Dec. 12, 2014 3:29 PM ET

Summary

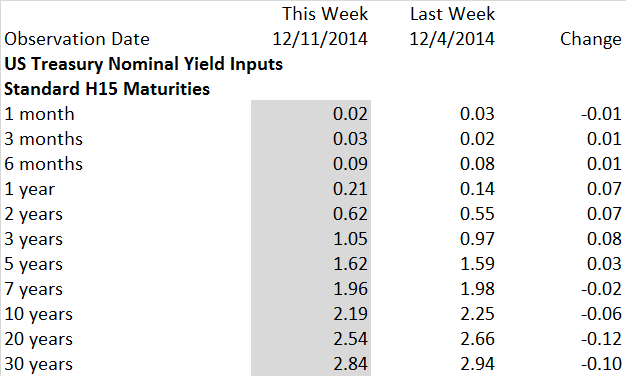

- Current Treasury yields rose 0.07% to 0.08% at 1 to 3 years and fell 0.12% and 0.10% at 20 and 30 years.

- The implied path for 1 month forward Treasury bill rates shows a peak at 2.91% in June 2021, 0.14% lower and 4 months later than implied last week.

- Forward 10-year Treasury yields in 2024 were implied at 3.00%, a major drop of 0.21% from last week.

We also present three potential scenarios consistent with the implied forecast that represent alternative paths for interest rates. This kind of multi-factor scenario generation is essential for comprehensive asset and liability management at banks, insurance firms, pension funds, and endowments. These scenarios are consistent with a multi-factor rate model benchmarked in 52 years of U.S. history, discussed below. For an update of the outlook for mortgages and the valuation of mortgage servicing rights, please see Kamakura Corporation's weekly mortgage forecast.

Here are the highlights of this week's implied forecast:

- Over the next 120 months, the maximum implied forward 1-month T-bill rate is 2.91%.

- The implied forward 1-month T-bill rate increases until reaching a peak at June 30, 2021.

- The largest increase in implied forward 1-month T-bills versus last week's forecast is 0.18% on October 31, 2015.

- The largest decrease in implied forward 1-month T-bills versus last week's forecast is -0.21% on November 30, 2024.

- The U.S. Treasury 10-year yield decreased this week by -0.06%.

- The 10-year U.S. Treasury yield is projected to reach 2.45% in 1 year, a change of 0.26% from current levels.

- Looking ahead 10 years, the 10-year U.S. Treasury yield implied by current bond prices is 3.00%, a change of 0.81% from current levels.

Note: Forward Rate Calculations are Not a Forecast

Many readers who are not familiar with forward rate calculations assume they are a forecast of interest rates with no more credibility than any other forecast. This is an error of understanding that we seek to clarify here. A forecast is a product of judgment, sometimes combined with analytics.

Forward rates, which we often label as "implied forecast," involve no judgment. Forward rates are the mechanical calculation of break-even yields such that investing in any maturity U.S. Treasury and rolling it over for 30 years will yield the same amount of cash in 30 years as investing in any other maturity. For example, if one is given the 4-week U.S. Treasury bill yield and the 13-week Treasury bill yield today, one can calculate how much the 9-week Treasury bill must yield in 4 weeks for a strategy of buying the 3-month Treasury bill or the one-month Treasury bill, followed by reinvestment in a 9-week bill, to yield the same amount of cash in 13 weeks. This calculation involves no more judgment than the calculation of the yield to maturity on a bond.

How does one use forward rates to forecast interest rates or to simulate them forward for asset and liability management or other risk management purposes? A series of authors beginning with Ho and Lee in 1985 and then followed by Heath, Jarrow, and Morton in a number of papers beginning in the late 1980s answered this question. The future path of interest rates must bear a specific link to forward rates that depends on the number of random factors driving interest rate movements and the nature of the volatility of those factors. In general, researchers agree that forward rates are biased higher than the average actual rates that will come about because long-term investors earn a risk premium for their long-term commitment of funds. The "expectations hypothesis" taught in economics for at least the last five decades postulated that, contrary to recent findings, forward rates were on average an unbiased forecast of interest rates. This is now understood to be incorrect.

Forward rates play an important role, however, in understanding where actual rates will end up.

The empirical relationship between forward rates and actual rates, using actual historical data from multiple countries, is a subject we will return to in the near future. For an introduction to the topic, we encourage readers to review recent Federal Reserve research by Swanson (2007), Rosenberg and Maurer (2008), Kim and Orphanides (2007), and Adrian, Crump, Mills and Moensch (2014). We refer readers with a technical background to the 2005 and 2008 papers by John Cochrane and Monika Piazzesi on this topic. Other excellent papers include Durham (2014), Rudebusch, Sack and Swanson (2007), and Cochrane (2007).

