. Even this tiny change was enormously controversial. Revenue-challenged local officials all over the state looked at the difference it made in their mandatory contributions and flipped out.

I have talked to numerous board members on multiple enormous public pension boards. Many of them would privately like to reduce their projected returns, but they know it is politically impossible to do so. Other simply say, This is what my consultants tell me, so I have to go with their expert opinion, don’t I?”

The return assumptions are a blend of past stock and bond market returns. This is where ZIRP starts to hurt. Bond returns have the advantage of being more predictable than stock returns, but now they are predictably low. Inflation-adjusted returns on Treasury and investment-grade corporate bonds are either zero, below zero, or not far above zero. They are certainly nowhere near the 5% or more that was once common.

If you can’t assume decent bond returns, can you make up the difference with higher stock returns? That’s not easy, either. Today’s behemoth pension funds don’t simply invest in the stock market; to a large extent, they are the stock market. It is mathematically impossible for all or even most of them to achieve above-market returns. They are just too big.

As I often say, long-run stock market returns are a function of economic, population, and productivity growth. Some companies always outperform others; but in the aggregate, stocks can’t outpace the economy in which they operate. If the economy grows slowly, then over the long run stock values will, too.

Growing slowly is exactly what the entire developed world has been doing and appears set to continue doing for years to come. If 2% is the best GDP growth we can hope for, then we are not going to see stock market returns over the next 20 to 30 years at anywhere near the 8% or 10% that many pension trustees assume.

If investment returns aren’t sufficient for pensions to pay the benefits they promised, all the consequences are bad. State and local governments must then implement some combination of higher taxes, spending cuts, or benefit reductions. All three hurt.

The same reality applied if you’re running your own pension. If you don’t save enough and/or fail to achieve your expected returns, you will face some unpleasant choices: work longer, live more frugally, or die sooner.

If ZIRP is bad, NIRP will be far worse for retirement planning. Bond-return assumptions will have to be even lower and potentially below zero. This situation would wreak havoc on every pension fund – but that’s not even the worst part.

Most asset allocations are generally in the ballpark of 60% equities and 40% bonds, so that is the standard portfolio we will be discussing. Other allocations will make some differences but not change the general direction. In other words, “your mileage may vary” – but probably not by much.

In an ideal world – which is the world that pension consultants live in – equities will return 10% nominal, and bonds will return 5%. A 60/40 portfolio blend will then yield an 8% overall return after fees, expenses, and management costs.

It doesn’t require a great deal of head scratching to realize that a negative interest rate environment is going to bring overall bond yields down below 2%. That paltry yield will drop the blended portfolio rate to 1.2%. How long can that low return last? Ask Japan. When we saw the advent of zero interest rates in the US seven years ago, no one thought they would be in place this long. No one.

The reality is that in our mega-debt world, long-term interest rates are going to be low for quite some time. One thing that could change that would be inflation’s charging back against consensus expectations. I don’t think the Fed really makes much of a move until inflation is over 3%. FOMC members would actually like to see 3% inflation for a while, though they will never say that. But then at some point they will have to make a move, and that is going to be exceedingly uncomfortable whenever it happens. But for the nonce, we are in a low interest rate environment.

Maybe we could just allocate more to equities? That is one possible solution, but the historical record suggests that might make our task even more challenging! When I start thinking about future possible returns, one of the first phone calls I make is to my friend Ed Easterling of Crestmont Research. He and I have collaborated on numerous papers on market cycles and future returns, most recently “It’s Not Over Until the Fat Lady Goes on a P/E/ Diet.” His website is a cornucopia of data and analysis. Let’s look at a few of his charts and conclusions.

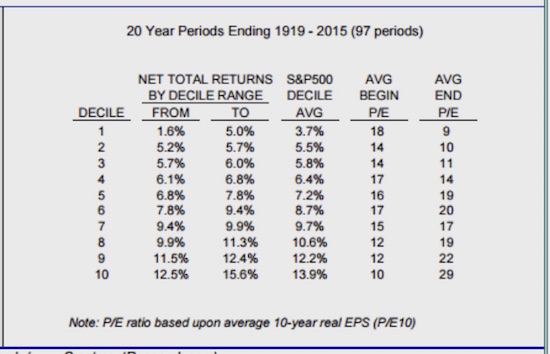

One of the more reliable predictors of future returns is the current price-to-earnings (P/E) level. There are only three sources of stock market growth: EPS growth, dividend yield, and the change in P/E ratios (http://www.crestmontresearch.com/docs/Stock-Waiting-For-Avg.pdf). Where you start from gives you an excellent indication of the range of returns you can expect to get over the following 20 years. For most people, 20 years can be considered the long run.

