A Crude Awakening For Banks And Stocks

by: Jieming Se

Both the S&P500 index and oil have started 2016 with a major sell off.

Banks were worst hit due to concerns over possible write downs of energy related loans.

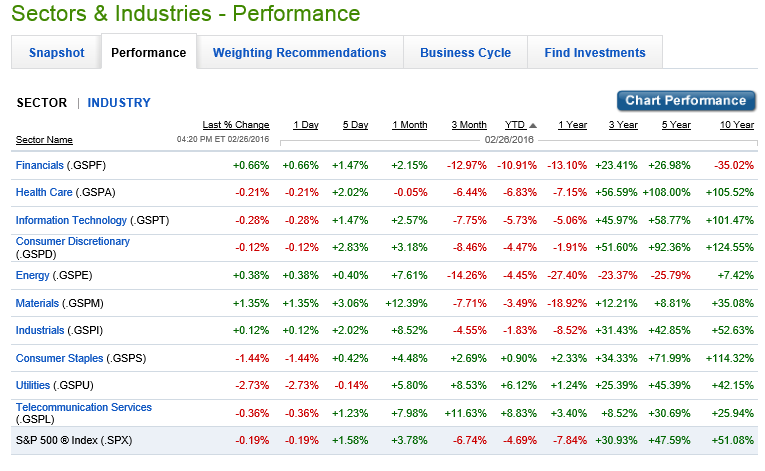

The financial sector has been the biggest contributor to S&P 500 earnings over the past year in the midst of the weakness in energy.

Some see the 2016 decline in oil as a potential repeat of the 2007 fall in home prices that led to subprime crisis.

Banks are better capitalized in 2016 and have far less exposure to oil and gas lending than they were to mortgage debt in 2007.

Banks were worst hit due to concerns over possible write downs of energy related loans.

The financial sector has been the biggest contributor to S&P 500 earnings over the past year in the midst of the weakness in energy.

Some see the 2016 decline in oil as a potential repeat of the 2007 fall in home prices that led to subprime crisis.

Banks are better capitalized in 2016 and have far less exposure to oil and gas lending than they were to mortgage debt in 2007.

Figure 1: Smoke on the water, fire in the sky. The oil markets have crashed and burned with disastrous effects on the financial sector. (Source: Flickr)

A crude awakening in 2016

US stock markets woke up in 2016 to the smell of burning oil. The S&P 500 index lost about 5.47% for the first two months of this year, reaching a low of 1,810.10 on 11th February before retracing back some of the losses to end February at 1,932.23. Crude oil has performed even worse. The United States Oil Fund (NYSEARCA:USO) (which tracks the daily price movements of West Texas Intermediate light sweet crude oil contract) lost more than 18% by the end of February.

Figure 2: On a year-to-date basis, the S&P 500 index has lost 4.87% while USO has plunged 20%. (Source: Yahoo Finance)

Amidst the market mayhem, the linkage between oil and stock price movements has been making headlines in the news. According to CNBC, the 30-day running correlation between WTI futures and the S&P 500 index reached above 0.6, a level not seen since early 2013. Oil and stocks have also moved in lockstep 83% of the trading days in February.

Historically, low oil prices were good for the economy as this meant lower productions costs and better profit margins for companies. However, since the 2008 financial crisis, a boom that took oil prices from $40 per barrel in 2009 to more than $100 a barrel in 2015 has become a new engine of growth for U.S. stocks. The conventional economy began to transform to a new commodity driven economy during this period as it relied more on oil explorers and shale producers to drive profit growth.

Banks and financials were able to tap in on oil companies' appetite for credit to earn fees and interests by financing their debt. Therefore, when crude oil prices fell drastically this year, what started out as doubts over the profitability of energy companies begin to morph into fear of default on oil related debt. Financial stocks were the hardest hit this year.

