Inflation Is Coming, Are You Prepared?

by: William Koldus, CFA, CAIA

- For a majority of the last five years, global financial markets have been stuck in a disinflationary spiral.

- Investors responded by going long the U.S. Dollar, long U.S. Treasury’s, long U.S. stocks, short emerging market stocks, and short commodity stocks.

- A historic reversal of the prevailing trades and sentiment is occurring, with inflationary pressures emerging.

- Investors responded by going long the U.S. Dollar, long U.S. Treasury’s, long U.S. stocks, short emerging market stocks, and short commodity stocks.

- A historic reversal of the prevailing trades and sentiment is occurring, with inflationary pressures emerging.

"Development is of primary importance to China and is the key to solving every problem we face."

"Pursuing development is like sailing against the current: you either forge ahead or you drift downstream."

- Chinese Premier Li Keqiang

"No-one has ever made real money following the crowd."

- Bill Bonner

"There's a trick to the 'graceful exit.' It begins with the vision to recognize when a job, a life stage, (an investment cycle) or a relationship is over - and let it go. It means leaving what's over without denying its validity or its past importance to our lives. It involves a sense of future, a belief that every exit line is an entry, that we are moving up, rather than out."

- Ellen Goodman

Source: HBO.

Introduction

For the past five years, financial markets have been "stuck" in a self-repeating cycle, where economic growth disappointed, central banks came to the rescue, and global capital flows were recycled into the perceived safety of U.S. stocks and bonds.

This resulted in unusual price action, with leading U.S. large-capitalization stocks, particularly large-cap growth stocks, becoming a safe-haven destination from 2011 through 2015. The outperformance of U.S. stocks, and bonds, over this time frame produced a virtuous cycle that culminated when seven large-cap growth stocks, including Alphabet (NASDAQ:GOOGL), (NASDAQ:GOOG), Amazon (NASDAQ:AMZN), Apple (NASDAQ:AAPL), Facebook (NASDAQ:FB), Microsoft (NASDAQ:MSFT), Gilead Sciences (NASDAQ:GILD), and Walt Disney (NYSE:DIS), dominated the S&P 500 Index's price action for a majority of calendar year 2015.

The rolling, stealth bear market, that had felled emerging markets, international stocks, and a majority of U.S. stocks over the past year, with the average U.S. stock falling over 25% from its highs, transformed from a quiet tropical storm into a full-fledged hurricane in January and February of 2016.

Much like hurricanes can reshape entire islands in the Caribbean, transferring one island's precious sand to another beach across the ocean, the investment landscape has taken a decided change after the latest storm has come and gone.

Notably, for the first time in five years, inflationary assets are outperforming and inflationary pressures are rising. Additionally, crowded trades are unwinding, as institutional and retail investors reassess their positions. In the aftermath of the storm, it is clear that the playbook that worked over the past five years for investors is going to have to be changed going forward.

Thesis

The investment landscape is transitioning from a deflationary environment to an inflationary environment.

Not A Typical Bull Market Thus Far

Normally in a bull market, the last phase of the bull market is dominated by economic sensitive stocks, including industrial and material companies. This phase is characterized by rising inflation, as a growing economy, for a prolonged period, of time stimulates pricing pressures.