Today the normalized P/E ratio is 23, which is right up there in the top 10% of historical rankings. Even if you want to quibble and drop the ratio a few notches, it’s still high. And by looking at the chart below, we find that historical returns 20 years on have ranged from 1.6% to 5.0%, with an average of 3.7%.

There is no historical instance of price-to-earnings multiples expanding from where we are today for any sustained length of time. In fact, levels like those we see today have generally indicated a brewing storm – a bear market. That doesn’t mean something new can’t happen this time. There are those who argue that because interest rates are so low, we can expect earnings multiples to continue to rise. Maybe, but for how long and how by how much?

If you take the highest historical return of 5% (from our current P/E) and marry that with the bond returns we discussed earlier, you find your 60/40 portfolio can now be expected to give you 4.2%. And the average historical equities return of 3.7% leaves you with only a 3.5% total return on your investment portfolio!

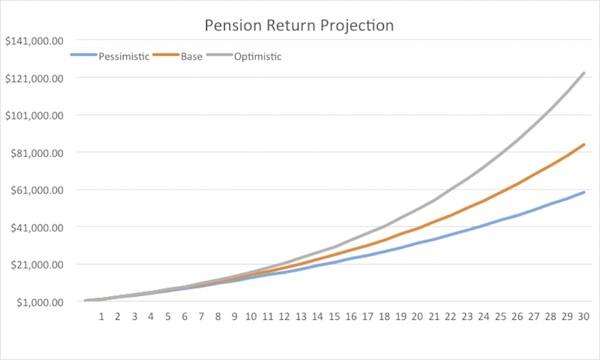

And the return level makes a huge difference to the eventual success of a pension. As in, a monster difference. Most people don’t realize that most of the money their pension will pay them in 20 or 30 years will come from the growth of the portfolio and not from their actual contributions. As we will see, your contributions might actually amount to as little as 20 or 25% of the total portfolio 20 years from now.

I’m going to start with a modest number, but you can add zeros to your heart’s content. Let’s say you save $1,000 a year for the next 30 years. Your pension consultant tells you that you can make 8%. And if you actually do, you find you have paid in $30,000, but your account has grown to $123,345.87, or over four times your contributions. Not a bad day at the office. You stick that into a 5% CD (bear in mind that we’re talking a fantasy outcome here), and you make $6,000 a year, or about $500 a month. Add a zero and save $10,000 a year for 30 years, and now you’re earning $5,000 a month, which, with a paid-for home and Social Security, provides you a comfortable, if somewhat frugal, lifestyle.

But what if you get only a 6% total return? Well, now you only have $84,801.68 after 30 years. Your 5% CD gets you only $4,000 a year. If you were able to save $10,000 a year, your monthly income would be roughly $3,500. Not bad, but much tighter. But that outcome depends on your being able to get 5% on your bonds or CDs. Do you want to bet your future that interest rates are going to be that much higher in 20 years? Maybe you need to save more.

Let’s turn to a little graph that my associate Patrick Watson whipped up for me in Excel. The top, gray line represents the 8% scenario; the middle, orange line is the 6% scenario; and the lower, blue line is the more pessimistic (but maybe realistic) 4% return.

What does that 4% return look like 30 years down the road? Your $30,000 in contributions have not even doubled, leaving you with just $59,328.34. That’s right, you don’t even get a double. And in our far distant future, that 5% CD is only going to give you $250 a month. Or if you save $10,000 a year for 30 years, you’ll be living on $2,500 a month.

But these numbers assume you don’t have to deal with that pesky inflation thing. A mere 2% inflation will guarantee that your money will be cut by about half after 30 years. (So even that $5,000 a month if you really make 8% won’t turn out to be that much of a lifestyle. And God forbid you make only 4%.)

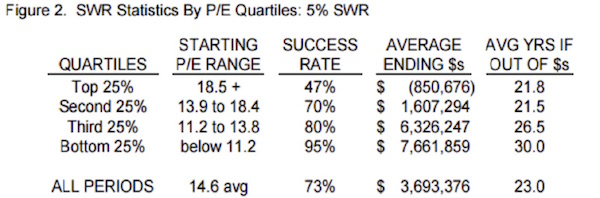

Well, that’s okay, many financial planners will say. You just dip into your principal, and when the market turns around you make it back up. I can’t tell you how many financial plans I’ve seen that assume the safe withdrawal rate (SWR) is 5%. As the table below (from one of Ed’s essays) demonstrates, a 5% withdrawal rate has historically (as in, since 1900) only been safe 47% of the time, and on average you are out of money after 21 years. Hardly safe!

