The Fed's Extremely Dovish Hike - Key Takeaways

- After seven years, the Fed finally ended its zero-interest-rate policy.

- Behind the 25 basis points hike, there are other key takeaways to consider, including the size of the Fed's balance sheet and the upcoming reverse repurchase agreements.

- Don't assume that just because the Fed raised rates, you'll be earning more on your deposits.

Maintaining the Size of the Balance Sheet

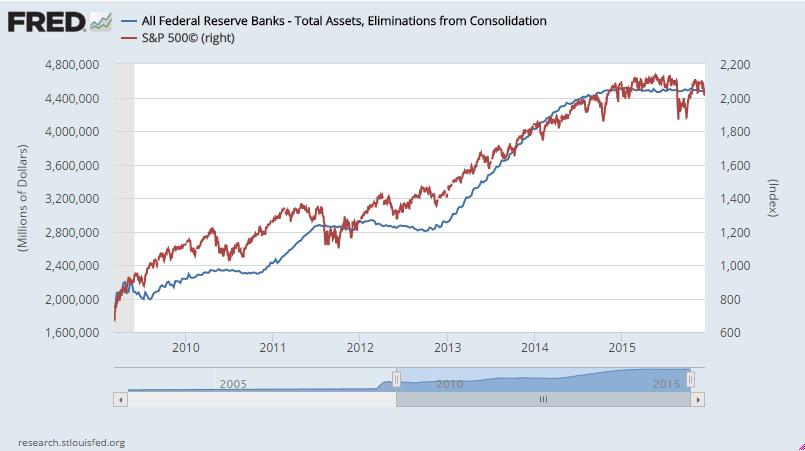

In my recent article, "These Charts Are Screaming 'Bear Market'," I showed the following chart, which I believe is key to understanding the driving force behind the 2009 to 2015 bull market.

The size of the Fed's balance sheet has been highly correlated with rising stock prices since the 2009 bottom. As the balance sheet rises, stocks tend to rise. As the balance sheet levels off, stocks seem to level off. From my perspective, the more important news than the 25 basis points hike can be found at the bottom of the Fed's press release in the following paragraph:

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee's holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions".What does this mean? By reinvesting its principal in agency and Treasuries securities, the Fed will keep its balance sheet relatively stable. This, in turn, means the Fed's balance sheet, which could easily have acted as a major headwind for stocks, will possibly be less of a headwind for the time being. I will address why I used the word "possibly" in a bit.

Moreover, the following sentence from the Fed's press release indicates further dovishness:

The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run" [emphasis added].When combining the Fed's stance on its balance sheet with its stated belief that the strength of the U.S. economy will only warrant gradual hikes going forward, Wednesday's announcement was extremely dovish. The extreme dovishness was likely necessary for Janet Yellen to be successful getting everyone on board for a rate hike.

The Fed is Absolutely Not Data Dependent

For quite some time, the Fed has told us rate hikes will depend on the evolution of economic data. In other words, the Fed would be data dependent when determining whether to hike rates.

Specifically, two things lead me to believe this was hogwash:

First, as I detailed in my recent article, "These Charts Are Screaming 'Recession'," there has been a noticeable weakening in the U.S. economy. If the data wasn't strong enough to raise the federal funds rate at any point earlier this year, then the data is absolutely not strong enough to do so now.

In particular, the Fed has shown a special focus on labor market conditions. The words "labor market" were mentioned seven times in the Fed's five paragraph press release. According to the Fed, "The Committee judges that there has been considerable improvement in labor market conditions this year," despite the fact that the Fed's own "Labor Market Conditions Index," is down notably from year-ago levels and is dangerously close to dropping below zero, something that has preceded each of the past five recessions.

Data dependency doesn't appear to be the reason for this week's rate hike. But if the data didn't warrant a hike, why did the Fed hike? I believe Janet Yellen expressed the real reason for the Fed's decision, when, during Wednesday's press conference, she said the following:

One factor that we've talked about is the desirability of having some scope to respond to an adverse shock to the economy by lowering the federal funds rate. And so, it would be nice to have a buffer in terms of having raised the federal funds rate to a certain extent to give us some meaningful scope to respond".I think the Fed is scared of what might happen if the economy were to enter a recession with rates still at the zero bound. In such a scenario, not only would the Fed lose a ton of credibility because financial market participants would see that indeed recessions and bear markets are possible with rates at zero, but the Fed would also lose its historically first line of defense against halting the negative impacts of a recession (or other adverse shock); that being a cut to the federal funds rate.

