Why Central Banks And Governments Will Both Fail In Fighting Deflation

by: Global Opportunities Analyst

Private deleveraging started in the US after the financial crisis but it didn't lead to deflation because China, and its massive credit binge, saved the world.

China is no longer the savior, but rather seems to be (for good reasons) the greatest deflationary threat in the horizon.

Governments will have to take over the job of fighting deflation from central bankers. And they will do so mostly through tax cuts for consumers.

Tax cuts for consumers will make the burden of debt easier, transferring it to governments, but that will not constrain deflation.

Risk asset prices fall in a deflationary environment, making the stock market a bad choice for investing. The situation will be worst for banks and indebted corporations.

China is no longer the savior, but rather seems to be (for good reasons) the greatest deflationary threat in the horizon.

Governments will have to take over the job of fighting deflation from central bankers. And they will do so mostly through tax cuts for consumers.

Tax cuts for consumers will make the burden of debt easier, transferring it to governments, but that will not constrain deflation.

Risk asset prices fall in a deflationary environment, making the stock market a bad choice for investing. The situation will be worst for banks and indebted corporations.

This is not necessarily a continuation, but rather an important part of the same issue I discussed in a previous article. There I argued that the Fed (followed by other central banks all around the world) has, since 1980, encouraged more private indebtedness in the economy, by making credit ever more accessible, cutting rates with the occasion of every economic slowdown. This strategy produced benign inflation for decades, associated with economic growth, all underpinned by a massive credit expansion, outpacing GDP growth significantly.

The subject of this article is to show why central bank and government attempts will fail in fighting deflation in the Developed world.

Why do we reach deflation anyway, as the decades-long struggle in Japan, and a more recent battle in Europe, suggest? It's a rather simple mathematical equation, where the formation of a credit cycle is associated with inflation, and then automatically its rolling back is supposed to be associated with deflation. But everybody seems to like the inflation that is caused by credit expansion, but they don't want to deal with paying back the debt at some point, and that is automatically going to be the reversal, hence deflation. It is important to understand how credit expansion, which has been going on for decades in the world as a whole, has been producing inflation, to also understand how its reversal is supposed to produce the opposite, deflation.

When there is an environment of credit expansion, consumers borrow money from banks, or from other sources, and spend it on buying things, usually expensive items that most people cannot afford to buy with hard cash, like houses and cars, or even vacations. Businesses use borrowed money to invest in expanding their production capacity and quality, both of which are intended to increase productivity. Both these actions, taken by consumers and businesses alike, trickle down into the economy, where existing capacity in offering goods and services cannot satisfy increased demand, therefore aggregate prices rise in goods and services so that supply meets higher demand. This phenomenon of balancing between demand and supply, through a rise in aggregate prices, is called inflation. When, for some reasons, credit expansion reverses on aggregate, meaning that consumers and businesses don't take on new debt, and older debt mature (hence credit contraction), that automatically leads to less aggregate consumer, and business, spending. And this leads to the reverse consequence, of falling prices - deflation.

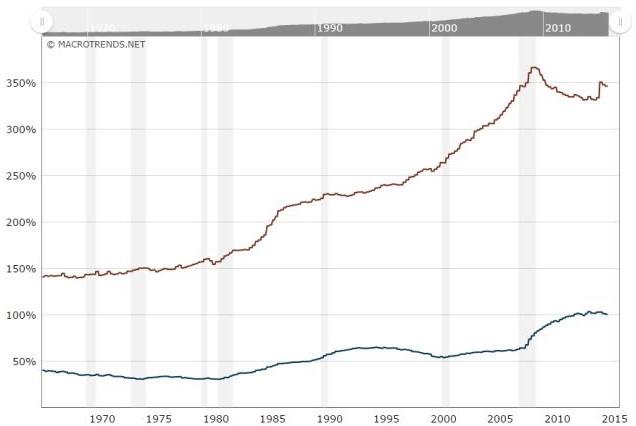

As the chart below demonstrates, almost 250% private debt to GDP is currently outstanding in the US, the remaining 100% or so being government debt.

Despite a private sector deleveraging in the US since the financial crisis, there hasn't been a fall in aggregate demand, and up until recently there has also been a reasonable amount of inflation. This can, theoretically, be the simplest debunking of the theory that deleveraging is supposed to be deflationary. But I believe the analysis is erroneous to only look at the US domestic picture. I believe that the real reason we have not seen the deflationary repercussions of the recent aggregate private deleveraging (though mild) in the US has been China (and to a smaller extent, up until 2014, also other Emerging economies). Keeping interest rates at zero, and lowering long term interest rates through QE (Quantitative Easing), have also helped, but the chart above clearly shows that private debt levels have slightly fallen. So they haven't done what they used to do up until 2008 - push private indebtedness to new highs against the GDP.

