Open

Letter to the Next President, Part 3

By John Mauldin

“The

liberating army we need in the Americas today is one of leaders who come

together in peace, in the spirit of cooperation.”

–

Oscar Arias

“There

are two Americas – separate, unequal, and no longer even acknowledging each

other except on the barest cultural terms.”

–

David Simon

Today

we continue my series of open letters to the presidential candidates. In the

meantime, we’ve drawn a little closer to knowing whom the two major parties

will nominate. A few people are vowing to consider minor parties, too.

In any

case, whoever replaces Barack Obama will face a world of challenges. The good

news is that most (not all) of the challenges are manageable – given the

willingness to make very difficult choices. Remember, in this letter we are

focusing on the economic realities that the new president will face, and those

realities will force stark choices in other arenas such as healthcare, defense,

and geopolitics. The economic picture is unequivocal – more so than in any era

since Roosevelt – and will compel the president to either choose among merely

very difficult options at the beginning of his or her term, or to put off

choosing and be left with only seriously bad choices toward the end of a first

term. There will be no easy choices, and the process will be messy, but I think

we’ll will muddle through.

In Part

1 we looked at China and Japan. Part

2 covered Australia, India, the Middle East and Europe. That leaves Africa,

South America, and North America. Let’s dive back in.

Dear

Presidential Candidates:

Many

Westerners still think of Africa as the Dark Continent – a mysterious, unknown

place brimming with danger. Many Africans think the same of the West. Faraway

lands are always mysterious and a little forbidding until you visit them, or at

least try to learn about them.

Having

been, at last count, to 15 African nations, I have learned how little I know

about Africa. It is a land of astonishing economic and cultural diversity. As

president, you shouldn’t have an African policy – you should have a whole

series of policies for different parts of Africa. One size will most definitely

not fit all.

You

should also remember that your actions as president will have consequences for

future presidents. Demographic projections suggest that by the year 2100

Nigeria will have a larger population than China will. Africa is going to make up

for lost time. From an economic standpoint, Africa as a whole is unlikely to

directly impact the United States for years to come, but there is an

opportunity in Africa that we have neglected for 100 years.

Owing

to the original colonial presence of the European powers, the various nations

of Africa are still economically connected to Europe. I remember being in Zaire

(now Congo), and meeting a young man who, oddly enough, is now one of the

country’s leading politicians. Kinshasa was a town of multiple millions of

people, and the local TV station did a story on “the” American who was visiting

and looking to do business. Talking with the European expatriates there, I was

left with the impression that in the early 1990s there may have been fewer than

100 adventurous souls from the United States on the whole continent. Given the

ease with which Europeans bribed their way into business in the countries I

dealt with – and the fact that if a US businessman acted similarly, he would go

to jail – US entrepreneurs started with one hand tied behind their backs.

Thankfully,

attitudes and practices are changing, and there is an anticorruption movement

in a host of African countries today. Africa is going to be one of the growth

stories of the coming 30 years, and it is a place where US businesses should

definitely be involved. The US can facilitate that involvement by appointing

ambassadors who are not just career diplomats looking to check another box on

their résumés but are instead actually US businessman with connections who can

introduce US businesses that would like to get involved. Not only would this

approach help our trade balance, it’s just good basic policy. In general,

Africa doesn’t need aid, but it does need our business acumen.

Oddly

enough, Africa’s relative lack of development may help it leapfrog the rest of

the world. Instead of slowly replacing outmoded telecom and energy

infrastructure, Africa is right now expanding mobile internet and solar energy

capacity faster than some developed nations are. Kenya’s M-Pesa payments

platform is helping millions of the “unbanked” enter a thriving economy, even

as the US struggles to adopt microchipped credit cards.

South

Africa, where I have many good friends, is struggling a bit from the

commodities downturn and some unwise decisions by the Zuma government. (I have

met with Zuma three times, and each time he affirmed that he wanted to create

economic growth and change. Instead, he has done nothing and made the situation

far worse.) Thankfully he will be leaving soon, and South African

businesspeople may once again have an opportunity to prosper.

As

president, you can set up the US to have good relations with Africa, or you can

create damage that will take decades to fix. Choose wisely.

Our

next flight takes us westward to South America. Here we find a blend of good,

bad, and very bad news. We’ll start with the country in the worst fix, which is

definitely Venezuela. The word meltdown

is no exaggeration here. Years of socialism are having the predictable result.