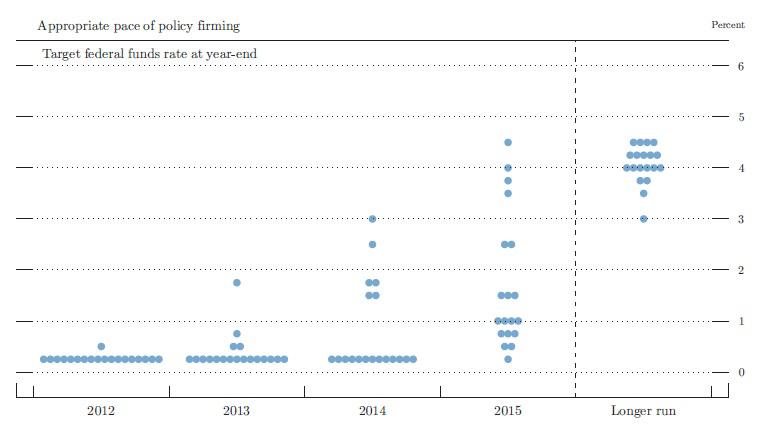

A Quick Word on the Dot Plot

I'm confident you will hear plenty about the Fed's dot plot over the coming days, while commentators debate the future path of rate hikes. Those readers wondering how credible the Fed's dot plot of fed funds projections are might be interested in a brief history lesson. First, here's a look at the Fed's dot plot on September 13, 2012:

Notice where participants thought fed funds would be at year-end 2013, year-end 2014, and shockingly, year-end 2015. Here we are at the end of 2015. Needless to say, the Fed was horrible at predicting what it itself would/should do.

Next, let's look at the dot plot on September 18, 2013:

At that time, 2015 projections, collectively, were way off. And looking ahead, I doubt those 2016 projections will, on the whole, be anywhere close to reality.

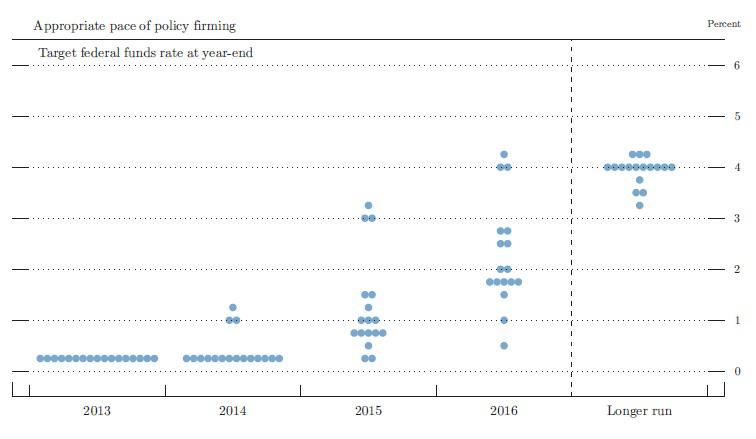

Last, let's look at the dot plot from September 17, 2014.

Just three months before the end of 2014, the majority of Fed members polled thought the federal funds rate would/should end up at 1% or higher by today. Furthermore, just 15 months ago, the overwhelmingly majority of those Fed members polled believed we would/should see rates at 2% or higher in 2016. The chances are pretty good that by this time next year, fed funds will still be a lot lower than 2%.

I don't plan to base my interest-rate assumptions on what the dot plot says.

