If Only We Could Blame China

John Mauldin

I regularly read Niels Jensen’s monthly letter, and this month’s edition is exceptional. Longtime readers will know that he has been featured in Outside the Box several times over the years. Today, Niels challenges the widespread belief that the steep drop in commodity prices is all about the economic slowdown in China. He also questions whether China is in fact more a victim than a villain of the recent plunge in global equity markets. He arrives at the conclusion that high and rising debt levels amongst corporates in emerging markets, in combination with a strong US dollar – particularly when measured on a trade-weighted basis – is a more likely cause of the fall-off. This is a very nonconsensus view, but it’s one that I found fascinating to seriously think about. And you probably should, too.

Will the current turbulence in global markets lead to a repeat of 2008, as many have suggested? Niels’ take on that question is interesting and convincing; but rather than spill his beans, I’ll turn you over to him.

I finish this quick introduction in a very cold and snowy Chicago – quite the contrast from the weather we’ve been enjoying in Texas. For the past two days I have been speaking about and in meetings discussing portfolio design, which is a topic I don’t often write about but do get a lot of questions about.

I’ve thought hard the last few years about how we should structure portfolios, especially our core positions, given my view of how the world is going to transform over the next 10 years. How can we make certain we’re in the markets at the right times and not in there when we don’t want to be? Or at least be reasonably sure? I’ve begun sharing my ideas with senior investment professionals around the country, and they and I think I may really be on to something special. I will be sharing these ideas in private and then making them publicly available within the next few months.

Working on the new book, it’s a challenge to try to describe not only how the world will change in 20 to 25 different areas but also how we should invest in the meantime. This process of thinking more long-term but accepting that we live and invest in a short-term world has gotten me to reconsider what to many of us has been a basic assumption. Is it possible that we are diversifying the wrong parts of our portfolios? Maybe… Coming soon.

It’s time to put on the jackets and scarves and gloves and brave the rush-hour traffic from Wheaton into downtown. In snow and ice. I can’t tell you how much I’m looking forward to it. At least I’m not the one driving. And yes, I will be very buckled up and padded…

Your getting more excited about the future analyst,

John Mauldin, Editor

Outside the Box

JohnMauldin@2000wave.com

If Only We Could Blame China

Niels C. Jensen, Absolute Return Partners

“When you combine ignorance and leverage, you get some pretty interesting results.”

– Warren Buffett

One thing we are exceptionally good at in the West is to blame China for pretty much anything that goes haywire. If you believe various commentators, it is all China’s fault that global equity markets have caught a serious cold more recently and, before that, China was blamed for the extraordinary weakness in industrial commodity prices. They have weakened – or so the argument goes – because China’s growth is not quite what it used to be, and commodity producing countries are over-producing as a result.

Whilst entirely correct that China’s GDP growth rate has indeed slowed substantially, perhaps someone should consider whether China is as much the consequence as the cause; whether China is in fact a victim rather than a villain? Let me explain.

The recent history of commodity prices

Commodity prices peaked in early 2008 (per the Bloomberg Commodity Index), only to fall dramatically as the Global Financial Crisis (‘GFC’) took its toll. Between 2009 and 2011, a substantial part (but not all) of those losses were recovered again, but since early 2011 it has been pretty much one way traffic. I do note, though, that in the early stages of the post-2011 fall in commodity prices, oil did not participate at all, as oil prices were pretty much flat between April 2011 and June 2014.

Phrased slightly differently, commodity prices have fallen well over 50% since April 2011, but oil prices have only participated in that rout since June 2014.

Energy (broadly defined) accounts for only about 31% of the Bloomberg Commodity Index, so there is definitely a bigger story unfolding here.

