France's Economic Deterioration Confirms That The Euro Currency Is A Failing Experiment

by: Zoltan Ban

- France entered the 2008 global crisis as an AAA country. Its current economic indicators, such as the unemployment rate, deficits & debt make it look more like a PIGS member.

- The Euro currency, which is too strong for some, while much weaker than should be for others, which is what led to the PIGS is also main factor affecting France.

- Whether France decides to leave the Euro experiment now, or waits for its demise, the end result will most likely be sovereign debt default.

- Most other European countries will most likely share the same fate, within about a decade at the most. We should start preparing, because it could happen at any moment.

- The Euro currency, which is too strong for some, while much weaker than should be for others, which is what led to the PIGS is also main factor affecting France.

- Whether France decides to leave the Euro experiment now, or waits for its demise, the end result will most likely be sovereign debt default.

- Most other European countries will most likely share the same fate, within about a decade at the most. We should start preparing, because it could happen at any moment.

It may not fit in as neatly as PIIGS, when it comes to acronyms, but I do believe that this increasingly fits the reality of the economic situation in Europe. Ireland is set to resume its strong economic performance, helping it dig itself out from the aftermath of its banking crisis, which caused its debt/GDP ratio to almost triple, from 44% in 2008, to 120% by 2011. Thanks to disciplined fiscal budgets, as well as robust economic growth, it managed to cut its debt/GDP ratio to below 100% as of the end of 2015.

The rest of the PIIGS, which in fact should read PIGS right now, have not fared very well since the crisis. In fact, it seems that without the ECB and the IMF, most of these countries would be in deep trouble. At the root of the problem in my view is the euro currency, which is way too strong for the needs of these countries. It is the economic performance, especially when it comes to net exports of countries like Germany, which is making the euro currency too strong. They fall further as a result, pushing the euro further below the level it would have to be if it were to reflect only the German economy. That in turn further stimulates Germany's export capacity.

It is a vicious cycle, which will never loosen its grip on the poor euro countries caught in it.

It may be argued that Ireland escaped therefore it is possible to exit the vicious cycle, but fact is that Ireland was never really caught in it. Its economy always had the capacity to resume the strong growth trajectory it saw before the 2008 crisis. The weak euro, mainly stemming from the Greek crisis, as well as worries about Italy, Spain and Portugal have in fact benefited Ireland, which just like Germany is rather competitive, aside from its banking sector which managed to get itself into trouble.

France sinking slowly but surely.

Entering the 2008 crisis, France was one of the AAA rated countries, considered to be one of the euro-area pillars of stability, alongside Germany. Since 2008 however, France's vulnerability has been exposed and frankly it is currently grossly under-estimated in my view.

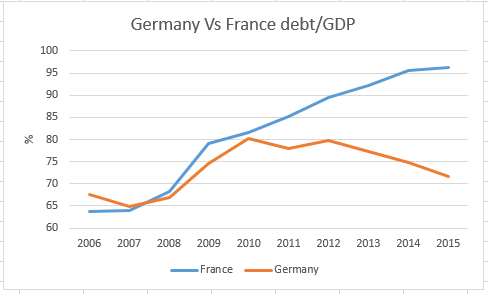

While Germany continued to maintain its solid fiscal situation and managed to solidify its trade balance situation, France is failing on all fronts.

Data source: Trading Economics.

As we can see, France is unable to get its government debt situation under control. In fact, it has been getting waivers from being subjected to sanctions due to its deficits surpassing the 3% threshold, under the Excessive Deficit Procedure rules for years now.

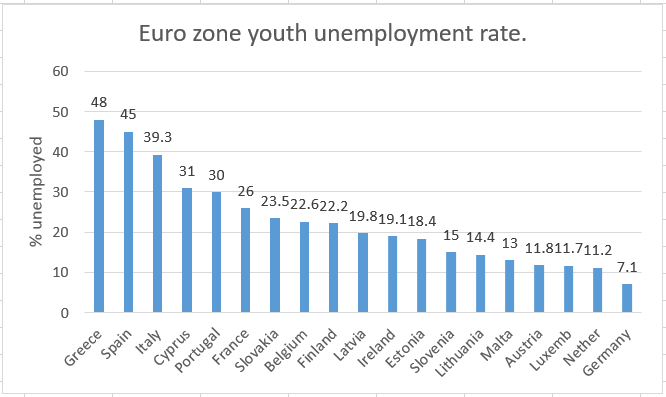

Unemployment is another problem area for France. Unemployment was a problem before, with the period before 2000 seeing it go over 10%. Between 2000-2008 things were on an improving path, with unemployment dropping below 7.5% by the beginning of 2008. Since then, it kept increasing.

