Gold: Tipping The Scales

by: Eric Parnell, CFA

.

Summary

- Gold continues to push to the upside, furthering what has been an impressive start to 2016.

- But what exactly has been driving gold higher in recent months?

- And is this force sustainable beyond the short term?

- But what exactly has been driving gold higher in recent months?

- And is this force sustainable beyond the short term?

It is worthwhile to begin by stating the following: I am meaningfully bullish on the long-term outlook for gold, and I have been for some time. Gold offers protection against price instability, whether it is inflation or deflation, and also provides a hard asset alternative global reserve currency versus the various paper fiat currencies that are backed by nothing more than the full faith and credit of their issuing governments and have been relentlessly distorted by unprecedentedly aggressive monetary policy by global central bankers during the post crisis period. In short, gold offers an ideal portfolio hedge and a lot of long-term appeal.

But it is also recognized that gold has endured a particularly difficult stretch over the past five years that has included a relentless decline from its 2011 peaks. The yellow metal has had a number of solid rallies along the way that have ended up being nothing more than false starts.

As a result, it is worthwhile to repeatedly put the latest gold rally to the test to make sure it can sustain what it has started. For once it truly gets going to the upside, the subsequent gains potential associated with gold is substantial. For these reasons, I have been for some time and remain to this day cautious about gold in the short-term.

A Primary Driver Of The Recent Gold Rally

So what exactly has been driving the recent rally in gold (NYSEARCA:GLD)? As discussed in a recent article, it has not been safe haven demand as of late, as the stock market (NYSEARCA:SPY) has been in full fledged rally mode since February 11 in gaining more than +10% over last few weeks. And it also has not recently been U.S. dollar weakness (NYSEARCA:UDN), as gold has managed to hold its ground despite a strengthening of the U.S. dollar (NYSEARCA:UUP) since mid-February. It has also notably deviated from silver (NYSEARCA:SLV), although it should be noted that the white metal has done rather well in working to catch up to the upside in recent days. If it is not any of these forces, what exactly is it?

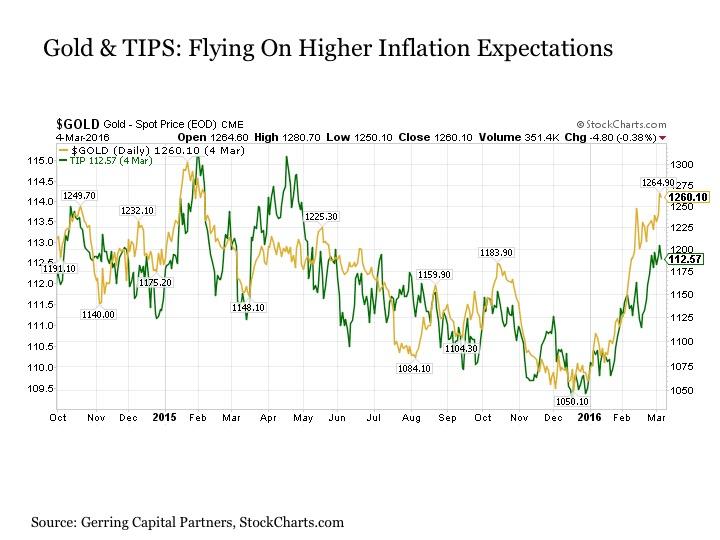

Inflation expectations appear to be the major driver of the gold price since the start of the year. Highlighting this point, it is worthwhile to overlay a gold price chart with that of Treasury Inflation Protected Securities, or TIPS (NYSEARCA:TIP). We can see that the relationship between gold and TIPS has been quite strong in recent years, albeit with gold exhibiting a notably higher beta relative to TIPS.

This raises an important question. If expectations for higher inflation going forward is a primary driver of the recent upside in gold, how sustainable are these expectations and subsequently this price advance in gold going forward?

Examining Inflation Expectations

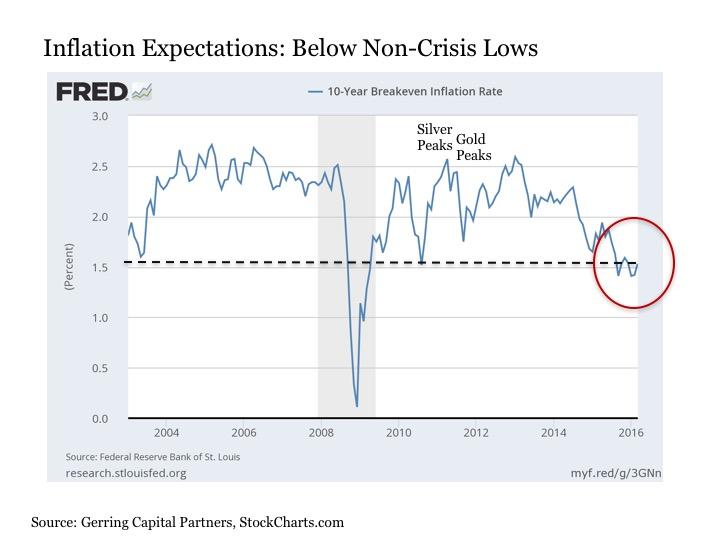

For answers, it is worthwhile to examine a chart of the 10-Year breakeven inflation rate for answers. This market based measure of expected inflation based on the difference between the yield on nominal bonds and inflation-linked bonds of the same maturity at ten years provides insight as to what inflation expectations have been in the past and what they are projecting to be going forward.