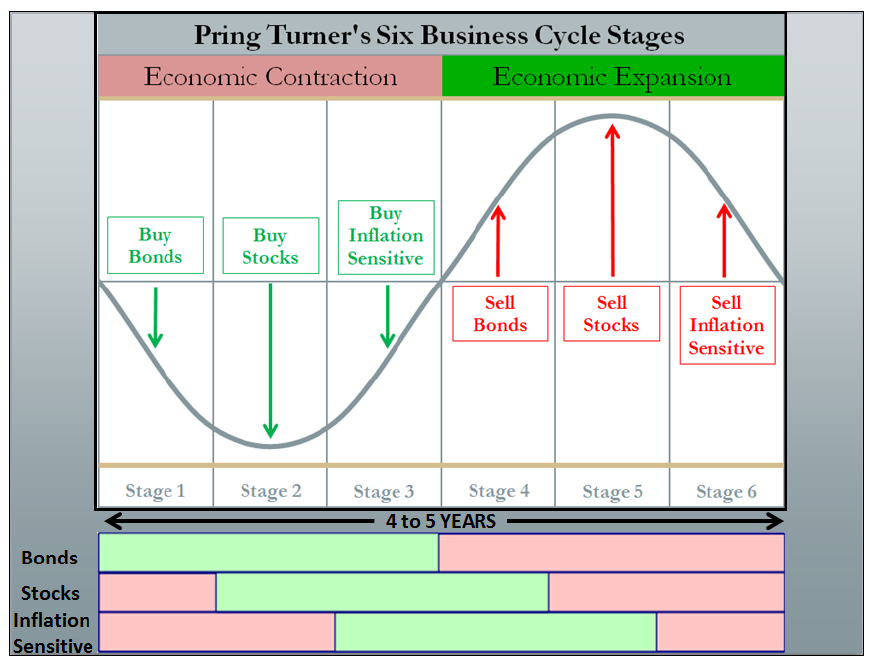

This is best illustrated by the following graphic from the website of one of my favorite analysts, Martin Pring.

Pring popularized the concept of investing according to the business cycle. In theory, this works wonderfully, but in practice, it has proved less than adept, as the current, extended seven-year bull market, has largely left behind these inflationary investments, as there simply has been no inflation, despite the proliferation of central bank "extraordinary measures", including repeated, and ever increasing "doses" of quantitative easing.

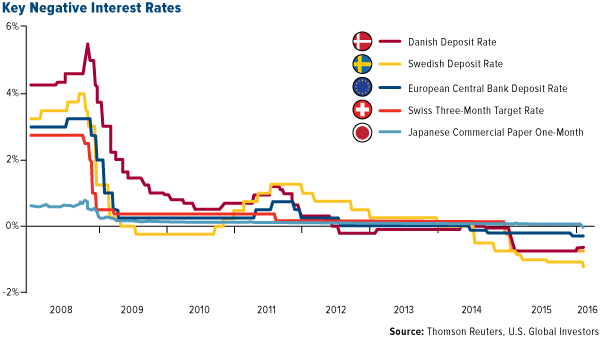

Investors Feared Deflation In 2015

Denmark, Europe, Japan, Sweden, and Switzerland have all embraced negative interest rates, and sovereign bond yields around the world plunged to record lows during 2015, and they generally remained anchored near these lows in 2016.

Low government bond yields across the globe were indicative of the prevalent deflationary pressures.

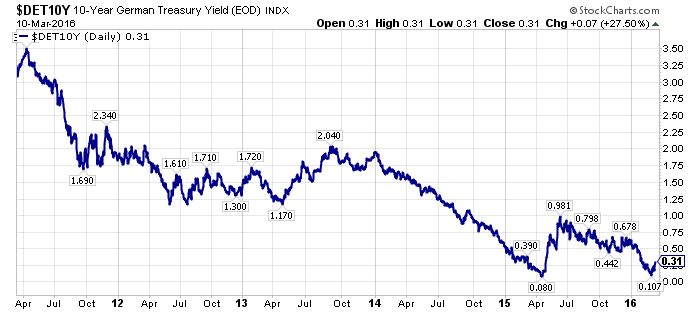

The sheer depth that higher quality sovereign bond yields plummeted to, which is shown by the chart of the 10-Year Germany Treasury Bond, provided a window into the panic and capitulation that was taking place in the global bond markets.

Worries About Deflation Have Overlooked Inflationary Pressures

As financial market participants struggled to cope with historically low yields, and embraced the inevitability of deflation, a funny thing happened - inflationary pressures began to build.

