Gold Weekly: Be Careful, Bears Will Come Back

by: Boris Mikanikrezai

Summary

- Money managers raised their net long positions as of February 16. The speculative positioning is not overstretched anymore.

- ETF investors continued to accumulate gold at a strong pace. Once momentum dissipate, ETF selling should resume.

- We implement a GLD short trade at $117.50 to play either a healthy consolidation or the end of the rally.

- Selling pressure will mainly come from upward revisions from investors regarding the path for fed rate increases.

- ETF investors continued to accumulate gold at a strong pace. Once momentum dissipate, ETF selling should resume.

- We implement a GLD short trade at $117.50 to play either a healthy consolidation or the end of the rally.

- Selling pressure will mainly come from upward revisions from investors regarding the path for fed rate increases.

Every week, we closely monitor net speculative positions on the COMEX as well as ETF holdings inasmuch as the historical economic behavior of gold prices suggests that over a short-term horizon (<3 months), gold prices are largely influenced by changes in the forward fundamentals, reflected in changes in net spec length and ETF holdings.

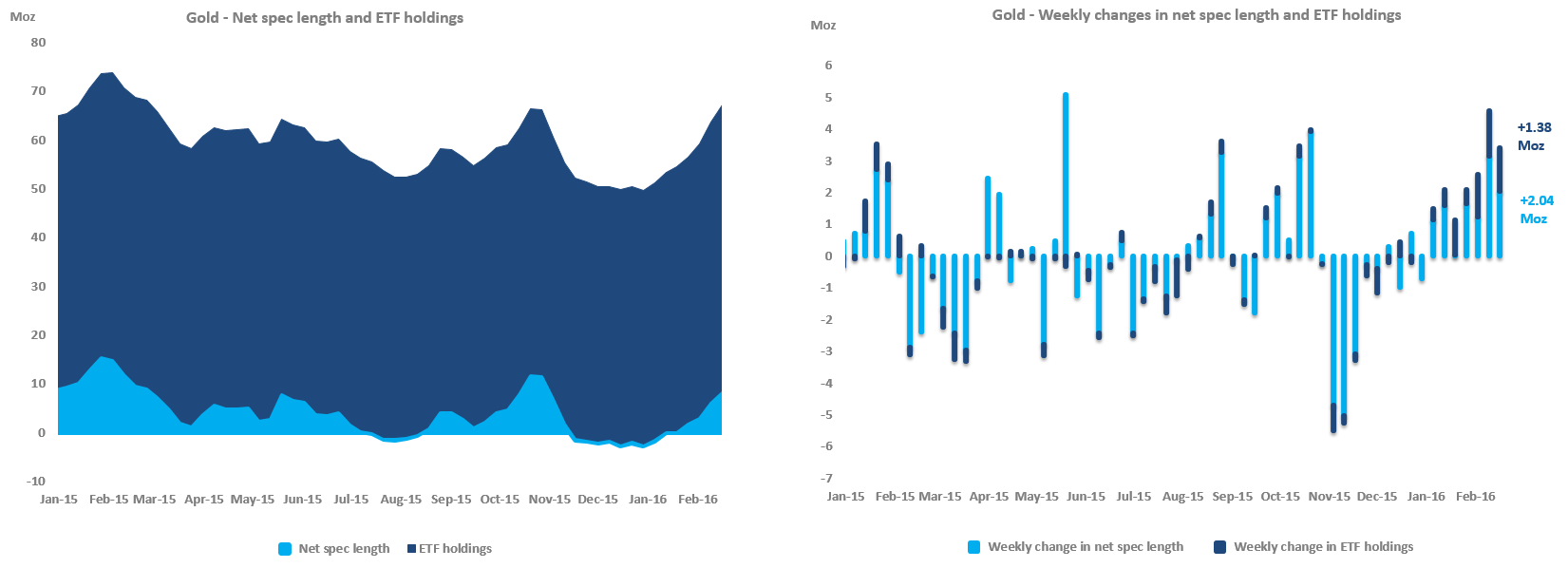

Speculative positioning

Source: CFTC.

