by: AllAboutAlpha

June 03, 2010

If there was one result from the “flash crash” that sent the world’s financial markets into a screaming tizzy, it was renewed focus on electronic trading systems, ETSs for short, and their perceived negative impact on trading activity, liquidity and transparency and broader financial market stability.

The connotation that the world’s biggest stock exchange could somehow implode with the press of an execute button prompted us to take a second closer look at an April report from New York-based consultancy Investment Technology Group (ITG) focused on dark pools in Europe.

To be clear, a dark pool isn’t just a hole in the ground with a lot of water. A dark pool in trading and execution terms is a type of ATS (Alternative Trading System) that does not display quotations to the public – in other words, the bid and ask price are kept in the dark. They have grown in popularity over the past few years, particularly for alternative investment managers looking to shop around and get a one up on price — and the competition.

Being awhile since taking a gander into the dark pool, so to speak, we decided to whet our appetite and take the plunge in analyzing ITG’s report, called “Alternative Trading Systems in Europe – Trading Performance by European Venues Post-MiFID,” (the full report can be requested by contacting ITG) which was pulled together from a sampling of trading activity in Europe spanning primary exchanges, dark pools and displayed alternative venues over the first three quarters of 2009.

Of particular note was that, despite broader concerns about electronic trading and fears that a single click can bring down global financial markets, trading in ATSs, dark pools in particular, continues to grow in popularity and has actually helped foster greater liquidity, more diversity and, perhaps surprisingly, more cost-effective ways for hedge funds and others to trade securities.

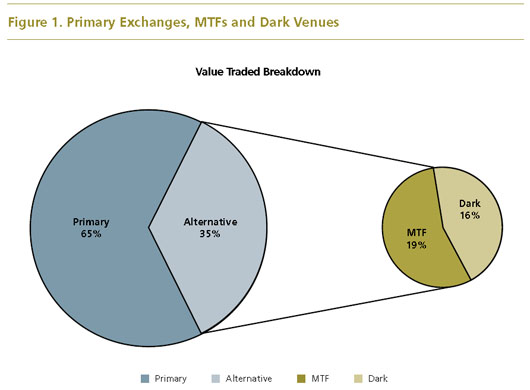

Indeed, according to the report, which was compiled from data culled by research consultancies Tabb Group and Aite Group, as much as 22% of total European equity volume is now executed through ATSs, most of which are registered as multilateral trading facilities. The sampling analyzed some 5.6 million trades in Europe over the nine-month period (see chart below for a value-traded breakdown of primary exchanges, MTFs and Dark Venues).

(TO ENLARGE CLICK ON : http://static.seekingalpha.com/uploads/2010/6/3/saupload_itg2.jpg)

{kind=link}

Not only have ATSs lowered the played field and contributed positively to overall liquidity, they have also made it cheaper for hedge funds and other traders to buy and sell stocks – 71% cheaper than incumbent domestic exchanges and 43% cheaper than multilateral trading facilities (MTFs), according to ITG. Cost savings are even more pronounced when trading small-cap and mid-cap stocks.

What’s more the risk of slippage – the difference between estimated transaction costs and the costs actually paid – is far greater in primary markets than in dark pools. The report also found that greater participation in dark venues versus “lit” markets resulted in higher basis-point cost savings. (see chart below from the report illustrating distribution of performance by venue type).

(TO ENLARGE CLICK ON : (http://static.seekingalpha.com/uploads/2010/6/3/saupload_itg1.jpg)

{kind=link}

In particular, the trend was most evident for orders that accounted for between 25-50% average daily volume (ADV), where dark pools were found to offer over 60 bps “in added value”, compared to under 10 bps for orders between 1-5% ADV.

The report cautions against increased regulatory oversight for dark pools, noting that shedding light on dark pool transactions could decrease interest in utilizing them, hence stifling best execution and other positives.

We at AllAboutAlpha.com are more than willing to bet a candle or a flashlight that more calls for increased scrutiny of various trading markets and systems have come into play since the flash crash occurred, including from the US Securities and Exchange Commission.

While not ones to ever advocate being in the dark about anything, there are certainly benefits that ATSs bring to the table. One can hope the US sees the virtues that MiFID has brought to the Europe trading scene, and not let a momentary “flash” blindly obscure the continued growth of electronic trading and diversity in America.

0 comments:

Publicar un comentario