Gold Is Due For A Pullback

by: Vladimir Zernov

Summary

- Gold rallied from $1050 to $1250 without any pullback.

- This was a fear-induced trade.

- As markets calm down, gold will fall from current levels.

- This was a fear-induced trade.

- As markets calm down, gold will fall from current levels.

Gold's (NYSE: GLD) rally was spectacular. The precious metal reacted to the general market's downside and shot to highs that were last seen in the first half of 2015.

Some investors believe that this rally marks the end of the multi-year bear market for gold. Others argue that gold went too far too fast. In this article, I lay out my views on the topic and discuss what factors will have influence on gold in the near term and what factors will likely be ignored.

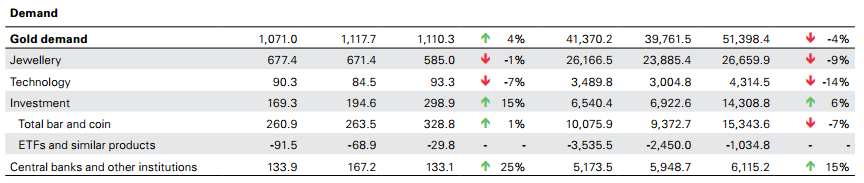

Demand

Let's look at the latest data by the World Gold Council.

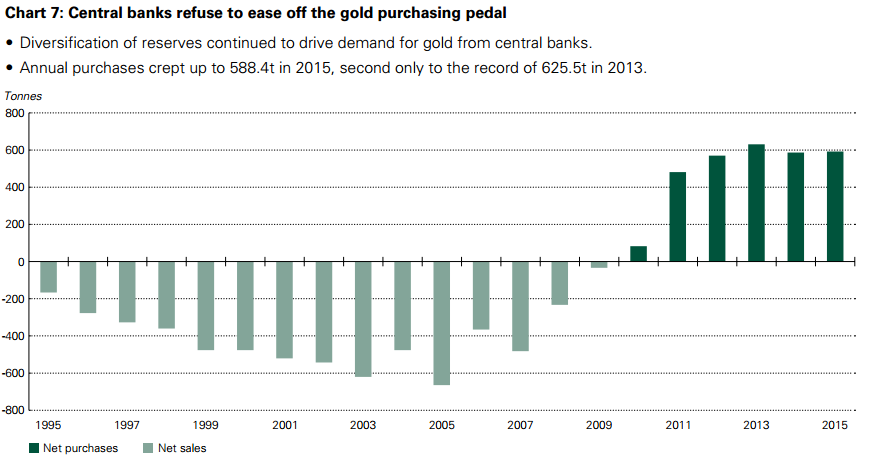

Gold demand increased in the fourth quarter of 2015 compared to the fourth quarter of 2014, and this increase was attributed to the increase of investment purchases and central bank purchases. It looks like Central Banks took their chance to purchase more gold for diversification purposes while the gold prices were relatively low.

Source: World Gold Council

One could argue that Central Banks are the smartest guys in the room so you should closely follow their action. However, the World Gold Council's data suggests the opposite. As you can see from the graph above, Central Banks were actively buying gold since 2011.

So, Central Banks started buying gold when it was $1400 per ounce, bought gold all the way up to $1900 per ounce and continued their purchases while the gold fell under $1100 per ounce. Prior to 2010, Central Banks were net sellers of gold. This data suggests that you probably should not be replicating the behavior of Central Banks on the gold front.

I'd argue that it was just natural for Central Banks to buy some gold given the low interest rates around the world. Gold pays no interest, but its liquid competitors also pay little interest. Thus, buying gold as a means of diversification looked like a smart idea for Central Bankers around the world.

Also, one should not forget about the risk of negative interest rates. The gold's inherent weakness as a storage of value is the fact it pays you no interest. This weakness turns into strength once you have to pay to park your money. When I was a kid and did not know about the existence of interest rates, I thought that people pay the bank to look after their money.

Back then, I thought that money was safer in the bank than under the mattress, so it was logical for me to believe that people pay for safety. As it turned out, banks are not invincible and, generally, people will try to avoid paying the bank for using their money. The negative interest rate world is certainly bullish for gold.