Unlike

the Socialism Lite that Senator Sanders represents, Venezuela has the real

thing. Government controls the means of production and so produces the wrong

things. The result is massive inflation and a crazy mix of excesses and

shortages – but no shortage of misery.

The

oil price collapse hasn’t helped. Venezuela’s high production costs made it one

of the first victims of the downturn and will also make the country’s recovery

that much harder. I do not know a painless way to pull Venezuela out of its

hole. I feel terrible for the people who must live in this manmade economic

disaster zone.

A

collapse in Venezuela could lead to a possible interruption in a significant

part of our oil supply. It’s not that there’s not plenty of oil in the world,

but many of our refineries are set up to handle the rather thick, low-grade oil

that comes from Venezuela. Retooling the refineries would be time-consuming and

very expensive. There is little that you as president can do to keep

Venezuela’s oil flowing, but the situation is one to watch.

You

will not be able to ignore Brazil, the world’s eighth-largest economy and

fifth-most populous country. The outlook there is better than in Venezuela, but

not by much. You are no doubt aware of the enormous scandal that is going on at

the highest levels of government over bribery and corruption charges involving

major government figures and Brazil’s national oil company, Petrobras.

President Dilma Rousseff is deeply implicated and will likely face impeachment.

A recent conversation between her and former President Lula has been made

public and furthers the impression of corruption.

The

Brazilian economy shrank 3.8% last year and is still heading south. It is not

likely to turn around until the political situation has been settled. Ordinary

Brazilians are making their displeasure known through massive street protests,

but it is hard to know from afar exactly who is unhappy with whom. Brazil’s

poorest have been in dire straits for a long time. The wealthy Brazilians caught

up in the scandals also control the country’s media outlets.

Making

a bad situation worse, the mosquito-borne Zika virus has brought to Brazil a

heartbreaking wave of deformed infants, with more on the wayexpected. And the

country will host this year’s summer Olympics, diverting resources from the

other problems and showing the whole world a nation in distress. (The Zika

virus is a real concern, as it is likely to come to the United States sooner or

later, and the Southeastern part of the US is home to the type of mosquito that

carries the virus.

There are companies developing both a cure and a preventive

vaccine, but their efforts are bogged down in bureaucracy, which you as

president could cut through.

As

with Venezuela, you may not be able to help Brazil much, but you also can’t

ignore it. US businesses and investors poured capital into Brazil when it

looked like a promising emerging market. Those investments don’t look so hot

now.

Argentina

is another economic basket case, but one that actually appears to be improving.

Argentina cycles through huge ups and downs. The government defaulted on about

$100 billion in international debt back in 2001. It is now in final

negotiations with some creditors who declined to accept previous restructuring

offers. If the parties can reach a deal, Argentina will again have access to

global capital markets.

That

deal can’t happen too soon. New President Mauricio Macri says he will reduce

deficit spending and keep inflation down to “only” 20–25%. He has already

lifted currency controls and done away with agricultural export tariffs. These

are important steps but only a beginning.

Finally,

let’s head up to Mexico, our North American neighbor and trading partner. I

find it stunning how ignorant most US citizens are about Mexico. On a

purchasing-power-parity basis, Mexico is the 11th-largest economy in

the world – larger than Italy, South Korea, Canada, Australia, or Spain. It is

generally growing faster than the countries ahead of it on the list. It is not

located in a faraway continent like Africa – many of us could easily drive from

our homes to the border in less than a day. Yet we still have a caricatured

view of Mexico. The caricatures do fit in some instances, but Mexico is so much

more.

My

colleague George Friedman recently shattered some misconceptions in an

excellent article, “Mexico

as a Major Power.” A quick excerpt:

Mexico

is commonly perceived, far too simplistically, as a Third World country with a

general breakdown of law and a population seeking to flee north. That

perception is also common among many Mexicans, who seem to have internalized

the contempt in which they are held.

Mexicans

know that their country’s economy grew 2.5 percent last year and is forecast to

grow between 2 percent and 3 percent in 2016 – roughly equal to the growth

projection for the US economy. But, oddly, they tend to discount the

significance of Mexico’s competitive growth numbers in a sluggish global

economy.

Here,

therefore, we have an interesting phenomenon. Mexico is, in fact, one of the

leading economies of the world, yet most people don’t recognize it as such and

tend to dismiss its importance.