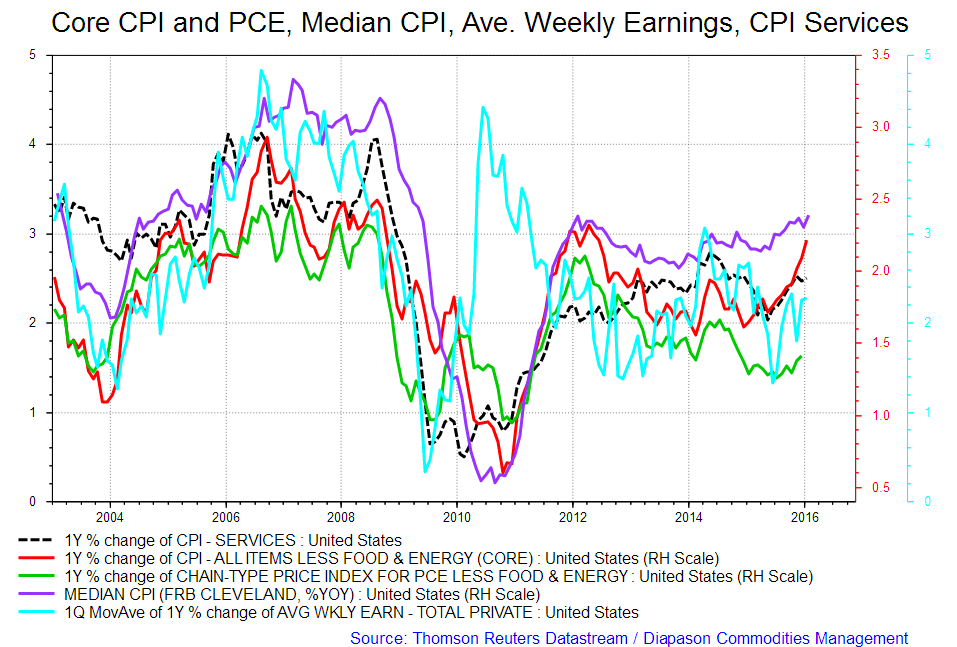

Fellow Seeking Alpha author Robert P. Balan, has published a terrific series of articles that have overviewed this changing investment landscape. His latest research piece, published on February 25th, 2016, and titled, "Inflation And GDP Growth Rise; Bond Yields Must Follow," was one of the best articles on Seeking Alpha in February, in my opinion. Please click on the link above to read it, if you have not already.

