The Cliff Is Nigh

by: Scout Finance

- PMI and global trade are showing declines.

- GDPNow is reversing course and is predicting 1.9% growth in Q1. That is too high.

- The level of unsecured debt is higher than in 2008 making the 2016 economy possibly worse than during the financial crisis.

- GDPNow is reversing course and is predicting 1.9% growth in Q1. That is too high.

- The level of unsecured debt is higher than in 2008 making the 2016 economy possibly worse than during the financial crisis.

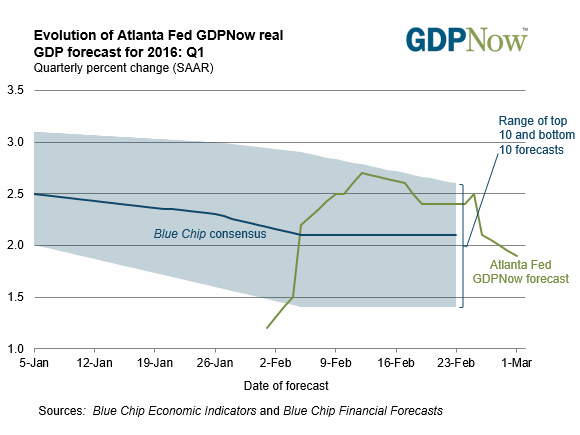

The prediction of a lower GDPNow report in my last post was correct as the estimate for Q1 growth went from 2.6% to 1.9%. The original point still holds, the GDPNow report will have to go lower in the next few weeks as the data is negative on the U.S. economy. PMI showed its first reading below 50 coming in at 49.5. Global trade declined 13.8% in 2015 spurred by the slowdown in emerging markets particularly China. This is the worst decline since the financial crisis.

I have made the point expressing the possibility that the recession could begin in Q4 2015 to evidence my bearishness on economy. My best bet has always been a Q2 2016 recession. The latest revision of Q4 GDP went from 0.7% to 1%. However, this was not considered good news because the level of inventories were revised from up $68.6 billion to up $81.7 billion.

Inventories increasing means production increased, but demand didn't match this. This leads to discounting to get rid of the excess inventory. This lowers profits margins. Instead of imports increasing 1.1%, they declined 0.6%. This decline in trade is consistent with other trade metrics such as the large decline in Chinese trade. Global trade is a sign of a healthy economy as trade is a mutually beneficial situation unlike what Donald Trump has been stating in his stump speeches. This decline shows the potential for a global recession in 2016.

As I showed in a previous post, the bond market tells the consistent truth about where the economy is going, while the stock market has greater countertrend rallies. The stock market is more volatile partially because it is smaller than the equities market. Regardless of the reasoning, the bond market has been consistent with its portrayal of a recession becoming increasingly more likely. As you can see from the chart, as the equities market has been experiencing a countertrend rally, the 10 year - 2 year spread has shrunk. It's currently at a cycle low 96 basis points.

The recession has been likely for quite a while. As we head into it in the next few months, the question will switch from "will there be a recession?" to "how bad will the recession be?" I lean towards thinking this recession will be very bad because the level of debt has increased since 2008. As you can see from the chart below, the amount of senior unsecured debt has increased quite rapidly over the past several years.

{kind=link}

Each recession has bigger and bigger consequences as the debt level increases. When the Federal Reserve has low interest rates, it causes malinvestment as investors search for returns in a low rate environment. This causes capital to flow more into equities markets and other risky assets such as junk bonds. Eventually the situation unravels. The business cycle is ending and the Fed is at near zero interest rates. Therefore, the Fed has little wiggle room to deal with a recession.

0 comments:

Publicar un comentario