Nov. 7, 2014 8:07 AM ET

The U.S. oil boom is one factor of many.

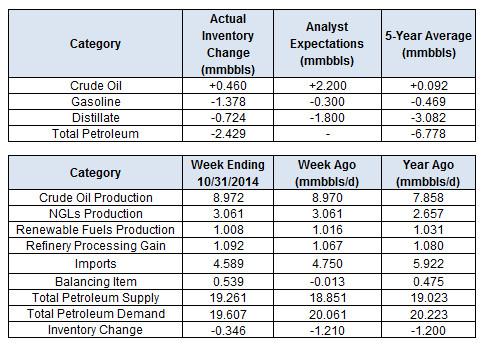

The Department of Energy reported this morning that in the week ending Oct. 31, U.S. crude oil inventories increased by 0.5 million barrels, gasoline inventories decreased by 1.4 million barrels, distillate inventories decreased by 0.7 million barrels and total petroleum inventories decreased by 2.4 million barrels.

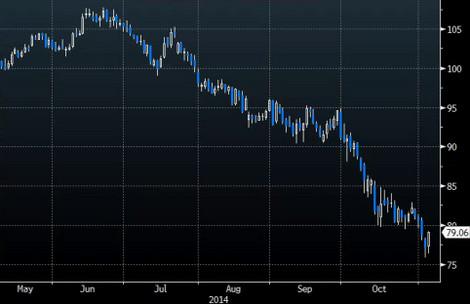

After hitting fresh multiyear lows on Tuesday, crude oil bounced back today following these latest inventory figures. Unconfirmed rumors of a pipeline explosion in Saudi Arabia also lent some support to prices.

Today's bounce notwithstanding, the big story in the oil market continues to be the "glut" in the market. Over the past several weeks, there have been countless articles talking about the oversupplied market, but very few of them explain how this glut suddenly developed between June, when Brent was trading above $115, and now, when it's trading in the low-$80's.

Some have pointed to the U.S. production boom, while others have blamed the Saudis for starting a price war. In many cases, these stories don't paint the entire picture, or worse, they are entirely inaccurate.

U.S. production has been surging for three years now. In 2012, output grew by 850,000 barrels per day; in 2013, it grew by almost 1 million barrels per day; and this year it is on track to grow close to 1.1 million barrels per day.

Yet oil prices weren't "crashing" in that three-year period. Just as we wrote above— prices were trading as high as $115 just a few months ago. Thus, we can conclude that it wasn't the U.S. oil boom in and of itself that caused oil's decline.

The U.S. boom is certainly a factor, but it's one of many that have pushed and pulled oil during the last few years. Over the past three years, there have been enormous production declines in certain oil-producing countries, which up until now had allowed U.S. production to be absorbed into the market without affecting prices.

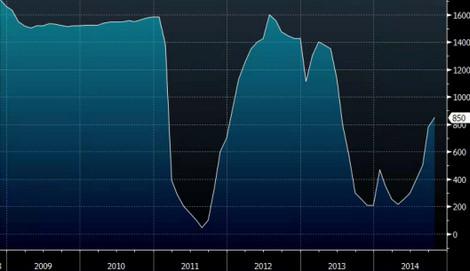

The first came in 2011, when Libya's output plunged from 1.6 million barrels per day to zero in the wake of the Arab Spring. The civil war in that year eventually led to the ousting of longtime Libyan dictator Moammar Gadhafi, and entirely shut down Libya's oil production for a period of time.

Libya Oil Production

The U.S. oil boom was just getting started at the time; thus, the Saudis were left to fill the hole in supply that had been left by Libya. The Saudis lifted their production significantly, making up for the Libyan shortfall.

Saudi Oil Production

In 2012, Libya's production bounced back as the country stabilized. But an oil-production plunge was just getting started in another country, Iran. A consequence of stringent sanctions placed on it amid a dispute over its nuclear industry, Iran's output tumbled from 3.6 million barrels per day to less than 2.6 million barrels per day in 2012.

