Nothing But Bad Choices

By John Mauldin

Sep 14, 2013

It is hard to imagine a more stupid or more dangerous way of making decisions than by putting those decisions in the hands of people who pay no price for being wrong.

– Thomas Sowell

With a few exceptions here and there, crises in government funding don't simply arrive on the doorstep unannounced. Their progress toward the eventual Bang! moment is there for all the world to see. What final misdeed triggers the ultimate phase of the crisis is less predictable, but the root cause is almost always the same: debt. And whether that debt is actually borrowed or is merely promised to the populace, when the market becomes worried that the ability of the government to fund its promises is suspect, then the end is near. Last week we began a series on what I think is an impending crisis in the unfunded pension liabilities of state and local governments in the United States.

To talk about the situation using the word crisis can seem a little hyperbolic. The problems are distributed throughout the country, yet not every city or state has significant unfunded pension liabilities. And even those that do can muddle through for very long time before a smoldering problem explodes into an actual crisis. Think Detroit. You could see the crisis building for years and years in the media before it finally reached the breaking point. And Detroit was not the first city to go bankrupt, though it has been the largest. But unless significant action is taken to alleviate the problem of debt, we are going to see even larger cities and then whole states enter a crisis period. And as we will see from the data, we are not talking insignificant states. This week we continue our series on the unfunded liabilities of states and cities. Note: this letter will print a little longer than most, as there are lots of charts and graphs.

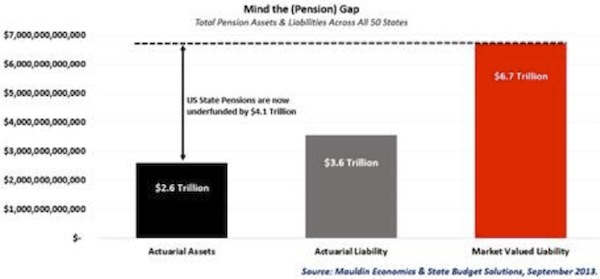

As we discussed in last week's letter on state pensions, official estimates of accrued liabilities understate funding shortfalls by conveniently assuming unrealistic investment returns into perpetuity. While official estimates report state-level unfunded liabilities across all 50 states at only $1 trillion today, the unfunded liability burden jumps to over $4 trillion if we discount those liabilities at more reasonable expected rates of return.

.

In case you were wondering, the $4.1 trillion funding shortfall includes only state-run pensions, meaning that funding gaps at local levels of government are not included. We went to great lengths this past week to calculate the total pension gap at both state and local levels across all fifty states, but we were told the data does not exist – at least not in one place.

Many cities and counties invest their funds with state pension plans rather than managing them separately, but the best estimate I could get was that if you included all the separately managed city and county pensions, it might increase the total amount by anywhere from 10 to 20%.

Even without another $500 billion to $1 trillion in unfunded pension liabilities, the implications of this gaping hole in the available pension research are truly mind-blowing, considering that, in extreme cases such as we are seeing in Detroit, local unfunded liabilities may become obligations of the states for purely political reasons. So we are stuck looking at the problem from a state-run-pension perspective, knowing that the actual shortfall could be even larger. If anyone knows of better sources for this data, I would really appreciate hearing about them.

The Aggregate or the Particular?

It may be tempting to look at aggregate pension shortfalls at the national level, but these shortfalls really amount to a state-by-state issue that will ultimately force troubled states to (1) increase taxes, (2) cut public services, and/or (3) reduce retirement benefits for current and already retired public employees. Cities and counties like Detroit (or Chicago?) that manage their own pensions and are underfunded will confront the same set of choices.

