Strong Dollar Imports Trouble for Fed

Falling import prices are stymying the Federal Reserve’s hopes for higher inflation.

By Justin Lahart

The dollar’s strength against global counterparts has helped cast a chill over the cost of imports. Photo: Kiyoshi Ota/Bloomberg News

The dollar’s strength against global counterparts has helped cast a chill over the cost of imports. Photo: Kiyoshi Ota/Bloomberg NewsFalling import prices have pushed the Federal Reserve’s goal of 2% inflation far into the future. If it raises interest rates next week, that could help push import prices even lower, and make its inflation goal even more distant.

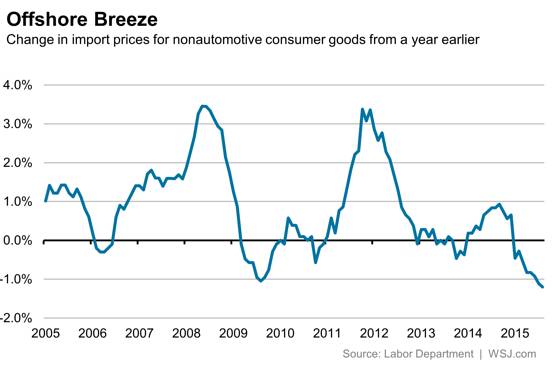

The combined effects of a strong dollar, falling commodity prices and economic weakness overseas have cast a chill on the cost of imports. The Labor Department on Thursday reported that overall import prices fell 1.8% in August from July, putting them 11.4% below their year-earlier level. Much of that owed to the plunge in crude oil prices, but prices for other items fell, too.

Nonautomotive consumer-goods prices, for example, were down 1.2% on the year, marking the largest decline the broad measure of retailers’ import costs has seen in 13 years. That drop will take some time to work its way into the prices consumers actually pay—it takes a while for imports to get trucked to store shelves, and stores aren’t exactly anxious to pass lower costs on to shoppers.

And the decline in import prices is far from finished. China’s weakening economy, and its spillover into other emerging-market economies, is worsening a supply/demand imbalance that will only be resolved by lower prices.

Then there is the dollar. It has risen nearly 20% since the middle of last year against the Fed’s broad, trade-weighted currency basket. That gain, the sharpest since the late 1990s, has yet to be fully reflected in import prices.

Contracts to buy imported goods tend to be inked well ahead of delivery, and they are often drawn up in dollars. So the prices for much of what is hitting the docks now reflect where the dollar was earlier this year.

One reason the dollar has strengthened is that the U.S. economy has been one of the better performers in the world, and therefore a better place to invest. Another is that while the Fed appears on the cusp of tightening policy, other central banks are moving to make policy even easier. That means that scant as U.S. yields are, they are rather attractive globally.

So what happens if, rather than take a pass until later this year, as many investors expect, the Fed raises its range on rates next week?

Historically a quarter-point increase in overnight rates wouldn’t matter much for currency markets. In the context of today’s ultralow rates, though, it could count a lot more, driving the dollar even higher and inflation even farther short of the Fed’s goal.

0 comments:

Publicar un comentario