Smoke on the financial sector, fire in the SPY

Contrary to popular belief, financial stocks and not the energy sector has been leading the sell-off in 2016. On a year-to-date basis, Financials have lost 10.9% making it the worst performing sector among the 10 S&P 500 groups, even underperforming the Energy sector's 4.45% loss.

Figure 3: The energy sector may have lost 27.40% over the past year but the financial sector is leading the decline on a year to date basis in 2016. (Source: Fidelity Research)

Figure 4: The Financials sector ETF has lost 10.3% this year, creating a major drag on the performance of the S&P 500 index. (Source: Yahoo finance)

Mirroring the decline, the Financial Select Sector Fund (NYSEARCA:XLF) has also incurred double-digit losses and is the main sector dragging down the SPDR S&P 500 ETF (NYSEARCA:SPY) this year. Worries over possible defaults on oil related loans and potential bankruptcies in the energy sector has gripped the markets this year, leading investors to question the outlook and future profitability of banks. Some reports in the media have even compared the current correction in the oil markets to the fall in home prices in 2007 that sparked off the subprime mortgage crisis and a wave of write downs of mortgage related debt.

This fear is not entirely unjustified as banks have been the main contributor to S&P 500 earnings. But whether the correction will morph into an Oil-pocalypse similar to 2008 deserves further analysis.

Oil burnt down the earnings house

Since oil prices started correcting downwards from $100 in 2014, earnings from energy companies have already started to decline around September 2014. Energy sector earnings contribution began turning negative for the quarter ending March 2015 and has remained in the red for 3 straight quarters.

Figure 5: Financials have been the biggest contributor to operating earnings for the S&P 500 over the past year while energy earnings remain deep in the red. (Source: Data from S&P Dow Jones Indices with analysis by author)

Conversely, earnings contribution from the Financial Sector has started to increase as a proportion of S&P 500 operating earnings since March 2015. It reached a high of 24.4% in March of last year and has generated almost a quarter of overall index profits for 3 straight quarters. In other words, Financials have been supporting earnings and earnings growth amidst the turmoil in the oil markets last year. If credit losses and write-downs on the energy portfolio start to materialize and drag down S&P 500 earnings what would be the impact on the index?

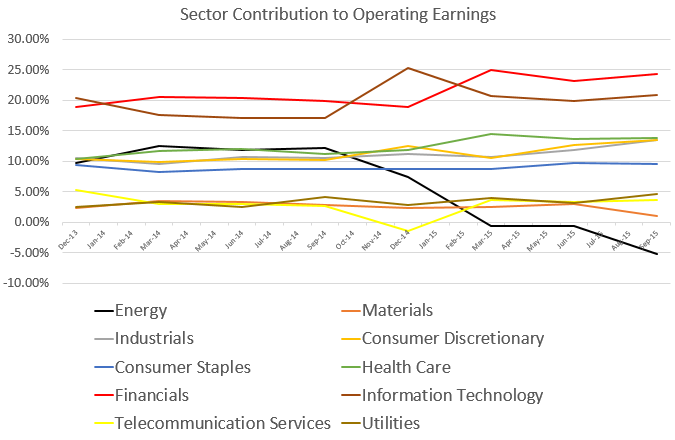

Figure 6: A steep decline in corporate earnings in 2008 caused a precipitous plunge in the S&P 500 index. (Source: data from S&P Dow Jones Indices with analysis by author)

The long-term price movement of the S&P 500 index generally follows operating and reported earnings per share very well in terms of both direction and magnitude. When earnings started declining from its peak in 2007, the index reflected the fall in subsequent quarters by falling almost 50% from Sep 2007 to December 2008. Reported earnings per share bottomed at a loss of $23.25 during the fourth quarter of 2008. The index rebounded in the following quarters as it got lifted by a turnaround in earnings.

With the current correction in oil prices reminiscent of the plunge in home prices in 2007, investors are starting to ask the trillion dollar question of whether we will see a repeat of the 2008 financial crisis for banks and stocks in 2016. In other words, will earnings fall off the cliff again and lead the index to correct by 50%? To answer this question, we have to compare the aggregate debt levels and the capitalization of banks in 2016 against pre-crisis levels in 2007.