China, in order to achieve its official growth targets, embarked on the world's most aggressive credit expansion ever after the financial crisis, coupled with a strengthening currency up until 2014 (like the rest of the Emerging economies), sent a significant amount of inflationary pressures all around the world. And Chinese credit expansion has not been halted (let alone reversed) yet. What has happened though is that any credit expansion, at some point, reaches its limits, leading to gross misallocations. These misallocations, in the past, have been overcome by monetary easing (rate cuts, and more recently QE), which has (time and time again, for 30 odd years) pushed for further private indebtedness, creating additional, greater, demand.

Interest rates being at (or even below, in Europe and Japan) their limits in the Developed world, Chinese credit expansion is not finding enough additional demand, because Developed economies cannot create new credit expansion, hence more demand, any longer. Some would ask, why China's domestic credit expansion would create inflation in the rest of the world?

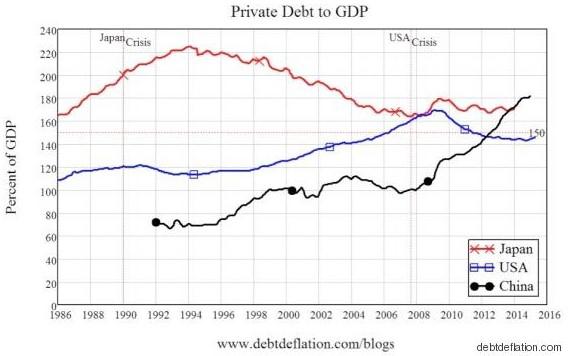

Because it has been (and is still ongoing) so massive. China used to be a rather small economy a decade ago, but it is the world's second largest economy now, and its currency has appreciated against the US dollar since 2005, a phenomenon which has been inflationary for the rest of the world - China could afford to buy more goods, assets, and services from other countries. And China's credit expansion, has been extraordinary (chart below).

The real issue here is not exactly how the chart (above) looks, but rather the numbers behind it.

According to a McKinsey report in late 2014, China's private debt to GDP levels were almost at 230% to GDP, a figure which is likely to be significantly higher now. But let's stick with this figure, and apply it to China's current GDP of about $11 trillion. According to the same McKinsey report, China's private debt to GDP was less than 120% before the financial crisis.

This equation shows an added private debt of over $20 trillion in just 7 years. This amount - greater than America's GDP - is sure to have an inflationary impact while it is being added, not just inside China, but also outside of it, especially when it has been associated with a strengthening yuan. China is still adding to its debts, but its credit expansion is no longer large enough to counter the natural deflationary tendency of capital misallocations that have been created. Credit expansion, in order to be sustained, needs to be followed by ever greater credit expansion. Otherwise, it is naturally inclined to lead to deflation.

Credit expansion, especially in the business sector, where jobs are created, leads to productivity growth, and in case demand does not outpace productivity growth, the natural tendency will be for prices to fall. The world is on the verge of another contraction in productivity because of falling prices, as misallocations (for example in commodities and energy) are abound. This happens once every few years, in various forms, leading to economic contractions (or recessions). Recent examples are 2001-2002 and 2008-2009. The world needs greater demand, which has for decades been created through credit expansion. Central bankers are no longer able to provide the world economy with additional demand through encouraging more indebtedness. It can no longer be done because interest rates cannot go below zero. Even if, theoretically, they do go below zero (as they have done in Europe and more recently in Japan), that will not encourage further credit expansion. How can you, realistically, encourage businesses to take on more debt because you take interest rates below zero? It doesn't make sense to businesses, because they still need to pay positive interest on their loans. Banks would not be willing to lend for zero interest. It would make no economic sense. Negative interest rates can only hurt banks and consumers by taking away some of their capital. It can also lead to speculation as investors would flee cash to real estate or other possibilities (gold and bitcoin for example) where they believe their capital is safe from negative interest rates.

Now that central bankers are unable to extend credit expansion, through more monetary 'easing' (meaning continuously reducing interest rates, short term and longer term), how will we counter a disastrous deflationary recession? The answer can be found in Japan, though probably in a more dramatic way, since there will no longer be the luxury Japan had in a still strong and growing export market. In the absence of monetary prowess, governments will have to replace central banks, and the easiest way to do it will be through individual income tax cuts.

