Inflationary Tsunami Early Warning

by: Kevin Wilson

- There are five ways to deal with a debt crisis: 1) government austerity plans; 2) private sector savings increases; 3) economic reforms; 4) currency devaluations & hyperinflation; 5) default.

- The fourth of these is important today, with over 30 countries having high inflation rates, and many nations using money printing, debt monetization, and currency devaluation as tools.

- Our concerns about deflationary waves may eventually be cast aside by the arrival of a Tsunami wave of high inflation or hyperinflation, especially if currency devaluations become disorderly.

- The fourth of these is important today, with over 30 countries having high inflation rates, and many nations using money printing, debt monetization, and currency devaluation as tools.

- Our concerns about deflationary waves may eventually be cast aside by the arrival of a Tsunami wave of high inflation or hyperinflation, especially if currency devaluations become disorderly.

I have written elsewhere about the need for leaders to face a debt crisis head-on in order to avoid an eventual catastrophe. This is important at present because the entire world has been in a debt crisis since 2007. Many countries are plagued by excessive levels of debt, yet the response of governments around the world has been to solve their debt problems by adding even more debt in vain efforts to boost demand. Indeed, an additional $57 trillion has been added to the global debt pile since Lehman Brothers failed. This has merely acted to slow down global growth, so it seems prudent to consider alternative approaches to the problem. Well-known economist Lacy Hunt, and others, have shown that the historically tested solutions to debt crises include: 1) government austerity plans; 2) massively increased private sector savings; 3) structural economic reforms; 4) currency devaluations and/or hyperinflation; and 5) default.

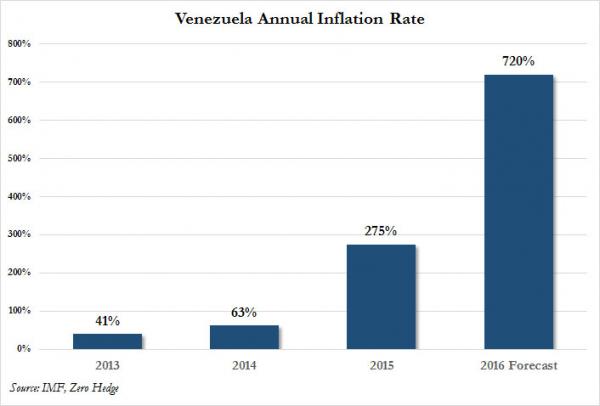

Recently the fourth of these crisis solutions came to mind again when the Financial Times reported that Venezuelan inflation will reach an astounding 720% this year. To get some perspective on this, let's compare the price of eggs on January 1, 2016 to what the price would be in three years (2019) at a compound inflation rate like the Venezuelans face, 720% per year.

Assuming we are buying organic free-range large eggs, the price for our hypothetical calculation starts at $3.99/dozen. Three years hence the price of eggs would be about $1,489.25/dozen! My guess is that political change will come to Venezuela if the inflation rate stays this high for an extended period of time.

When people in Europe worry from time to time about high inflation, many recall what happened in the 1920s, when Germany, Austria and Hungary were subjected to catastrophic hyperinflation in the aftermath of World War I. The trouble started when the costs of running the war in 1917 and 1918 were covered by increasing the supply of money. Then extremely punitive war reparations were demanded by the Allies after they defeated Germany. Germany didn't have the money, but they did have lots of printing presses, so they met the demands by printing even more money. This started an inflationary spiral as workers demanded higher wages to keep up with the inflation caused by depreciating currencies. The inflation had such a debilitating impact on society that a man named Adolph Hitler was able to exploit the situation and eventually rise to power. The rest is history.

It might be instructive to compare the present-day hypothetical Venezuelan example just discussed, which sounds pretty extreme, to one of the world standards for hyperinflation, the post-war Weimar Republic (Germany) in 1919-1923 (other examples would include Hungary in 1946 and Zimbabwe in 2008). So let's look at the price of eggs again. A dozen German eggs in 1919 (after years of already high inflation) may have cost, after converting currencies, about $0.05/dozen. But just four years later, in 1923, the cost had risen to a spectacular $821,988,182,000/dozen. Not that you could actually have found any eggs to buy, since by then nearly everyone was starving. The maximum rate of inflation on a monthly basis peaked at 29,525% (!) in Weimar Germany in October of 1923. Now that's inflation! Similar tragedies in 1946 Hungary, 1994 Yugoslavia, and 2008 Zimbabwe had peak monthly inflation rates in the billions, trillions, or even quadrillions of percent.