Some

of you candidates are having great success spinning Mexico as some kind of

conspiracy of nefarious people wanting to sneak into our country and do us

harm.

Yes, people do cross the border illegally and ought to be stopped. But

the irony is that today more Mexicans here illegally are going back to Mexico

than are coming in.

This has been the case since the Great Recession hit. Over

one million Mexicans, including US-born children, have left the US for Mexico

since 2009, far more than have entered illegally. They cross the border headed

south because they see better

opportunities in Mexico than they do in the US. That is the real problem you

should talk about – and try to change, if you reach the White House.

I am

not arguing that we don’t need to control our borders. Of course we do. Every

nation should. But we need to remember that we have right next door to us a

country that is quickly becoming an industrial powerhouse. In 20 years Mexico

is likely to be one of the five largest economies in the world. We need to

figure out how to do more business with Mexico, not less. The country is going

to become a huge potential market for us.

Our

other neighbor, Canada, managed to avoid much of our last financial crisis, but

its turn finally came. Instead of housing, it was energy prices that pushed

Canada toward the edge. The country is now in a technical recession, one from

which the new Justin Trudeau government promises it will escape by resorting to

old-fashioned fiscal stimulus. Keynes himself would be proud.

Will

Trudeau fail? Maybe, but it won’t be for lack of trying. The forthcoming

deficit spending will add to an already significant debt burden. I would be

very concerned if I were a Canadian. Thegovernment is well on its way to

amassing the kind of permanent debt burden we enjoy (?) here in the US.

The

whole point of fiscal stimulus is to boost consumer demand. Give people cash

and they will buy more stuff. Yet lack of demand is not Canada’s problem,

especially in the energy-driven provinces. Depressed oil prices are the

problem. Trudeau’s stimulus plans will do nothing to raise oil prices. That

problem is far outside his control.

I fear

Canada will fall into the same trap we are in. We ran deficits thinking they

would restore growth, boost tax revenue, and let us pay down our debt. In fact,

we got growth that is mild at best, not enough tax revenue, and yet more debt.

As I

wrote recently, growth

is the answer to everything. Enable economic growth and your other presidential

mistakes won’t matter so much. Suppress growth and even your best efforts will

not be enough to move us forward.

On

that note, we finally arrive back home.

Obama

announced a pivot to Asia at the beginning of his last term. Given the

importance of Asia to the world’s future, that is an understandable decision.

But in the next four-year term, economic reality is going to force the

president to pivot his or her focus back to the United States. There are a

number of factors coming together that are going to require serious crisis

management.

When

you take office in January 2017, the weakest recovery in modern history will

have stretched on for 81 months. It will already be the third-longest recovery

without a recession since the Great Depression. By 2018 it will be the second

longest. Only during the halcyon economic daze of the 1960s have we seen a

longer recovery; but that record, too, will be eclipsed sometime in 2019 – if

we don’t see a recession first. And note that we were growing at well over 3%

in the ’60s, not the anemic 2% we have averaged during this recovery and

certainly not the positively puny 1.5% we have endured lately. As we have

surveyed the economic scene around the world for this series of letters, it has

been clear (and IMF and BIS data confirms) that global growth is slowing down.

Given the fact that the US economy is barely growing at stall speed, it won’t

take much to nudge us into recession.

The

odds that you will see a recession during your first four years are therefore

quite high. Maybe not in your first year in office, but a recession is

something you need to plan for. Given the fiscal reality that you will be

facing and the limited number of arrows left in the Federal Reserve’s monetary

policy quiver, your administration is going to have a difficult time dealing

with the fallout from a recession.

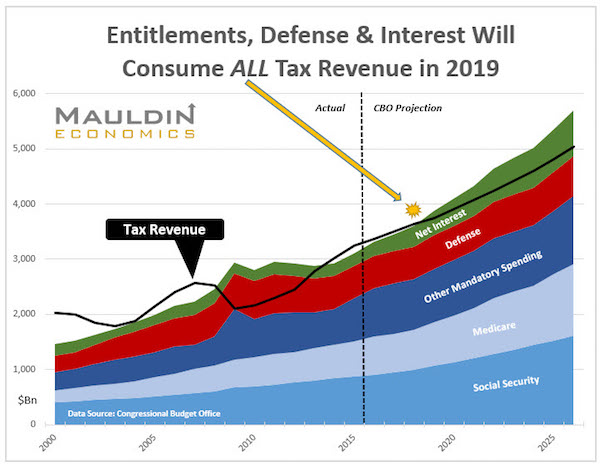

Let’s

look at fiscal reality. Sometime in your first year the US national debt will

top $20 trillion. The deficit is running close to $500 billion, and the

Congressional Budget Office projects that figure to rise. Add another $3

trillion or so in state and local debt. As you may imagine, the interest on

that debt is beginning to add up, even at the extraordinarily low rates we have

today.