This is the easiest way to reach the pockets of the ordinary consumers. This policy will be applied only after a deflationary recession will have hit, which will mean falling stocks and real estate. But I don't see how it can be applied to Europe where there is no common fiscal authority and no common debt. Europe will face a real existential question!

Most debts are linked to real estate and stock prices, one way or another. A fall in their values will be very discouraging in itself for consumers. A tax cut directed at consumers will not result in them spending the extra money. US household debt is currently above $12 trillion, of which almost 70% are in mortgages. This is an average debt per household of about $96,000, since there are almost 125 million households in the US. Would anybody realistically think that tax cuts will translate into increased consumption rather than reduced debt? Of course any tax cuts, in a recession where there is so much household debt, would facilitate debt repayment rather than create more consumption. And it would be a reasonable and wise decision.

Therefore, obviously, in the absence of an aggregate rise in consumption, deflation will continue unabated, though its repercussions will be much milder, because the number of delinquencies would be smaller as tax cuts would offer some relief for most of the indebted. Tax cuts will lead to huge government deficits, and unprecedented public debt, but that is not necessarily a major issue when interest rates are almost at zero and central bankers can keep buying government debt with printed money (QE). Japan has reached a public debt of more than 230% of GDP and its debt yields are smaller than much stronger and more fiscally conservative governments like the US and Germany! In a future of private deleveraging, and therefore deflation, fiscal profligacy will pretty much be the name of the game, and it will all, eventually, lead to currency valuations, deciding which economy is doing better or worse. Economies which will require much larger government fiscal expansion will have much weaker currencies, and those with less need of fiscal profligacy will have stronger currencies. But in the end, risk assets (real estate, stocks, corporate bonds etc.) and consumer prices will keep falling (at least in Developed economies), as there is no way of fighting it. Deflation will at some point come to an end, as governments will have taken over most of the debt from the private sector, but that has never happened in a global scale before and it is impossible to hypothesize when that will happen. It hasn't happened in Japan after more than 20 years and despite all their efforts. But Japanese private debt was bigger (to GDP) in early 1990s than what is the case now in the US and Europe. Emerging economies may see the opposite (high inflation) because of too much currency devaluation. In case governments would not act to cut taxes (which is very unlikely), deflation would be severe but it would be over relatively quickly (because of mass bankruptcies of indebted businesses) instead of being stretched for probably more than a decade, or a few, as has been the case in Japan until now. But non-intervention by governments in the face of deflation would lead to mass bankruptcies and unemployment, and nothing short of the 1930s depression.

What is to do in such an environment as an investor? I have argued for buying US Treasuries before, and I believe they still present the best choice out there. Government debt yields in developed economies (except southern Europe, as long as they have the euro) will eventually converge to zero, and this means good news for US Treasuries at this moment. Investing in risk assets has worked fine for decades, thanks to ever increasing leverage. Maybe it's time to be divesting (as opposed to investing) as the tide is going to turn, and leveraging will turn into deleveraging. This would practically mean shorting the market. Most people still believe that all central bank and government efforts against deflation will eventually succeed and that will be good news for stocks. That worked after 2008, as I explained, because of the China factor.

China is beyond loaded at this moment, and it will most likely have the opposite effect from now on. I believe that businesses most tied to debt will suffer worst. This would first of all mean banks, and then businesses with significant debts. A deflationary environment is a nightmare for debtor businesses as their products and services become cheaper, pushing down their revenues and earnings, while their debts either remain constant (best case) or become more expensive, in case they need to tap into new debt. This has already been happening in the US for more than a year, and it has, kindly, been called an earnings recession by the media. And this earnings contraction has been somewhat countered by corporations through more debt, which has gone to share buybacks and M&A (mergers and acquisitions).

The subject of this article is to show why central bank and government attempts will fail in fighting deflation in the Developed world.

Why do we reach deflation anyway, as the decades-long struggle in Japan, and a more recent battle in Europe, suggest? It's a rather simple mathematical equation, where the formation of a credit cycle is associated with inflation, and then automatically its rolling back is supposed to be associated with deflation. But everybody seems to like the inflation that is caused by credit expansion, but they don't want to deal with paying back the debt at some point, and that is automatically going to be the reversal, hence deflation. It is important to understand how credit expansion, which has been going on for decades in the world as a whole, has been producing inflation, to also understand how its reversal is supposed to produce the opposite, deflation.