Reverse Repurchase Agreements

I think it will take a number of weeks before financial market participants are able to fully gauge the impact of Wednesday's Fed announcement. Even though the size of the Fed's balance sheet will remain relatively flat, there is something else of importance that investors need to consider. In the Fed's "Implementation Note," also released on Wednesday, it announced that beginning December 17, "the Federal Open Market Committee directs the Desk to undertake open market operations as necessary to maintain the federal funds rate in a target range of 1/4 to 1/2 percent." This will include overnight reverse repurchase agreements, which will drain liquidity from the financial system in an amount limited "only by the value of Treasury securities held outright in the System Open Market Account that are available for such operations and by a per-counterparty limit of $30 billion per day."

As an aside, the Fed defines a reverse repurchase agreement as "a transaction in which the Desk sells a security to an eligible counterparty with an agreement to repurchase that same security at a specified price at a specific time in the future. The difference between the sale price and the repurchase price, together with the length of time between the sale and purchase, implies a rate of interest paid by the Federal Reserve on the transaction." When the Fed sells securities to its counterparties, it is draining liquidity from the financial system. How much liquidity are we talking about?

In addition to the 22 counterparties on the Fed's "Primary Dealers List," the potential size of the upcoming reverse repos made it necessary to create an expanded "Reverse Repo Counterparties List" that includes 65 counterparties. With 87 total counterparties, this means the theoretical limit for overnight repos is $2.61 trillion (87 multiplied by the $30 billion per-counterparty limit).

The exact amount of liquidity that will need to be drained from the system in order to keep rates at the Fed's target level is an open question. It could easily be measured in the hundreds of billions. Even though the Fed isn't planning to reduce its balance sheet anytime soon by permanently selling securities or letting securities mature and roll off, the Fed will be temporarily selling some of its securities during reverse repos. As the Fed notes, securities sold from the System Open Market Account (which holds assets acquired by the Fed) in reverse repos "continue to be shown as assets held by the SOMA in accordance with generally accepted accounting principles . . ." But make no mistake about it; although the Fed's assets may remain at elevated levels, the liquidity drain that will be happening could have negative consequences for the financial markets. An operation of this size is something new and we'll all just have to wait and see how things play out.

The War on Savers Is Not Over

For the past seven years, there has been an outright war against savers. One of the deflationary effects of the Fed's zero-interest-rate policy was the billions of dollars in lost interest income that millions of Americans would have earned on their deposits, and subsequently may have spent in various parts of the economy. There was a hope that once the Fed started raising rates, depositors might finally catch a break and see their rates go up. Sadly, initial indications are that this will not be the case at some of the nation's largest banks. Several banks, including JPMorgan Chase (NYSE:JPM), Wells Fargo (NYSE:WFC), PNC (NYSE:PNC), Citigroup (NYSE:C), U.S. Bancorp (NYSE:USB), and Bank of America (NYSE:BAC), among others, were quick to increase the Prime Rate they charge everyday people and small businesses on various types of loans. At the same time, CNBC reported that Wells Fargo indicated it will not be raising the deposit rate and a JPMorgan Chase spokesperson told CNBC "We won't automatically change deposit rates because they aren't tied directly to prime . . . We'll continue to monitor the market to make sure we stay competitive."

From the perspective of being a bondholder in JPMorgan, Wells Fargo, Citigroup, and Bank of America, I'm okay with this. A widening in the spread between loan rates and deposit rates is good for banks. With that said, from the perspective of being an everyday American who doesn't like being ripped off, what the banks are doing doesn't sit right. I assume the banks will be keeping a close eye on money market rates, some of which I suspect will be heading higher in the near future (and in some cases already have been). There will likely be plenty of people willing to shift their funds into money markets if banks decide not to compete on yield.

Conclusión

Wednesday's FOMC announcement was indeed a historic moment. It not only ended the zero-interest-rate policy that was a relic of the financial crisis, but it also marks the beginning of a historic liquidity-draining experiment that will play out in the weeks and months to come.

As I've mentioned before, I spent the past many months significantly de-risking my equity and high-yield bond exposure, raising cash for better opportunities on the horizon. I don't like picking up pennies in front of a potential steamroller. While it's too soon to tell if that's a steamroller coming into view, we do know that elevated asset valuations, a weakening economy, and an upcoming massive liquidity-draining experiment are reasons for elevated amounts of caution.

Good luck, and all the best in the New Year!

0 comments:

Publicar un comentario