Sometime

in 2019, entitlement spending, defense, and interest will consume all the tax

revenues collected by the US government. That means all spending for everything

else will have to be borrowed. The CBO projects the deficit will rise to over

$1 trillion by 2023. By that point entitlement spending and net interest will

be consuming almost all tax revenues, and we will be borrowing to pay for our

defense. Let’s look at the following chart, which comes from CBO data:

By

2019 the deficit is projected to be $738 billion. Almost every president wants

to run for a second term. To forge any hope of being successful with that

second run, a president needs to able to say that he or she made a difference

on the budget. There are only three ways to reduce that deficit: cut spending,

raise taxes, or authorize the Federal Reserve to monetize the debt. At the

numbers we are now talking about, getting rid of fraud and wasted government

expenditures is a rounding error. Let’s say you could find $100 billion here or

there. You are still a long, long way from a balanced budget.

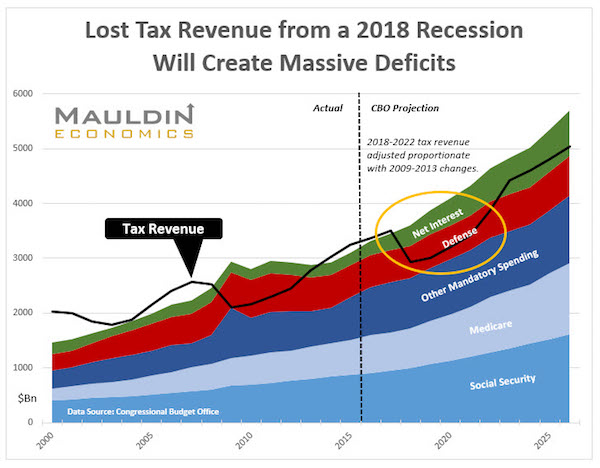

But

implicit in the CBO projections is the assumption that we will not have a

recession in the next 10 years. Plus, the CBO assumes growth above what we’ve

seen in the last year or so. Let’s contemplate what a budget might look like if

we have a recession. I asked my associate Patrick Watson to go back and look at

past recessions and determine what level of revenue losses occurred because of

the recessions, and then to assume the same average percentage revenue loss for

the next recession. We randomly decided that we would hypothesize our next

recession to occur in 2018. Whether it happens in 2017 or 2019, the relative

numbers are the same, and so is the outcome: it would blow out the budget.

Here’s a chart of what a recession in 2018 would do. Entitlement spending and

interest would greatly exceed revenue.

The

deficit would balloon to $1.3 trillion, and if the recovery occurs along the

lines of our last (ongoing) recovery, then unless we reduce spending or raise

revenues, we will not see deficits below $1 trillion over the following 10

years. The deficit will climb to $1.5 trillion just as you dive into the thick

of your second campaign in 2020. Not exactly a great campaign platform.

But

before I get all gloom and doom on you, let me say that I think there is a path

by which you can actually prevent a recession. There is a path to stimulating

growth, creating new jobs, and spurring a real economic recovery – but not by

doing the same things we have done for the past 16 years. If we continue in the

same general direction that we have been going, the economic realities I talked

about above are going to clobber you and what will be a very scared Congress in

the next four years.

No

Senator or Representative is going to want to run for election in the middle of

a recession, with deficits topping $1 trillion. If you think people are

vehement in demanding change today, they will really be out with the pitchforks

in 2018 in 2020 if we don’t get a grip on our budget and our economy. If we

can’t figure out how to engender growth and create new jobs – and real jobs – the general

rejection of “establishment candidates” will continue to intensify. You have an

opportunity to really change things, and the public clamor should give you a

great negotiating base for forcing Congress to deal with the realities in the

above charts.