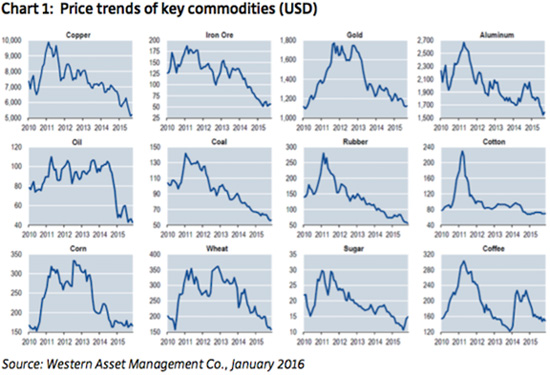

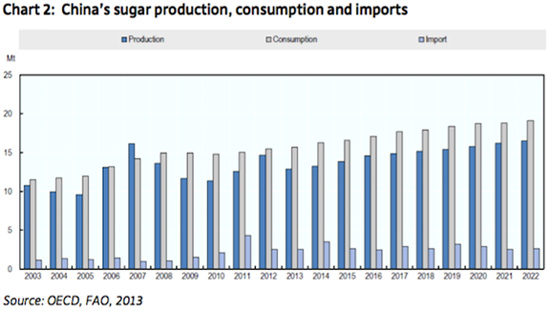

I suggest you take a quick look at chart 1. As you can see, commodity prices have fallen out of bed pretty much across the board. Anything from sugar to iron ore is down significantly, and it is really hard to blame the fall in sugar prices on China, even if I try my best. China is largely self-sufficient on sugar and is not a major player in international sugar markets (chart 2), so what is going on?

Rising corporate leverage in emerging markets

One theory – and the one I subscribe to – is that many commodity producing countries have chosen to ignore the fact that, not that long ago, virtually the entire world suffered from the GFC and have continued to pile on debt, as if there is no tomorrow. You may wonder why that is. I am sure there is more than one reason, but attractive borrowing conditions (low interest rates) have to be one of them.

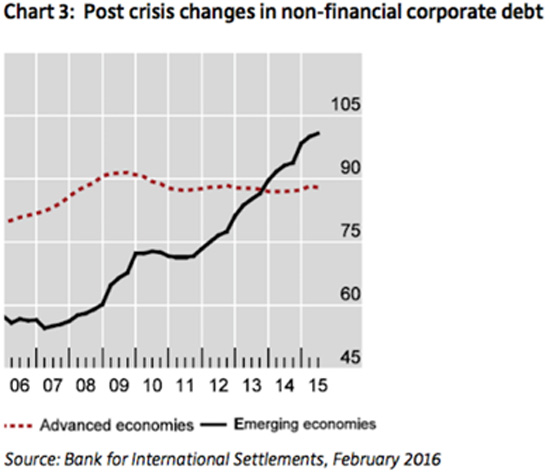

The net result today is that whilst corporates in developed markets have not added to pre-crisis debt levels, and in many cases actually reduced overall debt, corporate debt levels in EM countries are at an all-time high (chart 3).

Interest rates are currently low on either side of the Atlantic, but U.S. bank regulators are not coming down as hard on U.S. banks, as regulators over here are on European banks. Adding to that, the fact that many commodities are priced in U.S. dollars has made the USD an obvious choice of currency for borrowers in emerging markets, many of whom are commodity producers.

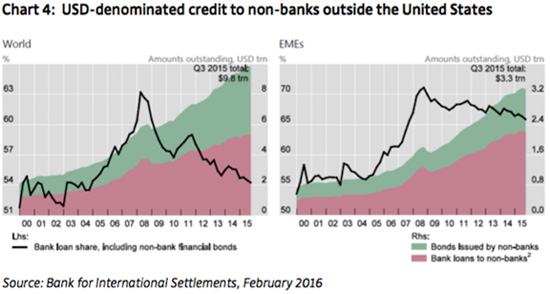

By drilling one level further down, it becomes apparent precisely how much total USD lending to corporates in emerging markets has actually grown.

Before the GFC, USD lending to non-bank corporates in emerging markets totalled about $1.5 trillion. As of the latest count, it now stands at $3.3 trillion (chart 4).

Before the GFC, USD lending to non-bank corporates in emerging markets totalled about $1.5 trillion. As of the latest count, it now stands at $3.3 trillion (chart 4).

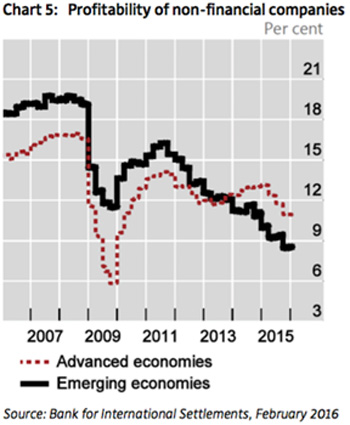

The rising leverage across emerging markets has begun to worry the central bankers at Bank for International Settlements (‘BIS’). As Jaime Caruana said, when he gave a speech on the topic at the London School of Economics in early February:

“Increased leverage would be less of a concern, if debt was used to finance productive and profitable investments.”

However, as he also pointed out, profitability of EM corporates has been declining in recent years and is now below that of DM corporates (chart 5).

And it doesn’t stop there. The combination of falling oil prices and a steep fall in the value of most EM currencies v. USD will have a knock-on effect on sovereign creditworthiness too. As many oil companies are state owned, and as most countries with large state owned oil companies depend on oil revenues to finance the government budget, low oil prices translate directly into large public deficits and hence falling sovereign credit ratings.