Will 2016 be a repeat of 2008?

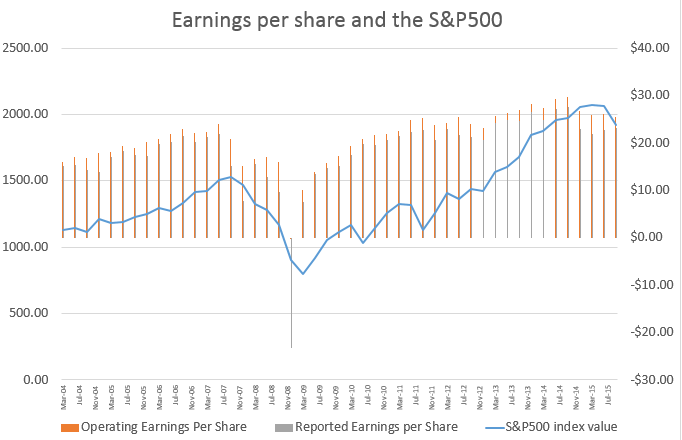

How does the current level of risky debt compare with pre-crisis levels in 2007? The simple answer is we are not anywhere near bubble proportions of 2007. As reported by Bloomberg News on 2nd February this year, credit and economic analysts at Deutsche Bank pointed out that outstanding mortgage debt (which was the epicenter of the last credit upheaval) made up 30% of total debt issuance in 2006. This is almost fifteen times the current proportion of high yield debt issuance (where risky energy loans form a substantial share) in today's credit markets. Even if energy loans do turn bad and we see a rise in defaults in high yield the fallout will not be as bad as it did in 2008.

Figure 5: While mortgage debt made up 30% of total issuance in 2006, high yield bonds stood at only 2% of total debt in 2014. (Source: Bloomberg News and Deutsche Bank)

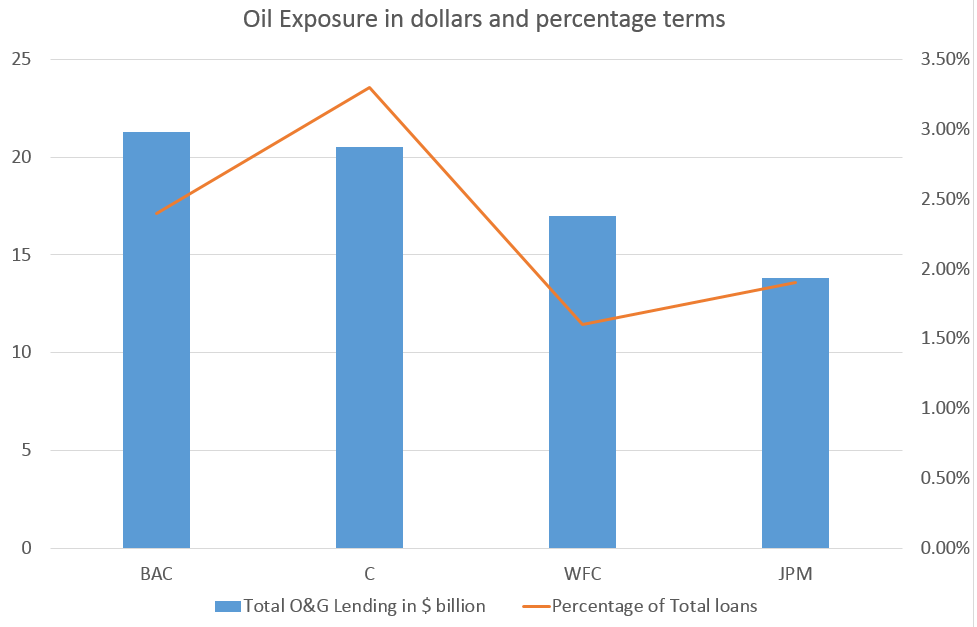

In terms of the credit exposure of the big banks to the beleaguered oil and gas sector, it has been very hard to obtain an exact number from official figures. However, estimates from banking analysts at Goldman Sachs, RBC Capital Markets have the numbers at somewhere between 2% to 4% of total loans or assets. Of all the major banks, Citigroup (NYSE:C) leads the way with 3.3% of total loans (about $20.5 billion in direct loans).

