Why Deflation Matters More Than Recession - Part 2

by: SG PrivateWealthBanker

Summary

- There are presently many cases worldwide where selling prices are deflating, yet the cost of goods sold is holding constant or falling at a slower rate.

- Manufacturing inventories are elevated everywhere in the World, and liquidation pressures among global industrial enterprises are considerable.

- A drop in selling prices is often not compensated by a drop in cost of goods sold.

- Wages are rigid on the downside, and labour compensation often makes for a noticeable share of variable costs.

- The deflation trade is alive and well.

- Manufacturing inventories are elevated everywhere in the World, and liquidation pressures among global industrial enterprises are considerable.

- A drop in selling prices is often not compensated by a drop in cost of goods sold.

- Wages are rigid on the downside, and labour compensation often makes for a noticeable share of variable costs.

- The deflation trade is alive and well.

Why deflation matters more than recession - Part 2.

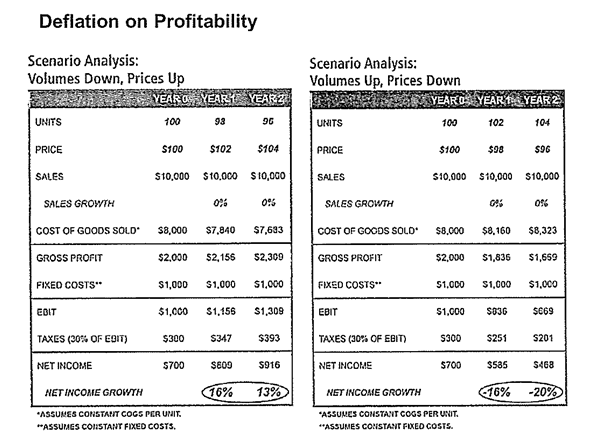

After the publication of ' Where Deflation Comes From And Why It Matters More Than Recession? '' earlier this month, as I received a lot of comments and questions, I have decided to update this previous article, giving more details on the subject. To refresh readers' memories, we are republishing the table that illustrates that a 2% drop in output prices and a 2% in units sold causes profits to contract by double-digit rate. Meanwhile, the inverse - a 2% drop in volumes and a 2% rise in prices - produces double-digit profit growth. In these examples, we maintain the cost of goods sold per one unit (variable costs per unit) and fixed costs remain constant.

Source: BCA Research.

Source: BCA Research.

True, if one were to reduce the cost of goods sold by the same percentage as the deflation in output prices, profits would not be more sensitive to a drop in prices than to a decline in volumes. However, there are presently many cases worldwide where selling prices are deflating, yet the cost of goods sold is holding constant or falling at a slower rate. In particular:

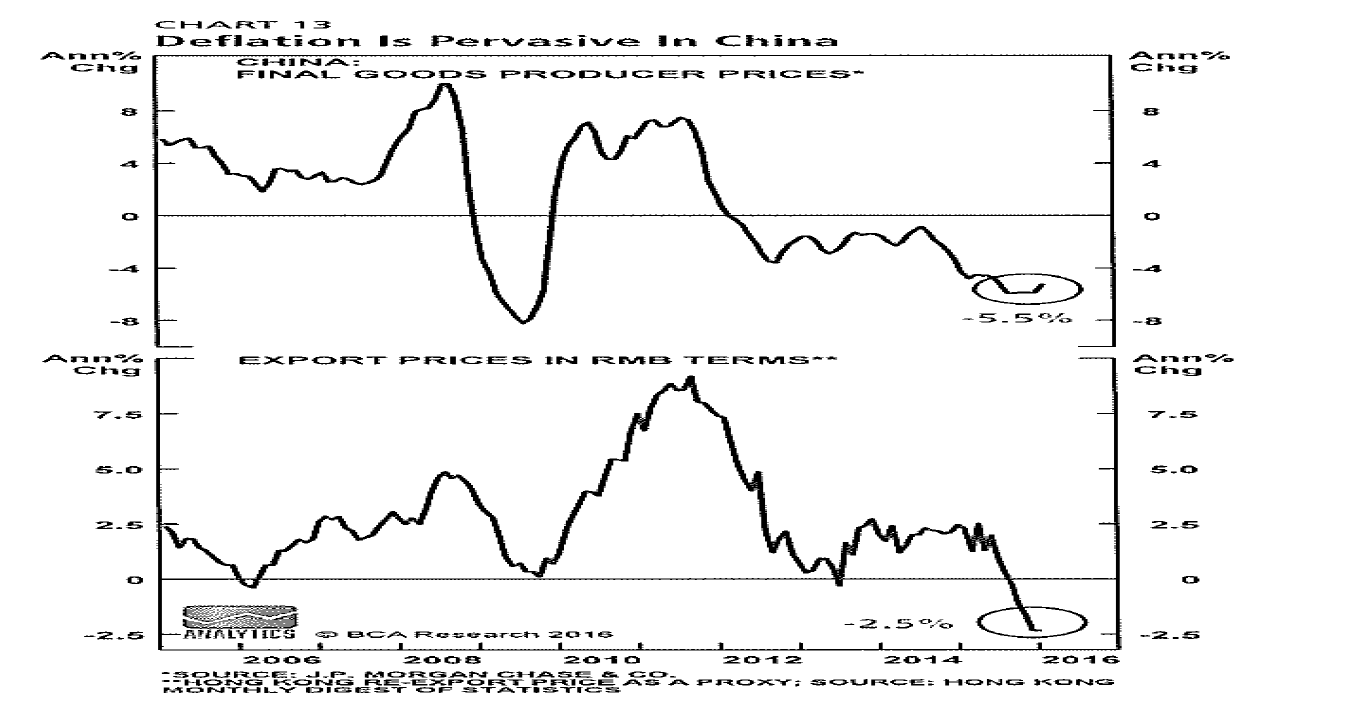

- Final output goods prices in China are deflating by 5% and export prices are falling at annual rate of 2.3% in RMB terms. At the same time, industrial wages in China are still growing.

Source: BCA Research.

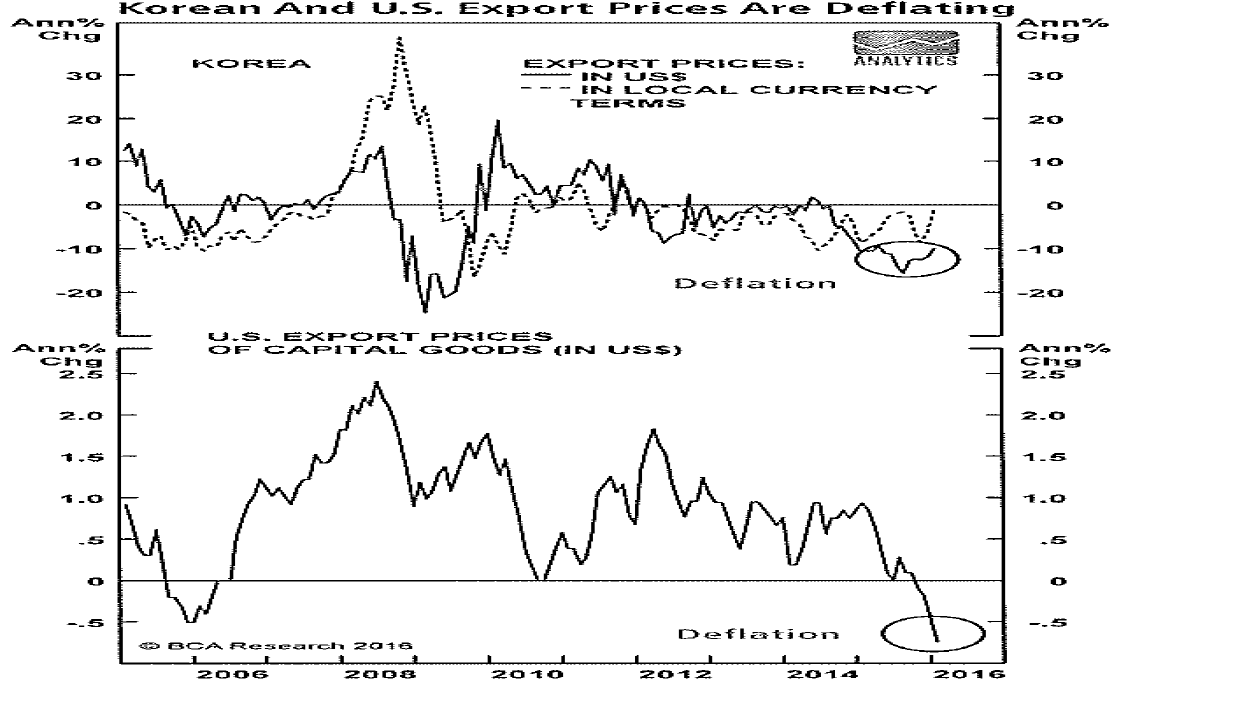

Source: BCA Research.- Now consider the example of Korean or US industrial firms that are competing with their Japanese and German counterparts. Due to the EUR and JPY depreciation over the past few years, let's assume German and Japanese companies have been able to cut their USD product prices by 10%. In order to preserve market share both worldwide and domestically, let's also assume that Korean and US industrial firms have matched the price reduction of their competitors by also cutting prices by 10% in USD terms. Notably, Korean and US export prices are deflating rather rapidly.

Source: BCA Research.

Source: BCA Research.Nevertheless, wages at Korean and US companies are not contracting, but rising in their local respective currencies. Provided wages are a sizeable part of the cost of goods sold, the latter cannot deflate much, even if non-wage input prices decline. Consequently, the cost of goods at these US and Korean industrial firms cannot drop as much as the deflation in their output prices.

- Moreover, manufacturing inventories are elevated everywhere in the world, and liquidation pressures among global industrial enterprises are considerable. As these producers have to cut their selling prices to liquidate their inventories, the impact on their profits will be devastating, even if their volume rises. The reason is that the costs for production of these goods have already been incurred and cannot be reduced.

Meanwhile, fixed costs are constant not only in the short-run but even in the medium-term.

Therefore, our thesis that deflation can lead to profit contraction without a decline in volumes is, by and large, reasonable. As such, it should not be surprising to witness contracting profits among industrial firms in many countries, even though their GDP growth remains positive.

0 comments:

Publicar un comentario