The only way you can be “safe” is to find that magical 5% CD of the future when you’re ready to retire. If the world then happens to look like it does now, though, you’ll just have to keep right on working until things somehow magically recover. I hope that never happens to you, because you could find that your work experience is no longer relevant in an increasingly rapidly changing future.

I also wouldn’t assume that 30 years is a reasonable additional lifespan starting from age 65. With the advances being made in medicine and biotech, your “healthspan” as well as your lifespan are going to increase, and we are going to see many people live well into their hundreds. I think people would be well advised to plan to live a great deal longer than their parents and grandparents did and to budget for retirement accordingly. For most people that means continuing to work. If the thought of working an extra five years at your current job is somehow unpleasant, then my suggestion is that you switch jobs as soon as you can and find something you can tolerate for the longer term.

The same numbers that we applied to individual returns also apply to pension funds.

Pension funds are going to wake up in 10 or 15 years, find they are massively underfunded, and look to taxpayers and businesses to re-fund them. Your corporate pension plan that is guaranteed by the Pension Benefit Guarantee Corporation is not as guaranteed as you might think. If the PBGC has to take over your fund, you may be lucky to get 50% of the promised benefits. Before you get too fat and happy, I would read the fine print on that guarantee. Then I would ask the pension plan management exactly what expected return they are planning to get; and when you hear the typical “7½% for the long run (blah blah blah),” start trying to figure out how to work well past your expected retirement age so that you can supplement your pension when it fails. Then again, maybe your corporation will be there in 20 years when you need it. No need to worry – just assume it wil l all work out. Everybody else plans that way, and they all tell you everything’s going to be fine – just ask your brother-in-law.

Pension funds are going to wake up in 10 or 15 years, find they are massively underfunded, and look to taxpayers and businesses to re-fund them. Your corporate pension plan that is guaranteed by the Pension Benefit Guarantee Corporation is not as guaranteed as you might think. If the PBGC has to take over your fund, you may be lucky to get 50% of the promised benefits. Before you get too fat and happy, I would read the fine print on that guarantee. Then I would ask the pension plan management exactly what expected return they are planning to get; and when you hear the typical “7½% for the long run (blah blah blah),” start trying to figure out how to work well past your expected retirement age so that you can supplement your pension when it fails. Then again, maybe your corporation will be there in 20 years when you need it. No need to worry – just assume it wil l all work out. Everybody else plans that way, and they all tell you everything’s going to be fine – just ask your brother-in-law.

Let’s step away from the unrestrained sarcasm to sum up the facts: Long before 20 years have passed and sometime after the onset of the next bear market, reality will set in, and pension fund managers will begin to plead for increased funding. And that is going to cause all sorts of repercussions. For a government plan, to obtain the needed funds, either taxes will have to go up, or other services and government expenditures will get cut. Either way, it appears that voters are in no mood to tolerate the status quo today. Imagine how much more fractious they’ll be in 20 years, when it’s clear that most people’s pensions are down the drain.

The biggest bubble in the world is the one we live in without being able to see it. It’s the bubble of government promises that government will not be able to fulfill. When it bursts, multiple generations will find their expectations destroyed. The politicians at ground zero had better be saying their prayers and putting their earthly affairs in order, because they aren’t going to last very long after that bubble bursts and reality sets in.

This is a mathematical certainty: hundreds of pensions are seriously underfunded, and many more will be endangered if we have another significant recession. Four percent returns for 10 years in a pension plan portfolio will result in massive future underfunding, even if things eventually get back to “normal.” There is going to have to be significant funding from corporations and taxpayers to make up the shortfall, at precisely the time when that money will be needed to rebuild infrastructure, retrain massive numbers of workers facing employment challenges from an ever-transforming environment, and deal with the fact that there will be more old people living than there are young people being born. This last fact is already the reality in Japan and much of Europe.

Next week we are going to look at what makes the pension challenge even more problematic: the difference between 2% GDP growth and 3% growth over the decades to come is every bit as dramatic as the difference between 4% and 8% portfolio returns. And if we don’t figure out how to get back to 3% GDP growth (and neither of the two leading presidential candidates are offering anything close to a plan that will get us there), the US is going to find itself even deeper in a hole, even as we continue to dig.