A few points are notable when reflecting back over the past decade.

First, inflation expectations have been chronically weak for the past five years. In fact, the peak in post crisis inflation expectations in April 2011 coincides almost exactly with the peak in silver prices. Of course, the top in gold followed a few months after in September 2011, and the rest has been a steady move to the downside for both inflation expectations and precious metals in the five years since.

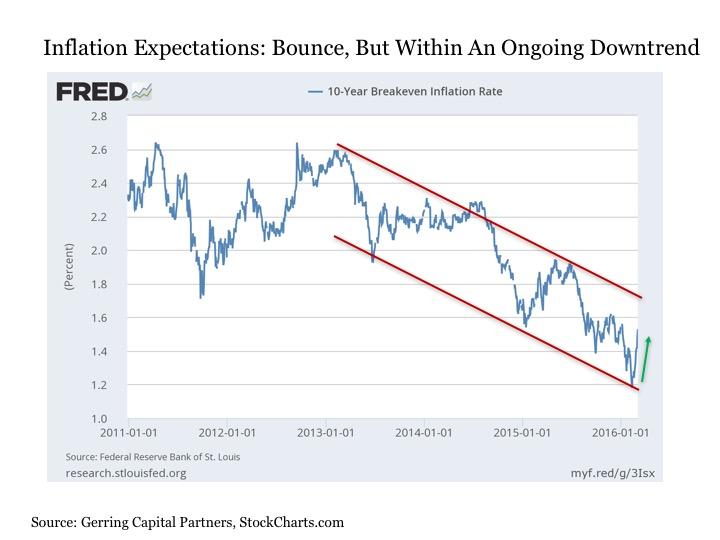

Second, inflation expectations had fallen so much recently that they recently reached levels that represented new millennium lows at 1.2%. Given how far inflation expectations had fallen, the fact that we have seen a measurable bounce higher in recent weeks is not necessarily a surprise.

Instead, the bigger question is whether the recent bounce is strong enough that it can follow through into a sustained reversal of the five-year downtrend? This would certainly be a welcome development for the U.S. Federal Reserve that remains eager to raise interest rates in an attempt to normalize interest rates and store up some dry monetary policy powder for the next recession.

Is The Recent Reversal Sustainable?

In order to determine whether the recent surge in inflation expectations is sustainable, it is worthwhile to consider the recent causes of the weakness in the first place.

A primary driver of weakening inflation expectations has been the chronically weak global growth outlook. Developed and emerging economies across the globe are continuing to struggle in the post crisis period in their efforts to reignite sustainably strong economic growth. Many have been mired in a deflationary slump and are struggling with increasingly impotent monetary policy responses and largely absent fiscal policy alternatives. Given the trend toward negative interest rates, it does not appear that these deflationary forces are set to change any time soon.

Another force that has been driving fading inflation expectations has been chronically weak commodities (NYSEARCA:DJP) prices. From agriculture (NYSEARCA:DBA) to base metals (NYSEARCA:DBB) such as copper (NYSEARCA:JJC), commodities prices have been falling steadily for years. And starting in the summer of 2014, energy prices including oil (NYSEARCA:USO) and natural gas (NYSEARCA:GAZ) have cascaded lower with a vengeance.

It is from this second category that a source of sustained inflationary pressures could potentially be derived. Prices across the commodities complex have fallen so far over the last several years that at some point they may be overdue to start rebounding higher, particularly as supply and demand fundamentals begin to right themselves across these various complexes. For example, oil prices have fallen from $108 per barrel as measured by West Texas Intermediate Crude in June 2014 to as low as $26 per barrel last month. At some point, oil prices will finally bottom and begin to recover or at least stabilize. The same could be said for copper, which peaked at $4.65 per pound back in early 2011 and have fallen as low as $1.93 per pound not long after the start of the year.

Put more simply, if we see a steadying of commodities prices and a sustained reversal higher after several years of steady decline, this will likely have a feed through effect of sustaining higher inflation expectations going forward.

But all of this remains a very big if. For while so many commodities are now trading so far below their all-time highs, these lows are still meaningfully higher than what was in place for years just over a decade ago. What was the big change that came along around the start of the new millennium?

China (NYSEARCA:GXC) emerged as a major buyer of commodities from across the globe. And if recent economic problems that have been plaguing the second largest economy in the world in recent years continue to manifest themselves, it is possible that we could see further downside in commodities prices as what has been by far the world's largest buyer continues to step back demand.

Only time will tell.

Bottom Line

Gold is a commodity that looks set to run to the upside. After five challenging years, the recent rally in gold has decisively broken a variety of long-term technical resistance levels. And a variety of sound fundamental reasons can be put forth as to why the recent rally is likely to continue well into the future. But with all of that said, it appears that the recent rally in gold is riding primarily on the bounce in inflation expectations. Other factors may eventually move to the forefront to continue the advance in gold, but in the near-term it is now worth watching inflation expectation signals such as TIPS, oil and industrial metals prices for signals as to how much longer the recent rally in gold may last. But if and when we see a sustained pullback in the gold price, it may provide some particularly good entry points to either initiate or add to existing long allocations. The key will be the set up if and when such a pullback finally arrives.

0 comments:

Publicar un comentario