Interest Rates: Another Ominous Signal For The Market

by: Brendan O'Boyle

Interest rate cuts signal central banks are expecting the economy to slow.

In the past declining rates have preceded recessions and troubled times for investors.

Most often this signal occurs after an inverted yield curve, but today this may not be the case.

In the past declining rates have preceded recessions and troubled times for investors.

Most often this signal occurs after an inverted yield curve, but today this may not be the case.

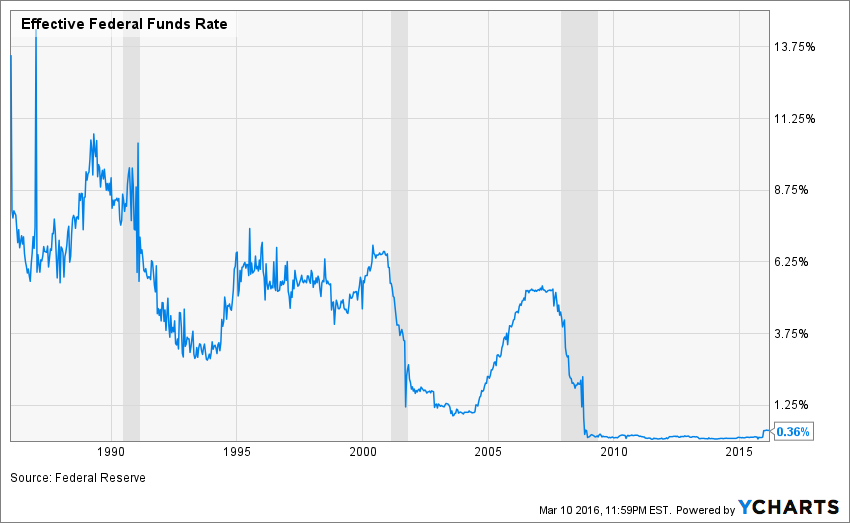

With central banks, most notably the ECB and Japanese Central Bank, cutting interest rates to deeply negative levels recently the consequences on the future direction of the stock market should be examined. As yet, the Federal Reserve is still in a tightening regime, but the pace of tightening is set to slow. It seems very unlikely now that the initially expected pace of rate hikes will be realized, instead forecasters expect one or two rate increases by the end of 2016 with the Fed funds rate most likely falling between 0.5 and 0.75% (39.3% probability). When the Federal Reserve began raising rates a 1.375% Fed Funds rate was anticipated by year-end 2016, implying four rate hikes. Currently, the market is implying odds of this occurring at around 2%.

These odds have considerably lessened in the previous several months while rates in Japan and the European Union have fallen. Effectively, as soon as positive rates emerged the market has begun to price in either a slower pace of increases or an outright cut in interest rates. Market participants are expecting a weaker economy and more accommodative central bank policies, not historically a favorable environment for stocks.

Over the past 50 years periods of declining interest rates are correlated with worsening economic conditions and a falling stock market. In fact, the Federal Reserve's first interest rate cut on September 18th 2007 perfectly timed the top of the 2002-2007 bull market.

Falling interest rates in late 2000 and 2007 were an ominous sign. In 1990, rates fell probably too late to be a useful timing signal. Rates then continued lower under Greenspan in the 1990's.

Why is this the case? Lowering interest rates is a tool that has a two-fold purpose. The first purpose is the discourage savers from hoarding cash and to spend it in the economy. This is relatively simple, if I earn a 5% interest rate on my savings account I should be more willing to part with it at 2% interest. The problem at the present time is that savers have not yet been encouraged to spend they are unlikely to do so if interest rates are cut from 0% to -1%.