The Analysis

The implied forecast takes the Treasury yield curve as a given and does not attempt to reverse the impact on the curve of quantitative easing by the Federal Reserve. See Jarrow and Li (2012) and Chadha, Turner and Zampolli (2013) for estimates of the impact of quantitative easing on Treasury yield levels.

We explain the background for these calculations in the rest of this note. The implied forecast allows investors in exchange traded U.S. Treasury funds: iShares 20+ Year Treasury Bond ETF (NYSEARCA:TLT), ProShares UltraShort 20+ Year Treasury ETF (NYSEARCA:TBT), Direxion Daily 30-Year Treasury Bull 3x Shares ETF (NYSEARCA:TMF), Direxion Daily 30-Year Treasury Bear 3x Shares ETF (NYSEARCA:TMV), iShares 7-10 Year Treasury Bond ETF (NYSEARCA:IEF), iShares 1-3 Year Treasury Bond ETF (NYSEARCA:SHY); bond funds: PIMCO Total Return ETF (NYSEARCA:BOND), Vanguard Total Bond Market ETF (NYSEARCA:BND); municipal bonds: Nuveen Municipal Value Fund (NYSE:NUV) and exchange traded mortgage funds: iShares Mortgage Real Estate Capped ETF (NYSEARCA:REM) to assess likely total returns over the next 120 months.

Today's implied forecast for U.S. Treasury yields is based on the December 11, 2014 constant maturity Treasury yields that were reported by the Department of the Treasury at 4 p.m. Eastern Daylight Time December 11, 2014. The U.S. Treasury "forecast" is the implied forward coupon bearing U.S. Treasury yields derived using the maximum smoothness forward rate smoothing approach developed by Adams and van Deventer (Journal of Fixed Income, 1994) and corrected in van Deventer and Imai, Financial Risk Analytics (1996). Kamakura Corporation recently announced new research by Managing Director Robert Jarrow, which confirms that the maximum smoothness forward rate approach is consistent with the no arbitrage conditions on interest rate movements derived by Heath, Jarrow and Morton [1992]. There are other yield curve smoothing methods in common use, which violate the no arbitrage restrictions. Among the methods, which cannot meet the "no arbitrage" standard are the Svensson, Nelson-Siegel, and Merrill Lynch exponential smoothing approaches.

U.S. Treasury Yield Implied Forecast

This graph shows the projected current path for 1-month implied forward Treasury bill rates in blue. Last week's implied forward path is shown in red.

(click to enlarge)

3 Scenarios around the Forward Rate Curve

In the rest of this section, we highlight three of the infinite number of scenarios that could come about. We ensure that these scenarios are consistent with an efficient, "no arbitrage" market for U.S. Treasury as described by Heath, Jarrow and Morton (1992). We start with the current U.S. Treasury curve. We assume that a 9 factor model drives U.S. Treasury rates at maturities ranging from 3 months to 30 years. The basis for this model is the study released by Kamakura Corporation on March 5, 2014, that proves at least 9 factors are needed to accurately model quarterly rate changes.

The study makes use of more than 52 years of daily data from the U.S. Department of the Treasury and the Board of Governors of the Federal Reserve. The 9 factors used are 6 more factors than the Federal Reserve used in its 2014 Comprehensive Capital Analysis and Review stress tests and 3 more factors than required by the March 2010 version of the Basel II market risk framework (see page 12, paragraph b) of the Bank for International Settlements. We use more factors for maximum consistency with U.S. yield curve history. The parameters of the model are estimated by Kamakura Corporation using quarterly data from 1962 through September 30, 2014. Interest rate volatilities used rise as interest rates rise for 5 of the 9 factors.

The model parameters are available by subscription from Kamakura Risk Information Services. The market consensus "implied forecast" (forward rates) is shown later in this report. We now turn to three specific scenarios selected by Kamakura's analytics team for their special features.

Scenario A: A Rise to March 2015 and Then a Rate Decline

The Federal Reserve's Comprehensive Capital Analysis and Review ("CCAR") process focuses on three specific scenarios provided by the Federal Reserve. In this section of our weekly commentary, we start with the forward curve for the current date, which we explain below in our implied forecast.