The Central Bank purchases and possible inflows into ETFs look bullish for gold. The other contributors to gold demand, technology and jewelry, will likely be bearish contributors. Technology is moving away from gold, especially in the dentistry section.

I believe that the current trend will continue and technology's demand for gold will shrink year after year. The good news for gold is that technology is the smallest contributor to overall demand, so big percentage drops in technology demand will result in rather small physical decreases in demand.

I expect that jewelry will take a hit. India could be a bright spot, but others will likely suffer. Demand from Russia and Turkey will continue to fall. Given all the political and economic hardship in two countries, its consumers will take a serious hit.

Middle East markets also don't provide sources of optimism with oil near $30 per barrel. The demand in Europe remains anemic, and I think that you can't only blame economy for this.

In my opinion, cultural reasons also play a role in Europe's gold demand dynamics.

In my view, the situation on the demand side will ultimately depend on whether increased Central Bank purchases and flow of money into gold ETFs will be able to offset declines in jewelry and technology.

Supply

Not surprisingly, supply dropped due to lower gold prices. Both mine supply and recycled gold contributed to the drop. I would argue that we will not witness a similar supply drop this year. Judging from what we heard from gold miners during this earnings season, they adapted to the gold price environment and generally don't need further cuts to improve their cost profiles.

For big players, current costs are well below current gold prices so they will likely produce as much as the can while remaining cautious about new capital-intensive projects. It will take much more than a few months of gold upside before we see the return of serious risk appetite for new ventures in the gold mining space.

All in all, the supply side looks moderately bullish for gold. In my view, we cannot expect a flood of new gold into the market after years of the bear market. On the other hand, it looks like gold companies trimmed the excessive projects and will likely make minor changes to their portfolios going forward.

Do supply and demand matter now for the gold price?

I believe that it there was no sudden change in the supply/demand balance in the last few months that could cause the rally in gold. Gold is a financial asset, like stocks or bonds, and money constantly flows in and out of assets and asset classes.

Currently, it looks like gold was a part of a major "fear trade". As money exited from biotech (NYSE: XBI) or energy (NYSE: XLE), it had to find a place somewhere. The first part of the "fear trade" led to purchases in dividend stocks that, in theory, should protect investors in case of additional market downturn.

Look at the charts of AT&T (NYSE: T), Consolidated Edison (NYSE: ED) or Verizon (NYSE: VZ) - their new highs reflect the demand for safety in uncertain times. The second part was the gold trade that quickly pushed gold from $1050 to $1200.

In my view, demand and supply dynamics for physical gold had little to do with the recent surge in gold price. That's why I believe that investors' stance on gold must depend on their view of where the general market and interest rates will be heading and also on their view about the fate of the U.S. dollar.

What could cause the next leg of upside?

I see several catalysts that could propel the gold price higher. The first one is negative interest rates in the U.S. I don't see this coming and I expect that the Fed will be able to raise the rate at least once this year.

Apart from my view that negative interest rates are absurd and won't work for anyone, I just can't see what problems make cause the Fed to step into the negative interest rates territory in 2016 after they just made their first hike.

The second possible catalyst is sub - $25 oil. Currently, oil looks stuck in the wide range and it looks like the negotiations among producers and continuing cuts in U.S. rigs finally stopped the never-ending oil price downside.

I am a bit upset with this development as oil was so close to my December target of $25 per barrel, but I still see risks that oil could retest lows if production freezes lead to nothing and Iran ramps up its production ahead of expectations.

The third catalyst is the weakness of the U.S. dollar. I don't expect this. I believe that demand for U.S. currency will continue to grow amid problems in multiple parts of the world.

I don't think that the dollar is overvalued now, although it clearly creates some problems for multinationals who got accustomed to the artificially low dollar exchange rates.

I don't see any of these possible catalysts coming now. Hence, I'm in the "too far too fast" camp and I believe that the current rally is due to a pullback. I think that when the S&P 500 breaks 1950 we will see a massive sell-off in gold.

0 comments:

Publicar un comentario