Deutsche Bank’s unappetising cocos

Discomforting brew

Investors are reassessing yet another complicated financial instrument

WHEN governments bailed out banks during the financial crisis, they tended to insist that shareholders suffer big losses. Most bondholders, however, got off scot-free. In theory, bondholders should have lost money too—but working out just how bankrupt the banks were, apportioning the losses and risking contagion among bondholders elsewhere seemed too risky to contemplate as the financial system was seizing up.

Regulators have since pushed banks to fund their activities with less debt and more loss-absorbing capital. The simplest form of capital is equity—the money raised by selling shares or retaining profits. But trimming dividends or increasing the number of shares reduces the value of the existing ones. So bankers and regulators dreamt up a new financial instrument that would act like debt, thus sparing shareholders dilution, unless capital was urgently needed.

These instruments are called contingent convertible bonds, or “cocos”, also known as additional Tier-1 securities. In exchange for annual interest of around 6-7%, investors take on the risk that, if the going gets tough, the bank may suspend interest payments, convert the bond into equity or write it off altogether.

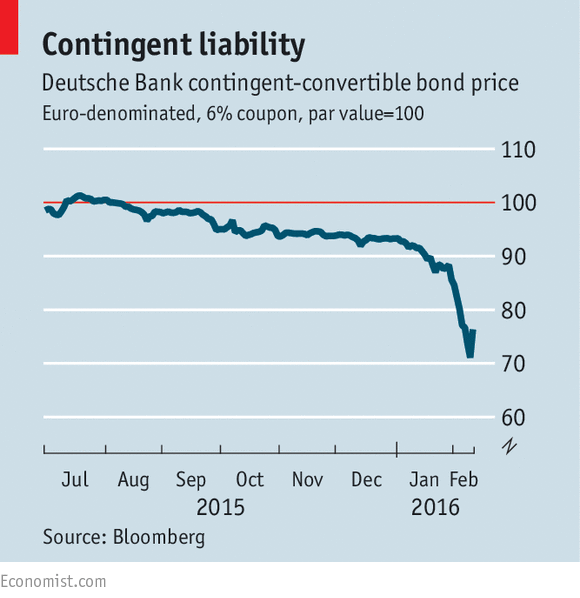

Cocos have proved popular, given how low most bond yields are: about €91 billion ($103 billion) of them have been issued since 2013. But this week analysts at CreditSights, a financial-research firm, questioned whether Deutsche Bank would have enough “available distributable items” (ADI, a subset of earnings from which interest on cocos must be paid) to cover the €350m due on its cocos next year. Their price promptly slumped to 70 cents on the euro (see chart). Other European banks’ cocos also suffered, although not quite as badly.

It is not unreasonable for investors to be nervous about Deutsche. It made a record loss last year. Its newish boss, John Cryan, has suspended the dividend for last year and this. Its big investment bank is a perennial underperformer. Many risks still lie ahead, from the costs of restructuring and regulatory infractions to potential losses on loans to energy firms.

If all this proves more expensive than imagined, it may exceed ADI, which has already been diminished by the bank’s recent losses. The problem is more acute at Deutsche than at other banks, both because it has performed especially poorly in recent years and because the German definition of ADI is narrower than in most other European countries. (Deutsche insists it will meet the payments with ease.)

The irony is that even those shunning Deutsche’s cocos accept that its cushion of capital is relatively thick, at 11%. The problem is its profits, or rather the lack of them. In other words, its cocos appear to have been poorly designed, at risk of taking money away from investors before the bank truly faces calamity. It would not be the first time a financial innovation did not work as advertised.

0 comments:

Publicar un comentario