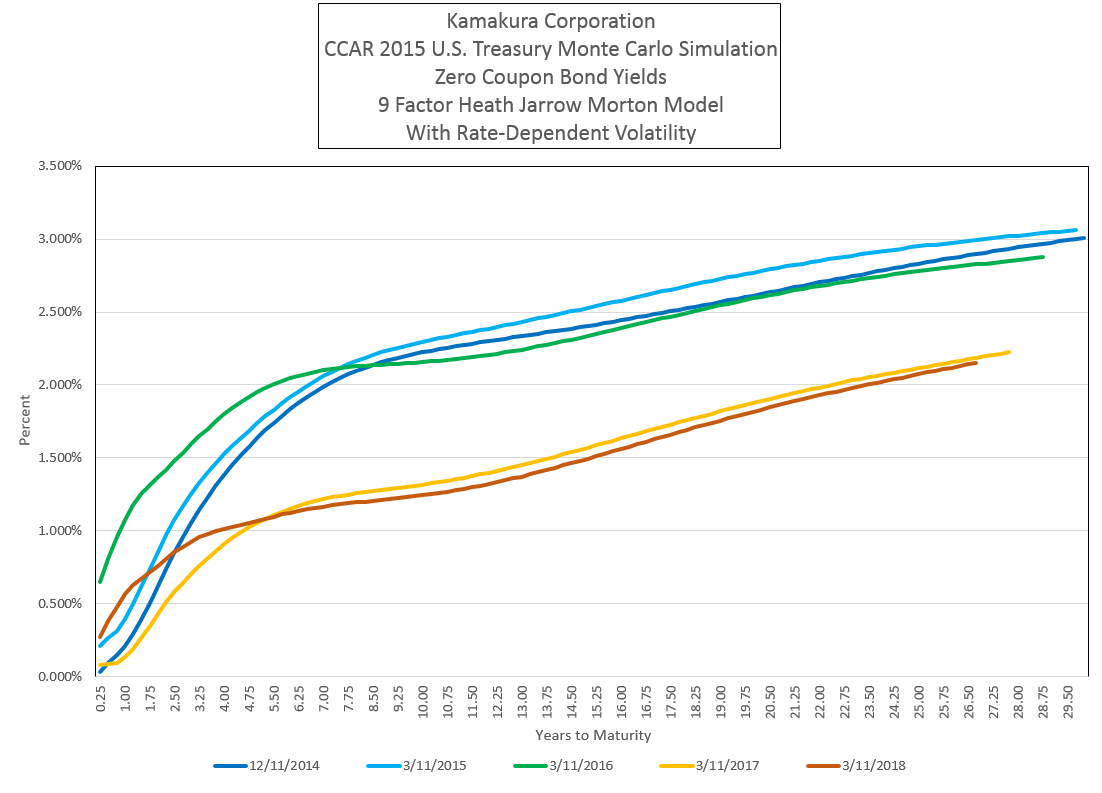

In this section of the report, we use Monte Carlo simulation in the Heath Jarrow and Morton framework using Kamakura Risk Manager. We project 13 quarters, consistent with the CCAR program, but we generate a large number of scenarios randomly. We select 3 that we hope will be of interest to readers. In the first scenario, the initial U.S. Treasury yield curve is shown in dark blue. In the first scenario, after a small rise in March 2015 (in light blue), the curve shifts up modestly on the short end of the curve in March 2016 (in green) and then shifts down in March 2017 (in yellow). In March 2018 (in red), the U.S. Treasury curve twists up slightly on the short end with long rates finishing near 2.00%.

(click to enlarge)