Figure 6: Exposure of the major U.S. banks to oil and gas is in the low-single digits. (Source: CNBC)

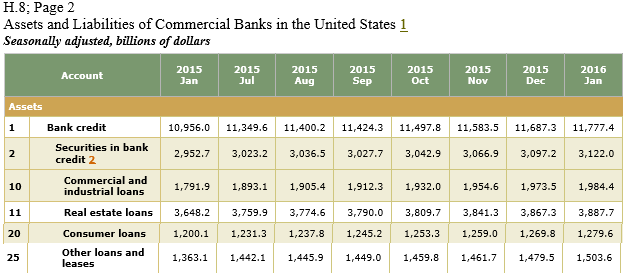

At low-single digits of 2% to 4% of banking assets, the analysts' estimates of energy credit exposure is quite consistent with the previous data from the debt markets. Put in perspective, a 2% to 4% credit exposure pales in comparison against other types of loans on the banking books. For example, real estate loans typically form around a third of bank credit while consumer loans form one tenth of bank lending. Suffice to say, a rise in default rates in the oil and gas sector may not be the powder keg that some market observers are expecting it to be.

Figure 7: Real estate and securities holdings form the largest proportion of U.S. commercial banking assets. (Source: Federal Reserve Board)

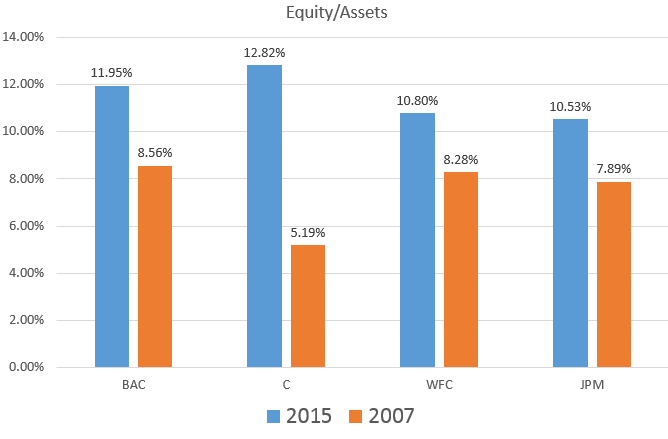

Even in the scenario that bank exposure to oil credit do exceeds the estimated range of 2% to 4%, banks have already boosted their capital levels considerably from 2008. The four biggest banks (Bank of America Corporation (NYSE:BAC), JPMorgan Chase & Co. (NYSE:JPM), Wells Fargo & Co. (NYSE:WFC) and C) are sitting on double-digit equity to assets ratio at the end of 2015. This compares with single-digit capital buffers during the pre-crisis period of 2007.

Citigroup has more than doubled its equity level from 5.19% in 2007 to 12.82% in 2015.

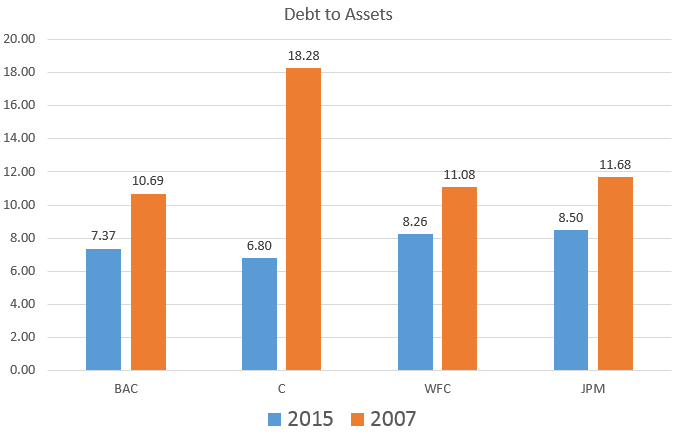

Leverage has also dropped significantly from 2007 levels. Banks like JPMorgan Chase, Wells Fargo and Bank of America have cut leverage from about 11 times in 2007 to around 7 to 8 times in 2015.