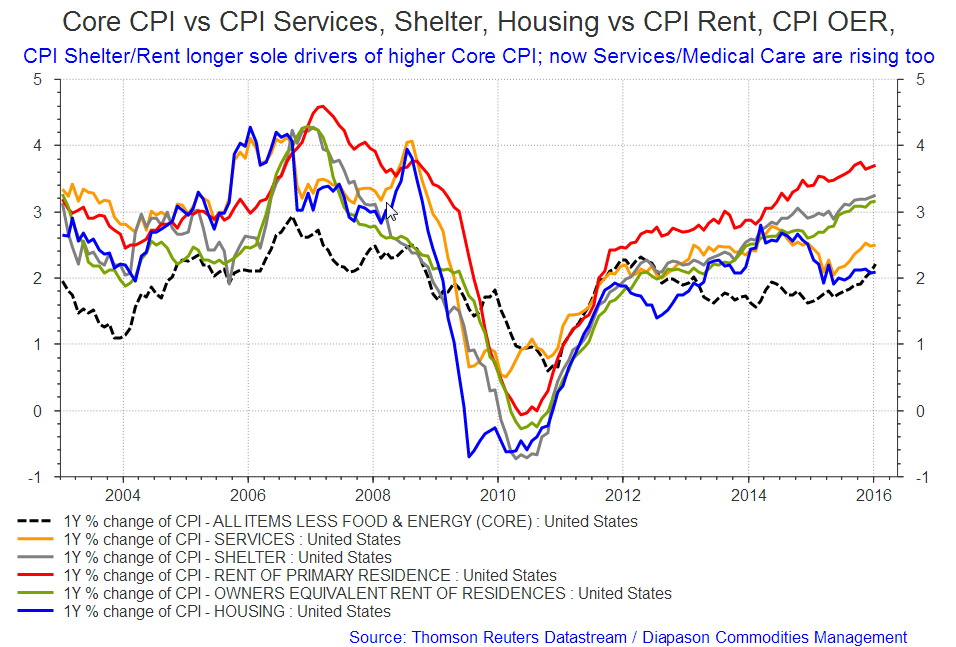

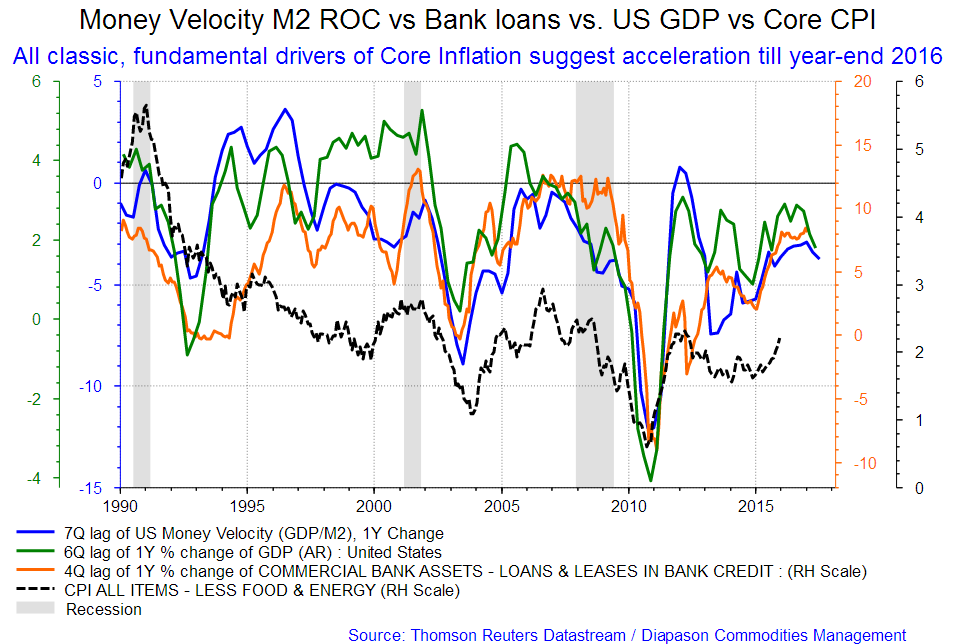

In the article, Mr. Balan included a number of charts and graphs that explained why investors should think about inflation, not deflation going forward. I have included three of these charts as follows:

The headline of Robert's last chart captures the mood perfectly, saying that, "All classic, fundamental drivers of Core Inflation suggest acceleration to year-end 2016." Within his article, Robert wrote that, "That may set up for the Core CPI a 'perfect storm' of several combined factors which will make it soar in a degree that nobody has expected."

To summarize, perhaps the Fed will be forced to raise short-term interest rates more than the market anticipates right now in 2016, and perhaps the era of deflationary concerns is giving way to inflationary concerns.

Winners & Losers

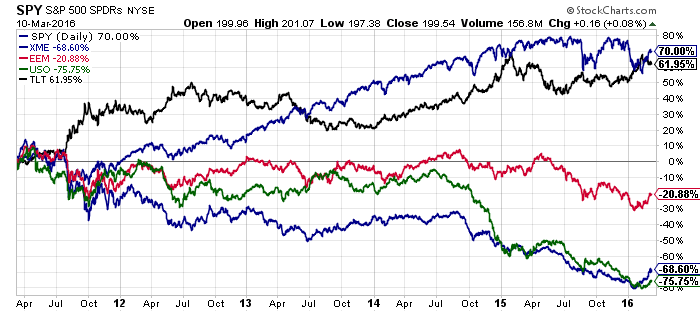

U.S. stocks and bonds were clear winners over the past five years, where disinflationary and deflationary pressures reigned, while emerging market equities, commodities, and commodity stocks were distinct losers.