Iran Oil Production

Who came to the rescue of the market? The U.S. As we wrote above, United States output put in its first year of big growth in 2012 when output jumped 850,000 barrels per day.

Then in 2013, the market learned how fragile post-Gadhafi Libya was when civil strife sent output plummeting again. Fortunately, the loss of 1.4 million barrels per day of output was largely made up for by U.S. producers, who increased their production by 1 million barrels per day.

Enter 2014, and the Libyan oil industry was still in chaos. Iraq was under siege by ISIS, and geopolitical risks were front and center for much of the first half of the year. Then by the middle of the year, the unexpected happened: Libya's output suddenly took off, jumping from 200,000 barrels per day to almost 900,000 barrels per day in a few short months.

At the same time, demand growth slowed significantly, with the International Energy Agency forecasting the year to have the weakest growth since 2009. Combined with another boom year for U.S. crude production to the tune of 1.1 million barrels per day, oil prices finally buckled.

Bottom Line: A confluence of factors pushed oil down rapidly during the last five months.

Likewise, it will eventually be a confluence of factors that will push oil back up again: Global demand growth, the Northern Hemisphere winter, this month's OPEC meeting, Libya's production levels, U.S. production levels and a host of other factors will influence where oil goes from here.

BRENT

WTI

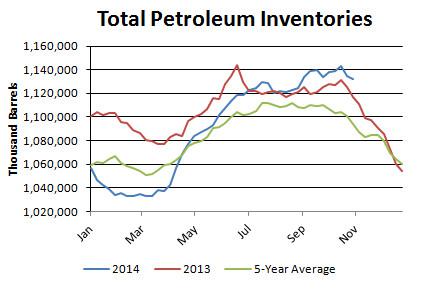

Turning to this week’s EIA inventory figures, total petroleum inventories in the U.S. fell by 2.4 mmbbl, against the five-year average of a 6.7 mmbbl decrease. In turn, inventories now have a surplus of 38.1 mmbbl, or 3.5 percent, against the five-year average.

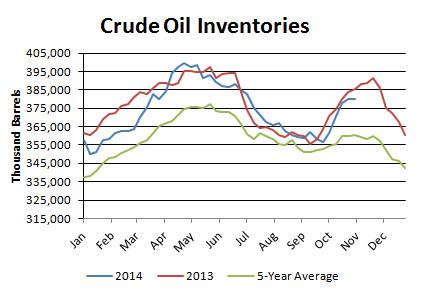

Crude oil inventories rose by 0.5 mmbbl, against the five-year average of a 0.1 mmbbl increase. In turn, the surplus in the crude category increased to 20 mmbbl, or 5.6 percent.

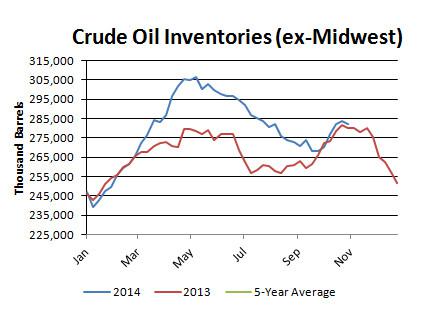

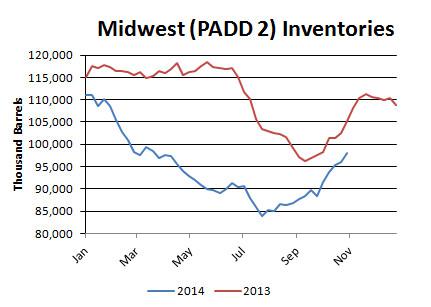

Regionally, inventories inside the Midwest rose, while inventories outside the region fell.

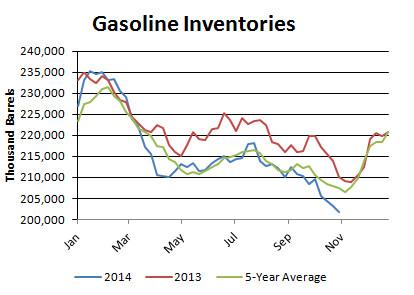

Gasoline inventories dropped by 1.4 mmbbl against the five-year average of a 0.5 mmbbl decrease.