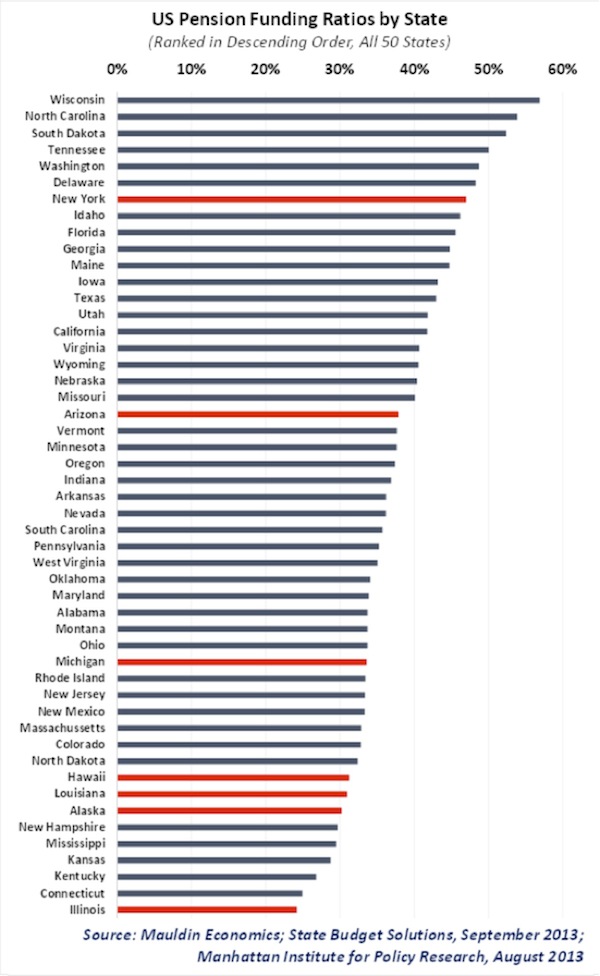

Making matters even more complicated, not all states can legally cut public employee retirement benefits. Illinois, Alaska, Louisiana, Hawaii, Michigan, Arizona, and New York (shown in red below) all have clauses in their state constitutions that protect public employee defined-benefit pension plans. While most states can reduce pensions to address their budget deficits, these seven must first amend their state constitutions. As you can see, several of these states are at the bottom of the pack in terms of funding ratios, but Illinois is the most vulnerable. (Funding ratios use the more conservative model suggested by Moody's and GASB, as we talked about last week.)

At only 24% funded, according to Moody's new methodology, Illinois is the single-most underfunded state in the union – the worst of an entire basket of bad apples. This week will focus primarily on Illinois, but we will cast our eye around the country in coming weeks.

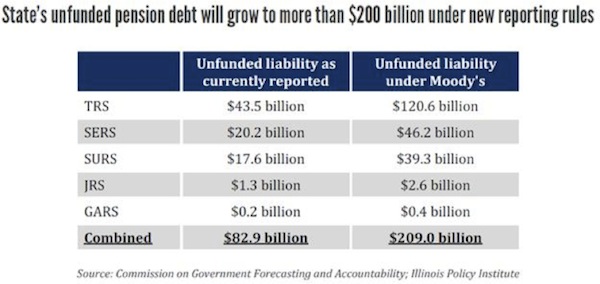

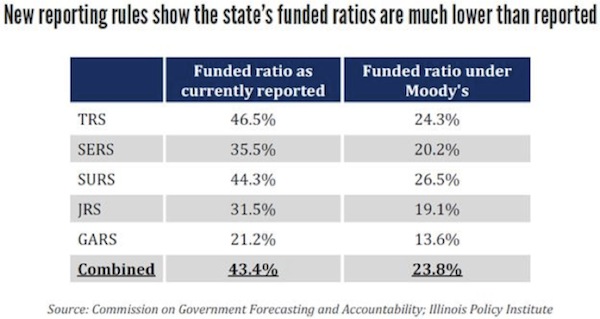

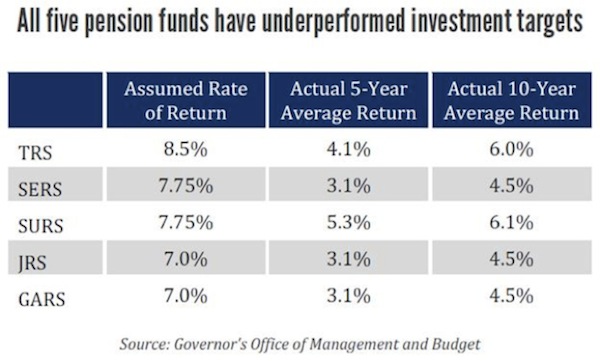

The state of Illinois's five state-level pensions (TRS, SERS, SURS, JRS, & GARS) report current accrued liabilities at $146 billion, but the state has set aside only $63 billion to cover future benefits. According to these official estimates (which are already a year old), the $83 billion shortfall in unfunded liabilities leaves the state’s pensions only 43% funded, on average. Unfortunately, the real numbers are far worse.

