Growth Is the Answer to Everything

By John Mauldin

“Growth is never by mere chance. It is the result of forces working together.”

– James Cash Penney

In this business we spend a lot of time thinking about problems. What if we could wave a magic wand and make them all go away? Maybe we can.

The wand isn’t made from wood. You don’t need Latin phrases or a special incantation learned at Hogwarts to make it work, either. It’s a simple six-letter word: growth. Get the economy growing at a decent pace again, and most of our problems will get better.

Conversely, they’ll only get worse if we stay in slow-growth mode. And don’t even think about what a recession will do to the markets in this environment.

Fortunately, there are things we can do to bring growth back. We just have to decide to do them.

A new reader browsing through my archives might get the impression I am a worrywart. In fact, I’m quite optimistic about our future – but I don’t deny we face serious challenges. My weekly letters are a peek into my ongoing thought process as I wonder how we will tackle those challenges.

Just in the past few months we’ve looked at problems like retirement, energy prices, political chaos, zero interest rates, negative interest rates, China’s economy, terrorism, unemployment, inflation, pensions, healthcare, refugees, and the Federal Reserve. And an overarching theme of many letters has been the very big problem of growing debt. Whew – so many problems.

We can look at each of these challenges individually and come up with possible solutions. Would our solutions work? I don’t know, but I’m confident we would see improvement on all fronts if we got GDP growth back up to 4% for a few years.

In the summer of 2012, a few weeks after House Speaker Newt Gingrich had withdrawn from the presidential race, he and his wife Callista came to visit me at the villa we were renting in a tiny town on a mountain in Tuscany, Italy. In addition to doing the usual tourist stuff, Newt and I spent more than a few evenings talking late into the night about an extraordinarily wide variety of topics and discovering that we had many interests in common.

I remember one late night in particular, when I challenged him a bit on the tax and budget plans he had outlined in his campaign. While I agreed with their general direction (and still do), I was concerned about the growing US debt and wanted to see a return to paying the debt down. His plan simply balanced the budget and held government budget growth below economic growth. “How do we deal with the debt?” was my question. His answer was simple: “With the budget and regulatory changes I outlined, we simply grow our way out of it.”

That had been his experience when he and Rep. John Kasich (to whom he still gives a great deal of credit) worked with then-President Bill Clinton to balance the budget – and the country actually began to run surpluses. We grew our way out of the problem. If the Republicans under President Bush had not squandered the opportunity Clinton, Gingrich, and Kasich left them with, we would have come to the 2008 recession with very little if any debt and a healthy ability to run deficits without damaging the long-term prospects for growth in this country. And if we had actually used those deficits to build the infrastructure that was talked about but never undertaken? We would have something to show for the massive government debt we’re saddled with now.

So, is growing our way out of debt a pipe dream? It shouldn’t be. The US economy grew about 3.5% a year from 1950 through the year 2000. During that period there were many expansions in which the economy grew even faster than that average, and there were recession years when growth was much lower.

This alternation is exactly what economic theory says we should expect – every economy goes through boom-bust cycles. Since the end of World War II, we have had a recession every 5–10 years or so. Our experience was that they always gave way to an expansion that made up the lost ground and then some.

It hasn’t worked that way this time. We entered a recession in late 2007 that officially ended in September 2009. Now it’s 2016. This month will mark 8½ years of economic expansion. So why is no one cheering?

Because the less than 2% average growth we have seen since the end of the recession (and actually, since the year 2000) has added very little real income to most American households. Many of us have seen our job situations end up dramatically changed, with our new positions offering significantly less income. In addition, instead of the reduced healthcare costs we were promised under Obamacare, most of us have seen our costs go up dramatically.

So the great majority of us aren’t feeling like we have recovered. While some are better off now, the growing divide between those who are flush and those who are scraping by has resulted in a groundswell of voters from both parties demanding change.

There is a fascinating quote attributed to Lord Salisbury, who was the Tory prime minister of England during Queen Victoria’s reign. Supposedly, when she said things must change, he said, “Change? Change? Aren’t things bad enough already?” Sometimes, when you wish for change, you’d better be prepared to get what you ask for. Sometimes you get it good and hard. And speaking of change…

Last month I ran across a fascinating study by economist John Cochrane. He is a senior fellow at the Hoover Institution, former University of Chicago professor, and adjunct scholar with the Cato Institute. He blogs as The Grumpy Economist but doesn’t seem all that grumpy, as economists go.

Cochrane wrote a paper on economic growth last year as part of a project to design presidential debate questions. Sadly, the candidates chose to talk about other issues such as finger length and personal energy levels, but Cochrane’s paper is still useful. I’ll discuss it briefly, but everyone should read the full version. It is not at all technical, and you will learn much.