Gasoline inventories now have a deficit of 5.8 mmbbl, or 2.8 percent. Distillate inventories fell by 0.7 mmbbl against the five-year average of a 3.1 mmbbl decrease. In turn, the distillate deficit narrowed to 20.2 mmbbl, or 14.5 percent.

Demand

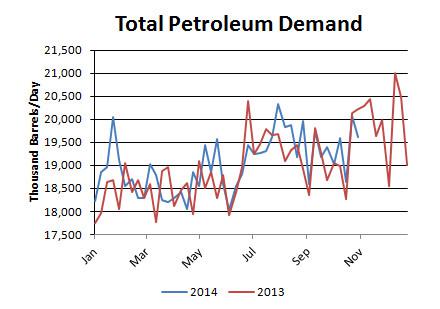

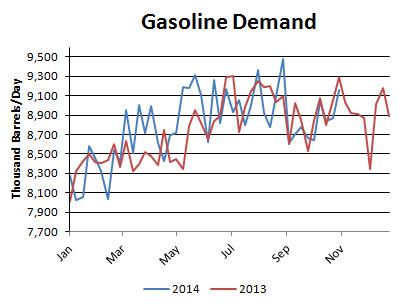

Total petroleum demand in the U.S. fell to 19.6 mmbbl/d, while gasoline demand edged up to 9.2 mmbbl/d and distillate demand retreated to 3.5 mmbbl/d. On a four-week rolling basis, total demand was up by 0.4 percent from last year. On that same basis, gasoline demand was down by 0.9 percent and distillate demand was down by 8.3 percent.

It’s worth noting that these figures may be overstated due to the EIA’s methodology for calculating demand. The administration does not distinguish between domestic demand and exports. Given that U.S. product exports (distillates, in particular) are running at record levels, U.S. oil demand seems greater than it is.

.

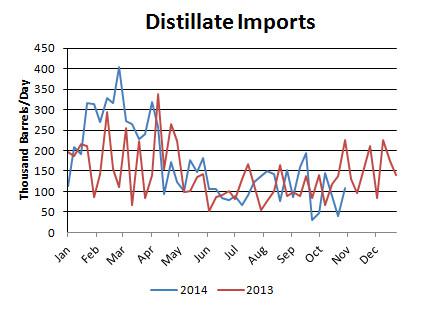

Imports

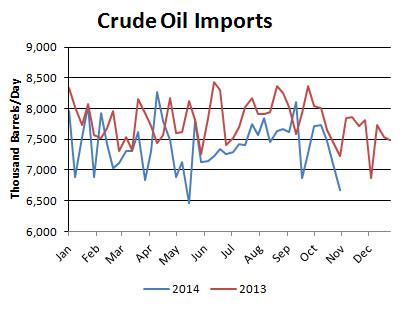

Crude oil imports fell by 0.4 mmbbl/d to 6.7 mmbbl/d. On a four-week rolling basis, imports have averaged 4.4 percent below the year-ago level.