Scenario B: Extended Pain and Suffering

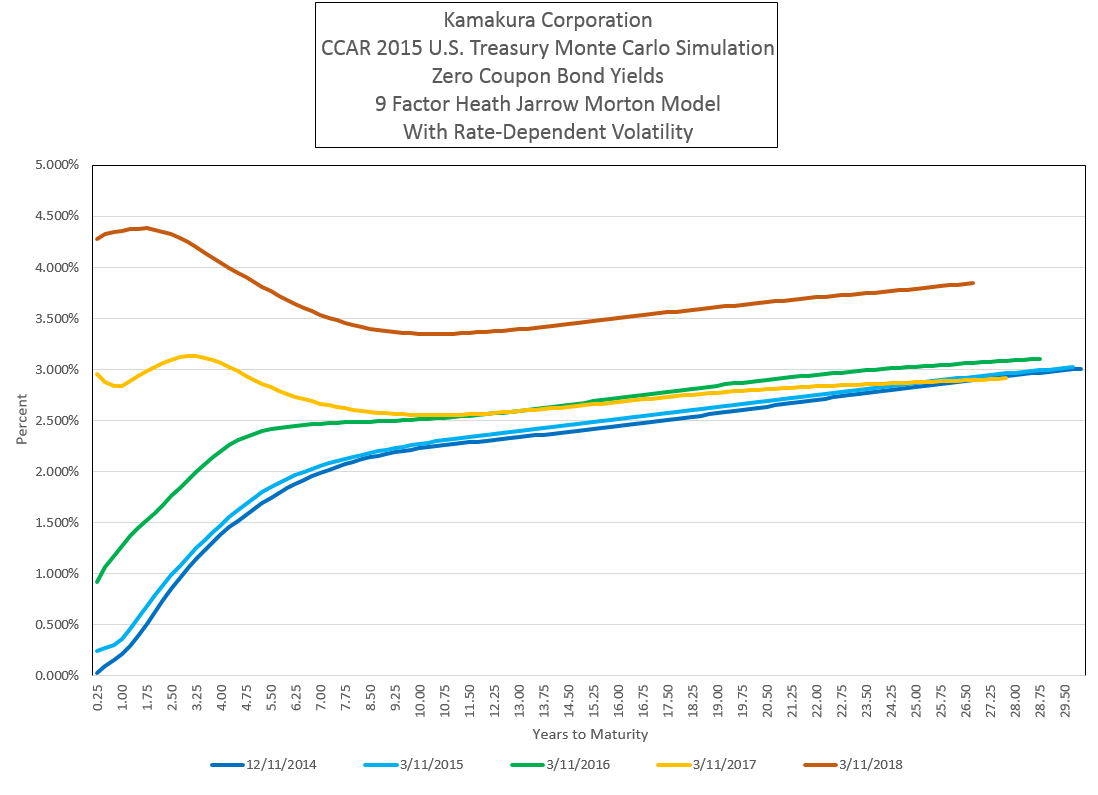

In the second scenario, the U.S. Treasury curve powers up consistently after a near zero change in yields in March 2015 (light blue). Rates then move up in March 2016 (in green), March 2017 (in yellow) and March 2018 (in red). In the Monte Carlo simulation of potential rate paths done for this note, most of the scenarios were similar to this one.

There is no respite for long-term bond holders in this scenario, with the long end of the U.S. Treasury yield curve settling near 4.50%.

(click to enlarge)