He begins by showing how small changes matter a great deal in the long run. The economy grew by over 3½% from 1950 to 2000. From 2000 the economy has grown at about half that rate, or 1.7%. And therein lies the reason that incomes have been so punk for much of America:

Small percentages hide a large reality. The average American is more than three times better off than his or her counterpart in 1950. Real GDP per person has risen from $16,000 in 1952 to over $50,000 today, both measured in 2009 dollars. Many pundits seem to remember the 1950s fondly, but $16,000 per person is a lot less than $50,000!

If the US economy had grown at 2% rather than 3.5% since 1950, income per person by 2000 would have been $23,000 not $50,000! [emphasis mine] That’s a huge difference. Nowhere in economic policy are we even talking about events that will double, or halve, the average American’s living standards in the next generation.

I don’t know about you, but to me those are stunning numbers, for several different reasons. I was born in 1949, so GDP per person has more than tripled in my lifetime. That’s in constant dollars, so it isn’t just “growth” by inflation.

Yet this tripling would not have occurred if the economy had grown at 2% a year instead of 3.5% during my lifetime. That extra 1.5% made an enormous difference. In fact, the difference is even greater.

GDP per capita does not capture the increase in lifespan – nearly 10 years – in health, in environmental quality, security and quality of life that we have experienced. The average American today lives far better than a 1950s American would if he or she had three rather than one 1950s cars, TVs, telephones, encyclopedias (in place of internet), or three annual visits to a 1950s doctor…”

Those 1950s doctor’s visits now seem like Stone Age medicine. And that doesn’t take into account mobile phones, Google maps, and a plethora of other things that make our life better because the growth of the economy made us better able to afford them.

But even these less quantified benefits flow from economic growth. Only wealthy countries can afford environmental protection and advanced health care. We can afford to worry about global warming. India worries about 600 people per toilet, emphysema from burning cow patties, and easily treatable parasitic infections. Our ability to defend freedom around the world – even if we are wise enough to do it sensibly – depends on robust economic growth. If GDP had grown at 2%, not 3.5%, we would only be able to afford half the military we have today. The immense improvements in the quality of goods and many services we have today are part of the engine of economic growth.

This is why the recent years of subpar growth are a big problem. It isn’t just the current feeble recovery: we are now almost a full generation into a low-growth era that marks a departure from most people’s prior experience. It’s no wonder so many folks are discouraged and angry. (And by the way, we’re growing faster in the US than they are in Europe and Japan.)

Some economists will argue that the last century was an aberration. Robert Gordon is a good example. Watch his TED Talk if you’ve never seen it. He believes a handful of one-time breakthroughs (electricity, automobiles) accounted for most of the economic growth we now think should be normal. I disagree with Gordon – and will attempt to rebut him in my upcoming book – but I have to admit he makes some very good, valid points.

(The short version of my view is that I think we’re on the cusp of changes that will be just as revolutionary as electricity and that will boost our growth considerably – even by the standard measure of GDP, which we know misses so much. This is why I am optimistic about our future.)

Cochrane points to the official Congressional Budget Office long-range outlook, which assumes 2.2% growth from now through 2040. That would be an improvement over the recent past, but it’s still historically low.

If you change that assumption from 2.2% to 3.5%, total GDP in 2040 will be 38% higher. That GDP boost means tax revenues will be 38% higher, and much of our debt problem will disappear. Shades of Newt Gingrich! Conversely, Cochrane notes that 1% GDP growth over that period would yield a 26% drop in GDP and tax revenue, leaving us in a deep hole.

On the other hand, there is no reason to think 3.5% growth is the ceiling. With a few changes we might be able to boost it even higher. Cochrane says what I have long believed: Rising productivity is the key to economic growth. The more each human can produce, on average, the higher everyone’s standard of living can rise.

Cochrane takes a matter-of-fact approach to the growth problem. What are the barriers to productivity growth, and what can we do to remove them? Not surprisingly, most barriers are the result of counterproductive government policies.

He breaks them down into categories. I’ll highlight a few.

Regulation: The government interferes in just about every segment of the economy. Sometimes it brings benefits like traffic safety and clean air. More often, regulation simply slows growth in order to transfer wealth from one group to another. It interferes with growth by impeding competition and distorting economic incentives. It distorts the signal that individuals send markets about their preferences and adds a great deal of noise and cost, which distorts economic activity from being its most efficient.

Finance: The Dodd-Frank financial regulations had the laudable goal of preventing future bank crises, but in reality they simply work against other government policies. Washington encourages and subsidizes debt and then tries to prevent the inevitable consequences. We wouldn’t need Dodd-Frank if the government were not rewarding excessive debt. As I’ve written about extensively in this letter (often citing Dr. Lacy Hunt and others), excessive, unproductive debt of the type we are generating in the US and Europe actually inhibits growth.