When there is an environment of credit expansion, consumers borrow money from banks, or from other sources, and spend it on buying things, usually expensive items that most people cannot afford to buy with hard cash, like houses and cars, or even vacations. Businesses use borrowed money to invest in expanding their production capacity and quality, both of which are intended to increase productivity. Both these actions, taken by consumers and businesses alike, trickle down into the economy, where existing capacity in offering goods and services cannot satisfy increased demand, therefore aggregate prices rise in goods and services so that supply meets higher demand. This phenomenon of balancing between demand and supply, through a rise in aggregate prices, is called inflation. When, for some reasons, credit expansion reverses on aggregate, meaning that consumers and businesses don't take on new debt, and older debt mature (hence credit contraction), that automatically leads to less aggregate consumer, and business, spending. And this leads to the reverse consequence, of falling prices - deflation.

As the chart below demonstrates, almost 250% private debt to GDP is currently outstanding in the US, the remaining 100% or so being government debt.

Despite a private sector deleveraging in the US since the financial crisis, there hasn't been a fall in aggregate demand, and up until recently there has also been a reasonable amount of inflation. This can, theoretically, be the simplest debunking of the theory that deleveraging is supposed to be deflationary. But I believe the analysis is erroneous to only look at the US domestic picture. I believe that the real reason we have not seen the deflationary repercussions of the recent aggregate private deleveraging (though mild) in the US has been China (and to a smaller extent, up until 2014, also other Emerging economies). Keeping interest rates at zero, and lowering long term interest rates through QE (Quantitative Easing), have also helped, but the chart above clearly shows that private debt levels have slightly fallen. So they haven't done what they used to do up until 2008 - push private indebtedness to new highs against the GDP.

China, in order to achieve its official growth targets, embarked on the world's most aggressive credit expansion ever after the financial crisis, coupled with a strengthening currency up until 2014 (like the rest of the Emerging economies), sent a significant amount of inflationary pressures all around the world. And Chinese credit expansion has not been halted (let alone reversed) yet. What has happened though is that any credit expansion, at some point, reaches its limits, leading to gross misallocations. These misallocations, in the past, have been overcome by monetary easing (rate cuts, and more recently QE), which has (time and time again, for 30 odd years) pushed for further private indebtedness, creating additional, greater, demand.

Interest rates being at (or even below, in Europe and Japan) their limits in the Developed world, Chinese credit expansion is not finding enough additional demand, because Developed economies cannot create new credit expansion, hence more demand, any longer. Some would ask, why China's domestic credit expansion would create inflation in the rest of the world?

Because it has been (and is still ongoing) so massive. China used to be a rather small economy a decade ago, but it is the world's second largest economy now, and its currency has appreciated against the US dollar since 2005, a phenomenon which has been inflationary for the rest of the world - China could afford to buy more goods, assets, and services from other countries. And China's credit expansion, has been extraordinary (chart below).

The real issue here is not exactly how the chart (above) looks, but rather the numbers behind it.

According to a McKinsey report in late 2014, China's private debt to GDP levels were almost at 230% to GDP, a figure which is likely to be significantly higher now. But let's stick with this figure, and apply it to China's current GDP of about $11 trillion. According to the same McKinsey report, China's private debt to GDP was less than 120% before the financial crisis.

This equation shows an added private debt of over $20 trillion in just 7 years. This amount - greater than America's GDP - is sure to have an inflationary impact while it is being added, not just inside China, but also outside of it, especially when it has been associated with a strengthening yuan. China is still adding to its debts, but its credit expansion is no longer large enough to counter the natural deflationary tendency of capital misallocations that have been created. Credit expansion, in order to be sustained, needs to be followed by ever greater credit expansion. Otherwise, it is naturally inclined to lead to deflation.

Credit expansion, especially in the business sector, where jobs are created, leads to productivity growth, and in case demand does not outpace productivity growth, the natural tendency will be for prices to fall. The world is on the verge of another contraction in productivity because of falling prices, as misallocations (for example in commodities and energy) are abound. This happens once every few years, in various forms, leading to economic contractions (or recessions). Recent examples are 2001-2002 and 2008-2009. The world needs greater demand, which has for decades been created through credit expansion. Central bankers are no longer able to provide the world economy with additional demand through encouraging more indebtedness. It can no longer be done because interest rates cannot go below zero. Even if, theoretically, they do go below zero (as they have done in Europe and more recently in Japan), that will not encourage further credit expansion. How can you, realistically, encourage businesses to take on more debt because you take interest rates below zero? It doesn't make sense to businesses, because they still need to pay positive interest on their loans. Banks would not be willing to lend for zero interest. It would make no economic sense. Negative interest rates can only hurt banks and consumers by taking away some of their capital. It can also lead to speculation as investors would flee cash to real estate or other possibilities (gold and bitcoin for example) where they believe their capital is safe from negative interest rates.

