WEO ANALYTICAL CHAPTER

Lower Potential Growth: A New Reality

Lower Potential Growth: A New Reality

By Patrick Blagrave and Davide Furceri

IMF Research Department

April 7, 2015IMF Research Department

- Potential output growth has declined since the global financial crisis

- Decline reflects impact of aging; lower capital and productivity growth

- Policy action required to boost productivity, foster capital growth, and offset the effects of aging

Since the onset of the global financial crisis, many economies have faced lower growth in their productive capacity, which may slow the rise of living standards in the future, according to a new study by the IMF.

The evidence presented in the study suggests that absent policy action to encourage innovation, promote investment in productive capital, and counteract the negative impetus from aging, countries will have to adjust to a new reality of lower speed limits.

Potential output: taking stock

Potential output measures a country’s productive capacity with stable inflation. It depends on the supply of two factors of production—labor and capital inputs—and how productively they are used. For potential output to grow, either the supply of these factors or productivity has to grow.

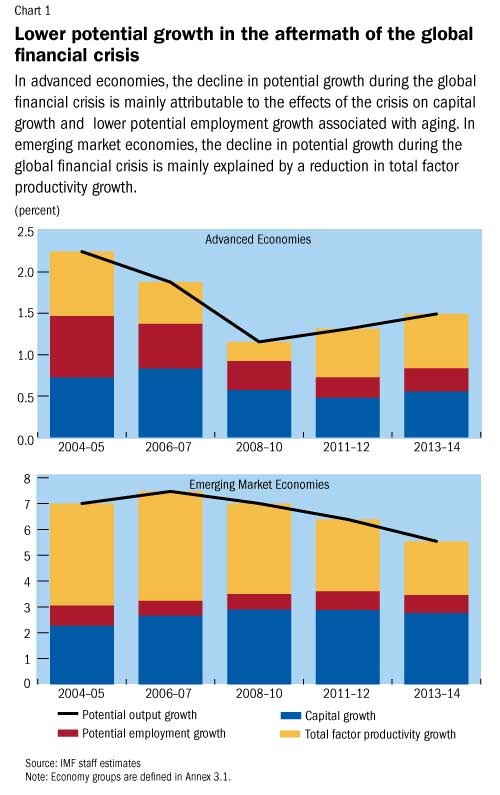

In the years since the global financial crisis many economies have witnessed slower expansions in one or more of these key components of potential output growth (see chart 1). Lower potential growth in advanced economies has been driven in roughly equal measure by slower capital accumulation and labor growth—due primarily to adverse demographics. In emerging market economies much of the decline is attributable to slower productivity growth.

Going forward: what can we expect?

As economic conditions improve and activity recovers, investment growth should pick up, fostering a gradual recovery in productive capital growth in many advanced economies.

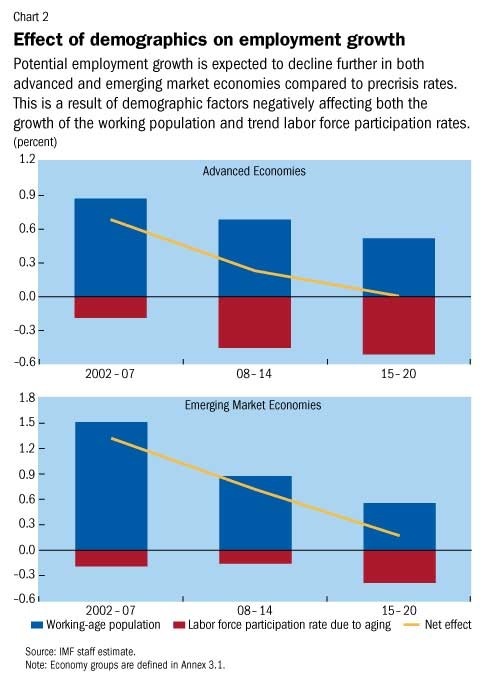

However, prospects for the labor force are grimmer. As chart 2 shows, demographic factors are likely to act as a brake on growth in many advanced and emerging market economies, as populations age and workers retire.

Productivity growth is not expected to pick up under current policies. In emerging market economies, past technological improvements and enhanced educational attainment have allowed these economies to narrow the gap between themselves and advanced economies. Although more strong growth can still be achieved from further improvements in these areas, the returns to education and innovation are unlikely to be as large as they were initially, when these economies were further from the technological frontier. This suggests weaker productivity growth in these economies in the future.

For their part, advanced economies should see productivity growth near recent rates in coming years.

Still, the rapid pace of expansion seen in the late 1990s and early 2000s—fueled by the exceptional information-communication-technology boom—is unlikely to be restored.

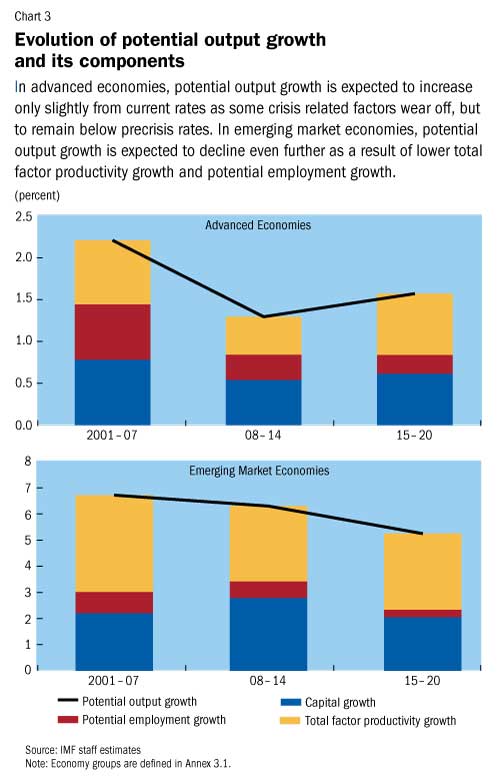

In sum, these scenarios suggest that potential growth in advanced economies is likely to remain below precrisis rates, while it is expected to decrease further in emerging market economies in the medium term (see chart 3).

These findings imply that living standards may expand more slowly in the future. In addition, fiscal sustainability will be more difficult to maintain as the tax base will grow more slowly.

Policy actions to raise the speed limit

There is still room for optimism—the future trajectory of potential output is not set in stone.

However, there is a need for action. To raise economic speed limits, policies need to encourage innovation, promote investment in productive capital, and counteract the negative impetus from aging. Although the right mix of policies will differ by country, some broad prescriptions can be made:

• Innovation can be encouraged and productivity can be enhanced with greater support for research and development—this can be achieved by strengthening patent systems and adopting well-designed tax incentives and subsidies in economies where these are low.

• Worker productivity can be increased by improving education quality and boosting secondary- and tertiary-level attainment.

• Bottlenecks that are holding back production in some emerging market economies can be eliminated through higher infrastructure spending.

• There is scope for better business conditions and improved functioning of product markets in some countries.

• Labor-force participation must be promoted, particularly among female workers in some countries, and aging workers in others—this would entail better designed tax and expenditure policies in some economies.

• Demand support through monetary and, where feasible, fiscal policy remains important in several economies to boost investment and capital growth.

0 comments:

Publicar un comentario