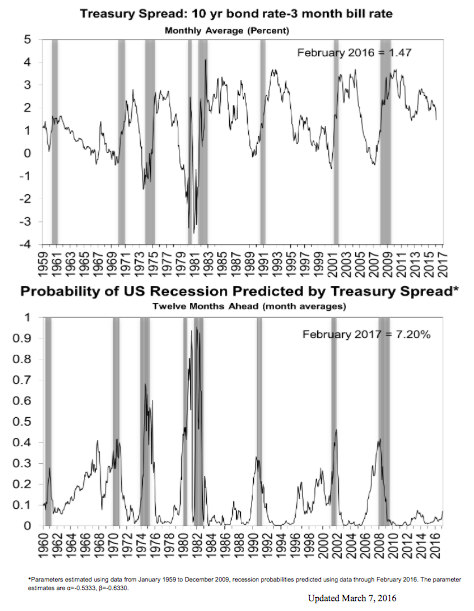

Second, lowering interest rates encourages banks to make loans. Banks borrow at the short-term rate and lend at longer-term rates. Thus, the rate on a 10-Year Treasury Note minus the rate on a 3-Month Treasury Bill is somewhat proportional to the profit a bank can expect from a loan. Typically before a recession begins the Treasury Spread is negative or almost negative.

Fixed income investors pile into longer dates securities because they expect interest rate cuts to come. Additionally the short-term rate is already high leading to a spread that is negative. This is also known as an inverted rate curve and it means that for a bank making loans is less attractive. The central bank by lowering the short-term interest rate can increase this spread.

So if central banks are trying to prop up the economy by lowering interest rates why are such actions typically ominous signals for the stock market and the economy? Inverted yield curves have signaled the past seven recessions with no false signals (although some early signals) when the yield on a 3-Month Treasury Bill exceeded that on a 10-Year Treasury Note. The problem is that the cuts are only performed because the economy is deteriorating. While central planners can try to stimulate the economy, they are not more powerful than the economic cycle. Thus, interest rate cuts are most often simply a warning that something is wrong.

Another important point regarding the previous graph must be mentioned: At the present time an inverted yield curve is not possible! In other words, when a 3-Month Bill yields almost zero it is almost impossible for a 10-Year Note to yield less. This is historically quite anomalous and it means that we cannot expect a spread of less than zero. Instead, we can only be aware that the lower the spread the greater the danger. We almost certainly will not be warned of the next recession by an inverted yield curve!

For all of this year the spread has fallen, although it has rebounded in the past several weeks.

What this means is that while the S&P 500 (NYSEARCA:SPY) is discounting approximately the same odds of recession as in January (-1.1% YTD), the Treasury market sees a higher probability of challenging economic conditions.

What this means is that while the S&P 500 (NYSEARCA:SPY) is discounting approximately the same odds of recession as in January (-1.1% YTD), the Treasury market sees a higher probability of challenging economic conditions.

As I have stressed in previous writings knowing the exact direction of the market is impossible.

However, given the valuation of the S&P 500 (P/E TTM = 23.02), the low growth environment of S&P 500 earnings (3.5% annually over the past 10 years) and the increased risks it is likely that the next few years may be bumpy with below average gains. As such, a 2.5% yield from an ETF such as the Vanguard Total Bond Market ETF (NYSEARCA:BND) may provide welcome diversification.

Personally, I have allocated over 90% to stocks over the past years, but I am now more comfortable holding 50-60% stocks with the remainder in bonds and cash. Positioned this way one will be well equipped to take advantage of a market swoon, but still invested if the market continues to rise.

Individual stocks with strong technicals and valuations that are less economically sensitive include: AT&T (NYSE:T), Dollar General (NYSE:DG), Icon Plc (NASDAQ:ICLR), Google (NASDAQ:GOOGL), Priceline (NASDAQ:PCLN), Travelers (NYSE:TRV) and Visa (NYSE:V).

The problem with Friday's market rally is that yesterday the market was happy with an interest rate cut, but tomorrow the market will have to come to terms with why interest rates were cut. Unlike quantitative easing, interest rate cuts do not usually precede strong stock market performance. Investors should view the current rally with suspicion; it may not be all that it seems.

0 comments:

Publicar un comentario