Gold. According to the latest Commitment of Traders report provided by the CFTC, money managers, viewed as a relevant proxy for speculators, continued to raise their net long position in the week ending February 16, while spot gold prices rose 1.15 percent over the period covered by the data (February 9-16).

The net long fund position now stands at 81,013 contracts, up 20,377 contracts or 37 percent from the previous week. The improvement in spec positioning for the seventh week in a row was largely driven by short-covering (-15,217 contracts) and further reinforced by long accumulation (+5,160 contracts).

The net long fund position, which fell 114,251 contracts in 2015, is now up 108,214 contracts.

We see limited scope for further short-covering because the speculative positioning is not anymore overstretched on the short side. Indeed, the gross short position, currently at 45,206 contracts, has converged toward its long-term average (2006 - present) of 29,913 contracts.

The recent weakness in gold prices since late last week after reaching a high of $1,264 per ounce reinforces our thesis according to which the speculative positioning has now reached a neutral level.

Looking ahead, we therefore expect profit-taking (i.e. a reduction in gross longs) to occur in the coming weeks, pushing the net spec length lower.

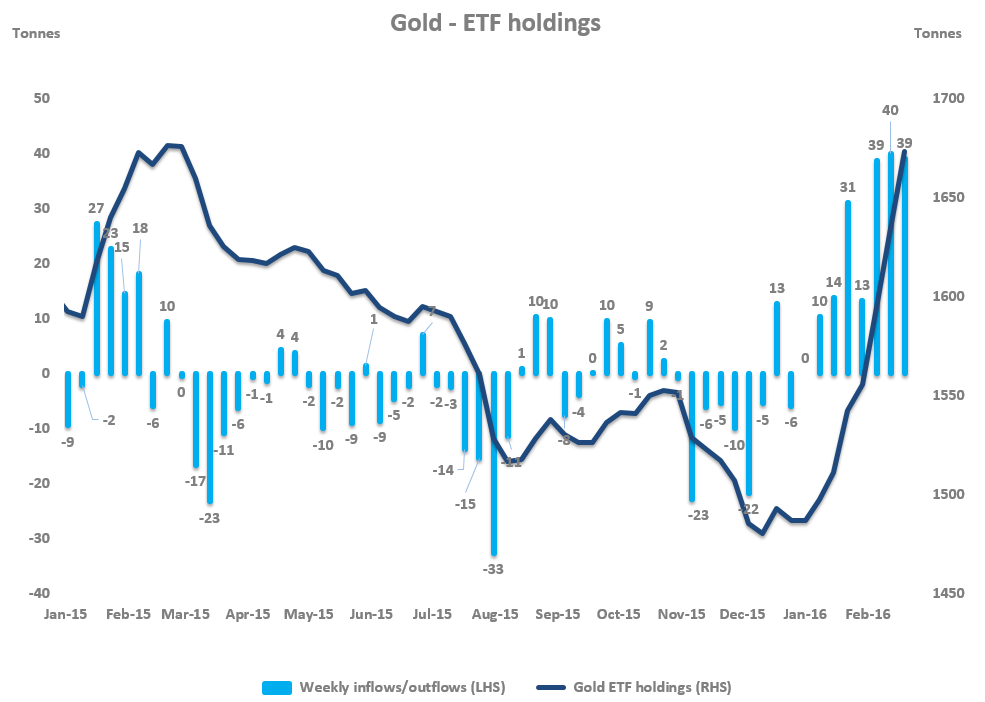

Investment positioning

Source: FastMarkets.

Gold. ETF investors bought gold for the seventh consecutive week at an average of 7.83 tonnes per day, pushing total ETF holdings up to 1,673 tonnes as of February 19.

ETF investors bought 39 tonnes of gold last week, following a 40-tonne inflow in the previous week, which marked the largest weekly increase since August 2011.