By cutting down leverage ratio, banks have minimized the gearing impact of decline in assets prices on equity value.

Figure 8: U.S. banks are better capitalized in 2016 than they were in 2008. (Source: data from DBS Vickers Research with analysis by author)

Figure 9: Debt to asset ratios in the U.S. have plunged to single digits from 2008 peaks. (Source: Data from DBS Vickers Research with analysis by author)

All in all, 2016 looks nothing like 2008. Firstly, potential trouble assets are not anywhere near the 2008 levels we saw during the subprime crisis (they are about 15 times smaller today).

Secondly, U.S. banks are in better position today than they were in 2008 to absorb these losses as they are sitting on thicker capital cushions. Looking ahead, the downturn is not expected to be as severe and financials should weather the near-term headwinds of declining oil prices and worsening energy credit quality.

Investment implications

For the equity investor, the smell of burning oil may soon be replaced by a whiff of opportunity.

During the last credit led recession, the Financials Select Sector Fund outperformed the SPDR S&P 500 ETF in the subsequent rebound as banks started to write down toxic assets and recapitalise. From the market bottom on 2nd March 2009 to 1 January 2011, the Financial Select ETF returned 124%, easily outpacing the 78% gain for the broader market index.

Figure 10: Financials outpace the market in the rebound after the last credit crisis. (Source: Yahoo Finance)

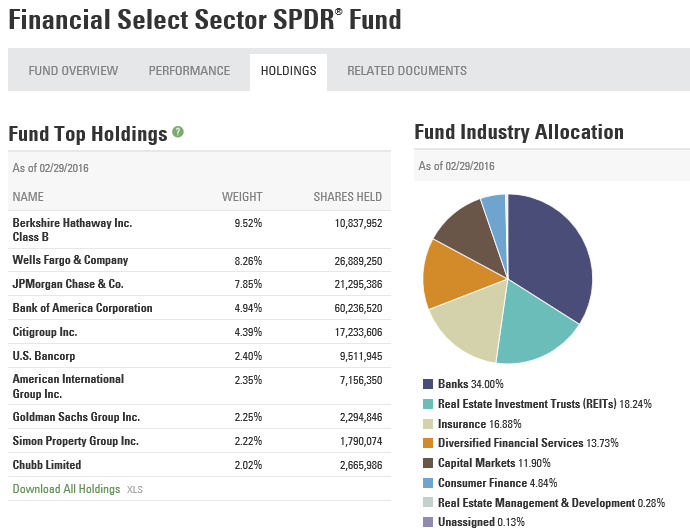

Figure 11: Banks make up almost a third of the fund. (Source: SPDRS)

Investor should consider investing in the ETF if they believe in a soft landing for banks from the energy fallout. The ETF has a 34% weighting in banks. 6 out of the top ten holdings are invested in commercial banks like Well Fargo, JPMorgan Chase, Bank of America, Citigroup and US Bancorp.

Conclusion

There is no denying that a downturn in oil related industries is already underway. This can be seen in the quarterly decline in earnings contribution of the energy sector over the past year and the weak share performance of energy companies. The question is whether the current weakness will turn into something more worrying like the financial catastrophe that we saw in 2008. Looking at the numbers, we conclude that the current downturn will not be as bad. As the economy rebalances and adjusts away from oil producing industries to oil consuming businesses (airlines, transport etc.), other sectors should see growth picking. Looking ahead, investors could see any correction in equity prices as opportunities to buy and bet on the rebound.

0 comments:

Publicar un comentario