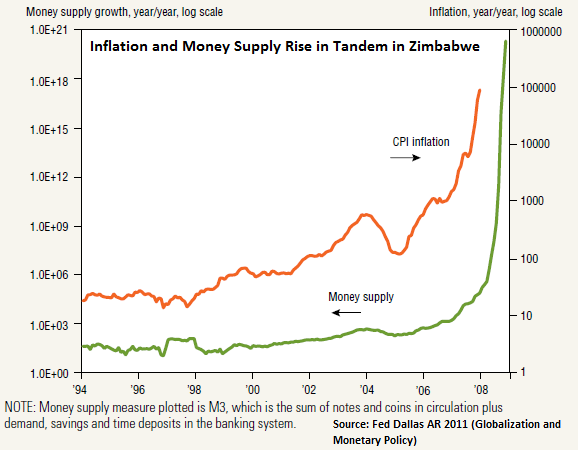

A great book on the tragic instance of devaluation and hyper-inflation in Weimar Germany was published by Adam Fergusson (When Money Dies, 2010 edition, Public Affairs, New York, 269p). He wrote about the massive shift of savers and investors to hard assets like real estate or the U.S. dollar, as everyone dumped German cash (marks) as soon as they could to avoid getting caught by currency losses. Barter became a common means of exchange as many people lost faith in the government and its currency. Debts were reduced by inflation to a tiny fraction of their original value, and even after the crisis ended, creditors never recovered more than a small fraction of their losses. If one wishes to get a feeling for what such huge inflation rates are like, it is instructive to consider the modern (2008) hyperinflation in Zimbabwe. At its peak, inflation reached an amazing 98% per day. So think about this stark fact: if you lived in Zimbabwe in 2008, got your pay check on a Friday morning and couldn't get to the bank until the next Monday, you would have lost about 70% of your pay already by the time you got to the bank.

Likewise in Hungary in July 1946, the daily rate of inflation peaked at 207%, according to Cato Institute data. So in our payday scenario, you couldn't even take a full day to get to the bank before the purchasing power of your entire paycheck was gone. The daily rate in Weimar Germany peaked at 20.87%, meaning prices were doubling every 4 days or so. This explains the stark pictures of street sweepers removing piles of cast aside money (Deutsche marks) from the curbs and gutters in Berlin that year, and also the pictures of people using old denominations of money as wallpaper. It is interesting to note that in each of the modern cases mentioned, i.e., Venezuela, Yugoslavia, and Zimbabwe, we have seen economically weak dictatorships printing money in huge quantities to support wars or other unfunded spending programs, and thus destroying their economies.

When people in the U.S. worry about high inflation from time to time, they usually recall the bad old days of the 1970s and early 1980s, when inflation averaged over 8% annually, oil prices soared, and bond investors lost money every year. But this was not really hyperinflation, which has been defined by inflation expert Phillip Cagan as inflation that exceeds 50% per month. High inflation, let alone hyperinflation, is indeed an insidious enemy, because it slowly attacks the standard of living of the middle class and the poor. And even relatively high, but not truly hyperinflation can cause a lot of damage over time. For example, inflation's acceleration in the 1970s U.S. episode just mentioned, plus its impact in the period since, calculates out to a requirement that wages would have to have risen by a factor of about 4.55 since then for workers to break even with their original buying power.

And that's assuming taxes stayed about the same! So if you made $21,000/year in 1975, a very good salary back then, you would have to make around $95,550/year now to enjoy the same lifestyle. But of course we were all much younger then, so we could probably live very cheaply compared to now. It's not the same at all when you add on another 40 years to your age. Add globalization to inflation, and you get a strong hit to household income, even with the 1970s kind of inflation. In fact, real wages have stagnated over the last 30 years, and household income has barely beaten inflation since 1975; the gains were mainly due to women entering the work force. The median income for men was actually higher in real dollar terms in 1973 than it was in 2009.