This is clearly illustrated in the chart below, that depicts the respective performances of the S&P 500 Index, as measured by the SPDR S&P 500 ETF (NYSEARCA:SPY), which increased 70%, the iShares 20+ Year Treasury Bond Fund ETF (NYSEARCA:TLT), which advanced 62%, the iShares MSCI Emerging Markets ETF (NYSEARCA:EEM), which declined 21%, the SPDR S&P Metals & Mining Index ETF (NYSEARCA:XME), which declined 69%, and the United States Oil Fund (NYSEARCA:USO), which lost 76% of its value.

From the chart above, "winning" and "losing" trends have been unambiguously defined, and investors and speculators from sophisticated hedge funds to plain vanilla retail day traders, have all been participating in these one-way trades.

A Turning Point - Stocks Suggest Inflation

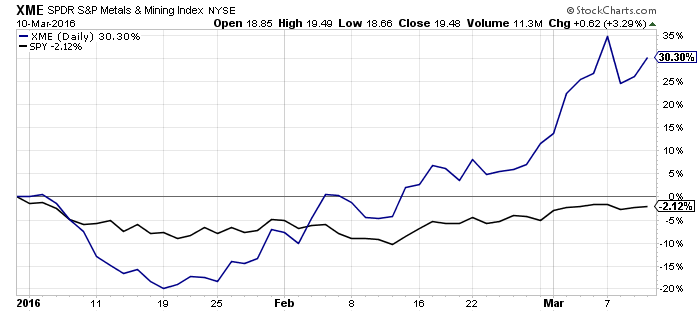

As 2016 has unfolded, a startling reversal of fortune has taken place in out-of-favor stocks and industries. This is best exemplified by the downtrodden XME, which had declined 69% over the past five years, but has now risen 30% year to date (YTD), while the SPY has declined 2% in 2016.

The top ten holdings of the XME have risen dramatically this year. AK Steel (NYSE:AKS), the largest holding, has risen 85% YTD. U.S. Steel (NYSE:X), the second largest holding has risen 81%. Newmont Mining (NYSE:NEM) is up 52%, CONSOL Energy (NYSE:CNX) is up 41%, and Cliffs Natural Resources (NYSE:CLF) is up 57% in 2016, thus far. The sixth largest holding, Hecla Mining (NYSE:HL) is up 42%, the same as Freeport-McMoRan (NYSE:FCX), while Coeur Mining (NYSE:CDE) has returned an eye popping 97% YTD. Closing out the top ten holdings, Royal Gold (NASDAQ:RGLD) has risen 38%, and Steel Dynamics (NASDAQ:STLD), one of the best performing material stocks the last several years, has appreciated a relatively pedestrian 18% in 2016.

A Front Row Seat With "The Contrarian."

Through a premium research service on Seeking Alpha, "The Contrarian," that I launched in December of 2015, I have been chronicling the changing investment landscape, pontificating about portfolio strategy, and generally trying to take advantage of what I feel is another once in a generation inflection point in the capital markets.

There are a series of portfolios within "The Contrarian" that have been designed to benefit from a reversal of the investment trends that have prevailed over the past five years. Recently, I profiled the "Bet The Farm" Portfolio, the most aggressive of the portfolios, and the thought process behind its strategy. The "Bet The Farm" Portfolio is an options based portfolio, and some investors may be uncomfortable dealing with the unique risks and rewards that participating in an options portfolio entails.