Healthcare: We’re all frustrated by Obamacare and health insurance generally. What we need is simple, portable, catastrophic health insurance. Instead of promoting it, the government makes it illegal.

Energy: Here again the government works at cross-purposes with itself. It subsidizes energy so that it costs less, then tries to prevent us from using too much of it. Cochrane says the ethanol mandate helps no one but the large corn-producing companies. Ditto for solar subsidies.

Taxes: Taxes should raise revenue, but instead we use them to redistribute income and encourage/discourage behavior. A simpler tax code would remove massive economic distortions, and it would be far better to tax consumption instead of income.

Social programs: Cochrane sees no need to be stingy with helping people in genuine need. Welfare programs are far less costly than the many subsidies we give the middle class and large corporations. The problem is that perverse incentives trap people and make them permanently dependent. He suggests consolidating all the aid programs and making them time-based, like unemployment benefits, rather than income-based.

Immigration: We can end illegal immigration overnight, says Cochrane, by making it legal. The question is the terms we apply to legal immigration. We should welcome skilled workers who want to stay in the US and contribute to our economy. He also points out, wisely, that whether someone should be here is a separate question from whether they should be allowed to work here.

Education: Public schools do not need more money; they need correct incentives. The way to deliver them and ensure better opportunities for all is to adopt vouchers and charter schools. The government doesn’t have to directly provide the service in order to help people afford it.

Implementing these reforms is a political challenge, not an economic one. One man’s waste is another man’s subsidy. People naturally resist when they perceive they are on the losing end of the bargain. Serious change is very hard if everyone insists on keeping whatever benefits they presently have.

Frankly, I realize that making these fundamental changes will be difficult, but we have to try. Cochrane stresses that even small changes make a big difference over time. In a few weeks, I will be sending you a very special Outside the Box, written by former Oklahoma Senator Tom Coburn, who has become my friend and who is one of the most focused and dedicated men I know when it comes to dealing with the deficit and debt. He is advocating a Convention of the States to propose constitutional amendments to force the government to effectively deal with the debt and regulation.

Numerous states (including Texas) have already adopted these proposals, and we anticipate as many as 15 more will adopt a resolution by the end of the year. Such a movement wouldn’t be necessary if we had a Congress and president that were capable of acting responsibly, but it appears the politicians of both parties are all too willing to make small changes around the edges without dealing with our central problems.

It is not just personal and government incomes that will continue to be affected if we don’t do something to boost growth; investors are going to suffer, too.

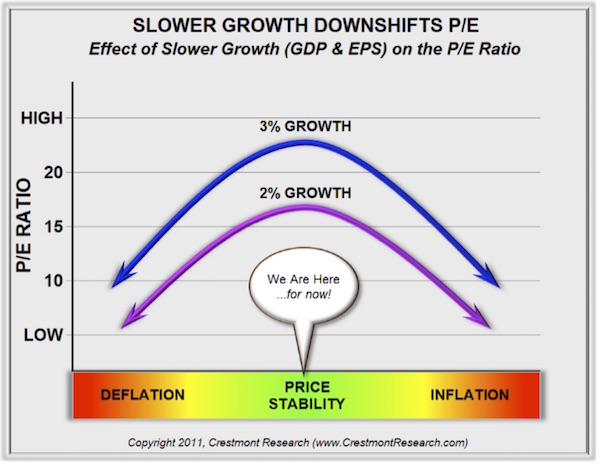

This week I received a very kind email from my friend Ed Easterling of Crestmont Research. Ed and I have collaborated many times over the past 15 years, most recently on “It’s Not Over Until the Fat Lady Goes on a P/E Diet.”

A big part of Ed’s research focuses on the relationships between price/earnings ratios and economic cycles. Bull markets end when company valuations grow excessively high. Then the ensuing bear market ends when valuations get unreasonably low. These secular bull or bear markets take many years (on average 17) to play out.

I noted at the end of last week’s letter that I would be writing about growth. Ed reminded me that economic growth is directly related to P/E growth and thus stock market returns. In the aggregate over a cycle, corporate profits can’t grow faster than the economy grows. Yes, you can always point to exceptions, but we’re looking at the aggregate here.

Here is one aspect of the problem: if people perceive that underlying economic growth has dropped to a permanently lower level, they will revise lower the amount they are willing to pay for a share of corporate profits, based on what they perceive as diminished future prospects.

Ed’s research shows that in a world in which 3% GDP growth is the long-term average, P/E ratios will average about 15.5. If expected GDP growth is only 2%, the historical average P/E drops to 11.5. That is a huge difference in long-term gains over a cycle.

Ed explained how he calculates the effect of slow growth on P/E in a 2013 article, “Game Changer: Market Beware Slower Economic Growth.” I suggest you read it. The implications are enormous. The difference between 3% and 2% long-run economic growth is a double whammy for stocks.