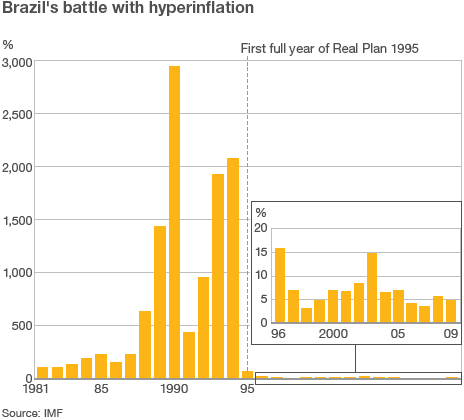

This discussion of high inflation and hyperinflation is relevant today because there have been a whole series of hyperinflation episodes around the world in the last 30 years. Vietnam saw inflation rates peak at 774%/year in 1988. Brazil saw inflation rates approaching 3,000% per year in the early 1990s. Yugoslavia's hyperinflation peaked in January of 1994 at a daily rate of 64%. Zimbabwe, as already mentioned, saw a peak inflation rate in 2008 that was so severe that their own currency was discontinued, and all trade was conducted using foreign currencies like the U.S. dollar. Finally, as mentioned above, Venezuela in 2016 is experiencing hyperinflation at 720%/year. Both high inflationary and hyperinflationary episodes are caused by familiar problems in world history; so familiar in fact that we can spot a major inflationary episode in Roman Egypt dating back to 334 AD. In that instance, inflation rose by about 17.2%/year for 58 years, raising prices by a cumulative factor of 10,000 in that time. Author David Hackett Fischer has studied inflationary waves (see his book, The Great Wave: Price Revolutions and the Rhythm of History; 1996, Oxford University Press, New York, 536p) that did great damage throughout history. For example, in medieval Europe an inflationary event in the 1320s sent the price of wheat in England, Italy and France soaring by over 300%.

Economist Milton Friedman demonstrated in his research that "inflation is everywhere a function of money supply." We can certainly see this in the data from Weimar Germany, where the correlation between the monetary base (bank reserves plus total currency in circulation) and wholesale prices was a very close one. We see much the same thing in Zimbabwe. But as most people understand, and as media reports suggest, currently we are seeing a huge deflationary wave hit the world economy, and inflation seems at first glance to be far off for most places outside of Venezuela. However, upon examining current data on global inflation rates, I was surprised to see a large number of countries with high rates. Right now annual inflation rates range between 10% and 55% for Russia, Brazil, Ukraine, Argentina, Turkey, Nigeria, Iran, Zambia, Sudan, Angola, and about 20 other countries. So perhaps the commodities decline and high debts have subdued inflation in many places, but money printing and debt monetization are also widespread in other places, it would seem. In this context global competitive devaluations are a bit like pouring gasoline on a fire, and our next problem might rather surprisingly be an inflationary tsunami washing upon the shores of the global economy.

A number of the advanced economies like Japan and the Eurozone countries have fallen so in love with government spending programs, that as a result of deficits and long-term debt burdens they have been "forced" to print money to cover their budget shortfalls. In fact, Japan has been monetizing about 70% of its annual deficit. The quasi-equivalent of money printing in the form of Quantitative Easing (QE), plus low or negative rates under ZIRP or even NIRP, plus the aforementioned debt monetizations are also collectively helping in the fight against the deflation wave, although the evidence of success here seems a little thin right now. The present round of currency devaluations is partially aimed at subduing deflationary pressures in countries like Japan and China, and in much of Europe, and also is partially aimed at boosting trade revenues. This attack on deflation should eventually work if the devaluations are severe enough, as indeed it did during the Great Depression. However, as John Mauldin and David Tepper have discussed in their recent book (Code Red, 2014, John Wiley & Sons, Hoboken, NJ, 354p), competitive currency devaluations, like the widespread ones we're seeing around the world in the last three years, are also often the eventual cause of higher inflation episodes or waves. The Fed's recent decision to raise rates may have been partially motivated by a desire to break this pattern of devaluations. This may be because the combination of money printing and devaluation is historically a harbinger of damaging waves of high inflation or hyperinflation, and the damage will be worse, the bigger and more effective the debt monetizations and currency devaluations.

In any case, I believe that once the deflationary wave trough passes in China, Japan, and a few other places, it will probably be replaced by a high inflationary, or even perhaps (in some cases) by a hyperinflationary wave crest. It will not take very long to happen if the currency devaluations become disorderly, as well they could in China or Japan. If things go badly it is possible that we could be talking about a great inflationary tsunami a lot sooner than most people would have guessed.

0 comments:

Publicar un comentario