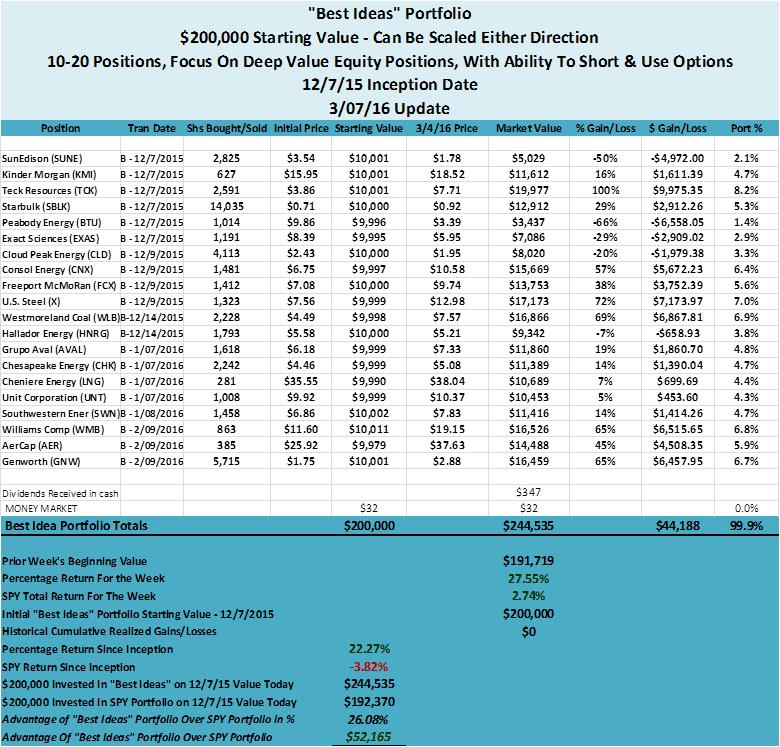

There is another, primarily stock based portfolio in "The Contrarian," with the moniker of "Best Ideas" Portfolio. I have copied and pasted the 3/7/2016 update below to document the reversal we have seen in out-of-favor stocks.

Last week, the "Best Ideas" Portfolio surged higher, advancing 28%, as the three intertwined, crowded trades, including long the U.S. Dollar, short emerging markets, and short commodity stocks, began to unwind.

Conclusion - Prepare For Inflation

After a historic bull market over the past seven years, where both stock and bond prices rose unremittingly in a disinflationary environment, the stage has been reset without most investors noticing. Inflation, not deflation, is the primary risk to investors, at this juncture. Meanwhile, most market participants are still looking in their rear view mirrors at the risks behind them (deflation), instead of looking forward at the challenges staring them in the face (inflation).

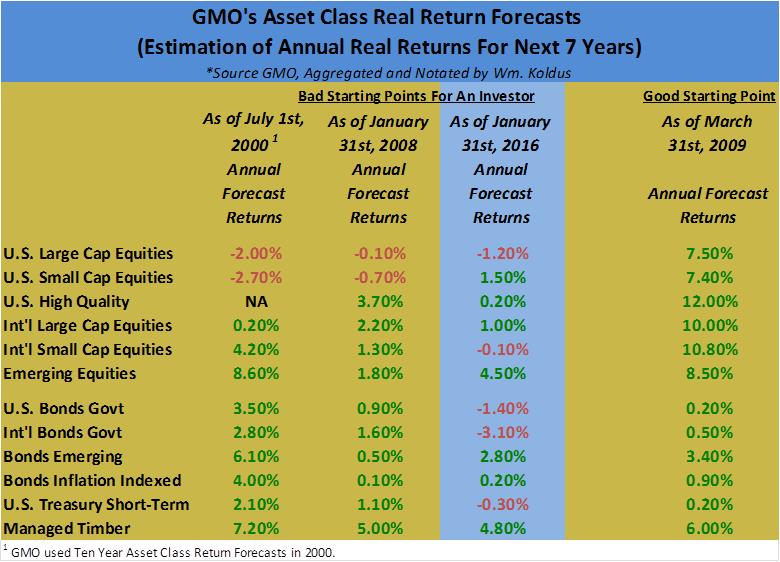

With stock and bond prices at record highs, and their corresponding valuations in nosebleed territory, especially if interest rates would rise, negative "real" returns, or flat returns at best, are now anticipated for the next seven years. This is illustrated with the table I have put together using data from GMO.

As Jon Snow famously opines in HBO's hit show, Game Of Thrones, "Winter Is Coming," and no one seems to care because they are busy fighting their own battles. In the investment markets, "Inflation Is Coming," so focus on how rising inflation could impact your portfolios.

The change in trend has just started, so it is not too late to reconsider some out-of-favor assets, and asset clases.

0 comments:

Publicar un comentario