Now that central bankers are unable to extend credit expansion, through more monetary 'easing' (meaning continuously reducing interest rates, short term and longer term), how will we counter a disastrous deflationary recession? The answer can be found in Japan, though probably in a more dramatic way, since there will no longer be the luxury Japan had in a still strong and growing export market. In the absence of monetary prowess, governments will have to replace central banks, and the easiest way to do it will be through individual income tax cuts.

This is the easiest way to reach the pockets of the ordinary consumers. This policy will be applied only after a deflationary recession will have hit, which will mean falling stocks and real estate. But I don't see how it can be applied to Europe where there is no common fiscal authority and no common debt. Europe will face a real existential question!

Most debts are linked to real estate and stock prices, one way or another. A fall in their values will be very discouraging in itself for consumers. A tax cut directed at consumers will not result in them spending the extra money. US household debt is currently above $12 trillion, of which almost 70% are in mortgages. This is an average debt per household of about $96,000, since there are almost 125 million households in the US. Would anybody realistically think that tax cuts will translate into increased consumption rather than reduced debt? Of course any tax cuts, in a recession where there is so much household debt, would facilitate debt repayment rather than create more consumption. And it would be a reasonable and wise decision.

Therefore, obviously, in the absence of an aggregate rise in consumption, deflation will continue unabated, though its repercussions will be much milder, because the number of delinquencies would be smaller as tax cuts would offer some relief for most of the indebted. Tax cuts will lead to huge government deficits, and unprecedented public debt, but that is not necessarily a major issue when interest rates are almost at zero and central bankers can keep buying government debt with printed money (QE). Japan has reached a public debt of more than 230% of GDP and its debt yields are smaller than much stronger and more fiscally conservative governments like the US and Germany! In a future of private deleveraging, and therefore deflation, fiscal profligacy will pretty much be the name of the game, and it will all, eventually, lead to currency valuations, deciding which economy is doing better or worse. Economies which will require much larger government fiscal expansion will have much weaker currencies, and those with less need of fiscal profligacy will have stronger currencies. But in the end, risk assets (real estate, stocks, corporate bonds etc.) and consumer prices will keep falling (at least in Developed economies), as there is no way of fighting it. Deflation will at some point come to an end, as governments will have taken over most of the debt from the private sector, but that has never happened in a global scale before and it is impossible to hypothesize when that will happen. It hasn't happened in Japan after more than 20 years and despite all their efforts. But Japanese private debt was bigger (to GDP) in early 1990s than what is the case now in the US and Europe. Emerging economies may see the opposite (high inflation) because of too much currency devaluation. In case governments would not act to cut taxes (which is very unlikely), deflation would be severe but it would be over relatively quickly (because of mass bankruptcies of indebted businesses) instead of being stretched for probably more than a decade, or a few, as has been the case in Japan until now. But non-intervention by governments in the face of deflation would lead to mass bankruptcies and unemployment, and nothing short of the 1930s depression.

What is to do in such an environment as an investor? I have argued for buying US Treasuries before, and I believe they still present the best choice out there. Government debt yields in developed economies (except southern Europe, as long as they have the euro) will eventually converge to zero, and this means good news for US Treasuries at this moment. Investing in risk assets has worked fine for decades, thanks to ever increasing leverage. Maybe it's time to be divesting (as opposed to investing) as the tide is going to turn, and leveraging will turn into deleveraging. This would practically mean shorting the market. Most people still believe that all central bank and government efforts against deflation will eventually succeed and that will be good news for stocks. That worked after 2008, as I explained, because of the China factor.

China is beyond loaded at this moment, and it will most likely have the opposite effect from now on. I believe that businesses most tied to debt will suffer worst. This would first of all mean banks, and then businesses with significant debts. A deflationary environment is a nightmare for debtor businesses as their products and services become cheaper, pushing down their revenues and earnings, while their debts either remain constant (best case) or become more expensive, in case they need to tap into new debt. This has already been happening in the US for more than a year, and it has, kindly, been called an earnings recession by the media. And this earnings contraction has been somewhat countered by corporations through more debt, which has gone to share buybacks and M&A (mergers and acquisitions).

0 comments:

Publicar un comentario