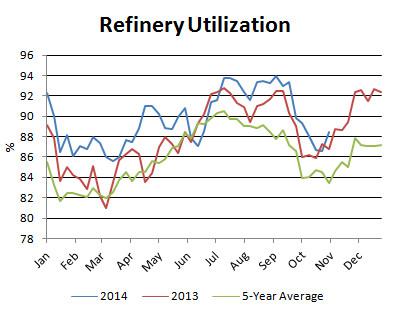

Refinery Activity

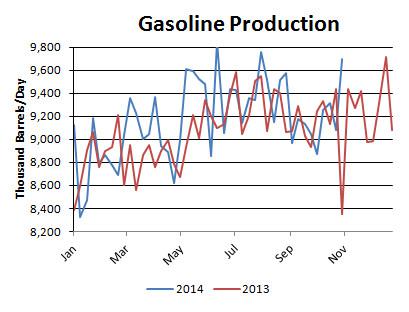

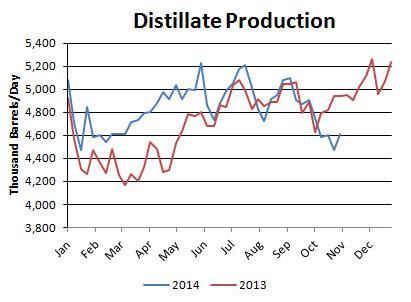

Refinery utilization ticked up from 86.6 percent to 88.4 percent. Utilization is above the year-ago level and the five-year average. Gasoline surged to 9.7 mmbbl/d, while distillate production advanced to 4.6 mmbbl/d.

Miscellaneous

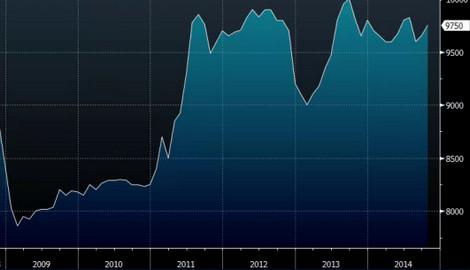

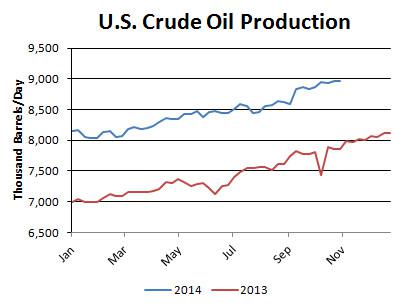

U.S. crude oil production inched up to 8.97 mmbbl/d, the highest level since April 1985. Output has been rising swiftly due to surging production in unconventional oil plays. Since the start of the year, output has averaged 1.1 mmbbl/d, or 14.6 percent, above the same period a year ago.

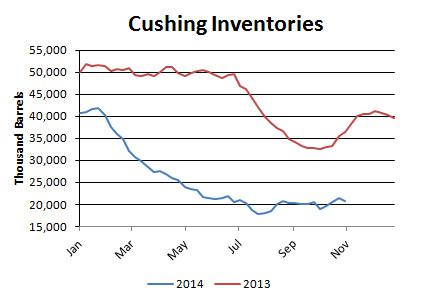

Inventories at the Nymex delivery point in Cushing, Oklahoma, fell by 0.6 million barrels to 20.8 million barrels, or 25.7 percent of the EIA’s estimate of capacity. Overall, Midwest inventories rose by 2.1 million barrels to 98.1 million barrels, or 60.8 percent of estimated storage capacity.

Front-month WTI calendar spreads are flat at -$0.00.

Front-month Brent calendar spreads remained in contango at +$0.44.

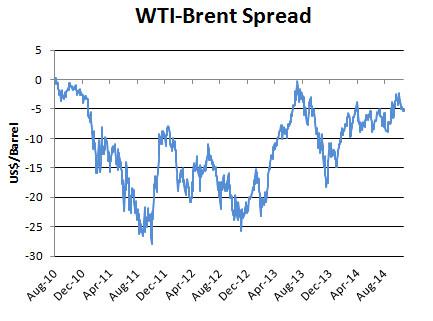

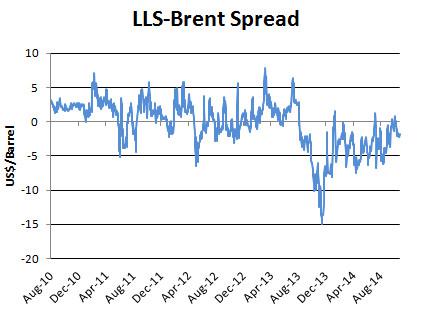

West Texas Intermediate’s discount to Brent increased week-over-week from -$4.89 to -$4.93.

WTI’s discount to Louisiana Light increased week-over-week from -$2.95 to -$3.15.

0 comments:

Publicar un comentario