Scenario C: Long Rates Controlled by a Spike in Short-Term Rates

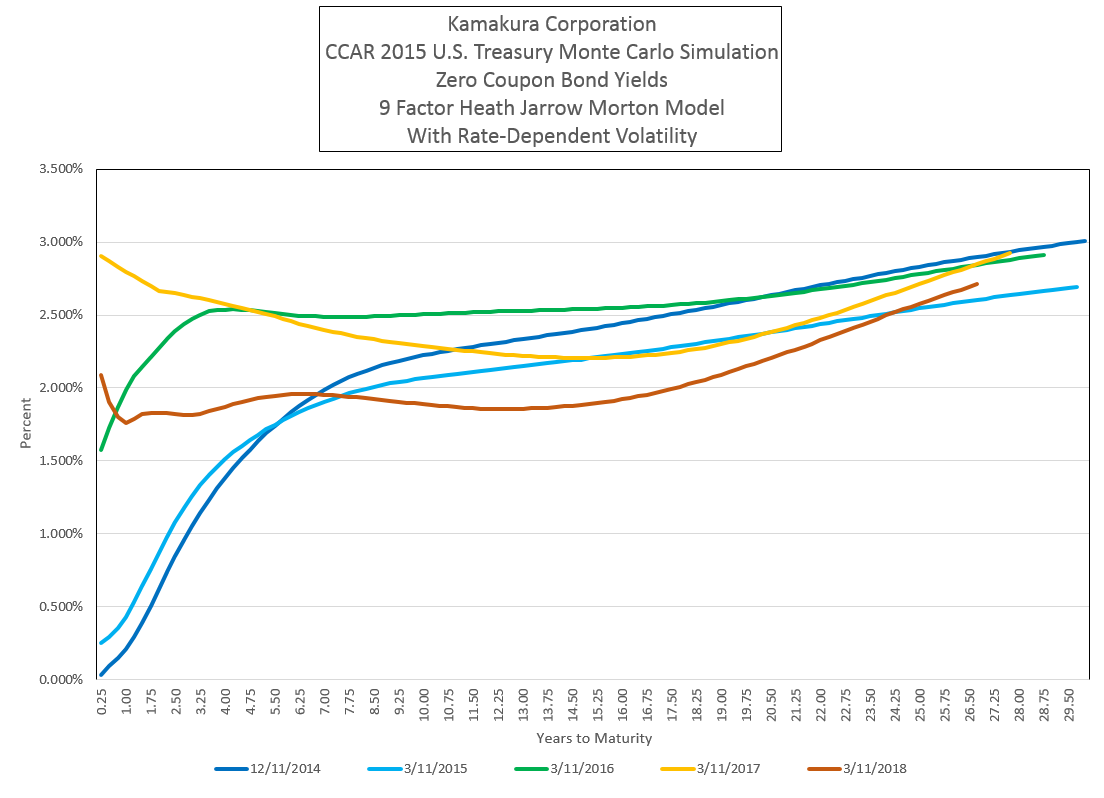

In scenario 3, the U.S. Treasury curve twists down slightly on the long end of the curve during 2015 (in light blue). In 2016, shown in green, the curve shifts up moderately with the largest increases on the short end of the curve. The curve in 2017 (in yellow) twists up on the short end of the curve and down at longer maturities. Rates shift downward in 2018 (in red), with long-term rates finishing at about 2.60%. This scenario was fairly rare in this week's Monte Carlo simulations.

(click to enlarge)

A Reminder to Readers about These Three Scenarios

All of these scenarios are plausible in that ((A)) they begin with the current U.S. Treasury curve and they are (B) simulated forward in a no arbitrage fashion ((C)) using historical U.S. Treasury volatilities. That being said, there are an infinite number of possible forward curve shapes and paths, and these three have been selected more for their drama than anything else. If one were to select only one scenario to focus on, it would be the forward rate "implied forecast" explained in more detail below.

Today's Kamakura U.S. Treasury Yield Implied Forecast

The Kamakura 10-year implied forecast of U.S. Treasury yields is based on this data from the Federal Reserve H15 statistical release:

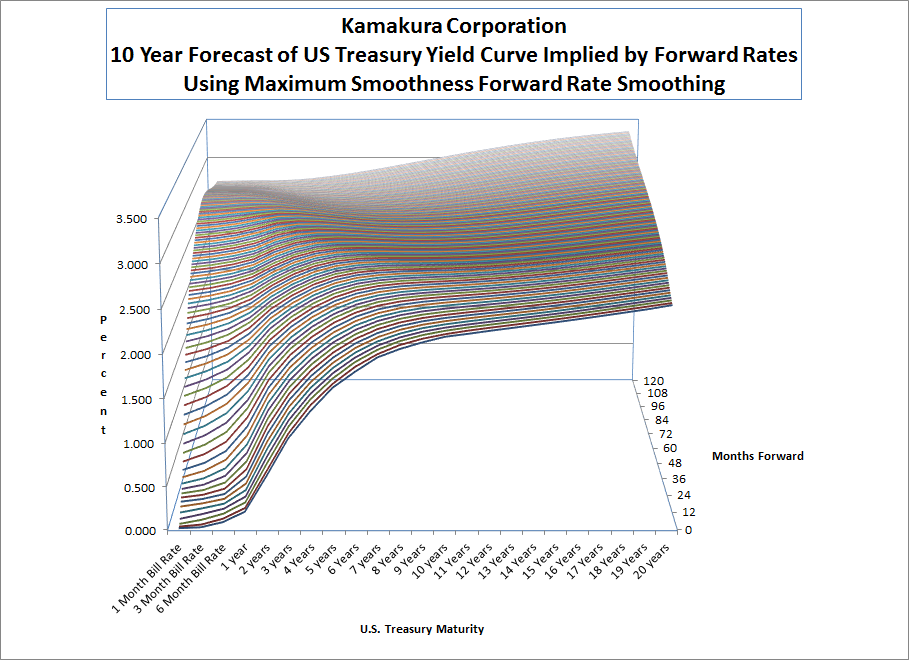

The graph below shows in 3 dimensions the implied movement of the U.S. Treasury yield curve 120 months into the future at each month end:

(click to enlarge)

These yield curve movements are consistent with the continuous forward rates and zero coupon yields implied by the U.S. Treasury coupon bearing yields above:

(click to enlarge)

In numerical terms, implied forecasts for the first 60 months of U.S. Treasury yield curves are as follows:

(click to enlarge)