But

you are going to have to have a plan, and that is where the rubber meets the

road. Every president chooses a chairperson for his or her Council of Economic

Advisers. Whom you should choose is going to be in large part a function of the

type of policies you will try to pursue. In the past, presidents have tended to

choose an economic advisor who was more or less mainstream (great academic

background, general acceptance in the economic community, etc.) –in short, an

establishment economist.

And I

don’t want to demean economists, but presidents and politicians of all stripes

tend to choose economists who will tell them what they want to hear. If you

feel that a certain policy is needed, you can probably find an economist who

will give you a well-thought-out academic justification for what you want to

do.

You

are going to be faced with problems that are the culmination of hundreds if not

thousands of previous decisions by US presidents and governments.

If you

choose to listen to economists who tell you that you can continue to run large

deficits – and you can find Nobel Prize-level economists who will oblige you –

the country will generally continue in the same direction it has been going

until the only real choice will be the one faced by Japan a few years ago: they

essentially realized they had to monetize their debt, and over time that

decision is going to significantly reduce the value of their currency and thus

the buying power their citizens depend on.

For

some economists, deficits are not a problem. They look at economists who argue

for a balanced budget and reduced leverage as antediluvian throwbacks. They

seem to feel that a small group of well-educated economists know how to run the

world economy better than the market of billions of people working in their own

self-interests can run it. They see a market-run economy as messy and

inefficient, prone to all sorts of problems.

Sadly,

there is no nirvana. Economic policy comes down to philosophical choices.

And

they are ones you are going to have to make.

Radical

monetary policy such as is being applied by developed-world central banks is

one of those things that work well in theory but not in practice. In theory,

ultra-low rates and quantitative easing are supposed to generate a boom in

investment and spending, which in turn will lead to growth and jobs. However,

we can look around the world where these solutions are being applied and see

that growth is lacking. And as nearly all economists agree, growth is the one

thing that can get us through the problems that are coming. There are just some

minor quibbles about how that growth should be achieved!

And

this is all before we even start talking about the accelerating pace of change

in the business and technological worlds, a global network of trade and other interactions

among countries that is vastly more complex than it was even a decade ago, and

the increasing dissatisfaction of a large group of citizens who feel left out

of the new era. As science fiction writer William Gibson said back in 1993,

“The future is already here. It’s just not evenly distributed.”

Of

course, I’m just focusing on the economic decisions you will have to make.

People will be pressing you to somehow solve a myriad of other problems as

well.

You

are going to get a great deal of advice as to what economic path and solutions

you should choose. The choices you make will determine the future of this

country and to a great extent the future of the world. That pressure and impact

comes with the Oval Office. You have chosen to step into that office at a

particularly stressful time in US and world history.

However,

the situation is merely hopeless but not critical. There are choices you can

make that I believe will reinvigorate the American economy and enable us once

again to grow at 3%-plus, deal with the deficits and debt, and as a side

benefit solve the problem of how to deliver healthcare. Choosing the right

economic team can make that transition doable. And you will actually have the

advantage of a potential crisis unfolding in your first term that will force

both sides of the political divide to seriously consider and agree on

outside-the-box solutions. You just have to come up with those solutions, as

very few embroiled in the partisan debate will see past their own time-worn

answers to conceive truly unique, workable, and productive policies.

Next

week I’m going to outline some of the policies that I think have the potential

to do all that. I can guarantee you that there are elements in my proposals

that will annoy almost everyone, but that is the nature of a compromise –

nobody gets everything they want.

If on

the other hand you’re content to go along in the same direction we are today,

with only minor course adjustments, I can just about guarantee that we’ll will

end up on the shoals, where all of your choices will be bad ones.

I fly

out on Monday for Rob Arnott’s fabulous annual client conference, where he

brings in some of the leading economic thinkers of the world to hash out

portfolio construction. The fact that he is one of those leading thinkers helps

him attract others. It is one of the few conferences I attend where I sit in

the back of the room and take notes and only rarely have the temerity to ask a

question. I have learned that you do not go head-to-head with Harry Markowitz

unless you are on really solid ground. The last time I was at the gathering, a

few years ago, I looked around and saw about $1 trillion of managed capital in

the room. And there were only about 50 people. Who take this stuff rather

seriously.