According to Moody's new methodology, which discounts future liabilities using the more reasonable rate of return on high-grade corporate bonds (about 4% today), current accrued liabilities tally to more like $272 billion. These figures drop the official 43% funding ratio to only 24%.

.

.

Official estimates of accrued liabilities understate funding shortfalls by assuming unrealistic investment returns into perpetuity. Over the past five- and ten-year periods, the five Illinois state pensions have discounted (underreported) their future liabilities by assuming rates of return between 7.0% and 8.5%. Every one of the state pension plans has significantly underperformed its return goals; and as we demonstrated last week, the next decade may be even more difficult from a returns perspective. Expecting more than an average of 4% nominal returns in the coming decade, given today's starting point, requires a large dollop of optimism.

When you look at the plans' five-year returns, note that these funds had the benefit of a 140% US bull market over the last four years, and their ten-year returns had the benefit of two bull markets and just one bear market (though it was a savage one).

.

The Illinois Policy Institute estimates the state pensions would need to earn a compound annual return of 19% from now through 2045 to make up the funding gap, while the markets may offer no more than 4% through the mid-2020s. Not even David Swensen at Yale can generate that kind of alpha. To reach their expected returns in a low-return environment, investment managers of these pensions would need to deliver 300 to 450 basis points of alpha, which would place them among the finest asset allocators in the world. Their recent track record suggests otherwise.

I seem to remember that it was only a few years ago that I was writing that pension funding shortfalls in Illinois were a mere $50 billion. The plans' continued lackluster performance has now made the problem much worse, and any additional underperformance will lead to even larger funding shortfalls.

Nothing But Bad Choices

To ease their shortfall, Illinois is going to have to find an additional $82 billion over the next ten years, if you believe their optimistic return projections. The more realistic projection suggests they will need to find $210 billion. That works out to $8-$10 billion a year for the next ten years. Of course, every year they continue to underfund and underperform makes that number bigger, but let's be charitable and assume the problem won't get worse. Let's analyze what these numbers mean.

Illinois is projecting approximately $35 billion of revenue for fiscal year 2014. Of this, 74% comes from individual income taxes (45%), sales taxes (21%), and corporate taxes (8%). The state of Illinois increased individual and business income tax rates in January 2011 to their current levels. These tax rates are set to roll back in January 2015 unless lawmakers vote to make them permanent. The first line below is individual, and the second line is business income tax rates.

Pre-January 2011 Tax Rates Current Tax Rates Planned Tax Rates (After January 15 Drop)

3% 5% 3.85%

4.3% 7% 5.25%

Having to vote to make already high tax rates permanent will make it difficult to then vote for even higher taxes (or at least one would think so).

Let me quote directly from Gov. Pat Quinn's speech when he delivered the 2014 fiscal year budget.

But this is also an honest budget that reflects our fiscal challenges … pays down the backlog of bills … and addresses funds that have been under-appropriated for too long. There are no gimmicks or fake numbers in this budget. This budget holds the line on discretionary spending, while fully meeting our skyrocketing pension obligations.

Inaction on comprehensive pension reform has left our state with less revenue for our most important priorities. Without pension reform, within two years, Illinois will be spending more on public pensions than on education. As I said to you a year ago, our state cannot continue on this path. Pension reform is hard. But we've done hard things before.

Maybe it's something in the water that makes Illinois politicians really good with rhetoric, but their math is a little hard for this Texas country boy to get his head around. The governor talks about a hard-fought agreement that saves $900 million over three years on pensions, but I look at this budget and can't seem to find the part about fully funding skyrocketing pension obligations.

