Inflation and deflation: the asymmetry of risk

March 18, 2014 6:30 am

by Andrew Smithers

Comments are flying around about whether inflation or deflation is the greater risk. This is almost invariably interpreted as asking which is the most likely and therefore misses the central point. Inflation is a much greater risk – not because it is more likely but because its consequences are far worse.

Deflation has been demonised. It has been harmless or even beneficial in Japan. While I think it would hurt the eurozone, its impact would be mild and easily reversed – or it would be if German economic policy was not so obstinately foolish. Inflation poses a much more serious problem, particularly in Japan, the UK and the US.

It used to be the standard economic view that inflation fell when there were unused resources of capital and labour (known as an “output gap”). This meant stagflation was possible only for a brief period while output was falling but still above its equilibrium level.

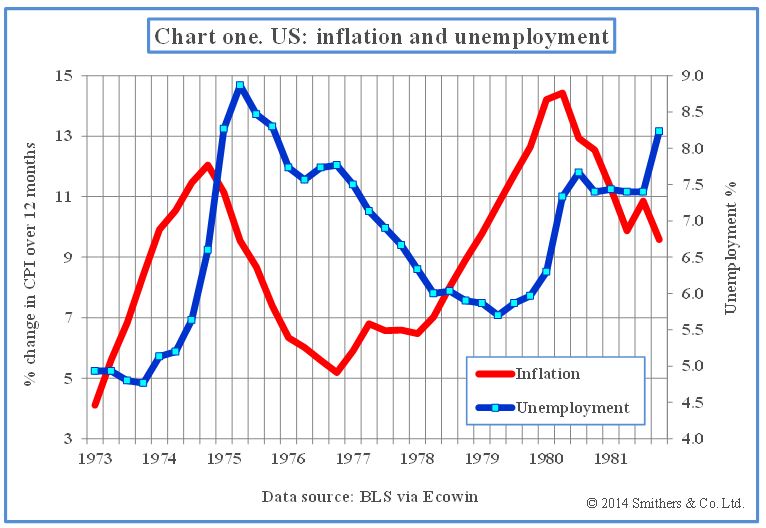

This theory was convincingly shown to be wrong in the 1970s and 1980s when stagflation was persistent. As chart one shows, unemployment rose from 5 per cent to over 8 per cent between 1973 and 1983, indicating a large amount of unused resources; and, despite this, inflation rose from 4 per cent to 7 per cent.

The theory was then revised, and it is now thought that rising inflation can occur despite persistent output gaps if inflationary expectations rise. When this happens, prices and wages are increased in expectation of higher inflation, which then of course occurs, so that inflation and its expectations form a self-supporting vicious circle. In order to bring this to a halt so that inflation falls and growth resumes, it is thought that a sharp shock is needed, in which interest rates rise much more than inflation.

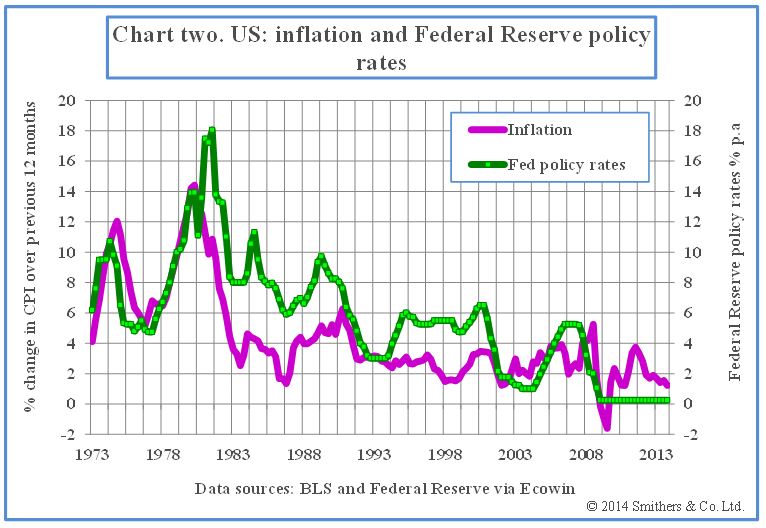

This was the medicine applied by Paul Volcker as chairman of the US Federal Reserve. Fed policy rates rose to 18 per cent in 1981 and remained well above inflation as it fell until 2002. The policy was successful – at the cost of a sharp recession with unemployment rising to almost 11 per cent in 1982.

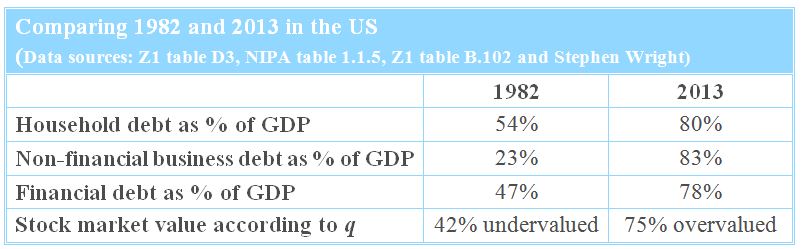

In 1982 the US economy was in far better shape to withstand a shock increase in interest rates than it is today. As the table shows, the market was undervalued rather than overvalued and debt levels were well below those of today.

I do not think that we are in much danger of either deflation or inflation in the US or the UK this year, but inflation will become a danger if the Fed and the Bank of England fail to respond adequately if unemployment continues to fall.

At the moment markets are wondering what central banks will do. They may soon need to ponder on what they should have done.

Deflation has been demonised. It has been harmless or even beneficial in Japan. While I think it would hurt the eurozone, its impact would be mild and easily reversed – or it would be if German economic policy was not so obstinately foolish. Inflation poses a much more serious problem, particularly in Japan, the UK and the US.

It used to be the standard economic view that inflation fell when there were unused resources of capital and labour (known as an “output gap”). This meant stagflation was possible only for a brief period while output was falling but still above its equilibrium level.

This theory was convincingly shown to be wrong in the 1970s and 1980s when stagflation was persistent. As chart one shows, unemployment rose from 5 per cent to over 8 per cent between 1973 and 1983, indicating a large amount of unused resources; and, despite this, inflation rose from 4 per cent to 7 per cent.

The theory was then revised, and it is now thought that rising inflation can occur despite persistent output gaps if inflationary expectations rise. When this happens, prices and wages are increased in expectation of higher inflation, which then of course occurs, so that inflation and its expectations form a self-supporting vicious circle. In order to bring this to a halt so that inflation falls and growth resumes, it is thought that a sharp shock is needed, in which interest rates rise much more than inflation.

This was the medicine applied by Paul Volcker as chairman of the US Federal Reserve. Fed policy rates rose to 18 per cent in 1981 and remained well above inflation as it fell until 2002. The policy was successful – at the cost of a sharp recession with unemployment rising to almost 11 per cent in 1982.

In 1982 the US economy was in far better shape to withstand a shock increase in interest rates than it is today. As the table shows, the market was undervalued rather than overvalued and debt levels were well below those of today.

I do not think that we are in much danger of either deflation or inflation in the US or the UK this year, but inflation will become a danger if the Fed and the Bank of England fail to respond adequately if unemployment continues to fall.

At the moment markets are wondering what central banks will do. They may soon need to ponder on what they should have done.

0 comments:

Publicar un comentario