The sinners

So here is what I think is actually happening. Because:

• commodities are the single biggest export article of most EM countries;

• many corporates have borrowed a lot in U.S. dollars in recent years; and

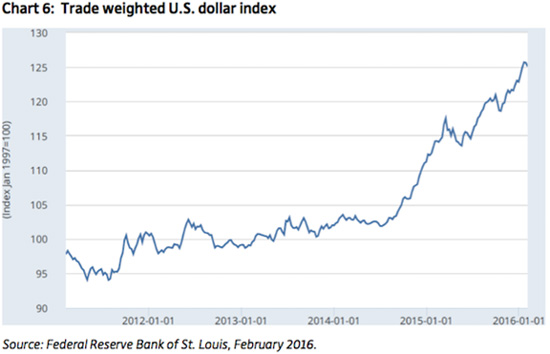

• the U.S. dollar on a trade-weighted basis has been very strong more recently (chart 6);

servicing the rapidly growing mountain of debt has proven a great deal more expensive than expected. Corporates have simply been forced to sell their commodities at increasingly deflated prices to service their rising debt. What many thought were exceedingly good borrowing terms now prove to be anything but, once currencies are taken into account.

Obviously, if the commodity in question is priced in U.S. dollars, the corporate involved will also generate income in USD, but that income has fallen steadily as prices have declined, so it is only a partial hedge.

I alluded to the link between rising leverage and falling commodity prices in the January Absolute Return Letter (which you can find here), where I wrote the following:

Almost all of the increase is due to a rise in corporate debt, and much of it has been borrowed in U.S. dollars as a result of the extraordinarily benign borrowing conditions in the United States since the outbreak of the GFC. As the Fed has now embarked on a cycle of rate hikes, which is likely to drive the dollar to new heights, and because commodity prices tend to be very negatively correlated with the dollar, I would expect the fall in commodity prices to continue well into 2016.

[...]

The combination of rising debt servicing costs and falling commodity prices is outright poisonous for the many EM companies that make a living out of exporting commodities to the rest of the world. If the U.S. dollar continues to appreciate (as we expect it to do) and commodity prices sink to new depths, the overall conditions for EM exporters can only deteriorate further.

Let’s just leave it at that. No need to elaborate any further.

A word on the link between China and oil

Up to this point, readers would be forgiven for thinking that I hold China free of any responsibility regarding the current slowdown in global economic activity, but that is not correct. China’s problems are just very different and have little to do with falling commodity prices. It is faced with a decapitated banking industry, which has been far too willing to lend to all kinds of investment projects – good and bad. At the same time, the Chinese growth model has been driven by investments and exports, whereas the growth in consumer spending has been relatively modest.

A few numbers to support that statement: As recently as 10 years ago, exports and investments constituted 34% and 42% respectively of Chinese GDP, i.e. less than a 1⁄4 of Chinese GDP came from the combination of consumer spending and government spending. By comparison, consumer spending accounts for over 70% of U.S. GDP.

By 2014, investments had grown to 46% of GDP, whilst exports had fallen to 23%. The further growth in investments has been funded by rapid credit expansion in China’s banking industry, which has grown from $3 trillion in 2006 to $34 trillion in 2015 (source: Hayman Capital Management, February 2016). That is a shocking amount of credit in a $10 trillion economy.

Now, the Chinese leadership face a big challenge. They must restructure the banking industry whilst at the same time seek to change the growth model. I can think of quite a few things that can go wrong in that process. Having said that, China is a user of commodities, not a producer and stand to benefit from lower commodity prices.

Informed sources tell me that Chinese GDP is growing at 3-4% per annum at present – not at 6-7% as claimed by official sources, but neither at 1-2%, as some pessimists have suggested more recently. The slowdown in Chinese economic growth is to a large degree down to the problems in the banking industry that I alluded to above. Non-performing loans are rising at no more than 1-2% if you believe official numbers, but the true growth rate in non-performing loans is more like 5-10%, or so I have been told.

The economic slowdown in China has certainly had some impact on oil prices, but one shouldn’t overstate China’s role in setting the price of oil. After all, China ‘only’ accounts for 16% of global GDP, and we have been through economic slowdowns of a magnitude similar to that of China before, without it having had the same dramatic impact on oil prices. I can only conclude that the steep fall in oil prices appear to be a supply problem, and have little to do with economic problems in China.