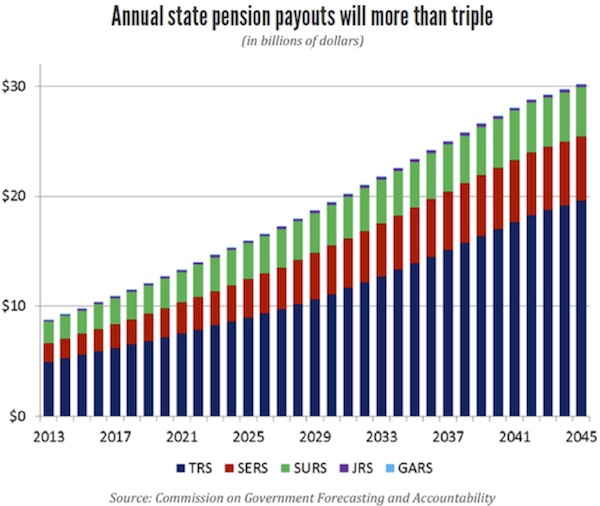

Pension contributions are planned to increase by $929 million, from $5.1 billion in FY2013 to $6.0 billion in FY2014. This falls short of the annual pension payout by $2 billion, meaning that unfunded liabilities will get worse every year until there is a fix. This shortfall could become a massive problem over time if the state government cannot significantly increase revenues to cover at least the growing annual payouts (or cut spending on public services or restructure pension liabilities). The state of Illinois projects that annual pension payouts will increase from $8 billion today to around $15 billion by 2022, to $20 billion by 2030, and to $30 billion by 2045. That is a total of $632 billion for pension benefits between now and 2045. For which the state of Illinois has set aside something like 10% of that total. How could anything possibly go wrong?

If the state were to increase individual income tax rates to cover these outlays, we would expect to see individual income tax rates rise from the current 5% to 12.5% by 2045. The longer Illinois waits to increase pension contributions, the bigger the unfunded liabilities will be and the higher tax rates will need to climb to make up for the shortfall. It may be painful to face the funding shortfall today, but the cost will balloon to enormous proportions in just a few years if lawmakers delay.

Note again that the Illinois state constitution does not allow the state to reduce pension benefits. I will grant the governor this: looking at the budget, there have been significant cuts in many areas of spending. But the "easy" work has been done. While pension contributions made up roughly 6% of operating expenditures in 2008, they account for 19% today. That number will grow dramatically if left unchecked. Looks like we are already starting to see the fallout from recent education cuts.

Going back to the original proposition, the state of Illinois needs to find an additional $20 billion a year to adequately fund its future pension obligations, or it is going to be digging an ever deeper hole every year. But where do you find an extra $20 billion a year in a $35 billion budget? This is the sort of situation that is typically described by politicians as "somebody else's problem," but to our children it will be their problema.

Promises Made, Promises Broken

There are other states besides Illinois that have significant unfunded pension liabilities. As this letter is already getting a little longish, I will leave you with just a taste of what we will cover next week. There are several ways besides the absolute numbers that you can look at unfunded liabilities. You could divide the total liabilities by the number of people in the state, giving you the debt on a per capita basis. In a fascinating report, a group called State Budget Solutions did that work for us. Quoting:

The states with the largest unfunded liability per person are Alaska ($32,425), Ohio ($24,893), Illinois ($22,294), Connecticut ($21,378) and New Mexico ($20,530). On the other hand, the states with the smallest unfunded liability per person are Tennessee ($5,676), Indiana ($6,581), North Carolina ($6,874), Nebraska ($7,212) and Arizona ($7,688).

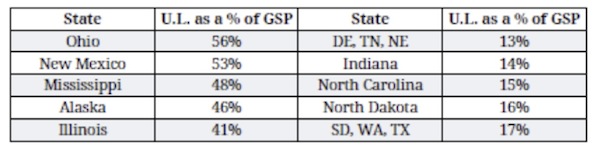

Another way to look at the debt problem is as a percentage of each state's gross state product, similar to the national GDP. That breaks down as follows:

Yes, there are states worse than Illinois, depending on how you view the data. Next week we'll get into this a little deeper.