By 2012, it went above 10% and has been there ever since. Presently, it is 10.2% as of January, according to Eurostat. A most worrying aspect of the January numbers is the progression of the youth unemployment rate. It went from 24.8% in January, 2015, to 25.9% in January, 2016. In this regard, it is firmly in the PIGS camp in the Eurozone. It is not yet as high as it is in those countries, but aside from Portugal, Italy, Spain and Greece, France does have the highest youth unemployment rate in the euro zone, aside from tiny Cyprus.

Data source: Eurostat.

It is very important to highlight youth unemployment when it comes to talking about a country's economic future. The young are always the future. As their lives will go in the longer run, so will the future of the society they belong to. As we can see, the young citizens and residents of France are not off to a very bright start.

More immediate results of failing to provide the environment for young people to launch themselves career-wise is a loss of the investment society makes in education, as their abilities gained through education tend to be lost and in many cases forever under-utilized. As a consequence, many people in this generation also lose the ability to become good consumers.

Construction, which tends to be a great boost to labor demand, ends up suffering as an increasingly large number of young people fail to form a family and buy a house. No house means no need for furniture either, and therefore no need for factories and stores selling the furniture. The trend works through the economy, leading to even fewer opportunities for young people.

A low income level and a lack of income stability also dampens demand for other goods such as cars or entertainment services such as restaurants. It feeds through the economy, with every year that passes, as a shrinking number of young people join the workforce due to demographic trends. Even among this shrinking demographic, far fewer of them become relatively successful in establishing a middle class lifestyle proportionally speaking, compared with previous post-WW2 generations.

It is very important to understand that the youth unemployment rate we are seeing is a symptom of a sustained deterioration of the French economy, but at the same time it is becoming a causing factor in cementing the trend of deterioration. It is an irreversible trend as long as major changes fail to materialize. There are those who think that it is only a matter of changing government policy on labor protection, taxation and other such adjustments. But in reality, there is only one way out, and that way is a return to its own national currency. It is clear at this point in time that France needs a currency which will weaken much more than the euro has in the past few years. The euro without the German effect would be much weaker today than it is, and it is in fact what most euro zone economies need, including France.

Short-term effects.

It is not as if France is the only country facing economic difficulties in the EU. Countries in the euro zone such as Cyprus, Belgium, Finland, Slovenia have all struggled to find traction through this so-called recovery period, which officially started in Europe in 2013. The reason why we need to keep an eye on France is because it is the second-largest Eurozone economy, meaning that the EU itself cannot gain much traction, especially given that Italy and Spain, which are the euro zone's third and fourth largest economies respectively, are also struggling. If the EU fails to gain traction and put in a few years of robust growth, then it is harder for France to exit its own slump as well.

Unlike smaller countries such as Slovenia, or Cyprus, which could go through an economic slump without having much effect on the overall EU economy, and tag along if the EU economy booms again, with France reality is that the EU cannot really enter a boom period without the full economic participation of France. At the same time, France cannot recover without an EU boom. This is especially the case given that many of the products made in France, such as cars, do not have the same access to the global market as German brands do. Renault, Peugeot and Citroen, which are France's car makers are all missing from the North American market, while German car producers are all present and selling in significant volumes.

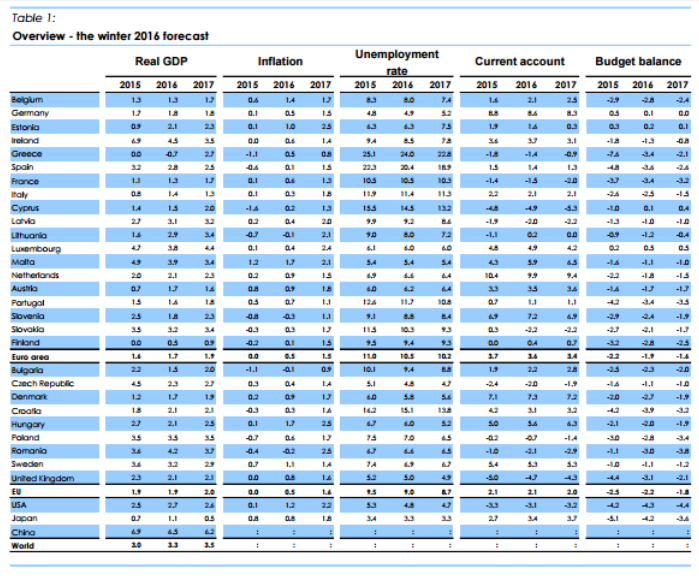

The resulting effect of the current situation is well-illustrated in the EC winter 2016 forecast for this year and next.