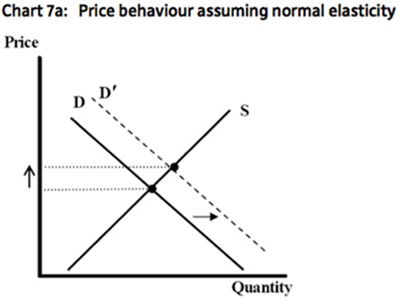

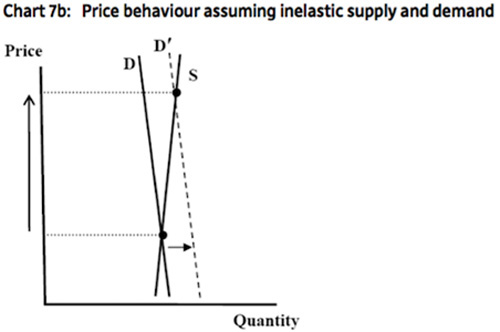

One additional point. Oil is widely known to be a very inelastic commodity, which explains precisely why oil prices have fallen as much as they have. A relatively modest slowdown in economic activity – not only in China but across the world – combined with higher than expected supplies, has created an imbalance between supply and demand, and the price has behaved exactly like the textbook prescribes.

So what precisely does the textbook say? Chart 7a provides a graphical illustration of the effect on price, should demand for a ‘normal’ commodity change modestly. In chart 7b you can see the effect the same level of demand change has on price, assuming that both supply and demand are inelastic. Not surprisingly, the price move is much more dramatic.

Source: www.SEDinc.com

However, before you conclude that, in the current environment, oil prices can only go one way, and that is further down, let me share with you an observation that was pointed out to me recently (source: Frank Veneroso, January 2016). Monthly crude oil production numbers suggest that U.S. oil production has fallen nearly 400,000 barrels per day more than what the weekly numbers have suggested – and which nearly everyone follows – implying that the global oil market surplus is less than most estimates, and is likely to fall fast as the year progresses.

I therefore maintain my long-term bullish view on oil prices. Most of the weakness is now behind us, but I will admit that prices can go anywhere in the short term.

However, when we enter 2017 (and perhaps even earlier), inventory levels will at least have stabilised, and oil prices will begin to creep upwards again. Shale will prevent us from seeing oil prices at $100+ anytime soon, though.

What it all means

Regular readers of the Absolute Return Letter will know that, back in January, I listed the EM crisis as one of my leading candidates for ‘story of the year’ in 2016, and I pointed out how it could quite possibly negatively affect asset prices world-wide. That the story has unfolded this early in the year has admittedly taken me by surprise, but the fact that it has unfolded at all has certainly not.

After the significant damage that the GFC did to the financial system across DM countries, both banks and their regulators are constantly on their toes to avoid another calamity, and they are now tightening credit conditions in emerging markets. Total credit to EM corporates actually fell in the third quarter of last year – for the first time since 2009.

This has created a rather bizarre situation. Where common sense would suggest the supply side to cut back when prices fall and follow the logic in chart 7, the exact opposite has happened. Suppliers of various commodities (not only oil) have actually increased production as prices have fallen – presumably to service their rising debts. There is a first time for everything, I suppose.

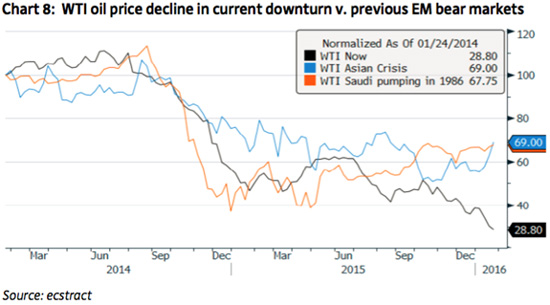

Having said all of that, this is not the first time that a crisis has hit the emerging markets. In 1997-98 the so-called Asian crisis did substantial damage to equity prices as well as commodity prices, and the ultimate saviour back then turned out to be the combination of low commodity prices – in particular low oil prices – and very competitive foreign exchange rates.

I see no reason why the present combination of low oil prices and attractive foreign exchange rates shouldn’t invigorate economic growth across emerging markets, just as it did it back then. After all, the fall in oil prices this time has been even bigger than it was in 1997-98 (chart 8).

EM equities could quite plausibly end up being the bargain of the year, although I am concerned about corporate leverage in many EM countries. One would therefore have to step carefully.

Finally a general observation: This is not a repeat of 2008, as many have suggested. An EM crisis is not likely to do nearly as much damage to the financial system in our part of the world, as the GFC did. Why? Because the banking system in DM countries have only limited exposure to corporates in EM countries. Recession? Possibly. 2008 all over again? No.

0 comments:

Publicar un comentario