I would like to invite those of my readers who have done the research on their particular city, county, or state to send me their data. If we get enough, we'll create one larger data set and post it.

Unfunded liabilities have the potential to become just as big a problem as subprime credit or European sovereign debt. The problems are mounting, and while in most areas they can be dealt with today, the longer the solutions are put off, the less possible they will be.

Either taxpayers will have to pay more, or benefits will have to be changed, or other services that people expect from local governments will have to be severely curtailed. That is the range of choices.

None of them will sit well. One group in Illinois proposes, as a partial solution, to freeze all cost-of-living adjustments for current retirees, to abandon defined-benefit plans for current employees in favor of defined-contribution plans, to raise the retirement age, and to take other drastic steps.

Last year a number of liberal cities in California, including San Jose and San Diego, voted to alter their pension plans rather than increase taxes. There comes a time when taxpayers simply say "No more!" On the other side of that equation are people who worked all their lives in expectation of a specific pension payout when they retired. To them a deal is a deal.

There is no surer way to upset me personally than not to live up to a deal that has been agreed upon. The anger of government employees when threatened with the loss of their benefits is something I can readily understand. But I also get the plight of taxpayers who see political favors bought and sold using their money. And I get more than merely frustrated with politicians who pile financial commitments on the shoulders of our children so that they themselves don't have to figure out how to pay for them. I think most people feel the same way about these matters, but here are no good solutions.

Ask Detroit. They put off the hard decisions, and now they're in bankruptcy court. The bankruptcy manager has threatened retirees with a far larger cut in their pensions than they might have negotiated a few years ago. City services have been cut, roads go unrepaired, most of the streetlights don't work, and there is not nearly enough money to cover fire and police services. That's what happens when you don't make the hard choices today. They become tomorrow's bad choices and next year's disastrous choices.

Ask Greece.

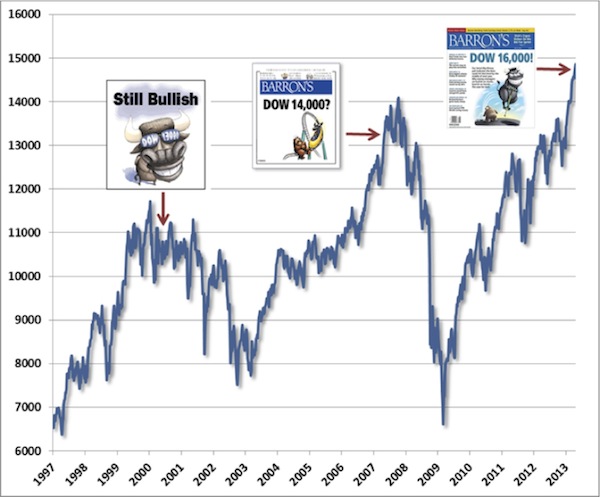

The Bull's in Charge

Last week I participated in a great webinar, "How Long Can the Bull Run? A Discussion on Long/Short Equity," with members of the investment team at Altegris. We engaged in a robust discussion on the equity markets and provided a much-needed perspective on the role that a long/short equity strategy can play in a well-diversified portfolio. We talked about some strategic moves investors can make now, whether their long-term outlook is bullish or bearish. My old friend Matt Osborne, one of the founding partners of Altegris, inserted a recent cover from Barron's magazine into his PowerPoint presentation. I am sure I saw a little mischief in his eyes, and I'm pretty sure he did it just to tweak me. I had just outlined a rather cautionary viewpoint, laying out the case that hedging at this point might prove useful, and Matt thought he should remind me that the consensus is still quite bullish. I thought a very interesting discussion ensued. "The Bull's in Charge!" indeed.

.

I was reminded of a recent graph from my friend John Hussman, which features three other Barron's covers. Some would say a Barron's cover like these is an invitation to the gods of the market to have a good laugh. I, however, am of the belief that these deities have no sense of humor whatsoever. Be that as it may, here is John's graph. I'll let you note the dates.

.

Your inspired by all the entrepreneurial spirit I saw analyst,

John Mauldin

Copyright 2013 John Mauldin. All Rights Reserved.

0 comments:

Publicar un comentario