While the calendar looks relatively open (at least by past standards), the need for me to go to Chicago has arisen in the last 10 days, and suddenly it’s two days with about ten appointments. My staff decided that we might as well redeem the time while we’re there. Then after that whirlwind trip I’ll will be home for a few weeks before heading out at the end of month to Rob Arnott’s fabulous advisory council meetings, this time at Pelican Hill in Newport Beach. Those of you who know Rob and Research Affiliates know that his conference is a tad more academic than most, but he combines the intellectual heavy lifting with a fabulous food and party experience. It’s kind of like Adult Nerd Heaven. Then the following week I’ll be in New York, speaking and attending a conference.

I want to give a shout-out to my research associate Patrick Watson. Patrick went to work for me for the first time some 25 years ago, and we have worked on and off together for all the intervening time. About 10 years ago he struck out on his own and began to do research for other publishing firms, ghostwriting a lot of famous people’s newsletters and learning a great deal. With my research and writing schedule getting away from me after 15 years of Thoughts from the Frontline, I needed help. I have hired other research assistants over the years, and it has never really worked. But for whatever reason, Patrick and I really click and seem to bring out the best in each other. I know he has helped me be more productive; and given the pressure to write this next book, I don’t think I could keep all the balls in the air without him.

And speaking of the book, my research groups are beginning to put chapter outlines and research together, and most of the chapter groups are hitting their time targets. In my experience, that means we’ve come to the second most important part of the book-writing process: the no-more-excuses-not-to-begin-churning-out-copy part. The most important part, at least to my ADD brain, is when you get to the “oh-my-God-I’m-not-going-to-make-my-deadline” moment. It is actually useful when those two points coincide. In fact, now that I think about it, they almost always do. Nothing like a looming deadline and no excuses to get your derriere in gear. It helps that I am totally into the whole intellectual process of trying to figure out what the world will look like in 20 years.

Just for the record – and I’ve told my researchers this – I expect we will get a lot wrong. The future is by definition unknowable. I will be more than happy if we get the direction right. Lots of chapters will offer dual scenarios, but that’s okay. That’s not unlike what we do in business: you have your base plan, but you’re aware of all the other things that could happen that might change your operations. And hopefully the surprises are pleasant…

Before I hit the send button, I want to give you a link to Peggy Noonan’s latest essay. I think Peggy may be the finest, most powerful essayist of my generation. She thinks with clarity and writes in a fluid writing style that propels you along on her hurtling thought train, rarely ever pausing to give you a chance to get off, until you realize you’ve arrived at what should have always been your own conclusion. Young writers, if you want to know how to turn a phrase and see what writing should feel like after you’ve written it, you should study everything Peggy has penned.

If you want to write science fiction, you have to read J.R.R. Tolkien, Isaac Asimov, and Robert Heinlein. They are the masters. But if you want to write political essays and persuade people to a point of view – and do so in an aggressively literate yet polite manner, you read Peggy Noonan.

Her latest essay, “Trump and the Rise of the Unprotected,” talks about how Trump has managed to collect his diverse and burgeoning following. It is not within the experience of the establishment political class to comprehend what is happening. This phenomenon is more than just Tea Party.

I’ve been involved in the political wars for some 40 years. I’ve seen the back and forth between voters and politicians. This time around, I’ve talked to friends all over the country who do not fit the stereotypes the media has painted of Trump supporters. They are articulate, educated, and successful. They are also frustrated as hell with politics as usual. There are only a few times in American history that even vaguely rhyme with the time we’re in – I think what we’re seeing is unique. When you add the current frustrations of American voters to those of European voters, particularly around the issue of illegal immigration, you come up with real potential for profound change in the world geopolitical scene over the next five or ten years. It’s certainly something to think about, and Peggy sets a great thought table.

The political analyst in me looks at the record-high unfavorable rating for Donald Trump as a national candidate and then looks at Hillary Clinton and sees the same thing. I have a feeling this election cycle could be more negative and downright ugly than any I’ve seen in my lifetime – and that’s saying something. And given the mood of the country, it’s impossible to know what the outcome will be. We are truly in no man’s land here – but hey, it promises to be an adventure.

It really is time to hit the send button. You have a great week and find time to read something fun.

Your trying to wrap his head around the words President and Trump in the same sentence analyst,

John Mauldin

0 comments:

Publicar un comentario