Next

week I go to New York and Chip Roame’s Tiburon gathering, which is essentially

for idea sharing and networking among financial services executives, focused on

what’s happening in the industry. I’m really looking forward to it. It looks

like a little media time is being slipped in here and there as well, and I will

let you know. Then I’m back to Dallas, where I go back to work on my book (like

I can ever forget about it – the weight of deadlines hangs heavy) before I head

out in the middle of May for Abu Dhabi; work in a quick trip to Raleigh, North

Carolina; and then fly home in time for my conference in Dallas.

Now,

I’m going to close with a story that I was reminded of as I was writing about

Africa earlier. As I said, I’ve been to about 15 African countries, mostly

during the ’90s, for a business venture I was pursuing. It was an expensive but

interesting pursuit. Back then pretty much every major capital had a few hotels

where all the foreign travelers and expatriates gathered. More often than not

the hotel was an Intercontinental. I learned that if I went to the bar toward

the end of the evening, I could meet old Africa hands who had been banging

around the continent for decades, and for the mere price of a drink they would

begin to tell me stories. And such marvelous stories. There were a few times

when I simply marched up to the bar and loudly announced, “I will buy the

drinks for the best Africa story in the room.” Somehow it seemed that the last

liar of the evening always won. Those were great times, and if you ever get a

chance to do som ething like that you should, though I am sure that Angola and

Mozambique and Congo and Côte d’Ivoire have all changed. Given the hellholes

that some of them were, that is a good thing.

So let

me relate my favorite African story. It was told to me by Pat Mitchell, who had

lived all over Africa for 30 years by that time, working as a lawyer after he

graduated from Stanford. The story was about his friend Alejandro Beradone, an

Argentinian running (I believe it was) a Rayovac battery-manufacturing plant in

Kinshasa, Zaire. I later met Alejandro, and we became friends and met on a few

occasions in Buenos Aires, where he introduced me to the concept of going out

to a steak dinner at 10:30 PM, which is considered normal behavior in Buenos

Aires. But then a lot of interesting things are considered normal in Buenos

Aires.

It

seems that the French Foreign Legion had a small outpost in Kinshasa. They came

to Alejandro and asked him if he would sponsor a four-man team to go to Liberia

to compete in a parachuting contest. He agreed, with the stipulation that he

and his 12-year-old daughter could go along. So a few weeks later they

chartered an eight-seat, twin-engine plane and flew to Liberia. It turned out the

French team won the contest, so they all went out and partied very hard, along

with the pilot (as is the wont in Africa), and then stumbled back onto the

plane the next morning. The pilot got them up into the air, set the controls on

autopilot, and told everyone to wake him in three hours. At which point

everyone promptly went to sleep.

Somewhat

more than three hours later, someone woke up and roused the pilot. He looked at

his instruments and got quite upset that nobody had awakened him. The plane was

running out of fuel. The pilot pulled out his maps and looked for an airfield

where he could set the plane down. The only real option was a grass field in

the People’s Republic of the Congo, a former French colony that was essentially

socialist/communist and really didn’t enjoy warm relations with the French, to

say the least. So when the plane landed, it was immediately surrounded by

guards who pretty quickly figured out that the French Foreign Legion was

aboard. They detained the group, took them to the capital city (Brazzaville),

and put them all in jail. The government decided that this was an international

incident because the French were clearly invading the country. It was a big

deal in the local papers. They put the entire group, including Alejandro’s

daughter, into the cell w ith him. Understand, this was an African jail. Not

exactly luxurious.

There

was basically no food, so the guards would come in and say, “Give us some

money, and we’ll go get you some food.” It didn’t take more than a few days before

they ran out of cash. They were still hungry, though; and the guard asked,

“Don’t you have any other way to pay?”

Alejandro

reached into his pocket and pulled out his American Express card. The guards

took one look at it and exclaimed, “Why didn’t you tell us about this in the

first place?” Then they gathered them all up and installed them in suites at

the Meridian Hotel (the finest hotel in the city), where they stayed for the

remainder of their “detention,” basking in luxury. (Remember, il est l’Afrique. Different

rules.)

That,

to me, is the ultimate “The American Express card – don’t leave home without

it” story.

You

have a great week. Walk into a bar or bang on your glass at a dinner gathering

and announce, “Everybody has to tell a story,” and then sit back and enjoy the

evening. I have never really found anybody who didn’t have a story. You’ll be

glad you asked, and you’ll walk away with a smile.

Your

always ready for a great story analyst,

John Mauldin

0 comments:

Publicar un comentario