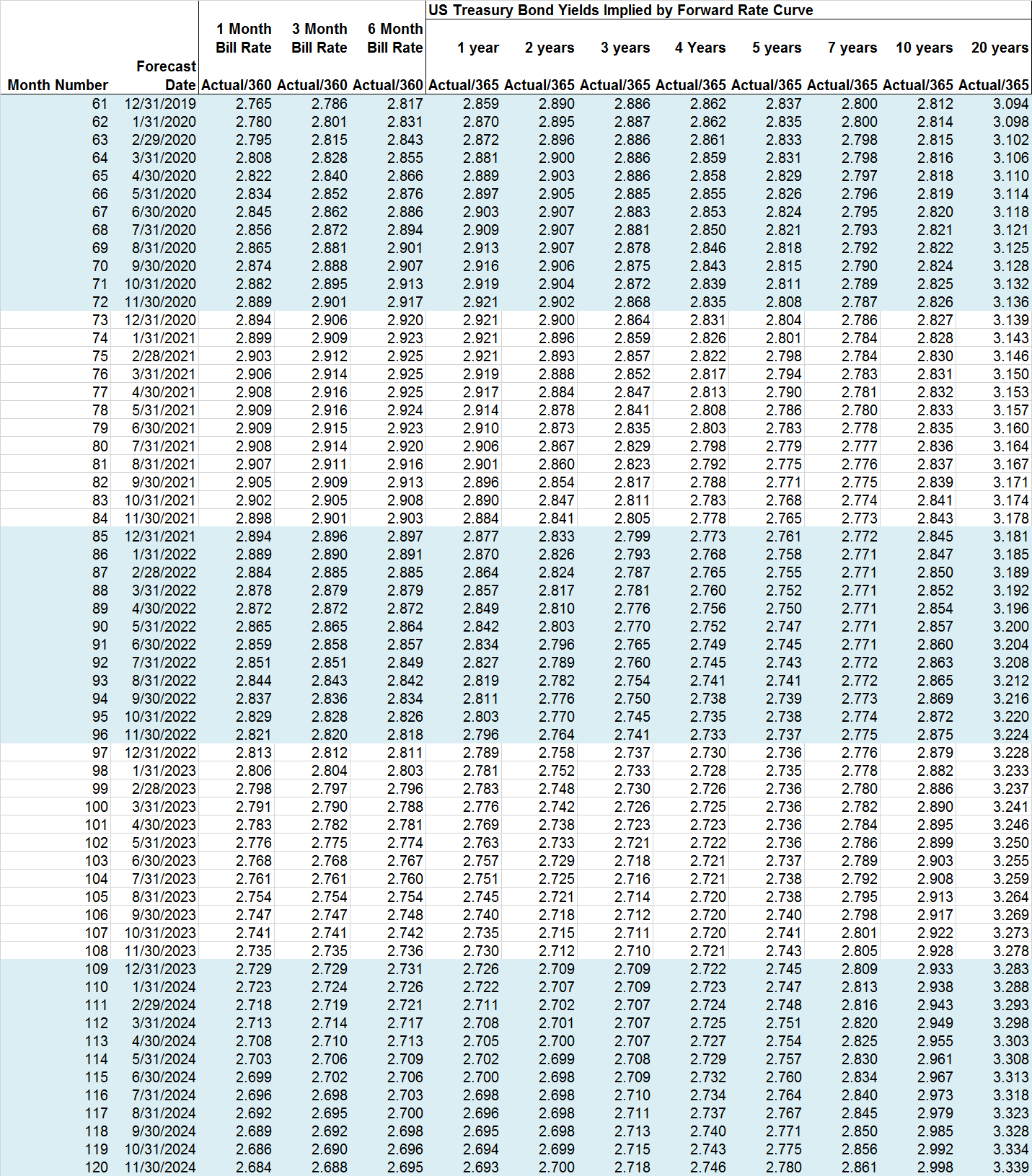

The implied forecast yields for months 61 to 120 are given here:

(click to enlarge)

Background Information on Input Data and Smoothing

The Federal Reserve H15 statistical release is the source of most of the data used in this analysis. The Kamakura approach to forward rate derivation and the maximum smoothness forward rate approach to yield curve smoothing is detailed in Chapter 5 of van Deventer, Imai and Mesler (2013).

Younger readers may not be familiar with the dramatic movements in interest rates that have occurred in modern U.S. economic history. Older readers were once familiar with these rate movements, but they may have forgotten them. Kamakura Corporation has provided a video that shows the daily movements in forward rates from 1962 through August 2011. To view the video, follow this link.

0 comments:

Publicar un comentario