Interestingly, ETF buying was concentrated on Friday, as investors bought 28 tonnes of gold, principally from SPDR (19 tonnes), according to FastMarkets' estimations, despite the fact that gold prices posted a 0.38-percent decline on that day.

Investors continued to accelerate their buying last week, which we attribute partly to loosening Fed tightening expectations following the testimony of Fed Chair Yellen on February 10 and 11.

Although her assessment on the US economy was broadly unchanged from that in December, her dovish remarks on negative interest rates as she pointed out "we would not take negative rates off the table", prompted investors to revise downward the expected pace and timing of US rates, as evidenced by the fall in the US 10-year yield and the decline in the dollar.

But we continue to believe that recent ETF buying has been exacerbated by tactical investors who aim at playing momentum over short-term horizons. If our thesis proves correct, this would suggest that ETF investors could reverse their buying in the near-term in so far as momentum is now fading.

Importantly, it is important to note that the rally in gold prices from the start of 2016 was largely driven by downward revisions from investors regarding the path for future fed rate increases, pressuring the dollar and (real) interest rates, which in turn boosted gold prices. But there is a clear divergence between investors and the official Fed views about expected Fed rate increases. According to the latest CME statistics, investors currently expect no rate increase in 2016, compared with 3 or 4 rate increases expected by the Fed. I guess that the reality is somewhere in between. I therefore conclude that gold buying has become too aggressive recently, suggesting that the risks to gold prices over a 3-month horizon are now skewed to the downside.

ETF investors have already bought 118 tonnes of gold in February after accumulating 74 tonnes in January, pushing total net inflows for the year to 192 tonnes, according to FastMarkets' estimations. As a reminder, ETF investors sold 112 tonnes of gold in 2015, after liquidating 158 tonnes in 2014 and 889 tonnes in 2013.

Looking ahead, we expect ETF inflows until the remainder of this month, but a reversal is likely either this month or at the beginning of the second quarter of 2016, we think.

Spec positioning vs. investment positioning

Source: MikzEconomics.

My GLD positioning - weekly chart

Source: TradingView.

The SPDR Gold Trust ETF (GLD) showed signs of exhaustion last week, closing at $117.54, slightly down from previous' Friday closing at $118.

After initially building a long GLD position at $104 on January 6, we closed our position last week (see our article) at $119, resulting in a profit of $15 per share, with an initial risk of $4 per share, providing us a reward-risk ratio of 3.75.

For a number of reasons that we will discuss shortly, we decided to implement a small short position on GLD on Friday at the close, i.e. $117.50, with a stop loss at the high of previous week ($120.83), in order to play either a temporary consolidation or the premature end of the rally.

Indeed, similar to last week, our crystal ball regarding gold prices in the near-term (<1 month) remains cloudy, but we believe that the risks are skewed to the downside.

First, the run-up in gold prices has led to overbought conditions from a technical perspective, which should therefore result at least in a mild correction to alleviate these overbought conditions.

Second, equities are showing signs of stabilisation, which suggests a rebound in risk-appetite. In this context, market participants who initially built risk-off related trades (long positions in government bonds or gold) should therefore pull back, pushing gold prices lower.

Third, short-term tactical investors could also exit their positions because there are tangible signs that gold has found near-term resistance, making the upward momentum story less attractive, at least for now.

Fourth, as we noted in our ETF positioning analysis, the clear divergence between the Fed and investors' view will probably dissipate in the weeks ahead, on the back of important macro data releases, which should induce upward revisions of the path for future fed rate increases, thereby pushing gold prices lower.

In this context, we believe that implementing a short GLD trade could offer a reward-risk ratio skewed in our favour. The main risks to our short GLD position would be 1-renewed signs of instability in the financial markets, prompting investors to re-build risk-off related trades and 2-buying on the dips from investors who did not participate in the rally due to their lack of conviction.

To sum up, we believe that the rally in gold prices has run ahead of itself, placing the risks to gold prices over a 1-month horizon now skewed to the downside.

0 comments:

Publicar un comentario