Companies will be less profitable if the economy grows more slowly, and P/E multiples will be lower because future profit expectations will not support the kind of valuations we used to think of as normal.

This is not a small problem. According to Ed’s research, if economic growth falls off just 1%, we should expect stock prices on large indexes to fall by 26%. That’s the difference between 15.5x and 11.5x P/E ratios. The reduction in stock prices will vary from cycle to cycle, but that is the average.

From there, the problems radiate outward. Anyone saving for retirement will have to reduce the amount they expect their stock portfolio to contribute. So will institutions and pension funds, which as we saw last week are already severely challenged. Lower profits mean less ability to invest in new capacity and more incentive to replace human workers with machines. Lower profits mean fewer new jobs and lower incomes. Less wealth flowing through the economy will reduce both tax revenue and contributions to charities.

I could go on, but I think you get the point. Economic growth really is the one-stop-shop answer to most of our economic problems. Income inequality? Low growth makes it worse, not better. Bernie Sanders’ many new taxes on top of the existing burden would make income inequality worse, not better. Middle America would soon be in a full-blown depression.

While most people agree the current recovery is too slow, I think many still believe we will eventually bounce back to the halcyon days of 3% and 4% GDP growth. I hope they are right, because we are all in deep trouble otherwise.

Many politicians would like to see the current growth malaise solved by monetary policy. Monetary policy can be useful, but it can’t overcome the enormous economic drag that bad fiscal and regulatory policies create. Without significant changes (and not the kind that “progressive” politicians endorse), the growth that we need will be very elusive. Think Europe.

We are one recession away from a fiscal nightmare. Lacking growth, government debt will explode. Pensions and insurance companies will be deeply underwater. In the wake of the next recession, income and employment will be hit even harder than during this last anemic recovery.

We can avoid that fate by taking the kind of steps John Cochrane outlines in his article. I would go further and say that we need to adopt budget and tax policies in the cooperative spirit of the Clinton/Gingrich era. I urge you again to read Cochrane's ideas and do whatever you can, politically or otherwise, to make some of them happen. As JC Penney once said, “Growth is never by mere chance. It is the result of forces working together.”

Update

I’ll be heading out at the end of month to Rob Arnott’s fabulous advisory council meetings, this time at Pelican Hill in Newport Beach. Those of you who know Rob and Research Affiliates know that his conference is a tad more academic than most, but he combines the intellectual heavy lifting with a fabulous food and party experience. It’s kind of like Adult Nerd Heaven. Then the following week I’ll be in New York, speaking and attending a conference.

For those who want to attend my annual Strategic Investment Conference this May 24–27 in Dallas, I hope you have registered. The conference is sold out, and we are creating a waiting list. We are trying to figure out how to accommodate more people but will not do so if we cannot make sure that the total experience for those already registered will be up to the standards we always strive for.

That said, if you want to attend, I suggest you go to the Strategic Investment Conference website and register to have your name put on the waiting list. I can almost guarantee that if we do find a way to accommodate a few more folks, those seats will almost immediately disappear, too. Those who wanted to wait to the last month to register are going to be disappointed. I won’t even tease you with the fabulous new speakers that we are seemingly adding every week. It just keeps getting better and better. And since I can’t take everybody to Austin for the amazing local music scene, we are working on bringing Austin music to Dallas. It’s going to be fun! Just a little Texas ambience for y’all.

Chicago was a whirlwind of meetings and good food. I was there with my associate Shannon Staton, and it happened to be her birthday. Along with some friends, we went to a restaurant that she wanted to try called The Girl and the Goat. It is quite famous locally and was evidently started by a lady who won a chef competition on TV. I should probably pay more attention, because the food was fabulous. Thanks to Brian Lockhart and Geoff Eliason for being wonderful hosts and introducing us to so many excellent new friends in Chicago.

In less than two weeks we are going to find out if the Republican Party is truly on its way to a brokered convention. I wrote a few weeks ago about what a brokered convention would look like, from the point of view of someone who has managed and been involved in floor fights at political conventions that are much larger than the GOP national convention. The vast majority of people have no idea just how truly wide open such a situation is. If I were responsible for running the upcoming Republican convention, I would be terrified at the prospect. National conventions are supposed to be coronations where everyone comes together, holds hands, and presents the party and the candidate to the nation. Conventions aren’t occasions when you want to air the family laundry on national TV to a world that simply won’t get the dynamics. I guess you could say the upside is that the media will be obsessed with every little twist and turn from individual delegates for three months leading up to the convention and will likely run 24-hour coverage during the convention. Then again, touting that upside might be reaching too hard for the silver lining in what could be a really dark cloud. It will be truly fascinating if the question of a brokered convention comes down to the final state convention in California. Just saying…

Your hoping that somebody will figure out the growth thing analyst,

John Mauldin

0 comments:

Publicar un comentario