Source: EC Winter 2016 forecast.

As we can see, this year and in 2017, France's economy will continue to grow considerably slower than the EU average. It is also one of only a few countries unable to bring its deficits below 3% as demanded by EU treaties. By 2017, it will be one of only two countries with a deficit above 3%, alongside Portugal in the 19 member euro zone. Even Spain, Italy and Greece are forecast to achieve deficits considerably below 3%. The unemployment rate is also set to continue to stay above the 10% threshold. We should keep in mind that this forecast does not include a possible global recessionary event, which would drastically change the outlook for the EU and France. At this point, if a global downturn were to strike this year or next, we could potentially see a situation where France will have to run deficits deemed much higher than considered to be sustainable, leading to a French sovereign debt crisis as bond investors rush for the exit door. Alternatively, we could see France attempting to reign in its deficit through a global downturn, which would in effect cause a similar economic contraction to what we have seen in Greece as it attempted to catch up to its fiscal imbalances, with counter-productive results, which resulted in a huge plunge in economic output year after year. Either way, whenever the next recession comes, given the poor state of France's economy when entering it, its chances of coming out of it as anything else but an addition to the PIGS club are slim, even if the acronym might not work as well in forming a neat word to remember it by.

Longer-term consequences.

As we saw with the Greek crisis, the end-result can only be one, and that is default. Greece did not officially go through a default yet, but it will, despite more than half a decade of suffering inflicted on its population in a futile attempt to prevent it. Similarly, whether France decides to dump the euro now, or a decade from now, after continued deterioration of its economy, the end-result can only be one and that is sovereign debt default. As I pointed out, France cannot hope to reform itself into competitiveness within the euro currency context. It could leave the euro now, but that will also come with its own pain and suffering. The increased costs of dealing with its main trade partners due to currency issues would initially offset the gain from having its own adjustable currency. Switching back to the French franc would also mean that markets would demand a much higher interest on France's bond issues, leading to a significant increase in interest expenses, putting further pressure on its government finances. This would lead to a spike in its debt/GDP ratio, leading to an eventual default within a few years.

As bad as that sounds, it would in fact be better for France to go down that road than continue on with this failed experiment. Sticking with the euro will only lead to a continued deterioration of its economy. It will continue to deteriorate until France will either decide to exit, be pushed out, or until the whole experiment comes to an end, which I would not dismiss at this point, given what is going on in Europe at the moment.

Implications for the global economy and investors.

The continued deterioration of France's economy, which was considered an AAA country by the ratings agencies going into the 2008 crisis, is perhaps the most credible confirmation that the euro currency is a failed experiment. It is now only a matter of time before it unravels at some point, in some fashion, leading to European economic disaster and a severe global crisis. The countries comprising the euro area, collectively make up the second largest economy on the planet after all, therefore the fallout will be very significant when it will happen.

Whether the euro will collapse this year as a result of the endless crises facing the EU, ranging from the continued economic stagnation, the threat of a British vote to exit the EU this summer, the continued antagonism between the EU and Russia, or the migrant crisis which is causing an unprecedented level of friction and animosity between EU countries, as well as between the people and their elites, whom they increasingly do not trust, makes it increasingly likely that the euro experiment will end rather soon. Even if that is not the case and all these problems will either go away or Europeans will manage to cope with the challenges and the consequences, the continued destruction of many euro zone economies means that the euro currency is unlikely to survive the shock of the next global economic downturn. There is simply nothing left to prop it up with.

Governments already have too much debt to try fiscal stimulus and the ECB is already being as accommodating as it can get when it comes to interest rates and QE. What this means to all of us is that we need to start preparing ourselves for a collapse of the euro within a decade at the latest. Odds of it happening are in my opinion higher than the odds of it not happening, so we all need to have a strategy meant to cope with the fallout.

My strategy is to keep some gold exposure, in case that it all unravels very suddenly. Others may try to bet on the US dollar and assets denominated in the US currency. Some more adventurous individuals may venture to prepare to short relevant assets, such as European ETF's or individual European companies. Some of these strategies may work better than others. One thing that is guaranteed to not work in my opinion is to ignore the facts and continue to just assume that this will work itself out. As the case of France shows us, there is no way out of this grand failing experiment, except for economic catastrophe.

0 comments:

Publicar un comentario